PERSONAL FINANCIAL PLANNING

FIN533

INDIVIDUAL ASSIGNMENT

Prepared by:

NURUL FATIHAH BINTI MOHD BAHARI

2019219618

BA2432P

Prepared for:

MISS NUR HANISAH BINTI MOHAMAD RAZALI

Date of Submission:

17th December 2020

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

finance individual project in faculty business mgt

Typology: Papers

1 / 18

This page cannot be seen from the preview

Don't miss anything!

a) Biodata of the family

b) Monthly Expenses

c) Balance Sheet

d) Cash Flow

e) Ratios

f) Income Tax

g) Comment and advices

h) References

he bought a motorcycle which is a Yamaha Y15 and there is still loan balance left that need to

be paid.

Last but not least, the relationship between myself and Mr. Mohd Bahari is that he is my

own father. Though he is my father, it is not easy to convince him to participate in my

assignment project. Thus, I am so glad that he accepted my request to interview him about his

financial status and become his financial planner.

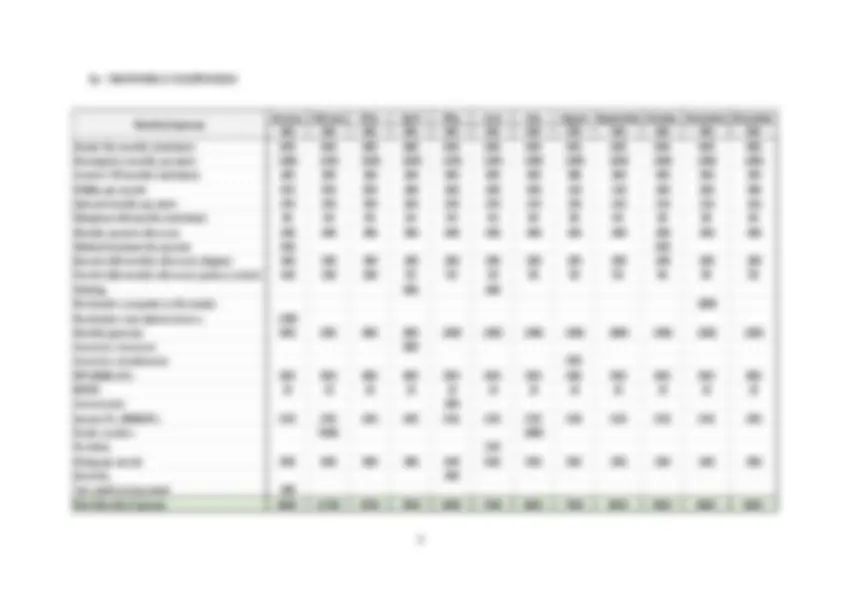

January February Mac April May June July August September October November December

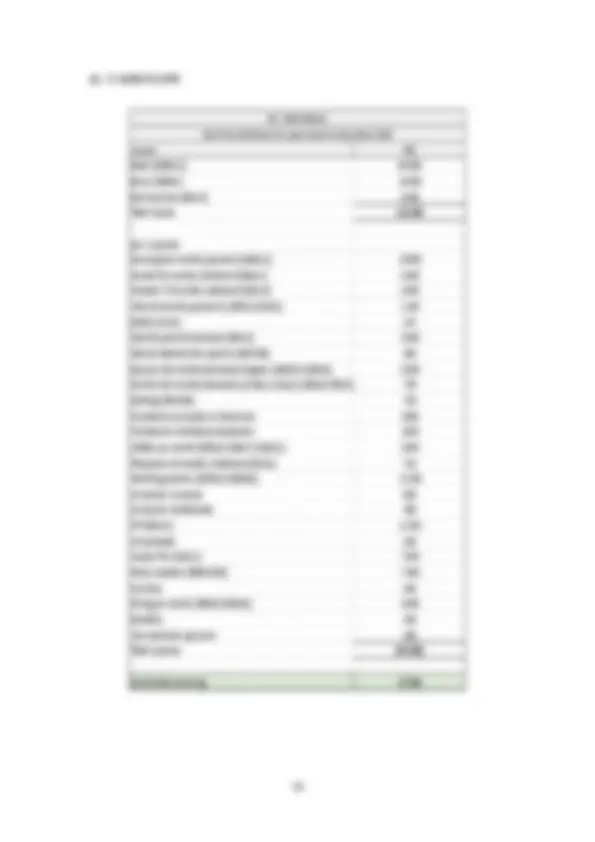

c) BALANCE SHEET

Assets RM RM Liabilities RM RM Liquid Assets Current Liabilities Cash in hand 2 000 Credit card 3 000 Balance in saving account 6 000 Total Current Liabilities 3 000 Total Liquid Assets 8000 Non-Current Liabilities Lifestyle Assets Double storey house loan balance at Selangor 186 400 Double storey house at Selangor(market value) 530 000 Honda City loan balance 60 200 Computer 2 300 Yamaha Y15 loan balance 3 740 Furniture 340 Total Non-Current Liabilities 250 340 Honda city (market value) 59 800 Perodua Myvi (market value) 26 800 Total liabilities 253 340 Toyota Innova (market value) 42 300 Smartphone 1300 Net worth 708 760 Yamaha Y15 (market value) 8 100 Yamaha LC (market value) 4 300 Clothing 700 Internet monthly payment 2 160 678 100 Investment Assests Double storey house at Pahang (market value) 276 000 Total Assets 962 100 Total Liabilities and Net Worth 962 100

Mr. Mohd Bahari Balance Sheet as at 31 December 2020

Table c) shows Mr. Mohd Bahari Balance Sheet as at 31 December 2020. Under the

assets, Mr. Mohd Bahari have total RM8 000 for his liquid asset. According to James Chen of

Investopedia, liquid assets means an asset that can easily be converted into cash within a short

amount of time. In this balance sheet, it shows that Mr. Mohd Bahari have some money in his

saving account that can be use if emergency occur. Next, the total for lifestyle assets of Mr.

Mohd Bahari is RM678 100. All vehicles that he owns are used by his family members. Mr.

Mohd Bahari car, Honda City is used by his first son for his work as a Grab driver. Second car

that he had, Perodua Myvi are used by his wife and daughter for any function. Third car is

Toyota Innova, Mr. Mohd Bahari will use this car when he and his family went to any vacation

around Malaysia or when he going back to his hometown at Pahang. Since he owns two

motorcycle, he gives one of his motorcycle which is Yamaha LC to his 18 years old son. The

motorcycle is used by his son in order to go to the work at Subang Jaya. Last vehicle that he

owns is Yamaha Y15 where Mr. Mohd Bahari used for himself to commute from his work at

TNB Shah Alam.

In the balance sheet above, it shows that Mr. Mohd Bahari also own two house which

both are double storey house at different state which is one at Pahang and another one at

Selangor. These house that he owns fall under different category of assets because of different

reason. First house that he bought is a double storey house at Pahang and it is for investment.

According to James Chen of Investopedia, investment means an asset acquired with the goal

of generating income. When an individual purchases a good as an investment, the intent is not

to consume the good but rather to use it in the future to create wealth. In this case, Mr. Mohd

Bahari bought the house in order to generate income and used the income for his own good.

On 2017, he settled all of his house loan balance in Pahang. Next, on 2013, Mr. Mohd Bahari

bought a double storey house for his family in order to provide a more comfortable house

compared to his old house which is a one storey house.

Thus, after calculate all of his liquid assets, lifestyle assets and investment assets, the

total of assets that Mr. Mohd Bahari owns is RM962 100.

Table d) shows Mr. Mohd Bahari cash flow statement for the year ended 31 December

individual cash that they earn and cash that they spend to determine either their have a positive

or negative net cash flow.

According to cash flow statement of Mr. Mohd Bahari, he received his income in three

method. First, salary which he received it every month. Second, bonus. Bonus is a payment

where Mr. Mohd Bahari will received at the end of the year and usually his employer will pay

his bonus equal to his two-month salary. Third, Mr. Mohd Bahari received his income from his

double storey house that he rented to a friend of him at Pahang. Every month, his friend which

is the tenant will pay RM800 to Mr. Mohd Bahari. Thus, after sum up all the income that Mr.

Mohd Bahari received in the year 2020, the total is RM121 600.

In order to determine either Mr. Mohd Bahari cash flow statement positive or negative, all

expenses will be added. After all the expenses of Mr. Mohd Bahari added, the total of expenses

is RM94 396. Then, the total income of Mr. Mohd Bahari will be minus with the total expenses

of Mr. Mohd Bahari, and will get contribution of saving amounted RM27 204.

= 253962 340100 x 100

= 26.33%

A good debt ratio should not be more than 30%. According to Mr. Mohd Bahari debt

ratio, it shows that it is 26.33% where it means that the debt ratio of Mr. Mohd Bahari is in a

good condition. Thus, it means that Mr. Mohd Bahari can easily get a new loan in the future.

= (^) ( 15600 (^96 000 + 9600 −^8 952 + 3360 ) )

= 3.05 times

An ideal debt service coverage ratio is 1.2 and above. According to Mr. Mohd Bahari

debt service ratio, it is 3.05 which it is in a good condition. Thus, it means that Mr. Mohd

Bahari is able to pay his new debt obligations without drawing on outside sources.

f) INCOME TAX

Income RM Salary 96 000 Bonus 16 000 Rent received 9 600 Aggregate Income 121 600

Less: Donation - Total Aggregate Income 121 400

Less: Tax Relief Self 9 000 Wife 4 000 Children: Second child (degree) 8 000 Fourth child (primary school) 2 000 Lifestyle (smartphone, computer and internet) 2 500 Parent allowances (mother) 1 500 Medical treatment for parent 600 SOCSO 250 EPF 4 000 Total Tax Relief (31 850) Chargable Income 89 550 Income Tax Computation: Tax Rate: First RM70 000 4 600 Next RM19 550 x 21% 4 105. Total Income Tax: 8 705. Less: Rebate Zakat - Tax Payable 8 505. Less: Monthly tax deduction 7 680 Balance Tax Payable 825.

Mr. Mohd Bahari Income Tax Assessment for the year 2020

g) COMMENT AND ADVICE

In conclusion, based on balance sheet of Mr. Mohd Bahari, his net worth figure is positive.

It means that he owns more than he owes. Next, referring to the cash flow of Mr. Mohd Bahari,

his income is greater than his expenses for the year of 2020. After the income minus by the

expenses, the figures show that Mr. Mohd Bahari is contributing to saving. It means that Mr.

Mohd Bahari can make some saving from that amount of money. Then, after calculate all four

ratios, it shows that three out of four ratios are in a good figure. It means that Mr. Mohd Bahari

financial position is in a good condition. Lastly, as for the income tax, Mr. Mohd Bahari need

to pay some of money which I believe Mr. Mohd Bahari able to pay it without any problem.

Financial planning is very important to each individual. First, insurance planning.

According to Mr. Mohd Bahari financial statement, there is no health insurance is taken under

the name of Mr. Mohd Bahari currently. This is because of Mr. Mohd Bahari medical bill is

supported by his employer, Tenaga Nasional Berhad (TNB). Then, there is also no health

insurance taken under the name of his wife and his child. This is also because of his employer

supported the wife medical bill and his two-child who are still studying. Thus, Mr. Mohd

Bahari did not take any health insurance for his family. Mr. Mohd Bahari also did not take

education insurance for the kids. However, it can be a bad situation if Mr. Mohd Bahari

dismissed from his current job because Mr. Mohd Bahari did not make any backup plan by

taking other health insurance. Therefore, my advices to Mr. Mohd Bahari are first he should

take a health insurance under the name of his last child because currently he is currently 8 years

old. He is still young and the future of him is unpredictable. So, it is important to make an early

preparation for his future. Second, Mr. Mohd Bahari can take an education insurance for his

last child. Just like health insurance purpose, since his last child is still young, it is better to

make a preparation before anything bad occur. Lastly, my advice to Mr. Mohd Bahari insurance

planning, he should take a health insurance for the sake of himself and his wife. The future is

unpredictable, he could be fired from his current job or facing a sudden and permanent

disability. Thus, it is a good move if he takes a health insurance from now.

Second, investment planning. Investment is made in order to gain more income and it is

very important for each individual to make an investment for the sake of their own future.

Currently, Mr. Mohd Bahari make an investment using the house that he bought at his

hometown. Back then, he purchased the house amounted RM 143 000. Currently, the house

price become RM276 000. There is difference amounted RM 133 000 which Mr. Mohd Bahari

earn from the house investment. Mr. Mohd Bahari decide to rent it with amount RM800 per

month following to its location that is in rural area. In my opinion, it is a good investment of

Mr. Mohd Bahari by purchased a house in his youth days. However, my advice to Mr. Mohd

Bahari for his investment is that he can try to invest in another way such as Tabung Haji

Investment, Amanah Saham Bumiputera (ASB) and many more.

Third, retirement planning. It is important to have retirement planning because once an

individual retire they will no longer receive a salary. In order to sustain a stable income once

they retire, they need to save for the future. Since Mr. Mohd Bahari is a private sector worker,

he only had Employee Provident Fund (EPF) which it will be not sufficient to cover his living

expenses in the future. My advice for this situation, Mr. Mohd Bahari should take a retirement

insurance plan provided by any insurance company. As for example, PRU Retirement Growth

by Prudential Insurance Malaysia. It provides a retirement insurance that can be bought start

from the age of 30 until 60. The insured can decide how long they want to subscribe the

insurance plan and at what age they want to receive the money back. Since Mr. Mohd Bahari

is 50 years old, the best decision he can make is that he purchased the retirement insurance for

10 years until he is 60 years old and at the age of 61 years-old, the insurer will pay it back

according to amount that he paid.

Last but not least, estate planning. According to Julia Kagan of Investopedia, estate

planning involves determining how an individual’s assets will be preserved, managed, and

distributed after death. It also takes into account the management of an individual’s properties

and financial obligations in the event that they become incapacitated. Currently, most of Mr.

Mohd Bahari assets is under his name and some of the assets under his wife’s name. Mr. Mohd

Bahari had named his wife as beneficiaries of his assets and still deciding some of his assets

will be used for charitable cause. My advice for Mr. Mohd Bahari for this situation is that he

should appoint an estate-planning lawyer in order to create a good estate plan for himself and

others. It is also important to appoint an estate-planning lawyer so there will be no issue occur

soon because the wills is legal.