Download Financial Leverage - E-Commerce - Lecture Slides and more Slides Fundamentals of E-Commerce in PDF only on Docsity!

Degree of Financial Leverage

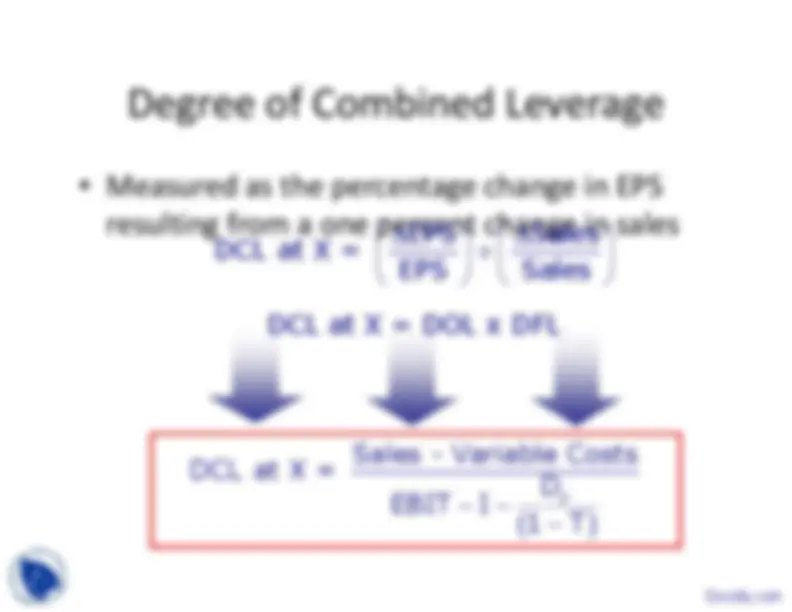

Measured as the percentage change inearnings per share (EPS) resulting from a onepercent change in EBIT ∆ ∆ ÷ EPS EBIT DFL at X = EPS EBIT

− − − p EBIT DFL at X = D EBIT I 1 T

Degree of Financial Leverage

Must measure the Degree of FinancialLeverage (DFL) at a given level of EBIT, X

DFL rises as EPS approaches 0 - Divide Preferred Share dividends by oneminus the tax rate to make them equivalentto interest - DFL rises as more debt is used to replaceequity on the Balance Sheet - When $1 of equity is replaced with $1 of debt

Degree of Combined Leverage

Model

% Changein Sales % Changein EBIT % Change in EPS Low High DCL Small EPS change Large EPS change DOL DFL

DOL & DFL Trade Off

A firm can “trade off” operating and financialleverage to control the degree of combinedleverage

A firm with a high degree of operatingleverage may choose a capital structure witha low degree of financial leverage to avoid ahigh degree of combined leverage

EBIT-EPS Analysis

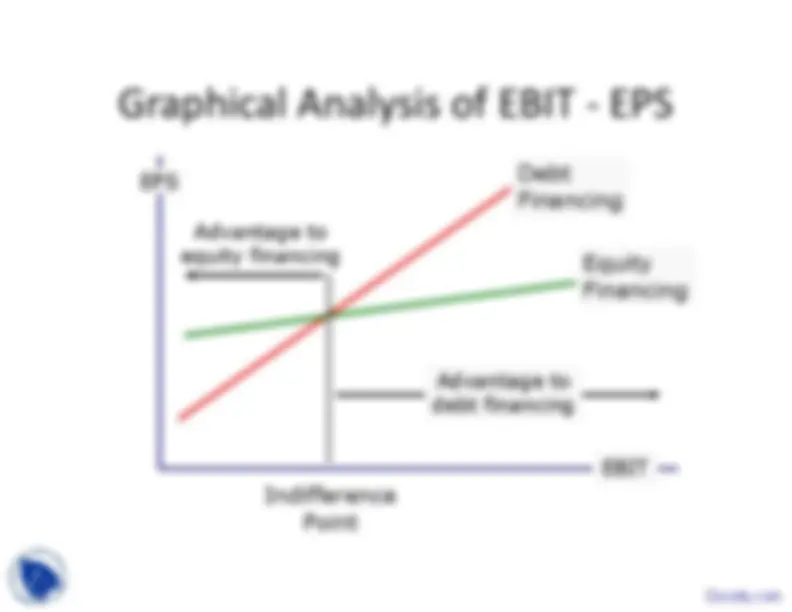

Determine the level of EBIT where EPS wouldbe identical under either debt or equityfinancing:

− − − − − = d p e p d e EBIT - I 1 T D EBIT I 1 T D N N I d = Interest if debt alternative chosen I e = Interest if equity alternative chosen N d = Shares outstanding if debt alternative chosen N e = Shares outstanding if equity alternative chosen T = Firm’s marginal tax rate

Graphical Analysis of EBIT - EPS

EPS EBIT DebtFinancing EquityFinancing Indifference Point Advantage to equity financing Advantage todebt financing

Riskiness of the Capital Structure

Examine the market evidence to see if thecapital structure is too risky in relation to thefirm’s level of:

Business risk - Industry norms for leverage and coverage ratios - Recommendation of the firm’s investment bankers

Factors in Capital Structure

Decisions

Tendency to cluster around industry average

Need for funds - Benchmark leverage ratios - By lenders and bond rating agencies - Managerial risk aversion - Retain control