M.Sc. Finance

M.Sc. International Banking and Finance

M.Sc. International Accounting and Finance

Finance 4

Leasing

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Detail Summery about Finance, lease, Leasing characteristics, Basic terminology, Why lease?, Good and bad reasons.

Typology: Lecture notes

1 / 64

This page cannot be seen from the preview

Don't miss anything!

Finance 4 Leasing

Issues for this unit •

Basic terminology

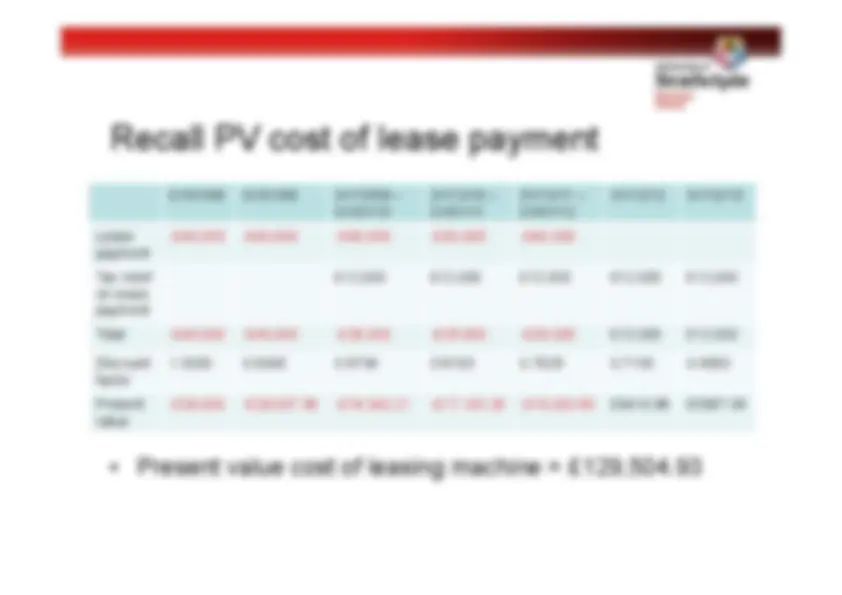

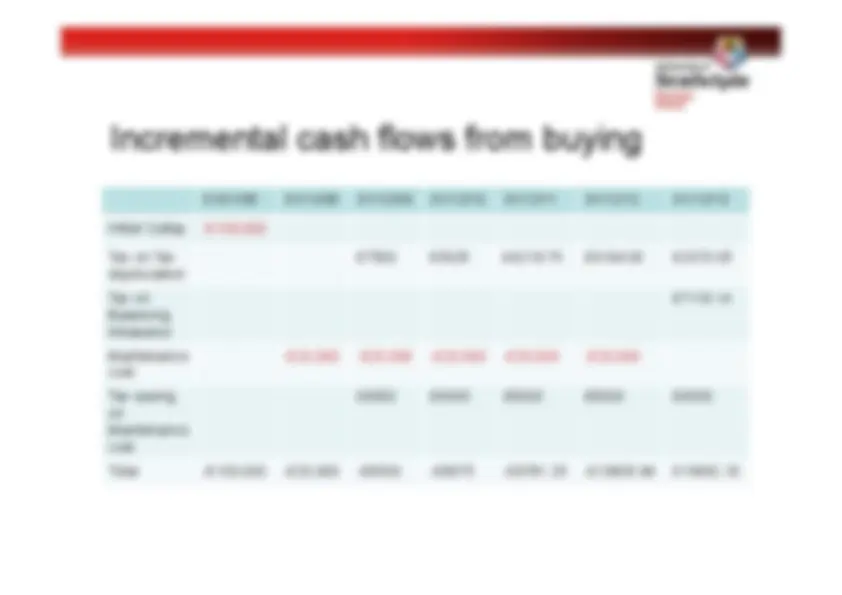

Present value of leasing vs. buying assets

Good and bad reasons

When can both lessor and lessee benefit fromlease?

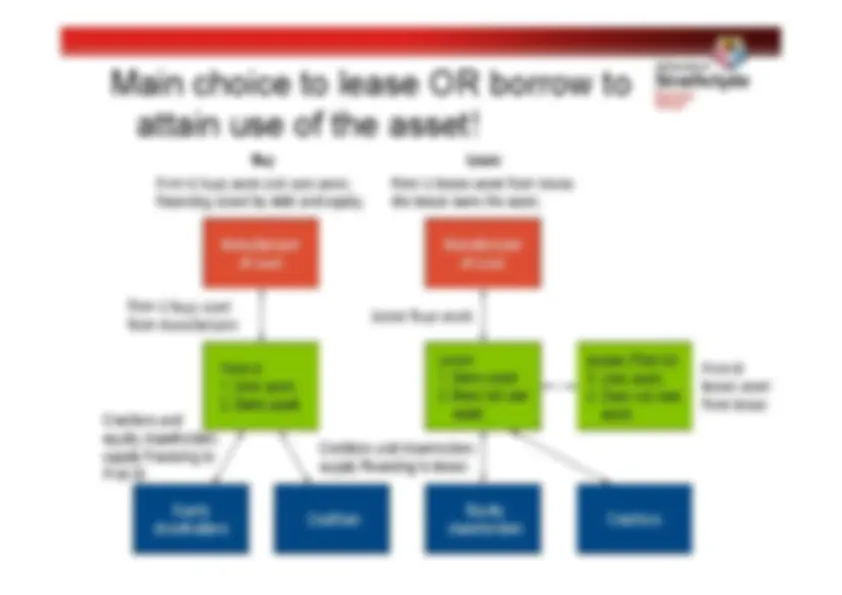

Parties to the contract •

Party who owns the assets and leases it to the otherparty

Specialist agencies (direct leasing) - Manufacturer of the asset (sales-type lease)

Firm acquiring use of asset

Significant majority of entities

Main choice to lease OR borrow to attain use of the asset!

Financing lease •

Lessor does not generally maintain / service asset

Lease is for full expected economic life of asset - Lessee has right to renew lease on expiration - Generally cannot be cancelled - More of a direct alternative to purchasing asset

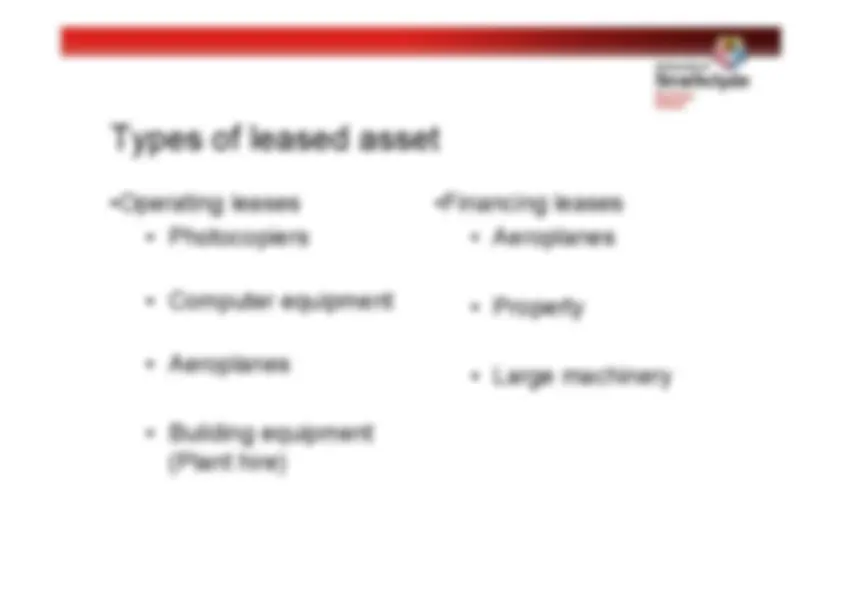

Types of leased asset • Operating leases

Photocopiers

Computer equipment - Aeroplanes - Building equipment(Plant hire)

Financing leases

Aeroplanes

Property - Large machinery

Leveraged lease •

Lessee uses the asset and makes lease payments

Lessor purchases asset and receives payments - But lessor only provides 40-50% of financing cost for asset - Lender supply remaining financing and receiveinterest payments - Loan is on non-recourse basis – lender cannot claimagainst lessor on event of lessee default - Lender has first claim on the asset and can collect leasepayments directly in the event of a loan default

Theoretically we can evaluate the NPV of an investmentproject with lease financing as:

Where: - C n is the net cash flow from operations - L n is the value of the lease payment - T C is the marginal corporate tax rate - But this approach cannot tell us about the NPV of thelease

n C n n N n = n 0

=

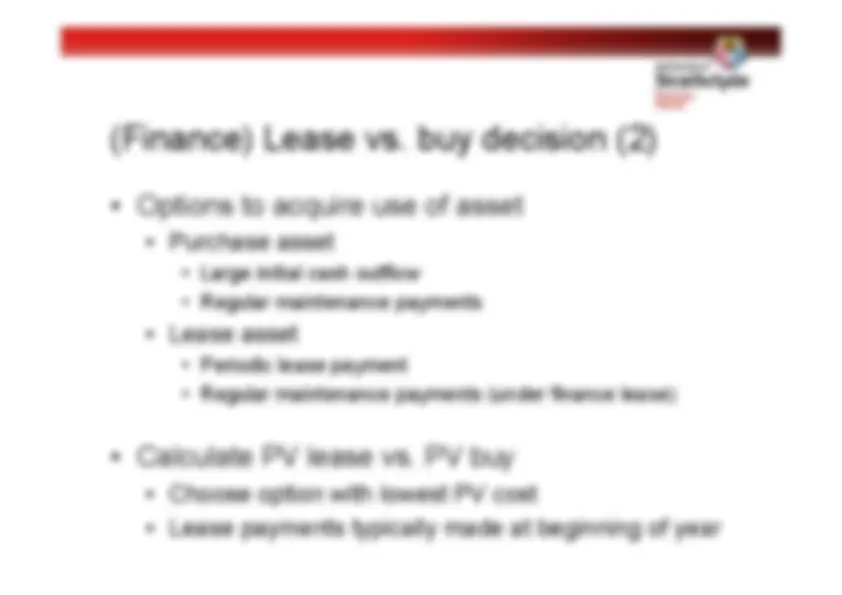

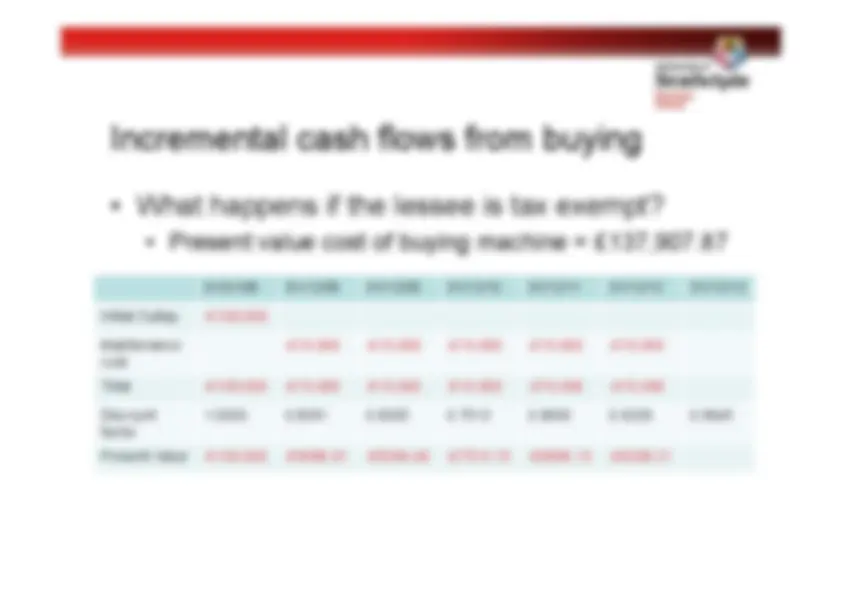

(Finance) Lease vs. buy decision (2) •

Purchase asset

Large initial cash outflow - Regular maintenance payments - Lease asset - Periodic lease payment - Regular maintenance payments (under finance lease)

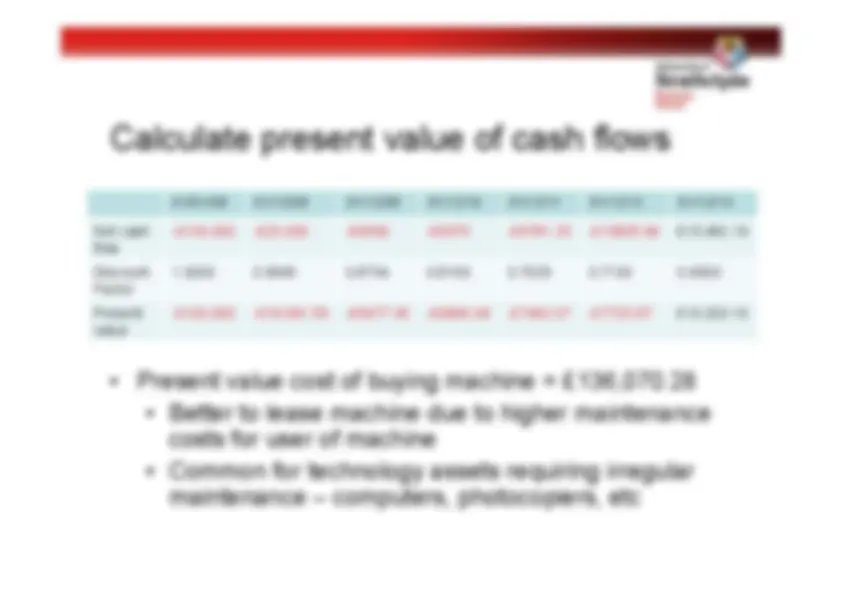

Choose option with lowest PV cost

Lease payments typically made at beginning of year

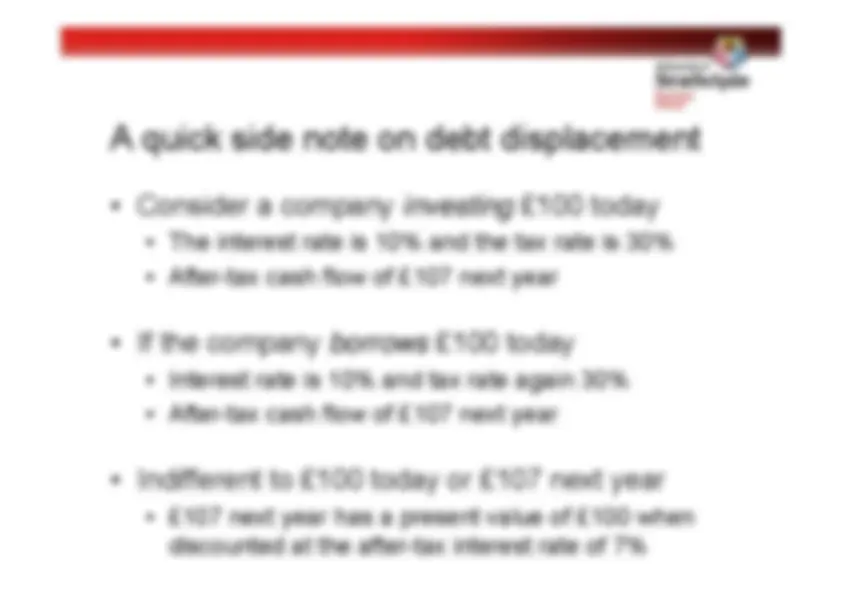

A quick side note on debt displacement •

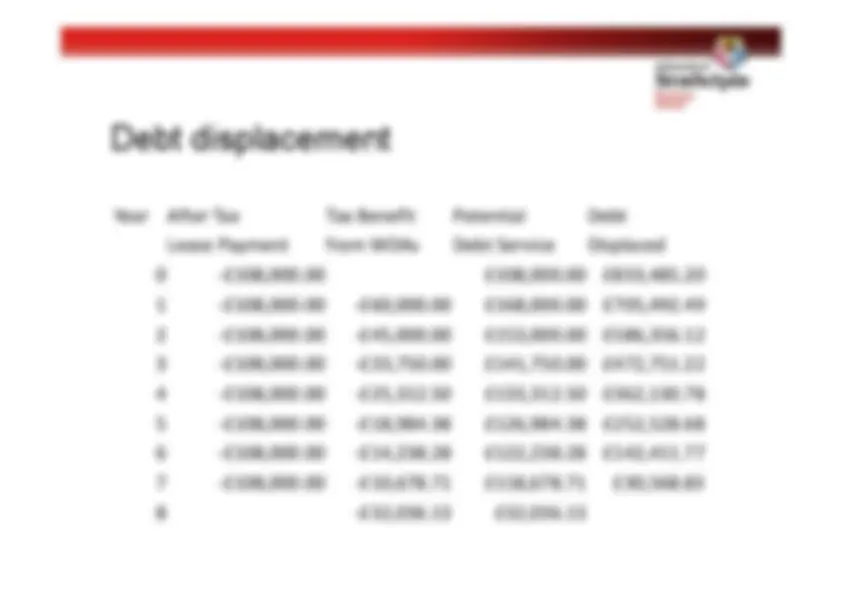

The interest rate is 10% and the tax rate is 30%

After-tax cash flow of £107 next year

Interest rate is 10% and tax rate again 30%

After-tax cash flow of £107 next year

£107 next year has a present value of £100 whendiscounted at the after-tax interest rate of 7%

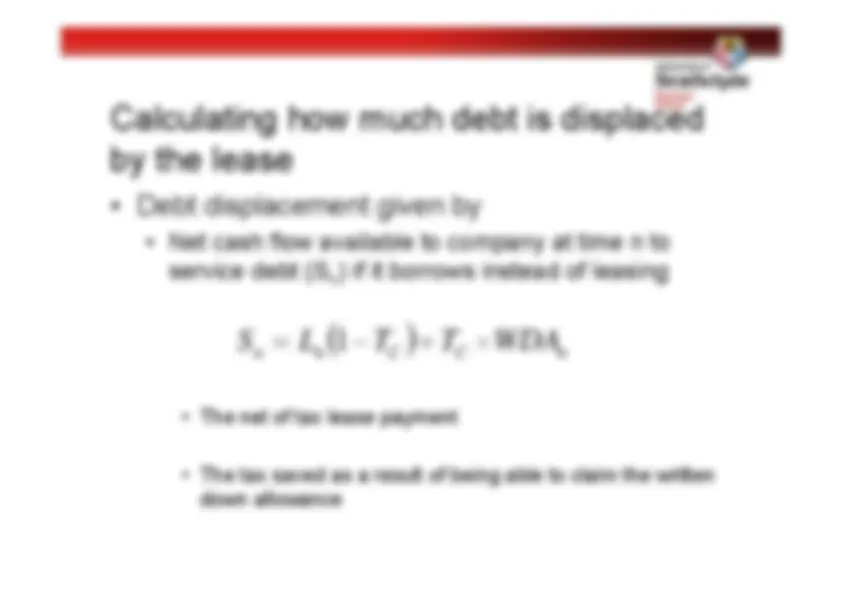

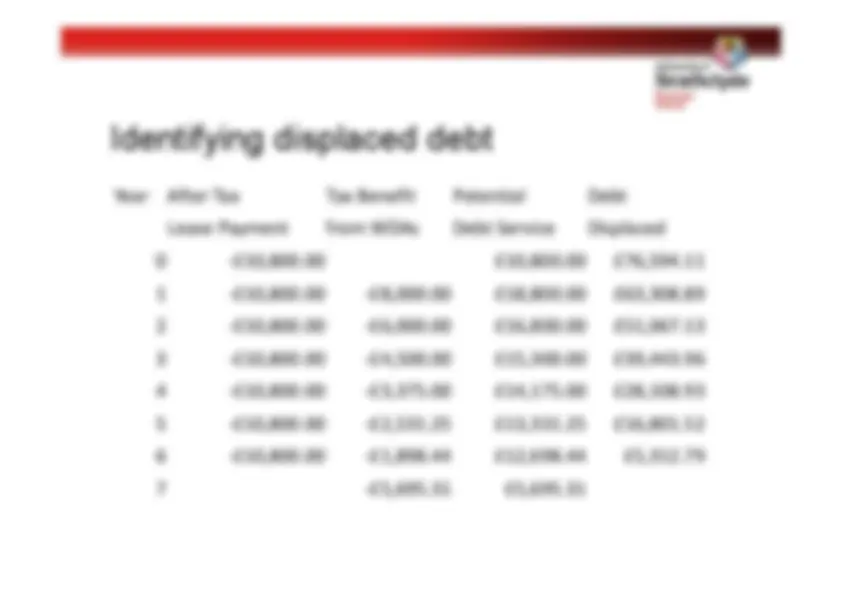

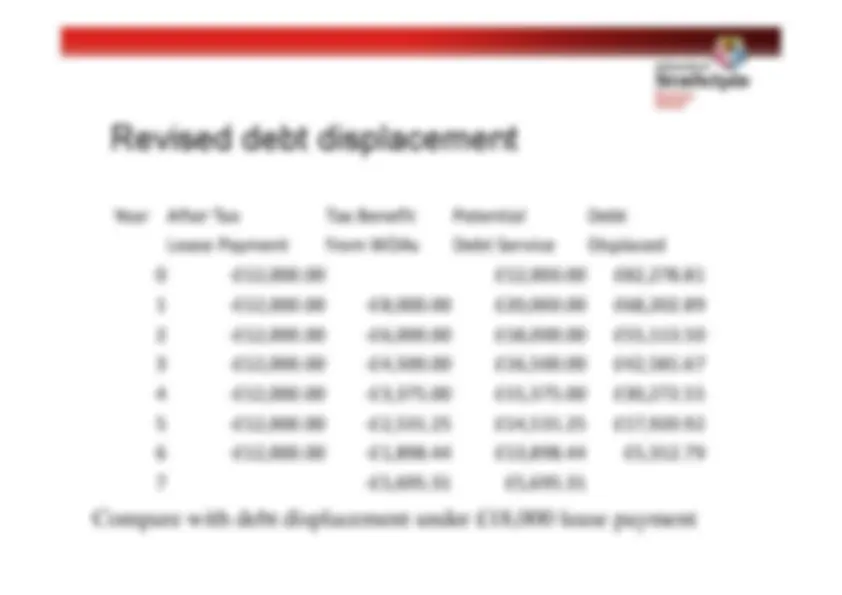

Debt displacement and leasing •

Future lease obligations reduce company’s ability toborrow today

Leads to reduction in tax benefits from debt financing

Enter tax advantage lost in each year of the lease,and discount at the interest rate on debt

Leave out the tax advantage to the interest paymentand discount at the after-tax interest rate

Structure of lease payments •

First payment made immediately

Contrast with standard annuity paid at end of each period - May be valued as growing annuity with inflation - Remember to be consistent with nominal and real discountrates

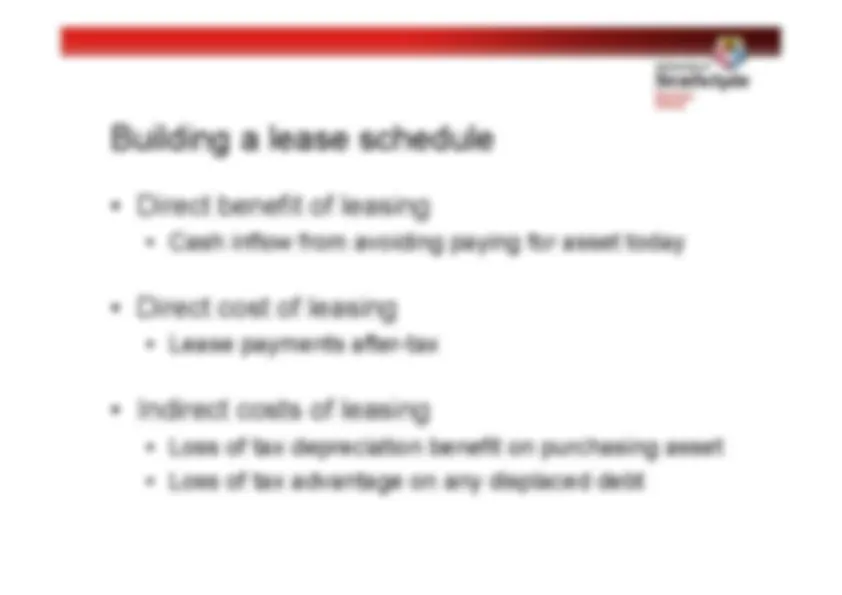

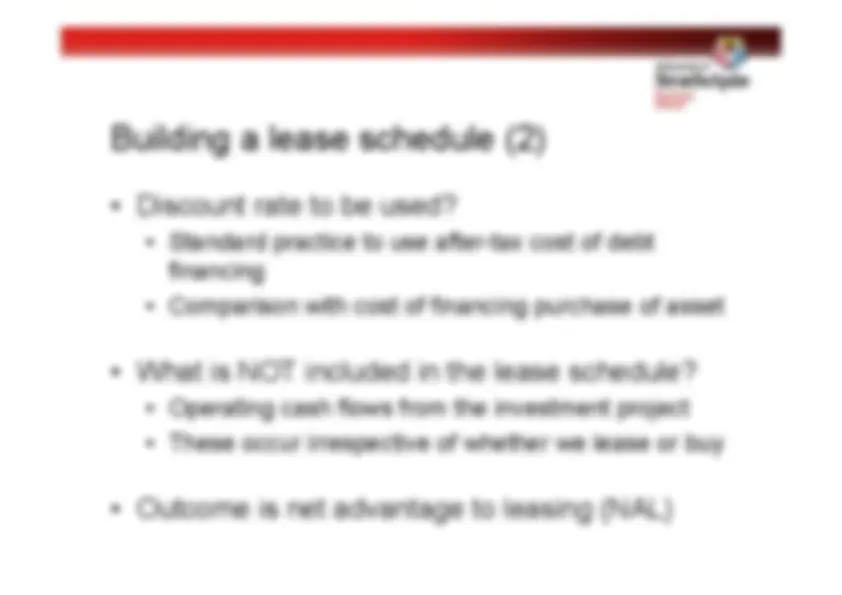

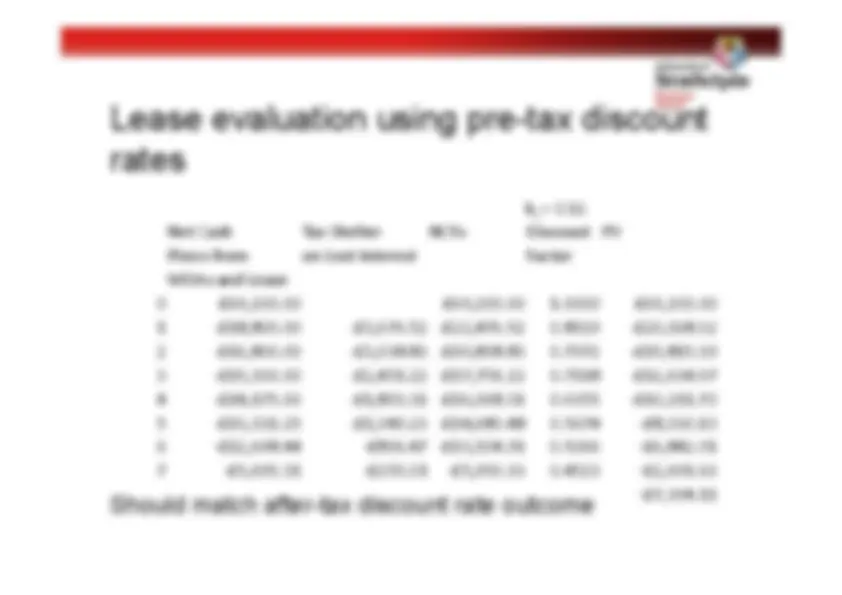

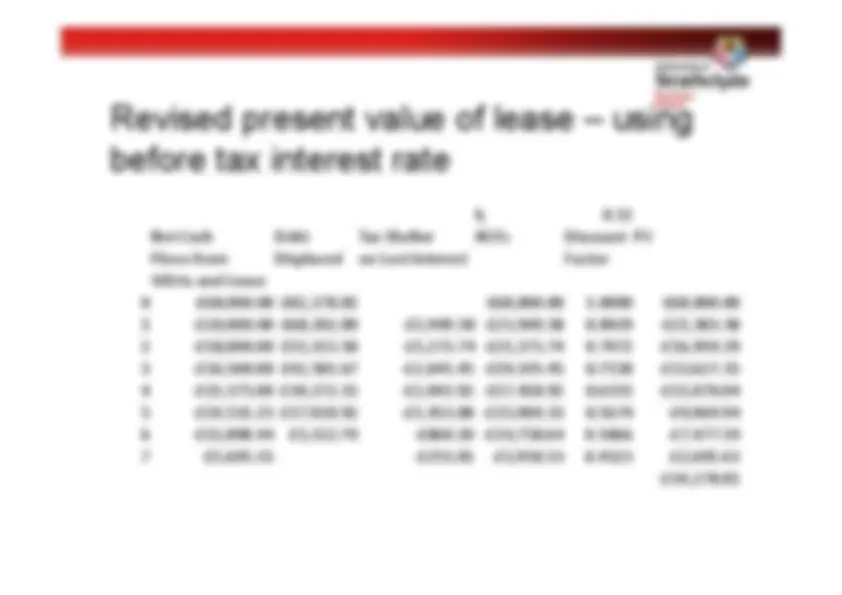

Building a lease schedule (2) •

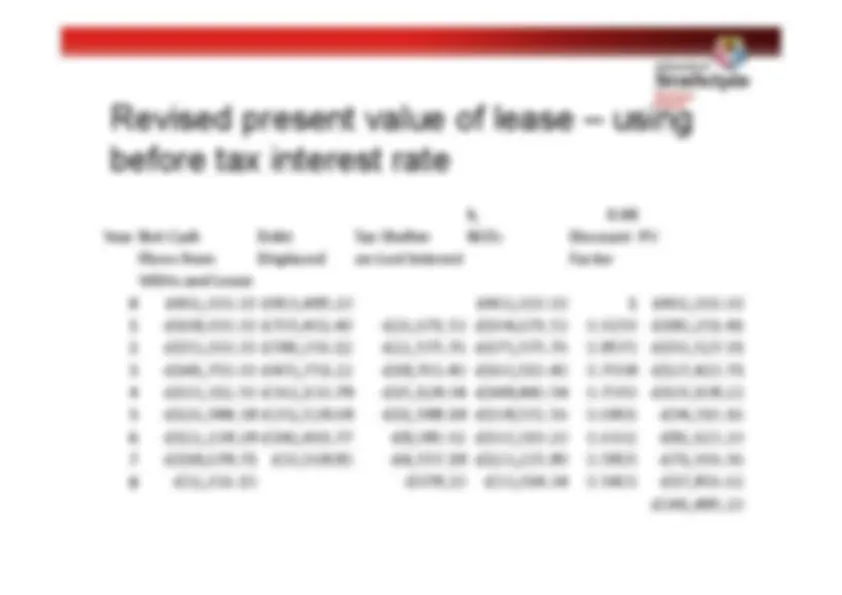

Standard practice to use after-tax cost of debtfinancing

Comparison with cost of financing purchase of asset

Operating cash flows from the investment project

These occur irrespective of whether we lease or buy

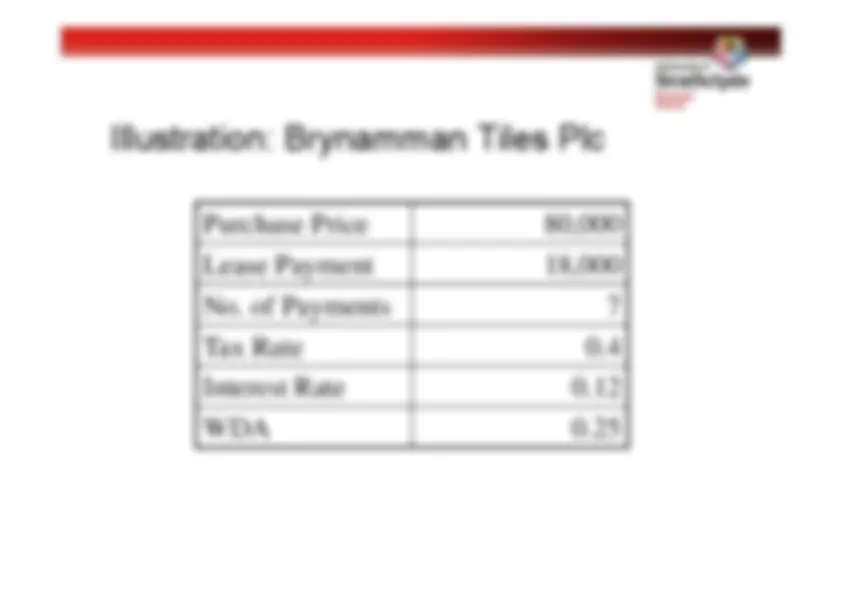

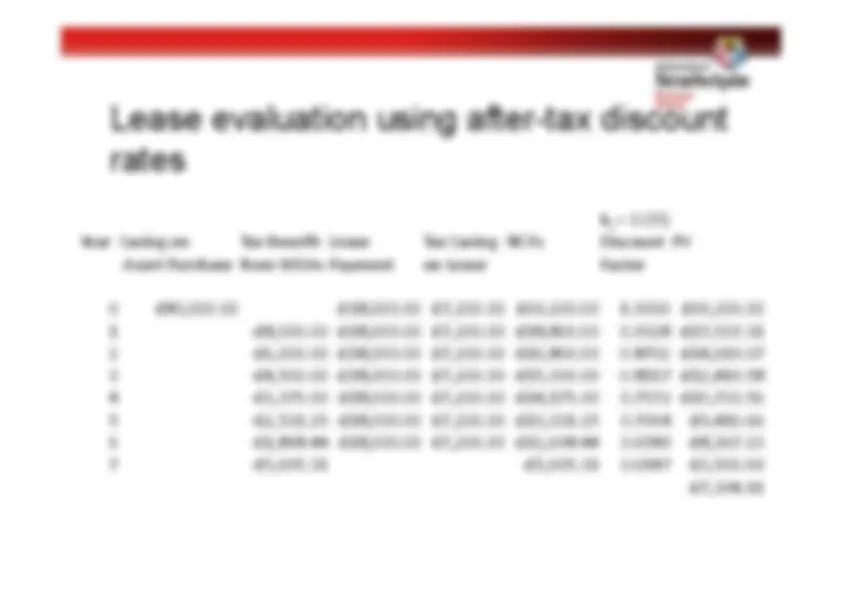

Illustration: Brynamman Tiles Plc