Download FOR WHOM CORPORATE LEADERS BARGAIN and more Exercises Corporate Finance in PDF only on Docsity!

1467

FOR WHOM CORPORATE LEADERS

BARGAIN

LUCIAN A. BEBCHUK,*^ KOBI KASTIEL†^ & ROBERTO TALLARITA‡

ABSTRACT

At the center of a fundamental and heated debate about corporate purpose, an increasingly influential view (which we refer to as “stakeholderism”) advocates giving corporate leaders increased discretionary power to serve all stakeholders and not just shareholders. Supporters of stakeholderism argue that its application would address growing concerns about the impact of corporations on society and the

- James Barr Ames Professor of Law, Economics, and Finance, and Director of the Program on Corporate Governance, Harvard Law School; B.A. 1977, University of Haifa; LL.B 1979, University of Tel Aviv; LL.M 1980, Harvard Law School; S.J.D. 1984, Harvard Law School; M.A. 1992, Harvard University; Ph.D. 1993, Harvard University. † Assistant Professor, Tel Aviv University Faculty of Law; Senior Research Fellow, Program on Corporate Governance, Harvard Law School; B.A. 2005, Tel Aviv University; LL.B 2005, Tel Aviv University; LL.M 2008, Harvard Law School; S.J.D. 2016, Harvard Law School. ‡ Lecturer on Law, Terence M. Considine Senior Fellow in Law and Economics, and Associate Director of the Program on Corporate Governance, Harvard Law School; J.D. 2003, Sapienza University of Rome. Presentation slides summarizing this Article’s analysis are available at Lucian A. Bebchuk, Kobi Kastiel & Roberto Tallarita, For Whom Corporate Leaders Bargain: Presentation Slides (July 7, 2021), https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3881969 [https://perma.cc/U7ZT-4E9H]. We have benefitted from discussions with and suggestions from many individuals including Bob Clark, Bob Eccles, Alex Edmans, Chris Havasy, Leo Strine, René Stulz, and Andrew Tuch. We are also grateful for the comments and questions of conference and workshop participants at Columbia Law School, Harvard Law School, the Corporate Law Academic Webinar Series, the Stigler Center at the University of Chicago, Oxford University, Northeastern University, and Tel Aviv University, the 2021 Global Corporate Governance Colloquium, and the 2021 National Business Law Scholars Conference. We also gratefully acknowledge the excellent research assistance of Maya Ashkenazi, Aaron Haefner, Tamar Groswald Ozery, Zoe Piel, Tom Schifter, and Wanling Su. We are especially grateful to Roee Amir for his invaluable and critical research assistance throughout our work on this Article. The Harvard Law School Program on Corporate Governance and the John M. Olin Center for Law, Economics and Business provided financial support. This Article is part of the research project on stakeholder capitalism of the Harvard Law School Program on Corporate Governance. Companion articles written as part of the project are: Lucian A. Bebchuk & Roberto Tallarita, The Illusory Promise of Stakeholder Governance , 106 CORNELL L. REV. 91 (2020); Lucian A. Bebchuk & Roberto Tallarita, Will Corporations Deliver Value to All Stakeholders? , 75 VAND. L. REV. (forthcoming May 2022), https://papers.ssrn.com/sol3/papers.cfm?abstract_id= 421 [https://perma.cc/H6NC-J82B].

1468 SOUTHERN CALIFORNIA LAW REVIEW [Vol. 94: 1467 environment. By contrast, critics of stakeholderism argue that corporate leaders should not be expected to use expanded discretion to benefit stakeholders. This Article presents novel empirical evidence that can contribute to resolving this key debate. Following a stakeholderist framework, the constituency statutes adopted by more than thirty U.S. states authorize corporate leaders to give weight to stakeholder interests when considering a sale of their company. Using hand-collected data, we study how corporate leaders in fact used their stakeholderist discretion in transactions governed by such statutes in the past two decades. In particular, we provide a detailed analysis of more than one hundred transactions governed by such statutes in which corporate leaders negotiated a company sale to a private equity buyer. We find that corporate leaders used their discretion to obtain gains for shareholders, executives, and directors. However, despite the clear risks that private equity acquisitions often posed for stakeholders, corporate leaders generally did not use their discretion to negotiate for any stakeholder protections. Indeed, in the small minority of cases in which some stakeholder protections were formally included, they were generally cosmetic and practically inconsequential. Beyond the implications of our findings for the long-standing debate on constituency statutes, these findings also provide important lessons for the ongoing debate on stakeholderism. At a minimum, stakeholderists should identify the causes for constituency statutes’ failure to deliver stakeholder benefits in the analyzed transactions and examine whether embracing stakeholderism would not similarly fail to produce such benefits. After examining alternative explanations for our findings, we conclude that the most plausible explanation lies in corporate leaders’ incentives not to protect stakeholders beyond what would serve shareholder value. Our findings thus indicate that stakeholderism cannot be relied on to produce its purported benefits for stakeholders. Stakeholderism therefore should not be supported as an effective way for protecting stakeholder interests, even by those who deeply care about stakeholders. TABLE OF CONTENTS INTRODUCTION .................................................................................. 1470 I. THE STAKEHOLDERISM DEBATE .............................................. 1478 A. A CRITICAL JUNCTURE ................................................................. 1478 B. THE SUPPORT FOR STAKEHOLDERISM .......................................... 1480 C. THE AGENCY CRITIQUE OF STAKEHOLDERISM ............................ 1481 D. ALTERNATIVE VERSIONS OF STAKEHOLDERISM .......................... 1483

1470 SOUTHERN CALIFORNIA LAW REVIEW [Vol. 94: 1467 “ Each of our stakeholders is essential. We commit to deliver value to all of them.... ” — Business Roundtable’s Statement on the Purpose of a Corporation (August 19, 2019) 2 “ Those who cannot remember the past are condemned to repeat it .” — George Santayana, The Life of Reason or the Phases of Human Progress (1905)^3 INTRODUCTION In the face of growing concerns about the effects of corporate decisions on nonshareholder constituencies, there has been increasing support for stakeholderism.^4 By “stakeholderism” we refer to the view, which has also been labeled “stakeholder governance” or “stakeholder capitalism,” according to which corporate leaders should be given discretion to serve non- shareholder constituencies, not just shareholders.^5 The term “stakeholders” refers throughout this Article to all nonshareholder constituencies, including employees, customers, creditors, suppliers, local communities, the environment, and society at large. Stakeholderism has been attracting increasing support not only from reformers concerned about stakeholders,^6 but also from business leaders and corporate advisors.^7 In August 2019, the chief executive officers (“CEOs”) of over 180 major public companies, issued the Business Roundtable Statement on the Purpose of a Corporation, in which they committed to deliver value to all stakeholders.^8 As of July 2021, companies led by the signatories of the Business Roundtable’s statement had a market capitalization of more than $20 trillion.^9 The World Economic Forum subsequently published a manifesto urging companies to move from the traditional model of shareholder capitalism to a model of stakeholder

- Business Roundtable Redefines the Purpose of a Corporation to Promote ‘an Economy that Serves All Americans , ’ BUS. ROUNDTABLE (Aug. 19, 2019), https://www.businessroundtable.org/ business-roundtable-redefines-the-purpose-of-a-corporation-to-promote-an-economy-that-serves-all-am ericans [https://perma.cc/W88D-RBDH].

- GEORGE SANTAYANA, THE LIFE OF REASON: OR THE PHASES OF HUMAN PROGRESS 284 (1905).

- See infra Sections I.A–B.

- See infra notes 36 – 39 and accompanying text.

- See infra notes 31 – 33 and accompanying text.

- See Business Roundtable Redefines the Purpose of a Corporation to Promote ‘an Economy that Serves All Americans , ’ supra note 2.

- See id.

- Market capitalization data as of July 31, 2021, for each U.S. publicly traded signatory company was collected from Compustat.

2021] FOR WHOM CORPORATE LEADERS BARGAIN 1471 capitalism.^10 Critics, however, worry that corporate leaders do not have incentives to use their discretion to protect stakeholders and therefore should not be expected to do so.^11 In particular, a companion article by two of us provides a detailed agency critique of stakeholderism based on an analysis of the array of incentives that corporate leaders face.^12 This analysis concludes that corporate leaders have incentives not to protect stakeholders beyond what would serve shareholder value.^13 In this view, acceptance of stakeholderism would be counterproductive: rather than protecting stakeholders, stakeholderism would serve the private interests of corporate leaders by increasing their insulation from shareholder oversight and would raise illusory hopes that could deflect pressures to adopt laws and regulations protecting stakeholders.^14 In the debate between the stakeholderism view and the agency critique of this view, there lies a key empirical question: if corporate leaders are authorized and encouraged to protect stakeholder interests, as proponents of stakeholderism advocate, will they use their discretion to protect stakeholder interests? In this Article, we put forward novel empirical evidence that can contribute to answering this question, and thus advance the ongoing critical debate. Although stakeholderism has enjoyed unprecedented levels of support in recent years,^15 many states, during the era of hostile takeovers, adopted, and still retain to this day, constituency statutes that embrace an approach similar to that advocated by modern stakeholderists.^16 Proposed as a remedy to address the adverse effects of acquisitions on employees and other stakeholders, these statutes authorized corporate leaders to give weight to the interests of stakeholders when considering a sale of their companies.^17 The current debate on stakeholderism should be informed, we argue, by the

- See Klaus Schwab, Davos Manifesto 2020: The Universal Purpose of a Company in the Fourth Industrial Revolution , WORLD ECON. F. (Dec. 2, 2019) [hereinafter Schwab, Davos Manifesto 2020 ], https://www.weforum.org/agenda/2019/12/davos-manifesto- 2020 - the-universal-purpose-of-a-company- in-the-fourth-industrial-revolution [https://perma.cc/P8VW-XSTU]; see also Klaus Schwab, Why We Need the ‘Davos Manifesto’ for a Better Kind of Capitalism , WORLD ECON. F. (Dec. 1, 2019), https://www.weforum.org/agenda/2019/12/why-we-need-the-davos-manifesto-for-better-kind-of-capital ism [https://perma.cc/62J6-89ME].

- For articles expressing such concerns, see sources cited infra note 48.

- Lucian A. Bebchuk & Roberto Tallarita, The Illusory Promise of Stakeholder Governance , 106 CORNELL L. REV. 91 (2020).

- Id. at 92.

- Id.

- See infra notes 35 – 40 and accompanying text.

- For an account and discussion of the constituency statutes that are the focus of this paragraph, see sources cited infra notes 57 – 58.

- See infra text accompanying note 58.

2021] FOR WHOM CORPORATE LEADERS BARGAIN 1473 We now turn to provide an overview of our analysis and some of the conceptual choices and challenges we faced. In Part I, we begin by discussing the importance of the debate on stakeholderism. We explain that the debate seems to have reached a critical juncture and briefly describe the positions of stakeholderists and their critics. In particular, we explain how the disagreement between them is substantially driven by their different expectations of corporate leaders’ use of discretion to protect stakeholder interests. As the discussion of Part I explains, our analysis engages with alternative versions of stakeholderism, based on different rationales as to why corporate leaders should give weight to stakeholder interests. Some supporters of stakeholderism argue that the purpose of the corporation is to advance the interests of all constituencies. Others urge companies to consider stakeholder interests because doing so serves the interests of shareholders, either because it induces stakeholders to invest in and contribute to the corporation’s success or because shareholders are interested not only in financial payoffs but also in stakeholder welfare. While these supporters vary in the rationale they use, they all support corporate leaders’ use of their discretion to protect stakeholder interests when negotiating an acquisition. Part II sets the stage for our empirical analysis. We first discuss the key role stakeholderist concerns played in the adoption of constituency statutes. We also provide an overview of the landscape and main features of constituency statutes. We then explain why private equity acquisitions of public companies provide a good setting for our empirical investigation. Because they move assets into the hands of managers with powerful incentives to maximize financial returns, these transactions often pose risks to stakeholders. Indeed, as we discuss, there is evidence that private equity acquisitions in general, and those in our sample in particular, pose substantial risks for employees and local communities. Thus, given the risks that private equity acquisitions pose to stakeholders, corporate leaders who are willing to use their discretion to negotiate for stakeholder protections should be especially likely to do so in the context of private equity transactions. We note that we have also collected a sample of more than one hundred transactions in which strategic buyers acquired targets incorporated in states with constituency statutes and have found a similar pattern of general lack of stakeholder protections.^21 However, because we view private equity transactions as especially likely to pose risks to stakeholders, the lack of

- This sample was collected with the same methodology used to collect the sample examined in the Article, except for the typology of buyer. See infra Subsection III.A.1. The dataset is on file with the authors.

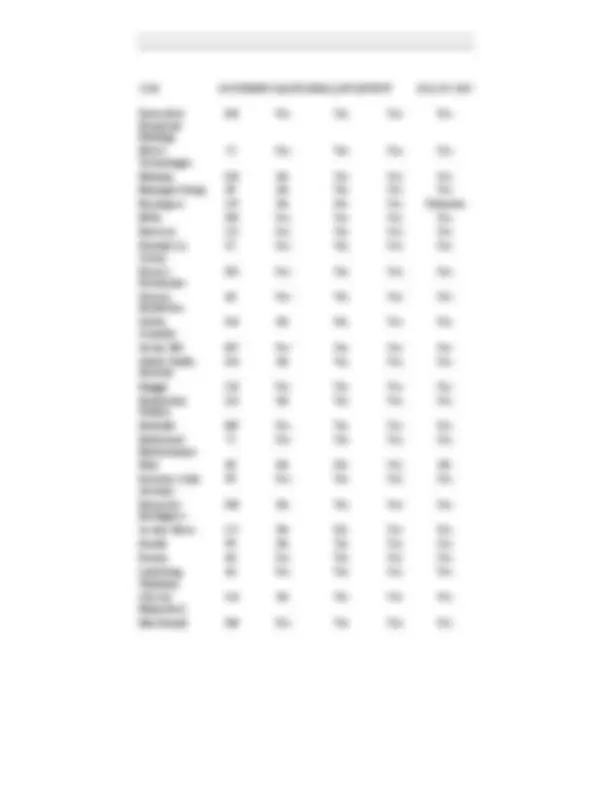

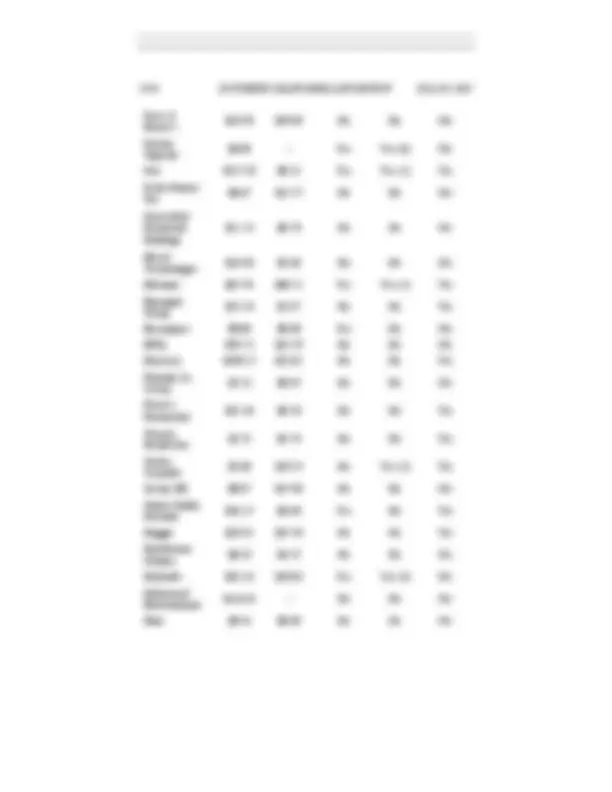

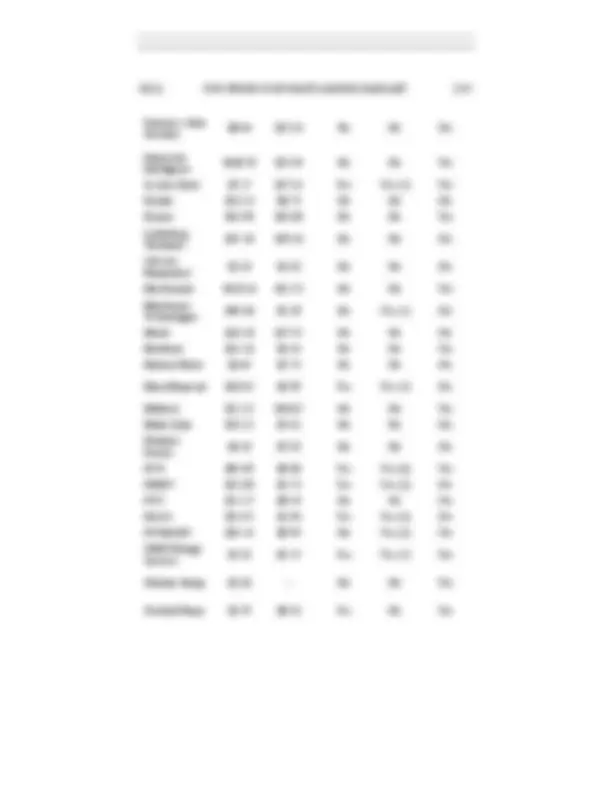

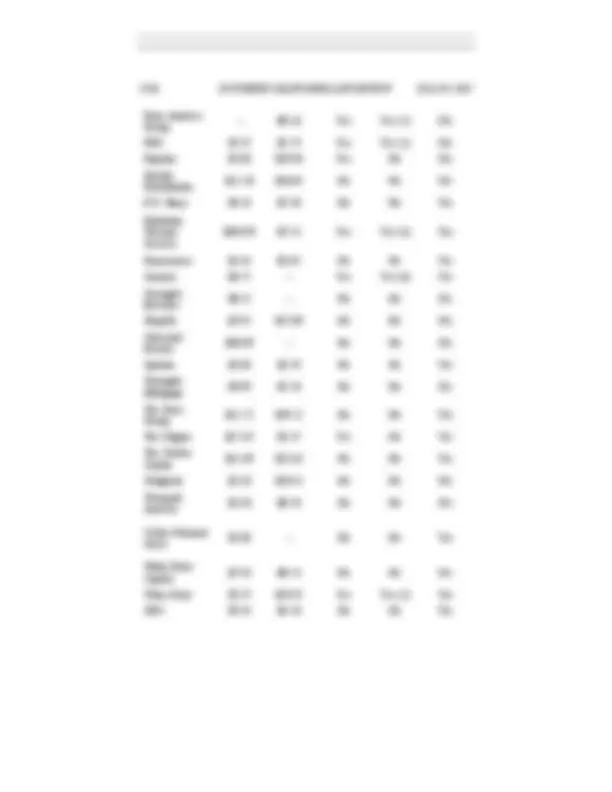

1474 SOUTHERN CALIFORNIA LAW REVIEW [Vol. 94: 1467 stakeholder protections in such transactions is especially telling, and we have therefore chosen to focus on these transactions. Part III presents our empirical analysis. In Section III.A, we discuss our data collection efforts and the universe of deals that we studied. We focus on the twenty-year period of 2000 through 2019, examining all transactions during this period in which a private equity buyer acquired a public company of significant size that was incorporated in a state with a constituency statute. Our sample includes 110 acquisitions of companies incorporated in seventeen states. Section III.B examines several dimensions of the bargaining process and shows that the terms of the acquisition agreements were generally the result of substantial negotiations. Section III.C and Section III.D examine what the negotiations obtained for shareholders and corporate leaders, respectively. Shareholders received substantial financial gains, enjoying sizable premiums over the pre-deal stock price. In addition to the gains made on their own equity holdings, corporate leaders also frequently secured additional payments in connection with the transactions and often obtained commitments for continued employment after the acquisition.^22 In Section III.E, we take up the central question of what corporate leaders obtained for stakeholders. We document that, despite the clear risks to stakeholders posed by the expected transfer of control to a private equity buyer, corporate leaders generally did not negotiate for any stakeholder benefits or any constraints on the post-deal power of the private equity buyer to make choices that would adversely affect stakeholders. Labor unions were induced to support constituency statutes because they were seen as an instrument to address concerns about layoffs and reduced employment,^23 and the evidence indicates that private equity buyers often reduce employment.^24 Nonetheless, we found that corporate leaders did not negotiate for any restrictions on post-deal layoffs in the vast majority of the transactions in our sample. Furthermore, in the tiny number of cases in which we found such restrictions, their presence was largely cosmetic because the terms of the acquisition agreement chose to deny employees any power to enforce these constraints.

- As we discuss in Subsection III.D.2, due to the focus of our inquiry, we do not examine the extent to which the benefits to corporate leaders themselves came at the expense of shareholders. Finding that shareholders do obtain a substantial fraction of the gains produced by the transactions, we focus on whether stakeholders get to participate in these gains as well. Given this focus, the question of how corporate leaders choose to allocate the gains between shareholders and themselves is not one that we need to consider for our central inquiry.

- See sources cited infra notes 82 – 85.

- See evidence cited infra notes 119 – 20 and accompanying text.

1476 SOUTHERN CALIFORNIA LAW REVIEW [Vol. 94: 1467 the general lack of stakeholder protections in transactions governed by constituency statutes, one can conclude that the statutes failed to produce such protections, as this conclusion holds regardless of whether such protections were also lacking in transactions not governed by such statutes. Finally, Part IV discusses the implications of our empirical analysis and findings. Section IV.A explains that the evidence we present enables us to reach a clear conclusion on the performance of constituency statutes: they failed to deliver the promised and hoped-for benefits for stakeholders. We then proceed to discuss the implications of our findings for the broad stakeholderism debate. Because constituency statutes had stakeholderist justifications and goals, all involved in the ongoing stakeholderism debate, stakeholderists should seek to learn from the experience with these statutes. Stakeholderists must wrestle with the failure of these statutes, identify the factors that caused it, and examine whether these factors would also undermine their current proposals. The most plausible explanation, we show, lies in corporate leaders’ incentives. Although the interests of corporate leaders do not perfectly align with the interests of shareholders, the interests of corporate leaders and shareholders are substantially linked.^26 By contrast, there is no significant link between the interests of corporate leaders selling their companies and the post-sale interests of stakeholders. In fact, to the extent that stakeholder protections would constrain the buyer and thus be costly to it, the inclusion of such protections in the deal could result in somewhat lower gains for the shareholders and the corporate leaders. Thus, corporate leaders had no incentives to use their negotiating power—and indeed had incentives not to use this power—to negotiate for protections for stakeholders. Section IV.B then discusses several possible alternative explanations for and objections to our conclusion. In particular, we show that our findings cannot be attributed to five potential alternative explanations: the influence of shareholder-centric norms on corporate leaders, the need to obtain shareholder approval for the acquisition, uncertainty about the interpretation of the statutes, the shadow of the Delaware Revlon, Inc. v. MacAndrews & Forbes Holdings, Inc. doctrine (“the Revlon doctrine”),^27 and the peculiar incentives in final-period decisions. It might be argued that, although we do not detect any material concern for stakeholder interests in the universe of analyzed transactions, corporate leaders might have been motivated by such concerns to decline some

- For a detailed analysis of the array of incentives and market forces that align the interests of corporate leaders and shareholders, see Bebchuk & Tallarita, supra note 12 , at 139–55.

- Revlon, Inc. v. MacAndrews & Forbes Holdings, Inc., 506 A.2d 173 (Del. 1986).

2021] FOR WHOM CORPORATE LEADERS BARGAIN 1477 opportunities to sell the company to a private equity buyer. In particular, it might be hypothesized that, encouraged by the presence of a constituency statute, corporate leaders in many cases declined an opportunity to sell to a private equity buyer because of their concern that the acquisition would make some stakeholders worse off. However, our findings suggest that this hypothesis is implausible. If a potential private equity acquisition would produce overall efficiency gains but make some stakeholders worse off, stakeholder-oriented directors can negotiate for stakeholder protection rather than give up the potential acquisition gains altogether. In this way, those directors can secure the gains of the acquisition and benefit both shareholders and stakeholders.^28 Thus, if corporate leaders were often motivated by concerns that potential acquisitions could make some stakeholders worse off, we should expect to observe a significant number of transactions in which the acquisition does take place but with stakeholder protections that ensure that no stakeholders are made worse off. The lack of such protections in our universe of transactions is thus inconsistent with the hypothesis that corporate leaders are materially concerned about allowing an acquisition that would hurt stakeholders. Thus, the empirical findings of this Article highlight that considering the incentives of corporate leaders is critical for assessing the promise of stakeholderism. Stakeholderism is based on the premise that corporate leaders would use their discretion to substantially serve stakeholder interests. Our evidence indicates that, in the case of constituency statutes, this assumption was unwarranted, and more generally it casts doubt on whether stakeholderism should be expected to deliver its purported benefits for stakeholders. Finally, before proceeding, we would like to note that the evidence and conclusions of this Article are strongly reinforced by another research project that we are about to conclude. This project, which we title Stakeholder

- To illustrate, suppose that the acquisition of a company, with a market value of $400 million, produces aggregate gains of $150 million, including some cost savings arising from the layoff of 200 employees. Such gains can be distributed among the relevant parties in different ways. For example, the buyer might offer target shareholders a 25% premium for a total of $100 million, give target executives extra payments for a total of $10 million, and keep the residual gains of $40 million. If target leaders wish to mitigate the prospective harm for employees and are empowered by the constituency statutes to take employee welfare into consideration, they might reject the offer, thus saving 200 jobs. However, such decision would also result in the loss of $150 million gains. Alternatively, target leaders may obtain a commitment from the buyer to pay a substantial severance payment for each employee who is laid off (say, a year’s worth of salary, or $50,000 per employee) in exchange for a lower premium for shareholders. In this way, the buyer would still gain $40 million, target executives would still gain $ million, and target shareholders would receive a slightly lower premium of 22.5% (rather than 25%).

2021] FOR WHOM CORPORATE LEADERS BARGAIN 1479 Merrick Dodd.^31 Support for stakeholderism has over time been expressed by many prominent legal,^32 economic, and business scholars.^33 Nonetheless, until recently, the shareholder primacy view has commonly been more prevalent among both academics and practitioners.^34 In the past few years, however, stakeholderism has returned to the center of the corporate governance discourse, and the debate seems to have reached a critical juncture. In August 2019, the Business Roundtable—an influential association of corporate CEOs—issued a statement, signed by the CEOs of 181 major public companies, in which they committed to “lead their companies for the benefit of all stakeholders” and to “deliver value” not just to shareholders, but also to employees, customers, suppliers, and communities.^35 The statement has been hailed by many commentators as a radical change in the conception of corporate purpose and the harbinger of a major transformation in corporate governance practices.^36 The World Economic Forum similarly urged companies to move from the traditional model of “shareholder capitalism” to the model of

- For the articles in this exchange, see generally A. A. Berle, Jr., Corporate Powers as Powers in Trust , 44 HARV. L. REV. 1049 (1931); E. Merrick Dodd, Jr., For Whom Are Corporate Managers Trustees? , 45 HARV. L. REV. 1145 (1932); A. A. Berle, Jr., For Whom Corporate Managers Are Trustees: A Note , 45 HARV. L. REV. 1365 (1932).

- See generally, e.g. , LYNN STOUT, THE SHAREHOLDER VALUE MYTH (2012); Einer Elhauge, Sacrificing Corporate Profits in the Public Interest , 80 N.Y.U. L. REV. 733 (2005).

- See generally, e.g. , COLIN MAYER, PROSPERITY: BETTER BUSINESS MAKES THE GREATER GOOD (2018). The seminal defense of stakeholderism in management literature is R. EDWARD FREEMAN, STRATEGIC MANAGEMENT: A STAKEHOLDER APPROACH (1984).

- See, e.g. , STOUT, supra note 32 , at 21 (“[B]y the close of the millennium.... [m]ost scholars, regulators and business leaders accepted without question that shareholder wealth maximization was the only proper goal of corporate governance.” (alteration in original)); Henry Hansmann & Reinier Kraakman, The End of History for Corporate Law , 89 GEO. L.J. 439, 441 (2001) (“[T]here is convergence on a consensus that the best means to this end (that is, the pursuit of aggregate social welfare) is to make corporate managers strongly accountable to shareholder interests and, at least in direct terms, only to those interests.”).

- Business Roundtable Redefines the Purpose of a Corporation to Promote ‘an Economy that Serves All Americans , ’ supra note 2.

- See, e.g. , Alan Murray, America’s CEOs Seek a New Purpose for the Corporation , FORTUNE (Aug. 19, 2019, 1:30 AM), https://fortune.com/longform/business-roundtable-ceos-corporations-purpose [https://perma.cc/8BJE-JQRC] (“[T]he BRT [Business Roundtable] announced a new purpose for the corporation and tossed the old one into the dustbin.” (alteration in original)); David Gelles & David Yaffe- Bellany, Feeling Heat, C.E.O.s Pledge New Priorities , N.Y. TIMES, Aug. 20 , 2019, at A1 (stating that the Business Roundtable statement “[b]reak[s] with decades of long-held corporate orthodoxy” (alteration in original)). A more skeptical view regarding the significance of the Business Roundtable statement is offered in a recent Wall Street Journal op-ed by two of us. Lucian Bebchuk & Roberto Tallarita, ‘Stakeholder’ Capitalism Seems Mostly for Show , WALL. ST. J. (Aug. 6 , 2020, 7:07 PM), https://www.wsj.com/articles/stakeholder-capitalism-seems-mostly-for-show- 11596755220 [https://per ma.cc/BV4W-GFWZ].

1480 SOUTHERN CALIFORNIA LAW REVIEW [Vol. 94: 1467 “stakeholder capitalism.”^37 In addition, the Reporter and advisors for the American Law Institute are considering the introduction of stakeholderist elements into its ongoing project of Restatement of the Law, Corporate Governance.^38 These developments led observers to view 2019 as a “watershed year in the evolution of corporate governance” due to the “advent of stakeholder governance,”^39 and 2020 as a “decisive inflection point” in the stakeholderism debate.^40 B. THE SUPPORT FOR STAKEHOLDERISM The stakeholderism view holds that the welfare of each group of corporate stakeholders is relevant for a company’s purpose and valuable regardless of its effect on the welfare of shareholders. Therefore, corporate leaders should serve not only shareholders but a plurality of independent constituencies, and they should weigh and balance a plurality of autonomous ends.^41 An important corollary of the fact that the welfare of shareholders and the welfare of stakeholders are independent factors is that there could be cases in which corporate leaders may choose a stakeholder-friendly course of action even if it would prove costly to shareholders. With a stakeholderist approach, stakeholders could in theory receive a larger share of the value created by the corporation than with a shareholder primacy approach. This is, in fact, the goal of stakeholderism. In practice, stakeholderist proposals rely on the discretionary judgment of corporate leaders. It is up to directors and top executives to determine which groups should be considered stakeholders of the corporation, when a situation involves a potential trade-off between shareholders and some group of stakeholders, how to quantify and weigh the respective welfare gains or losses in such trade-offs (especially when they are not immediately or easily monetized, such as, for example, matters of job security, health and safety, or environmental issues), and how to resolve the trade-offs.^42

- See Schwab, Davos Manifesto 2020 , supra note 10 (“The purpose of a company is to engage all its stakeholders in shared and sustained value creation. In creating such value, a company serves not only its shareholders, but all its stakeholders... .”).

- The Reporter discussed this possibility in an N.Y.U. roundtable on December 6, 2019, attended by one of the authors. See also Laying Down the Law: Edward Rock Will Oversee Drafting of the First ALI Restatement on Corporate Governance , N.Y.U. L. (Apr. 5, 2019), https://www.law.nyu.edu/ news/ideas/edward-rock-ALI-corporate-governance-restatement [https://perma.cc/FJ2S-DU5A].

- Martin Lipton, Steven A. Rosenblum & Karessa L. Cain, Thoughts for Boards of Directors in 2020 , HARV. L. SCH. F. ON CORP. GOVERNANCE (Dec. 10, 2019), https://corpgov.law.harvard.edu/ 19/12/10/thoughts-for-boards-of-directors-in-2020 [https://perma.cc/B8V 6 - 2Y6R]. 40_._ Martin Lipton, Spotlight on Boards , HARV. L. SCH. F. ON CORP. GOVERNANCE (July 18, 2020), https://corpgov.law.harvard.edu/2020/07/18/spotlight-on-boards-7 [https://perma.cc/WQ4K-RNFZ].

- Bebchuk & Tallarita, supra note 12 , at 114–15. For a recent defense of stakeholderism, see MAYER, supra note 33 , at 39.

- Bebchuk & Tallarita, supra note 12 , at 121–23.

1482 SOUTHERN CALIFORNIA LAW REVIEW [Vol. 94: 1467 incentives to give substantial weight to the interests of shareholders and to their own interests but have no incentive to advance the interests of stakeholders beyond what is instrumentally beneficial to shareholders.^49 This critique of stakeholderism reflects an agency view that stresses that the behavior and choices of corporate leaders might be substantially influenced by their incentives and not just by the aspirations behind legal rules and principles. According to the agency view, at least under the existing structure of incentives, corporate leaders are unlikely to use the broad discretion granted to them in a stakeholderist arrangement in a way that would materially improve the welfare of stakeholders.^50 Even supposing that directors and CEOs were allowed to balance and trade off the interests of stakeholders with those of shareholders, why would they ever use this power in a way that would redistribute value from shareholders to one or more groups of stakeholders? Such a choice would be a strategic mistake for corporate leaders, whose compensation is in substantial part linked to the financial performance of the company,^51 and whose prospects in the job market (that is, the likelihood of retaining their positions or finding equivalent or better positions in another company) heavily depend on the company’s performance in terms of shareholder value.^52 Redistribution in favor of stakeholders would also, by definition, be harmful to shareholders, who are the only constituents legally empowered to appoint and replace directors and therefore the only parties who can directly reward or punish directors for their decisions. Therefore, corporate leaders who would choose to benefit stakeholders at the expense of their own or their shareholders’ interests would be acting contrary to their own interests and more likely to find themselves at a professional disadvantage. Hence, corporate leaders have no economic incentive to favor stakeholders at the expense of shareholders, and shareholders have no economic incentive to encourage this kind of choice. BUS. LAW. 321, 338 (2015); Leo E. Strine, Jr., The Dangers of Denial: The Need for a Clear-Eyed Understanding of the Power and Accountability Structure Established by the Delaware General Corporation Law , 50 WAKE FOREST L. REV. 761, 768 (2015); Jill E. Fisch & Steven Davidoff Solomon, Should Corporations Have a Purpose? 101, 123–27 (Eur. Corp. Governance Inst., Law Working Paper No. 510/2020, 202 1 ), https://ssrn.com/abstract=3561164 [https://perma.cc/E7AM-GSP3].

- Bebchuk & Tallarita, supra note 12 , at 147.

- Id. at 102. 51_. See, e.g._ , ALEX KNOWLTON, AMIT BATISH, ELIZABETH CARROLL, JOSEPH KIEFFER & HAILEY ROBBERS, EQUILAR, CEO PAY TRENDS 18 (Alex Knowlton & Courtney Yu eds. 2018); TONY MEYER, TRENDS AND DEVELOPMENTS IN EXECUTIVE COMPENSATION 1 – 2 (2018), https://www.merid iancp.com/insights/2018-trends-developments-executive-compensation [https://perma.cc/KB95-HGD7]. 52_. See generally, e.g._ , Steven N. Kaplan & Bernadette A. Minton, How Has CEO Turnover Changed? , 12 INT’L REV. FIN. 57 (2012); Dirk Jenter & Fadi Kanaan, CEO Turnover and Relative Performance Evaluation , 70 J. FIN. 2155 (2015).

2021] FOR WHOM CORPORATE LEADERS BARGAIN 1483 One crucial point of contention between stakeholderists and their critics is based on differing analyses of the forces that shape corporate decision- making. At the core of the dispute, however, lies a simple empirical question: if directors and executives are given the power to take into account the interests of stakeholders, as proponents of stakeholderism advocate, will these corporate leaders use this power to improve the welfare of stakeholders? In this Article, we seek to answer this question by observing the choices actually made by corporate leaders of companies subject to statutory rules that closely resemble those advocated by stakeholderists. D. ALTERNATIVE VERSIONS OF STAKEHOLDERISM The discussion above focused on a version of stakeholderism that is based on a conception of corporate purpose that incorporates stakeholder interests. Before proceeding, however, we would like to note two other prevailing justifications as to why corporate leaders negotiating a deal should give weight to stakeholder interests, and to explain why our empirical analysis in this Article speaks to them as well. First, under a long-standing view in the literature, corporate leaders should give weight to stakeholder interests, in general and in the context of an acquisition in particular, to fulfill an implicit promise toward stakeholders. This view was proposed in the 1980s in influential articles by Andrei Shleifer and Larry Summers, as well as by John Coffee.^53 Under this view, stakeholders could be induced to invest ex ante in the success of an enterprise if they expect to be treated well by corporate leaders ex post, including in the event of an acquisition offer. Therefore, so the argument goes, to support such expectations and ex-ante reliance by stakeholders, it is in the ex-ante interest of shareholders that corporate leaders act ex post to treat stakeholders better than they are legally required to do. Indeed, holders of this view have argued that this consideration provides a basis for management power over acquisitions, because such power enables them to protect stakeholder interests in an acquisition and is therefore in the ex-ante interest of shareholders.^54 Thus, holders of this view, 53_._ Andrei Shleifer & Lawrence H. Summers, Breach of Trust in Hostile Takeovers , in CORPORATE TAKEOVERS: CAUSES AND CONSEQUENCES 33 (Alan J. Auerbach ed., 1988); John C. Coffee, Jr., Shareholders Versus Managers: The Strain in the Corporate Web , 85 MICH. L. REV. 1 (1986); John C. Coffee, Jr., The Uncertain Case for Takeover Reform: An Essay on Stockholders, Stakeholders and Bust-Ups , 1988 WIS. L. REV. 435, 435 [hereinafter Coffee, Jr., Uncertain Case ]. For more recent work supporting the “implicit contract” theory, see William C. Johnson, Jonathan M. Karpoff & Sangho Yi, The Bonding Hypothesis of Takeover Defenses: Evidence from IPO Firms , 117 J. FIN. ECON. 307 , 310 (2015) (arguing that firms with greater need of ex-ante investment by stakeholders adopt more takeover defenses at IPO in order to facilitate the ex-post protection of stakeholders). 54_. See, e.g._ , Coffee, Jr., supra note 53 , at 108 (arguing that anti-takeover statutes are intended to serve stakeholder interests and can be defended on such a basis from a general welfare standpoint).

2021] FOR WHOM CORPORATE LEADERS BARGAIN 1485 equity firms pose substantial risks for some groups of stakeholders and therefore provide a context in which we can expect that stakeholder-oriented corporate leaders would be particularly active. A. CONSTITUENCY STATUTES

- The Promise of Constituency Statutes From the mid-1980s to the early 1990s, in response to a massive increase in hostile corporate takeovers, many U.S. states adopted statutes that strengthened the power of directors to fend off bidders. These anti-takeover laws included statutes explicitly permitting the use of “poison pills” against unwanted suitors, statutes preventing freeze-out mergers for a certain period after the acquisition of a significant stake in the company, and statutes requiring bidders to pay a “fair price” in the second part of a two-tier merger.^57 In this Article, we will focus on a specific type of anti-takeover legislation that took the form of an explicit experiment in stakeholderism. These statutes—often referred to as constituency statutes—authorized directors to consider the interests of employees and other stakeholders when assessing an acquisition offer.^58 Many statutes went even further and authorized directors to consider the interests of stakeholders when making any kind of decision.^59 Although Delaware, the most influential state for corporate governance,^60 retained a shareholder-centric view of corporate purpose,^61 a substantial majority of states adopted constituency statutes.^62 The purported motivation for such a remarkable legal innovation was to protect employees, local communities, and possibly the economy at large

- For a discussion of state anti-takeover laws, see Michal Barzuza, The State of State Antitakeover Law , 95 VA. L. REV. 1973 , 1988 & n.44 (2009).

- For a general overview of these statutes, see generally Comm. on Corp. L., Bus. L. Section, Am. Bar Ass’n, Other Constituencies Statutes: Potential for Confusion , 45 BUS. LAW. 2253 ( 1989 ); Eric W. Orts, Beyond Shareholders: Interpreting Corporate Constituency Statutes , 61 GEO. WASH. L. REV. 14 (1992); Stephen M. Bainbridge, Interpreting Nonshareholder Constituency Statutes , 19 PEPP. L. REV. 971 (1992); Jonathan D. Springer, Corporate Constituency Statutes: Hollow Hopes and False Fears , 1999 ANN. SURV. AM. L. 85; Barzuza, supra note 57. Other labels that have been used for these statutes are “other constituencies statutes” and “stakeholder statutes.” See, e.g. , Comm. on Corp. L., supra ; Orts, supra , at 17 n.18.

- For the various structures and provisions of the constituency statutes, see infra Subsection II.A.2. 60_. See_ Martin Lipton & Steven A. Rosenblum, A New System of Corporate Governance: The Quinquennial Election of Directors , 58 U. CHI. L. REV. 187, 191 n.6 (1991) (“Because about 50 percent of the major public companies are incorporated in Delaware, the Delaware courts, more than any others, have been compelled to be the judicial arbiters of the corporate governance debate.”).

- See Coffee, Jr., Uncertain Case , supra note 53 , at 436 & n.3 (noting that Delaware passed weak anti-takeover legislation in 1988).

- See infra note 90.

1486 SOUTHERN CALIFORNIA LAW REVIEW [Vol. 94: 1467 from the adverse effects of hostile acquisitions.^63 This theory occupied a central place in the contemporaneous works of lawyers and academics.^64 For example, Martin Lipton—who very early on contended that takeovers threatened the welfare of stakeholders and that directors should be able to reject a takeover offer on the grounds of concern for stakeholders^65 — welcomed the adoption of constituency statutes as a way for directors to protect nonshareholder constituencies.^66 Steven Wallman, another prominent lawyer and a drafter of the Pennsylvania constituency statute, observed that many takeovers resulted in a transfer of wealth from stakeholders to shareholders, and that constituency statutes allowed directors to reject those deals, thus benefitting employees and other stakeholders who could not easily protect themselves.^67 The perception of the policy rationale behind the constituency statutes and other anti-takeover laws was summarized by Lyman Johnson and David Millon during the wave of enactments: [T]heir [state anti-takeover laws’] chief purpose is to protect non shareholders from the disruptive impact of the corporate restructurings that are thought typically to result from hostile takeovers. Rightly or wrongly, state legislators perceive that hostile takeovers cause lost jobs, destruction of established supplier and customer relationships, and loss of tax revenues and charitable contributions.^68 At the very least, hostile acquisitions were thought to be causing a geographical redistribution of wealth away from areas of the country traditionally dependent on manufacturing jobs.^69 By allowing corporate decisionmakers to consider the effects of an acquisition on employees, suppliers, and the local community, constituency statutes explicitly sought to mitigate or eliminate the threats that takeovers posed to local jobs. The view that takeovers often damaged stakeholders found some support in economic literature.^70 While the increasingly dominant theory was

- See infra text accompanying note 68.

- See infra text accompanying notes 65 – 68.

- Martin Lipton, Takeover Bids in the Target’s Boardroom , 35 BUS. LAW. 101, 122– 23 (1979) (“It is reasonable for the directors of a target to reject a takeover on... [the grounds that it would have an] adverse impact on constituencies other than the shareholders... .” (alteration in original)).

- See Lipton & Rosenblum, supra note 60 , at 215.

- Steven M.H. Wallman, Corporate Constituency Statutes: Placing the Corporation’s Interests First , BUS. LAW. UPDATE, Nov./Dec. 1990, at 1, 2. 68_._ Lyman Johnson & David Millon, Missing the Point About State Takeover Statutes , 87 MICH. L. REV. 846, 848 (1989) (alteration in original).

- Coffee, Jr., Uncertain Case , supra note 53 , at 436–37. Perhaps for this reason, some “states— particularly those in the ‘Rustbelt’ extending through New York, Pennsylvania, Ohio, Indiana, Wisconsin and Minnesota—have become protective havens for target corporations, while the Congress has tended more towards neutrality.” Id. at 436.

- See infra note 74 and accompanying text.