FINANCIAL STATEMENT ANALYSIS

UNIT IV

FINANCIAL MANAGEMENT

BBA 4 Semester

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

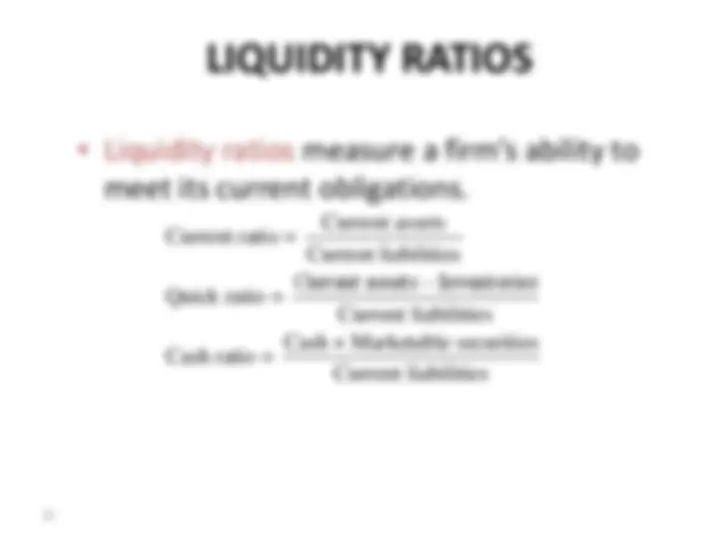

An in-depth exploration of essential financial statements, including the balance sheet, profit & loss statement, and cash flow statement. Learn about assets, liabilities, equity, current assets, fixed assets, current liabilities, long-term liabilities, and various financial ratios for liquidity, leverage, activity, and profitability analysis. Understand the role of financial analysis for stakeholders and the importance of trend analysis.

Typology: Study notes

1 / 49

This page cannot be seen from the preview

Don't miss anything!

BBA 4 Semester

Accounting profit is a result of the arbitrary allocation of expenditures between expenses (revenue expenditure) and assets (capital expenditure).

Economic profit is the net increase in the wealth of the firm, and it is measured in cash flow.