Download Accounting and Financial Management for Managers: A Comprehensive Guide and more Assignments Microfinance in PDF only on Docsity!

ACCOUNTANCY & FINANCIAL

MANAGEMENT

FOR MANAGERS

(MCS-35/MTTM 05) FOR

MCA/MTTM- JAN 2020

Academic Counselor

BINOD RAJ SINGH

[CA (Nepal), CA (India), BCOM, MCOM, CS Professional, LLB II]

BLOCK - 1 (Accounting System) Accounting & Its Function Accounting Concepts & Standards Basic Accounting Process, Preparation of Journal, Ledger & Trial Balance

5

Concept

What is Accounting?

Where did this term came from?

What is Debit & Credit?

Scope of Accounting

Data Creation & Collection

Data Evaluation

Analytical and Interpretative

Data Reporting

Accounting as information

system

External Users

- Shareholders, Lender, Govt., Employee,

Customer, Creditor

Internal Users

Emerging Role of Accounting

Stewardship Accounting, Financial

Accounting

Cost Accounting, Management

Accounting

Social Responsibility Accounting,

Human Resource Accounting

Inflation Accounting

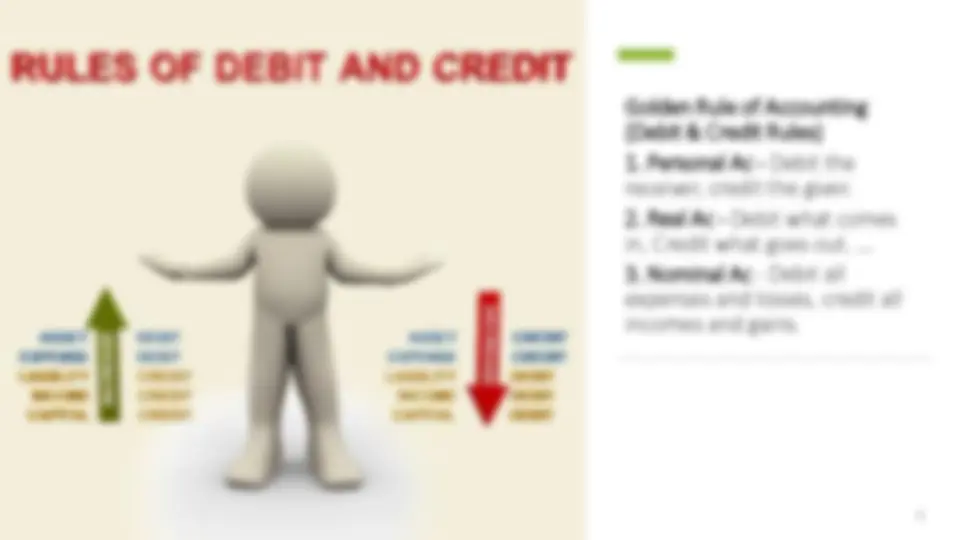

Meaning of “Debit” & “Credit”??? Dictionary Meaning Debit= Left Side Credit= Right Side Latin Word Meaning Debit in Latin means "he owes" Credit in Latin means "he trusts"

Golden Rule of Accounting (Debit & Credit Rules)

- Personal Ac - Debit the receiver, credit the giver.

- Real Ac - Debit what comes in, Credit what goes out. ...

- Nominal Ac - Debit all expenses and losses, credit all incomes and gains.

Role Of Accountant Accounts Keeping Control Conscience (Good or Bad) of Organisation Information to Management Fiscal Advisor Accounting Personal Accountant in Public Practice

- Chartered Accountants (A- Class Auditors)

- Registered Auditors (B, C & D- Class Auditors) Accountants in Private Employments

- Internal Auditors

- Finance Controller

- Treasurer

- Finance Officer

Chapter - 2 Or Break?

- Entity Concept

- Money Measurement Concept

- Continuity Concept (Going Concern)

- Accrual Concept

- Cost Concept (Historical Cost)

- Conservatism Concept

- Materiality Concept

- Consistency Concept

- Periodicity Concept

- Substance Over Form Accounting Concepts

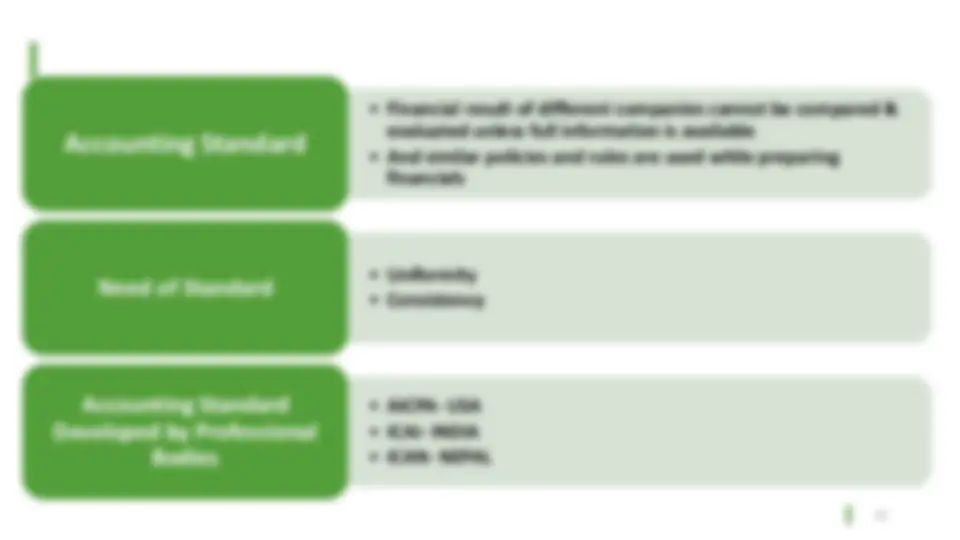

- Financial result of different companies cannot be compared &

evaluated unless full information is available

- And similar policies and rules are used while preparing

financials

Accounting Standard

- Uniformity

- Consistency Need of Standard

- AICPA- USA

- ICAI- INDIA

- ICAN- NEPAL Accounting Standard Developed by Professional Bodies

- Uniform AS at International level

- Concept started at Sydney in 1972, in accounting convention

- International AS committee was formed

- All member countries agreed to adopt similar concept

- Since 1973: So, far 41 International Accounting standard (IAS)

has been issued

Standard at International Level

- ICAI- 1949 ESTD

- ICAI formed ASB in 1977

- ICAI-ASB issued 29 AS so far & 3 recommendatory AS Accounting Standard in India

By: Binod Raj Singh

- ICAN- 1997 ESTD

- ICAN formed ASB in 2003

- ICAN- ASB issued 19 AS Compulsory & 7 AS Voluntary AS in Nepal

- IFRS was one of the most significant change in accounting history

- In 1973: 41 IAS were issued by Board of International Accounting Standard Committee

(IASC)

- On April 2001, new International Accounting Standard Board (IASB) took over ISAC to for

setting international accounting standard called IFRS

- Total 17 IFRS has been issued till date ( from 2003 – 2018)

- Europe adopted IFRS in 2005, USA adopted for SEC regulated entities in 2008

- 120 + Nations have implemented IFRS till date

- IFRS is set to become the Global Accounting language

- Nepal have also adopted IFRS called as NFRS ( Started from 2014 with target to complete

by 2018)

IFRS Concept (International Financial Reporting Standard)

Chapter - 3

Accounting Information & Its Application