Introduction to Fi

nancial

Statement Anal

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

This lecture introduces financial statement analysis, its purpose, and the users of financial information. Topics include the importance of financial analysis, the role of financial analysts, and the various users of financial statements. The document also covers the financial information available to users and the concept of agency costs.

Typology: Study Guides, Projects, Research

1 / 57

This page cannot be seen from the preview

Don't miss anything!

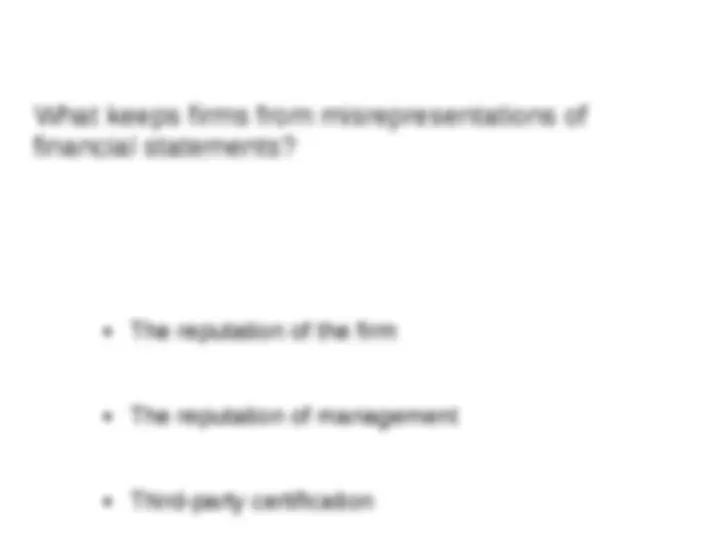

reliability of accounting statements.

Intermediaries:–^ Public