Download Financial Statement Analysis: Understanding Fundamental and Technical Approaches and more Study Guides, Projects, Research Finance in PDF only on Docsity!

Analysis of Financial Statements

Two Approaches to Analysis

- Fundamental Analysis

- Analyses the business, economic and financial fundamentals

- Technical Analysis

- Analyses historical share prices to help predict future share prices & movements

An Analysis Framework

- A framework for fundamental analysis can break business analysis and valuation into the five stages outlined below. - Business Strategy Analysis

outcomes.

- Financial Analysis

- Evaluates the financial data which will include a detailed ratio analysis.

- Prospective Analysis

- Forecasting future profits and cash flows.

- Valuation

- Company valuation (dividend discount model, discounted earnings approach, accounting models etc.)

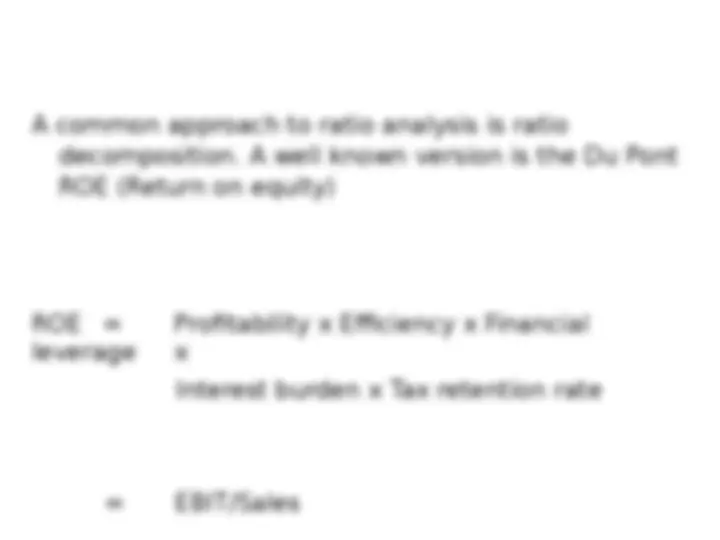

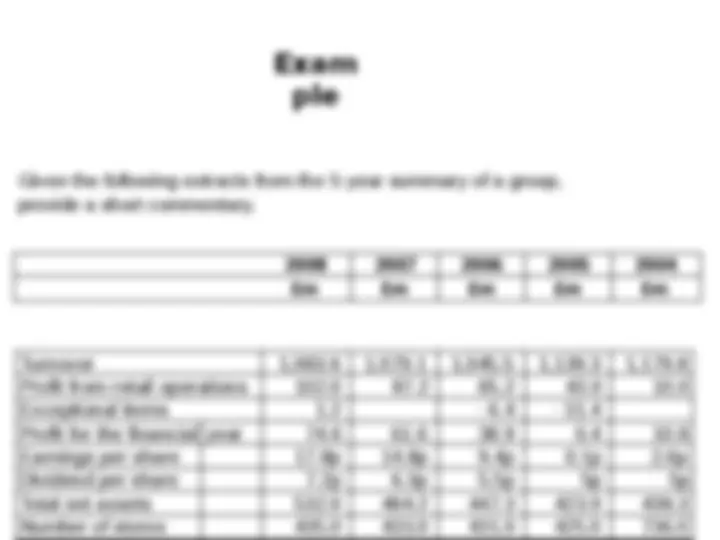

Financial Analysis ‐ Ratios

- Ratios provide a quick and simple means of examining financial health of a business.

- By calculating a small number of ratios it is often possible to build up a picture of the position and performance of a business. Thus they are widely used by investors and others interested in business performance.

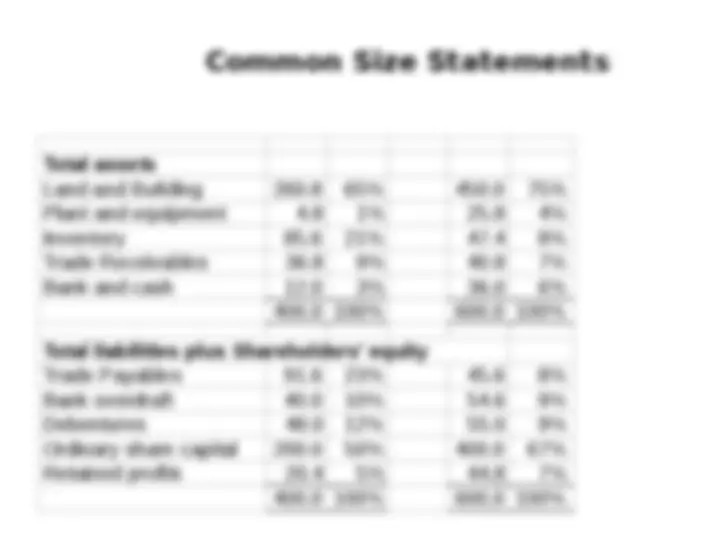

Advantages of Ratios

- Figures in accounts are often only meaningful when considered in relation to other figures.

- Enable us to compare businesses of different size.

- Enable us to gain a vision of the company’s trading pattern.

- Enable comparison with published industrial averages.

- Substitute a small set of ratios to replace the complexity of the detailed financial statements.

- Efficiency/Working Capital Activity Ratios

- Investment ratios

Profitability

Ratios

- Businesses aim to create wealth for owners. Profitability ratios provide an insight to the degree of success. They express the profits made in relation to other key figures in the financial statements.

- There are 4 main profitability ratios:

Profit before interest and taxation x 100 Shareholders’ funds plus long term debt

Often called ‘Operating profit’ or EBIT

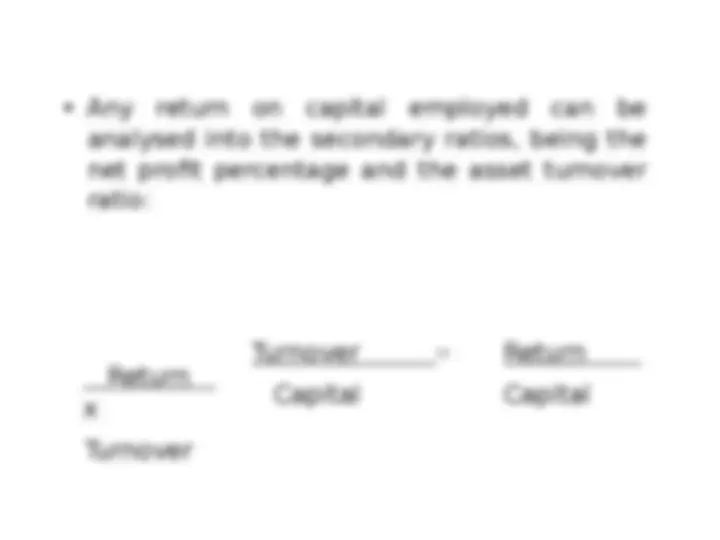

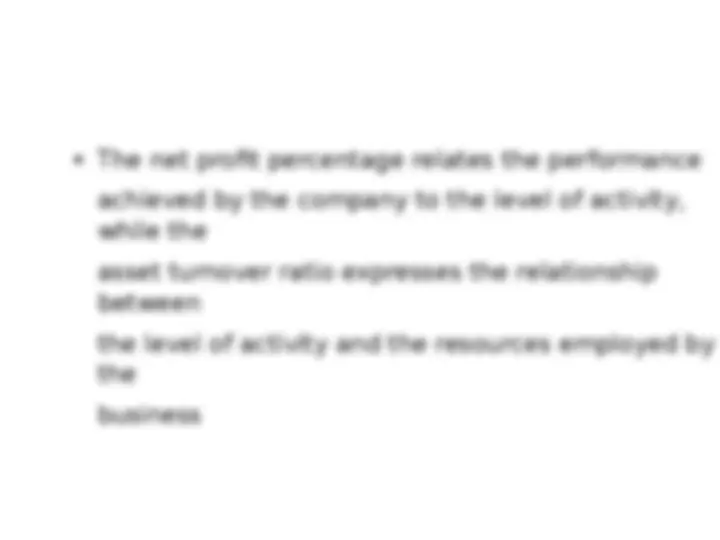

There are a number of ways of calculating ROCE ratios, each

one with a different definition of profit and capital. BEWARE

Definition ROCE is a fundamental measure of business performance which expresses the relationship between the profit generated by the business and the long term capital invested in the business.

Bottom line questions

- Recent increases in assets may not yet have created profit

- Selling assets can increase ROCE

- Is there any debt ‘off balance sheet’?

Return on Shareholders Funds

‐ ROSF

(also called Return on Equity ‐ ROE)

Profit attributable to equity shareholders x

Gross profit [margin] ratio

- The gross profit margin relates the gross profit of the business to the sales generated for the same period.

- Gross profit represents the difference between sales and the cost of sales. The ratio is thus a measure of profitability in buying/producing goods before any other non‐manufacturing expenses are taken into account.

Gross Profit

Sales

x 100 = X%