Download Financial Ratios - Lecture Slides and more Slides Financial Accounting in PDF only on Docsity!

Financial Ratios

FOUR BASIC TYPES - most commonly used for each - can be used for some financial companies.

LIQUIDITY

- Current ratio = Current Assets / Current Liabilities

Not so relevant for financial firms - most assets liquid.

MANAGEMENT SKILL

- Total Asset Turnover = Sales / Total Assets

Again, not so relevant because traditional sales are typically not very large. Interest and investment income is more relevant.

PROFITABILITY

- Operating profit margin = Operating Profit/Sales

- Return on Revenues = Net Income (or EBIT)/Tot. Assets

- Return on Assets = Net Income (or EBIT)/Total Assets

- Return on Equity = Net Income/Equity

These are measures of top-line profitability and bottom- line profitability, respectively. Similar for financial firms.

FINANCIAL RISK

- Debt Ratio = Debt / Assets

- Times Interest Earned = Net Operating Income / Interest Expense Leverage and interest-paying ability - used for financials.

MANAGEMENT EFFICIENCY

- Earning Assets to Total Assets = Assets-(Cash+Fixed Assets+Non-earning Deposits) / Total Assets

- Burden = (Noninterest Exp.-Nonint. Inc.)/Tot. Assets

- Efficiency = Nonint. Exp./(Nonint. Inc. + Net Int. Inc.)

- Asset Utilization = Total Operating Income / Total Assets

PROFITABILITY Interest Margin to Earning Assets = (Interest Income-Interest Expense)/Earning Assets

- Profit Margin = Net Income/Total Operating Income

- Return on Earning Assets = Net Income/Earning Assets

- Return on Equity = Net Income/Equity

FINANCIAL RISK

- Loan Loss Coverage = (Pretax Income+Loss Provisions) /Net Charge-offs

- Provisions to Charge-offs = Loss Provisions/Net Charg.

- Loss Allowance to Loans = Loss Allow./Loans

- Equity to Assets = Equity / Total Assets

Other issues important to financial analysis of banks

- Examine assets for risky asset types (LDC debt, related party loans, allowance for loan loss etc.).

- Examine shareholder equity for unrealized gains/losses.

Making Loans and Reserving

for Losses Versus Guarantees

- Financial firms, particularly banks, can make risky loans or provide loan guarantees and both are conceptually the same.

Risky loan value = risk-free value + loan guarantee value

- When a loan is made, the bank earns interest above the risk- free rate. The premium above the risk-free rate is a premium for bearing risk as well as compensation for analyzing the and monitoring the borrower’s financial condition.

Loan rate = risk-free rate + risk premium and compensation

Effect of Loans vs. Guarantees

on Financial Statements

- The effects of loans - transparent.

- The loan appears as an asset on the balance sheet.

- A loan loss reserve appears as a contra-asset that reduces the loan value by an amount to cover the expected loss on the loan - a risk measure.

- Interest is collected periodically and appears on the balance sheet.

- The effects of loan guarantees - opaque

- Off-balance sheet “intangible” liability - no contingent liability is booked. Footnote should provide some info.

- Large up-front fee may appear immediately on income statement or periodic fee shows up over time.

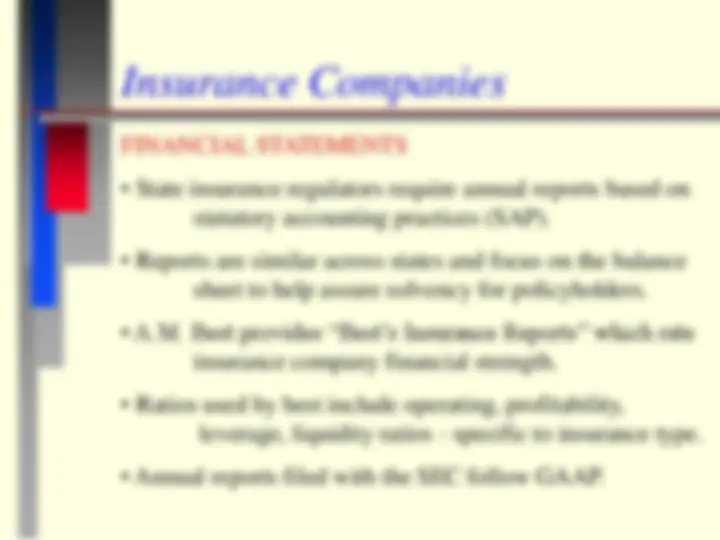

Insurance Companies

FINANCIAL STATEMENTS

- State insurance regulators require annual reports based on statutory accounting practices (SAP).

- Reports are similar across states and focus on the balance sheet to help assure solvency for policyholders.

- A.M. Best provides “Best’s Insurance Reports” which rate insurance company financial strength.

- Ratios used by best include operating, profitability, leverage, liquidity ratios - specific to insurance type.

- Annual reports filed with the SEC follow GAAP.

Insurance Ratios

MANAGEMENT EFFICIENCY

- Loss Ratio = Incurred Losses/Premiums Earned

- Expense Ratio = (Sales + Service Expenses)/Premiums Earned

- Dividend Ratio = Dividends/Premiums Earned

- Combined Ratio=Loss Ratio+Expense Ratio-Dividend Ratio

- Combined Ratio after Dividends =Loss Ratio+Expense Ratio

- If the Combined Ratio after Dividends exceeds 1, then the company must rely on investment income for profit.

Other issues in financial analysis of Insurance Companies

- Look for significant differences between fair value of investments and their costs or amortized costs.

- Check the equity section for unrealized gains (losses).

- Check for a deferred policy acquisition cost buildup.

- Check that loss reserves grow adequately with insurance in force.

Other Financial Companies’

Ratios and Financial Issues

Other financial companies have more conventional financial statements and one can use the conventional ratios discussed at the beginning of this lecture.

Issues for Securities Companies and Investment Banks

- Look for excess leverage using Equity to Assets.

- Examine the degree of long or short positions relative to total assets for extreme positions.

- Look at the list of securities held for large positions in risky securities.

- Is income largely from fees (more stable) or trading?

Issues for Finance Companies

Examine

- Expense Ratio = Expenses / Operating revenues

- Loans to Equity = Loans / Equity

- Return on Revenues = Net Income / Revenues

- Can be treated similar to banks in many ways because they provide loans, otherwise, use traditional ratios.

Issues for Real Estate Companies

- Focus on funds from operations = Earnings+Depreciation+Differed Taxes.

- Consider current value of real estate as market or discounted future income value, not book value.

- Short-term or variable rate debt used to fund real estate increases earnings risk.

Cash Flow Statement

Illustration of Inflows and Outflows

Inflows Outflows Operations Operations Cash Revenues Payment for Supplies Collection of A/R Wages, Rent, Tax, etc. Investments Investments Sell Securities, Assets Working Capital From Subsidiaries Capital Investments Financing Financing Issue Securities Pay Interest & Dividends Obtain Loan Repay Loans and Bonds Retire Equity

- Handout Cash Flow Statement or show on web.

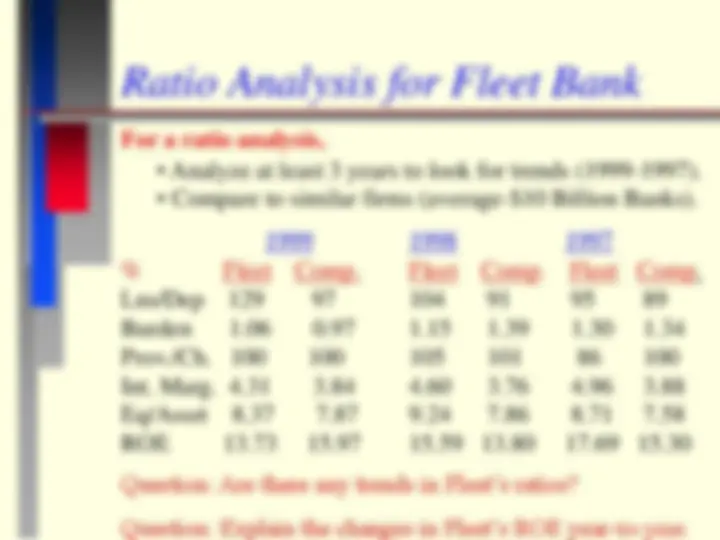

Ratio Analysis for Fleet Bank

For a ratio analysis,

- Analyze at least 3 years to look for trends (1999-1997).

- Compare to similar firms (average-$10 Billion Banks). 1999 1998 1997 % Fleet Comp. Fleet Comp. Fleet Comp. Lns/Dep 129 97 104 91 95 89 Burden 1.06 0.97 1.15 1.39 1.30 1. Prov./Ch. 100 100 105 101 86 100 Int. Marg. 4.31 3.84 4.60 3.76 4.96 3. Eq/Asset 8.37 7.87 9.24 7.86 8.71 7. ROE 13.73 15.97 15.59 13.80 17.69 15.

Question: Are there any trends in Fleet’s ratios?

Question: Explain the changes in Fleet’s ROE year-to-year.