Lesson One 1

FINANCIAL ACCOUNTING 1

FINANCIAL ACCOUNTING

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

The Accounting cycle descriptions and illustrations together with elaborated articulations

Typology: Lecture notes

1 / 588

This page cannot be seen from the preview

Don't miss anything!

On special offer

FINANCIAL ACCOUNTING;

Nature and scope of financial accounting………………………………………………

Users of Accounting information………………………………………………………..

Illustrations on the above………………………………………………………………...

Accounting for purchases, sales, income and expenses………………………………….

Return inwards and return outwards…………………………………………………...

Accounting for drawings and discounts………………………………………………….

Source documents and books of original entry………………………………………….

Sales invoice, purchase invoice and debit notes………………………………………….

Illustrations on the above………………………………………………………………….

CHAPTER THREE

Petty cashbook and columnar system of book- keeping…………………………………

Imprest sytem……………………………………………………………………………….

Accounting concepts conventions and policies……………………………………………

Qualities of a useful financial information………………………………………………..

Final accounts for sole traders…………………………………………………………….

Illustration on the above…………………………………………………………………...

Standard revision questions……………………………………………………………

Partnerships accounts………………………………………………………………….

Goodwill and revaluation………………………………………………………………

Illustrations on the above……………………………………………………………….

Interpretation of final accounts………………………………………………………..

Royaties,containers and consignment accounts………………………………........

Standard revision questions………………………………………………………..

Lease and hire purchase transactions……………………………………………..

Allocation of finance charges……………………………………………………….

Standard revisions questions……………………………………………………….

Contract,investments and insurance claims………………………………………

Requirements as per IAS 11……………………………………………………….

Standard revision questions……………………………………………………….

Accounting for investments with fluctuating rate of return on nominal value..

Revision questions………………………………………………………………….

Insurance claims…………………………………………………………………..

Revision questions…………………………………………………………………

MKanufacturing accounts………………………………………………………..

Illustrations on the above…………………………………………………………

Distinction between partnerships and limited companies……………………….

Definition of accounting;

Accounting is defined as the process of identifying, measuring and reporting economic information to the users of this information to permit informed judgment It is thus concerned with the recording o f the financial transactions of business in a systematic manner.

Users of Accounts Information

Accounting information is produced in form of financial statement. These financial statements provide information about an entity financial position, performance and changes in financial position.

Financial position of a firm is what the resources the business has and how much belongs to the owners and others.

The financial performance reflects how the business has performed, whether it has made profits or losses. Changes in financial positions determine whether the resources have increased or reduced.

The users of accounting information have an interest in the existence of the firm. Therefore the information contained in the financial statements will affect the decision making process.

The following are the users of accounting information

i. Owners:

They have invested in the business and examples of such owners include sole traders, partners (partnerships) and shareholders (company). They would like to have information on the financial performance, financial position and changes in financial position.

This information will enable them to assess how the managers of the business are performing whether the business is profitable or not and whether to make drawings or put in additional capital.

ii. Customers

Customers rely on the business for goods and services. They would like to know how the business is performing and its financial position.

This information would enable them to assess whether they can rely on the firm for future supp

Prepared by Serem Vincent, BCOM (Hons), MBA (Financial Management), MBA ( Strategic Management) Page 10

information would be important as they can use it to negotiate for better terms including salaries, training and other benefits.

They can also use it to assess whether the firm is financially sound and therefore their jobs are secure.

viii. The Public Institutions and other welfare associations and groups represent the public. They are interested with the financial performance of the firm. This information will be important for them to assess how socially responsible is the firm.

This responsibility is in form the employment opportunities the firm offers, charitable activities and the effect of firm‟s activities on the environment.

A business owns properties. These properties are called assets. The assets are the business

resources that enable it to trade and carry out trading. They are financed or funded by the

owners of the business who put in funds.

These funds, including assets that the owner may put is called capital. Other persons who are

not owners of the firm may also finance assets. Funds from these sources are called liabilities.

The total assets must be equal to the total funding i.e. both from owners and non-owners. This

is expressed inform of accounting equation which is stated as follows:

Prepared by Serem Vincent, BCOM (Hons), MBA (Financial Management), MBA ( Strategic Management) Page 11

Each item in this equation is briefly explained below.

Assets :

An asset is a resource controlled by a business entity/firm as a result of past events for which

economic benefits are expected to flow to the firm.

An example is if a business sells goods on credit then it has an asset called a debtor. The past

event is the sale on credit and the resource is a debtor. This debtor is expected to pay so that

economic benefits will flow towards the firm i.e. in form of cash once the customers pays.

Assets are classified into two main types:

i) Non current assets (formerly called fixed assets). ii) Current assets. Non current assets are acquired by the business to assist in earning revenues and not for resale.

They are normally expected to be in business for a period of more than one year.Major

examples include:

Land and buildings Plant and machinery Fixtures, furniture, fittings and equipment Motor vehicles Current assets are not expected to last for more than one year. They are in most cases directly

related to the trading activities of the firm. Examples include:

Stock of goods – for purpose of selling. Trade debtors/accounts receivables – owe the business amounts as a resort of trading. Other debtors – owe the firm amounts other than for trading. Cash at bank. Cash in hand.

Liabilities:

These are obligations of a business as a result of past events settlement of which is expected

to result to an economic outflow of amounts from the firm. An example is when a business

buys goods on credit, then the firm has a liability called creditor. The past event is the credit

Prepared by Serem Vincent, BCOM (Hons), MBA (Financial Management), MBA ( Strategic Management) Page 13

Name

Balance sheet as at 31.12.

Sh Sh Sh Sh

Capital xx Non Current Assets

Land & Buildings xx

Non Current Liabilities Plant & Machinery xx

Loan xx Fixtures, furniture & fittings xx

Motor vehicles xx

Current liabilities xx

Overdraft xx Current Assets

Creditors xx xx Stocks xx

Debtor’s xx

Capital and Liabilities Cash at bank xx

Cash in hand xx xx

xx Total assets xx

Prepared by Serem Vincent, BCOM (Hons), MBA (Financial Management), MBA ( Strategic Management) Page 14

The above format of the balance sheet is the horizontal format however currently the practice

is to present the Balance Sheet using the vertical format which is shown below.

Name;

Balance sheet as at 31.12.

Non Current Assets Sh Sh Sh

Land & Buildings xx

Plant & Machinery xx

Fixtures, furniture & fittings xx

Motors vehicles xx

Current Assets;

Stocks/inventories xx

Debtors/ trade receivables xx

Cash at bank xx

Cash in hand xx

Current Liabilities;

Bank Overdraft xx

Creditors/trade payables xx (xx)

Net Current Assets xx

Net assets xx

Capital xx

Non Current Liabilities;

Prepared by Serem Vincent, BCOM (Hons), MBA (Financial Management), MBA ( Strategic Management) Page 19

Capital; 8,

Remember the Accounting equation:

Assets = Liabilities + Capital.

To get capital we rearrange the equation as follows:

Capital = Assets - Liabilities

Total Assets = ₤12,

Total Liabilities = ₤4,

Capital = ₤ 12,900 - 4,

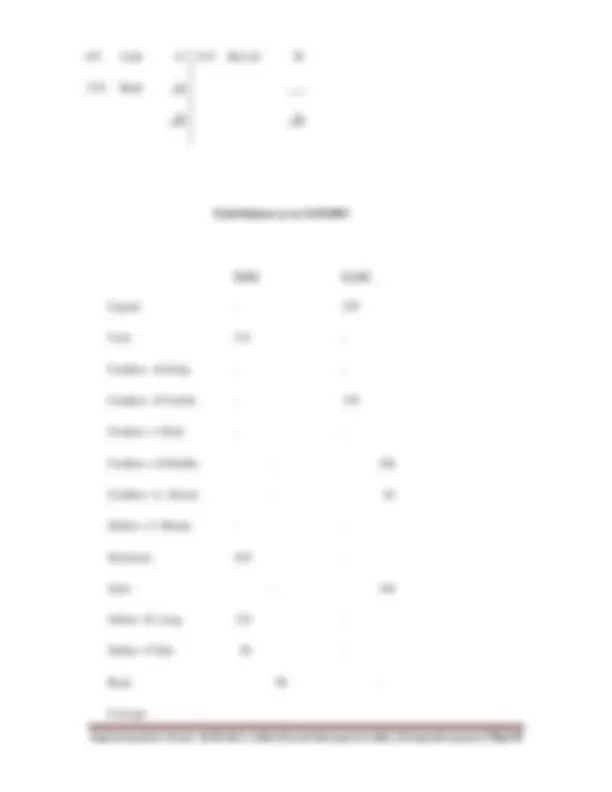

Example;

C Kings has the following items in his balance sheet as on 30 June 2002.

Capital £41,800, Creditors £3,200, Fixtures £7,000, Motor Vehicles £8,400, Stock of goods

£9,900, Debtors £6,500, Cash at bank £12,900 and Cash in hand £240.

During the first week of July 2002:

Prepared by Serem Vincent, BCOM (Hons), MBA (Financial Management), MBA ( Strategic Management) Page 20

a. He bought extra stock of goods £1,540 on credit. b. One of the debtors paid him £560 in cash. c. He bought extra fixture by cheque £2,000.

You are to draw up a balance sheet as on 7 July 2002 after the above transactions have been

completed.