FOI 2556

Document 9

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

An analysis of the TVM (Tax Value Method) and its role in addressing the complexities and inadequacies of the current income tax legislation, specifically focusing on tax relief for capital expenditure. the historical context of income tax legislation, the implications of its complexity, and the potential benefits of the TVM in simplifying the tax system and reducing compliance costs.

Typology: Lecture notes

1 / 64

This page cannot be seen from the preview

Don't miss anything!

1. The Reform Context

TVMís context within tax reform

1.1 The following analysis explains how TVM fits within the broader tax reform context.

TVM as one part of the reform agenda

The ANTS reforms present an overall package.

The initial Review of Business Taxation (RBT) documents

identified a broad range of possible reforms for Australiaís

taxation system. The highest level aims of reform have been to

promote Australiaís economic growth, to strive for equity

between taxpayers and to promote simplicity and certainty within the taxation system.

Within the reform agenda, TVM addresses a specific part ñ income tax legislation.

The scope of reform covered by the broad heading of ëTax

Value Methodí is essentially the legislation governing income

tax, and the systems and processes that are built on that

legislation. Thus the reform covers the treatment of a major part of the tax base (income, as distinct from expenditure),

currently treated under many taxation regimes, expressed in

several thousand pages of legislation.

The proposed reformÖ

Some basic parameters help to define the scope of this area of

reform:

Öshould not alter the tax baseÖ

! the reform should not substantially change the income tax

base itself; that is, new legislation in this area should extend to the same range of income, expenditure, gains and

losses as are currently covered by income tax legislation;

Öshould not alter basic tax principlesÖ

! the reform should not touch the basic principles on which

the whole of the tax system is based ñ for example, it

should work within given structures such as annual taxation periods, and within the existing concepts of

taxable entities (other reform measures were designed to

Öbut its greatest impact is in combination with other reforms.

The greater potential of a reform of this kind is truly seen only

in the context of the whole reform agenda. A government of

any persuasion will identify opportunities to promote

economic growth by changing the tax treatment of certain kinds of business activities. (Several such reforms are included

in ANTS.

) However, within the current framework of income

tax legislation it is extremely difficult to introduce such

changes without making the system yet more complex and

uncertain. Moreover, any such change to the present system tends to create loopholes exploited by tax specialists, which

compromises the equity of the system on one hand, and

requires further complex legislative ëpatch-upsí on the other.

An effective reform to the structure of income tax legislation

would potentially allow present and future tax reforms aimed at economic growth outcomes to be put in place without

greatly increasing the complexity of tax law , and thereby with

significantly less potential for loopholes and the inequities they

bring.

Some fundamentals about an income tax system

1.2 All income tax systems establish the tax value of assets and liabilities. Tax value is not

a new concept, even if it is not always specifically recognised (e.g. the tax written down value

of a wasting asset equals its tax value).

1.3 Tax policy determines the incidence of taxation which, in turn, determines the tax

value of each asset and liability in a business. The reconciliation of accounting profit to

taxable income is the difference between the tax values of assets and liabilities and financial

(balance sheet) values of those assets and liabilities.

1.4 Changing tax policy brings about changes in tax outcomes (and, therefore, tax values).

Adopting a principle-based approach improves the equity and efficiency of the tax system.

What is a principle-based approach?

! Taxing transactions closer to their economic substance than their legal form.

! Taxing similar transactions in a similar manner, irrespective of their legal form.

! Symmetry in the tax recognition of income and expenses.

! Adopting standardised approaches.

1.5 If principle-based reforms are to be adopted, the argument for TVM is that it is the

most efficient, simplest and most transparent method of implementing it. The principle-based

approach leads to greater equity. TVM presents an opportunity for that to be achieved with

greater integrity and in fewer pages of legislation.

1.6 TVM is not the only method of achieving the desired result. Policy changes could be

incorporated into existing legislation, but at a substantial cost in terms of volume of

legislation and complexity. At the end, the tax value of assets and liabilities would be

identical with what is being proposed in TVM provided the more complex legislation could

deliver the intent. That is, the same outcome could be achieved but at a higher ongoing cost.

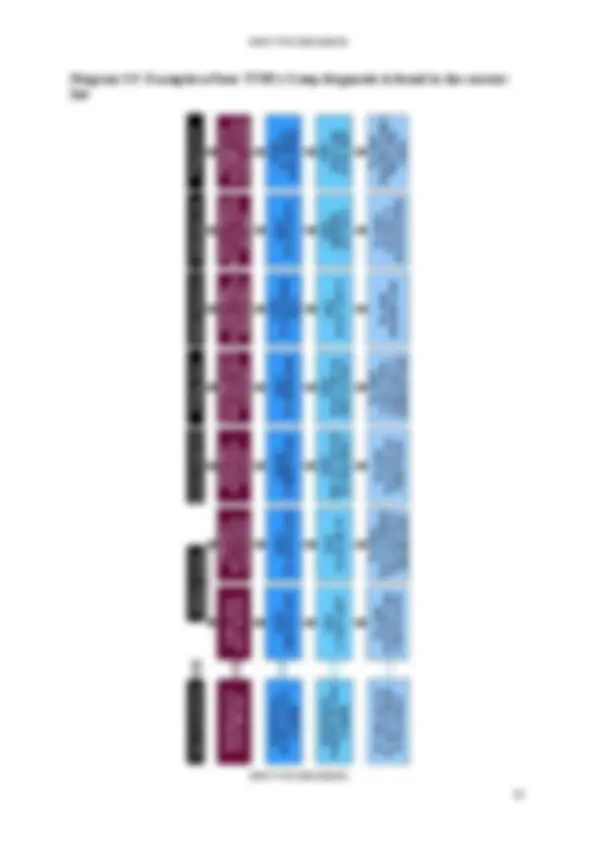

Diagram 2.1 The current system: systemic complexity caused by accretion

All business gains

Ordinary Statutory income income

Reclassification of gains to avoid tax

Reclassification of gains for better tax treatment

New regimes to extend the tax base

Business gains still not covered under income tax legislation

Extra legislation to deal with overlaps

Almost all $ $ business gains are part of the tax base

Continuing reclassification of assets to avoid tax

New areas of business activity create new classes of assets

All business expenses

General deductions linked to ordinary income

Other allowable deductions

New regimes for allowable deductions

Black hole expenditure

Some black holes remain

New kinds of business expense

Coverage of business expenses is almost universal

First Australian Income Tax Act (24 pages)

Income Tax Assessment Act (81 pages)

Gradual process of additions and amendments

legislation and other reforms (1400 pages)

Accelerating amendment process

Income Tax Assessment Act (4300 pages)

2.5 Two themes present in the earliest Australian income tax legislation have major

implications for the complexity of legislation that we have today:

ëordinary incomeí and some limited ëstatutory incomeí.

Both of these were basically limited to revenue items, based on the judicial distinction

between revenue and capital.

2.6 To these 2 themes we could add an absent theme ñ one that is not present in the early

framework, but has become a source of complexity since that time because of the extension of

the tax base to recognise most gains and, post-RBT, most losses:

for recognition of those gains and losses.

2.7 The bulk of our present legislation has been built on a framework that included these

basic features.

2.8 Under the first of these features, we have seen a gradual extension of the income tax

base by a series of new tax regimes and amendments to existing law. At present, the intended

tax base is almost universal ñ i.e. practically all business gains are intended to be assessable

for income tax. But the legislation covers this tax base like a patchwork quilt: new patches

cover new kinds of business gain, and extra patches repair conflict and uncertainty between

regimes. This complex patchwork might be reasonable if the final result was a clear and

unambiguous coverage of all business gains. But it is not. Ambiguity still remains, so that the

tax treatment of some business activity is unclear and subject to dispute. Further, the

patchwork quilt can never cover all gains in a certain way, because it is always possible that

new forms of business gains will emerge that we cannot yet imagine.

2.9 From the second and third features has evolved an asymmetric treatment of gains and

losses (or assets and liabilities) in business activities. In fact, within the current framework, a

business must translate the normal concepts of liabilities and losses into a quite different tax

concept of ëdeductionsí. And while the tax base has expanded to become almost universal

over the past 80 years or so, an expansion of the concept of ëallowable deductionsí followed

hand-in-hand, but with its own series of regimes and amendments. In the current system, most

assets and gains by business are taxable, and most losses and liabilities are deductible,

but

the 2 sides of the equation usually speak, as it were, entirely different languages, despite their

economic similarity.

2.10 From the third feature ñ the lack of a timing principle in the early legislation ñ has

grown the need to specify timing in many of the new regimes and amendments. The timing of

taxation can be an important point of leverage for business, so much effort (legitimate and

otherwise) goes into seeking the best tax treatment for many business activities. As above, if

the result of the current legislation was a clear treatment of timing for all kinds of business

activity, its complexity would pose no great problem. However, this is not the case, and

questions about classification of gains and losses continues to burden business, tax

administrators, legislators and policy makers.

2.11 Taking this historical perspective of our current income tax system highlights 2 kinds

of complexity, one necessary and useful, and the other simply a result of an unprincipled

evolution of legislation.

2.12 The necessary complexity relates to the variety of business activities. Some categories

of activity need special taxation treatment, according to government policy. This will always

be the case, and therefore complex questions will always be present regarding the

classification of certain actions.