IntroductiontoFinancial

StatementAnalysis

CHAPTER2

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

It will discuss the difference between book value of stockholders’ equity and market value of stockholders’ equity and explain why the two numbers are almost never the same.

Typology: Slides

1 / 38

This page cannot be seen from the preview

Don't miss anything!

Learning

Objectives

List

the

four

major

financial

statements

required

by the

for

publicly

traded

firms,

define

each

of^

the

four

statements,

and

explain

why

each

of

these

financial

statements

is^ valuable.

Discuss

the

difference

between

book

value

of^

stockholders’

equity

and

market

value

of^

stockholders’

equity;

explain

why

the

two

numbers

are

almost

never

the

same.

Compute

and

interpret

various

financial

ratios

Discuss

the

uses

of^

the

DuPont

identity

in^ disaggregating

and

assess

the

impact

of^

increases

and

decreases

in^ the

components

of^

the

identity

on^

Describe

the

importance

of^

ensuring

that

valuation

ratios

are

consistent

with

one

another

in^ terms

of^

the

inclusion

of^

debt

in^ the

numerator

and

the

denominator.

Firms’

Disclosure

of

Financial

Information

Financial

Statements ◦^ Firm

‐issued

accounting

reports

with

past

performance

information

◦^ Filed

with

the

SEC

◦^ 10Q

‐^ Quarterly ◦^ 10K

‐^ Annual ◦^ Must

also

send

an^

annual

report

with

financial

statements

to^ shareholders

Preparation

of^

Financial

Statements

◦^ Generally

Accepted

Accounting

Principles

(GAAP)

◦^ Auditor^ ◦^

Neutral

third

party

that

checks

a^ firm’s

financial

statements

Firms’

Disclosure

of

Financial

Information

Financial

Statements ◦^ Balance

Sheet ◦^ Income

Statement ◦^ Statement

of^ Cash

Flows

◦^ Statement

of^ Stockholders’

Equity

Global

Conglomerate

Corporation

Balance

Sheet

Net

Working

Capital

◦^ Current

Assets

Liabilities

Market

Value

Versus

Book

Value

◦^ Market

Value

of^ Equity

(Market

Capitalization)

◦^ Market

Price

per^

Share

x^ Number

of^ Shares

Outstanding

◦^ Cannot

be^ negative ◦^ Often

differs

substantially

from

book

value

Market

Value

Versus

Book

Value

◦^ Market

‐to‐

Book

Ratio

◦^ aka

Price

‐to‐Book

Ratio

◦^ Value

Stocks ◦^ Low

M/B

ratios

◦^ Growth

stocks ◦^ High

M/B

ratios

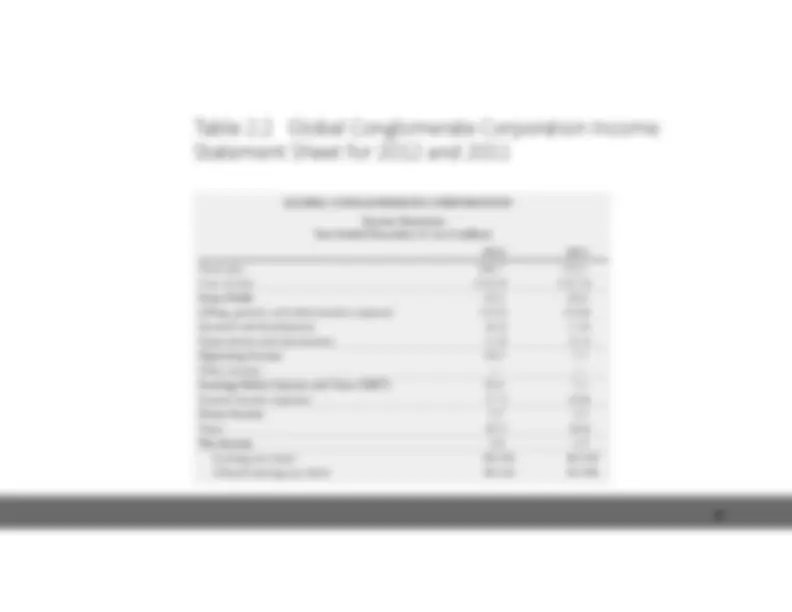

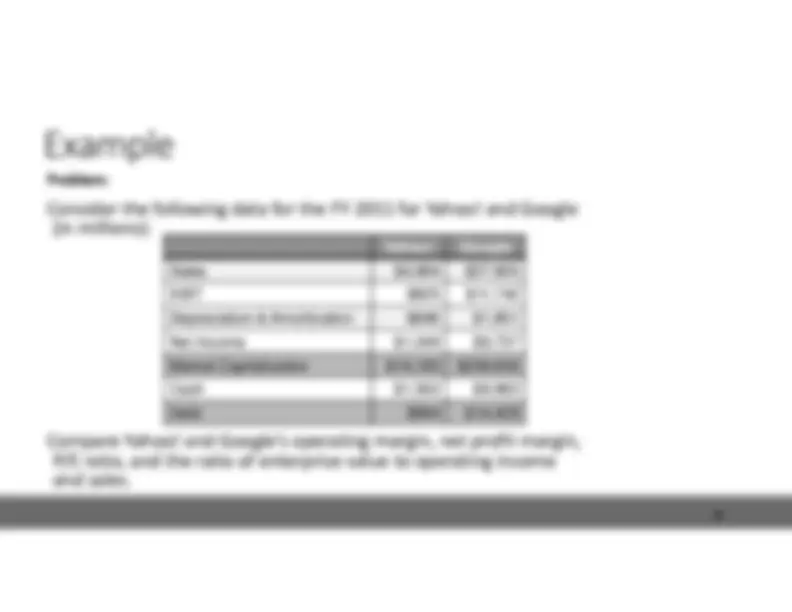

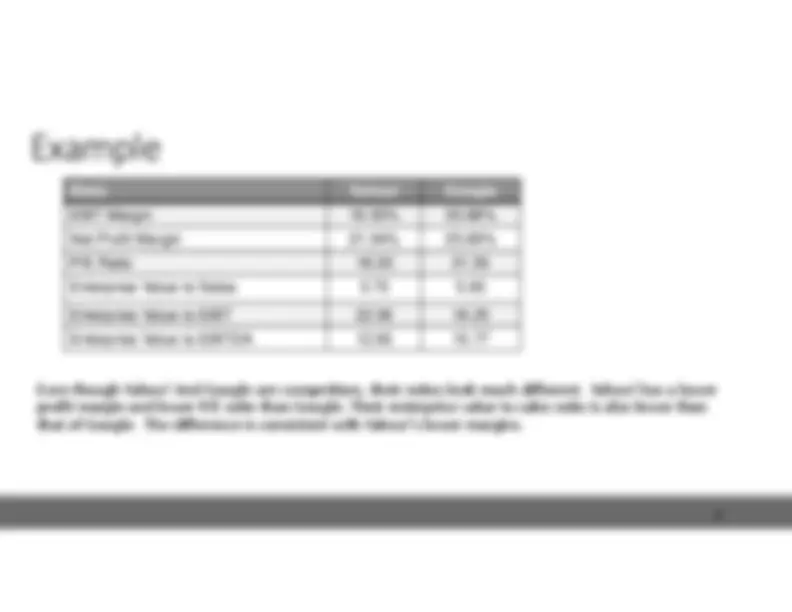

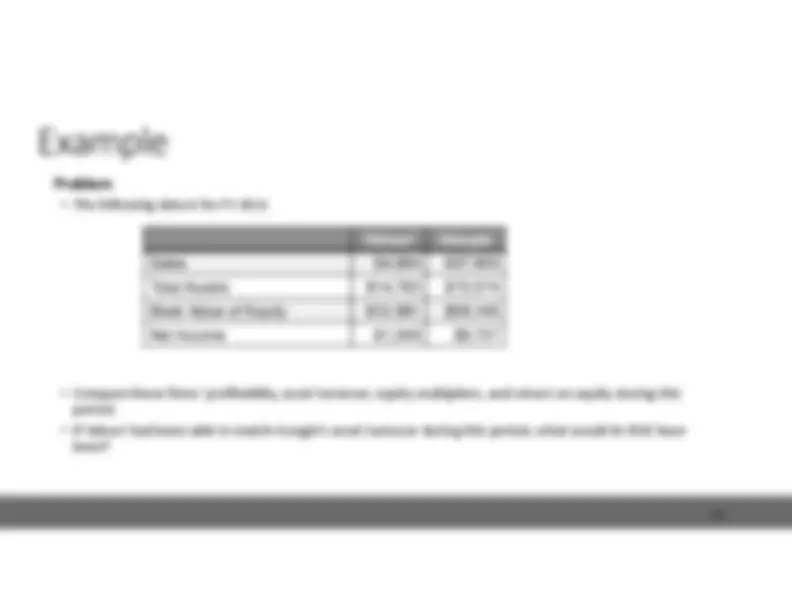

Table

Global

Conglomerate

Corporation

Income

Statement

Sheet

for

2012

and

2011

Income

Statement

Earnings

per

Share

Stock

Options Convertible

Bonds

Dilution^ ◦^ Diluted

EPS

Statement

of

Cash

Flows

Net

Income

typically

does

equal

the

amount

of^

Cash

the

firm

has

earned.

◦^ Non

‐Cash

Expenses ◦^ Depreciation

and

Amortization

◦^ Uses

of^ Cash

not

on^

the Income

Statement

◦^ Investment

in^ Property,

Plant,

and

Equipment

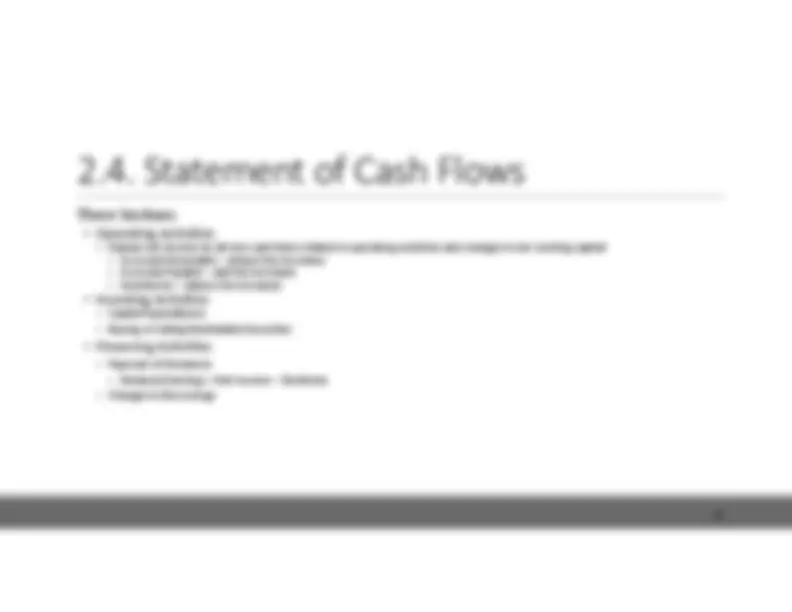

2.4.

Statement

of

Cash

Flows

Three

Sections ◦^ Operating

Activities ◦^ Adjusts

net^

income

by^ all

non

‐cash

items

related

to^ operating

activities

and changes

in^ net

working

capital

◦^ Accounts

Receivable

the^ increases

◦^ Accounts

Payable

the^

increases

◦^ Inventories

the^

increases

◦^ Investing

Activities ◦^ Capital

Expenditures ◦^ Buying

or^ Selling

Marketable

Securities

◦^ Financing

Activities ◦^ Payment

of^ Dividends ◦^ Retained

Earnings

=^ Net

Income

◦^ Changes

in^ Borrowings

Other

Financial

Statement

Information

Management

Discussion

and

Analysis

◦^ Off

‐Balance

Sheet

Transactions

Notes

to^

the

Financial

Statements

Financial

Statement

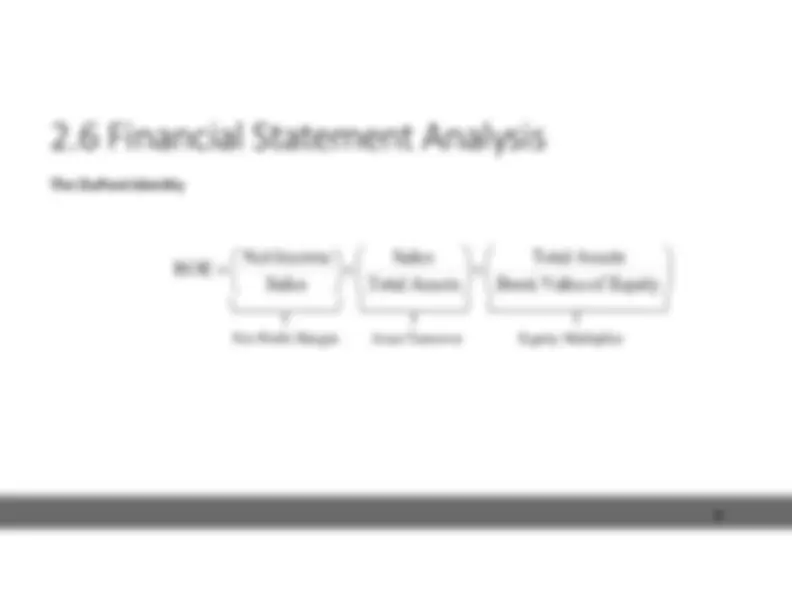

Analysis

Financial

Statement

Analysis

Working

Capital

Ratios

◦^ Accounts

Receivable

Turnover

◦^ Accounts

Payable

Turnover

◦^ Inventory

Turnover

Accounts Receivable Turnover ൌ

Annual Sales Accounts Receivable

Accounts Payable Turnover ൌ

Annual Cost of SalesAccounts Payable

Inventory Turnover ൌ

COGSInventory

Financial

Statement

Analysis

Working

Capital

Ratios

◦^ Accounts

Receivable

Days

◦^ Accounts

Payable

Days

◦^ Inventory

Days

Accounts Receivable Days ൌ

Accounts ReceivableAverage Daily Sales

ൌ^

AR ሺSales/365ሻ

Accounts Payable Days ൌ

Accounts Payable Average Daily Cost of Sales

=^

AP ሺCOGS

/ଷହሻ

Inventory Days ൌ

Inventory Average Daily Cost of Sales

ൌ^

InventoryሺCO365/ܵܩሻ