Download Globalization and Fiscal Decentralization: An Unexpected Relationship and more Papers German Philology in PDF only on Docsity!

Globalization and Fiscal Decentralization

Geoffrey Garrett Yale University PO Box 208343^ EPE Program New Haven, CT 06520-8343Yale University E-mail: [email protected]: (203) 436- Fax: (203) 436-

Jonathan Rodden MIT Department of Political ScienceE53- 77 Massachusetts AvenueCambridge, MA 02139 E-mail: [email protected]: (617) 253- Fax: (617) 258-

Prepared for delivery at the Conference: Globalization and Governance The Grande Colonial Hotel, La Jolla, CAMarch 30-31, 2001 Draft 2, Completed March 15, 2001

Globalization and Fiscal Decentralization^1

I. Introduction

The decentralization of authority to state and local governments and the international integration of markets are widely perceived as two defining trends of the contemporary era. This paper asks whether the two are causally connected: has globalization caused decentralization? Several plausible pathways have been proposed, but the most prominent and well-developed argument asserts that the international integration of markets has facilitated decentralization by reducing the economic costs of smallness (Alesina & Spolaore 1997, Bolton & Roland 1997). Larger units allow for scale economies in the production of public and private goods, but they also reduce the scope for localities and regions with distinctive preferences to pursue their own political and economic strategies. Free trade and capital movements reduce the costs of going it alone, freeing smaller units to pursue their own destinies. The primary purpose of this paper is to show that using one natural indicator of political economic authority – the balance of taxing and spending between central governments and state and local governments – international market integration has been associated with fiscal centralization, rather than decentralization. There are several reasons why this might be the case. It may become more costly for the central

(^1) Without implicating them, the authors wish to thank conference participants and UCSD, the Midwest Political Science Association, and the American Political Science Association along with the followingindividuals for helpful comments: Carles Boix, Kelly Chang, Lucy Goodhart, Pieter van Houten, Miles Kahler, David Lake, Robert Powell, Beth Simmons, and Richard Steinberg.

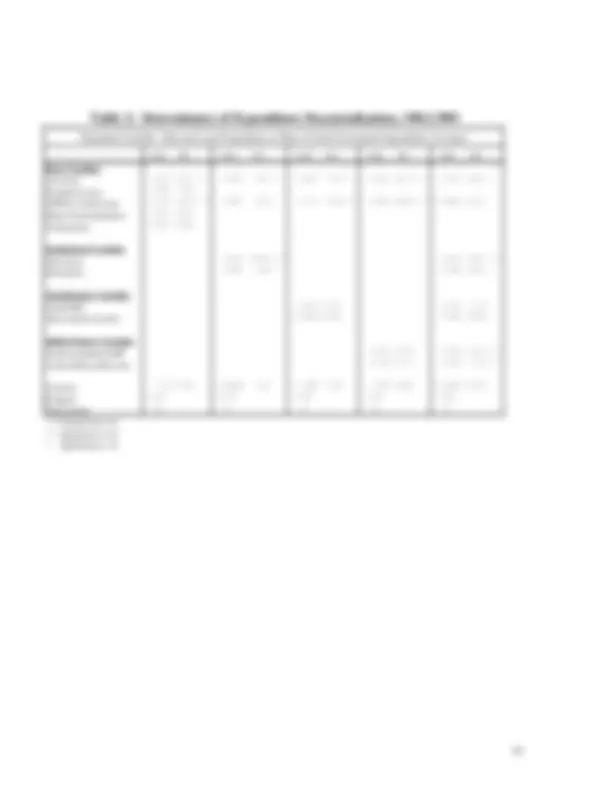

expenditures. Table 1 provides an overview of countries for which yearly expenditure data have been available for most of the last two decades.^2 Averages for the period from 1982 to 1989 and for 1990 to 1997 are shown in the first two columns. This cut-off is useful because several countries underwent transitions to democracy in the late 1980s, and by all accounts, global economic integration has increased substantially after 1990. The countries displayed in Table 1 demonstrate a good deal of variation in vertical fiscal structure. They range from heavily decentralized Canada and the United States, for which more than half of all government expenditure takes place at subnational levels, to countries like Paraguay or Thailand, where less than ten percent of total expenditure is done by subnational governments.

[TABLE 1 ABOUT HERE]

For our purposes, the right-hand column in Table 1 is the most important. It shows that fiscal decentralization was by no means a universal phenomenon in the 1990s. Some countries—in fact nearly half of the sample—became more centralized. But on the other hand, some countries —most notably Brazil, Mexico, Peru, and Spain— considerably decentralized expenditures between the 1980s and 1990s (by more than 10 percent of total expenditures). The question is whether and how these differences correlate with the extent of international market integration in these countries The remainder of the paper is divided into six sections. The second section begins with a general overview of the literature on fiscal decentralization. Section three

(^2) All public finance data are taken from the IMF Government Finance Statistics Yearbook, various years. Most of the averages shown in Table 1 are for the entire period specified, but because of missing data,

then reviews new arguments positing a link between globalization and decentralization. We offer a critique and alternatives to these arguments in section four, arguing that there are good reasons to believe that globalization should promote fiscal centralization. Our empirical tests of these contending perspectives are presented in sections five (based on cross-section averages) and six (using time-series cross-sectional data). The concluding section draws out some broad lessons and maps out an agenda for further research.

II. The Determinates of Decentralization

This section reviews some old and new arguments about the determinants of decentralization. We begin with existing arguments about essentially invariant factors that likely affect overall levels of decentralization. In these arguments, levels of decentralization are viewed as long-run efficient responses to demands made by investors and voters. We then move on to discuss the effects of democracy and federalism – two institutional factors that might affect both cross-national and diachronic variations in decentralization. Finally, we discuss the possibility that decentralization is a result of opportunistic attempts by central governments to balance their budgets on the backs of local governments.

Preference Heterogeneity Previous theoretical and empirical studies of decentralization have focused on basic underlying characteristics of societies that might affect the costs and benefits of adopting a decentralized fiscal system (Oates, 1972; Panizza, 1999; Diaz-Cayeros 2000).

some of the averages reflect slightly shorter periods.

descriptive political science literature on transitions to democracy (Haggard 1999). In many cases, regional elites have played important roles in the protests and negotiations that have led to democratic transitions. In such new democracies, decentralization is often an attractive political strategy for reelection-seeking politicians who wish to build or consolidate local bases of support (O’Niell 2000).

Levels of fiscal decentralization might also be influenced by the presence of federal political institutions. Above all, federal systems are distinct from unitary systems in that they provide formal or de facto veto authority to regional politicians over all or some subset of federal policy decisions (Rodden 2000). In most cases this is accomplished through special constitutional protections and amendment procedures and an upper house that disproportionately represents the regions. It seems likely that such institutions will allow subnational officials to bargain for a larger share of the public sector’s resources than their counterparts in unitary systems.

Strategic Deficit-Shifting Whether demands for (de)centralization come from voters, investors, or multilateral lending agencies, these demands are only transformed into policy if they are compatible with the incentives of the central government. Decentralization does not simply happen—it is a strategic choice made by self-interested politicians. Central government officials may face incentives for decentralization that have little to do with the demands of voters, investors, or lenders. A common complaint among critics of fiscal decentralization in Latin America, Africa, and Eastern Europe, for example, is that it is little more than a thinly veiled attempt to offload central government deficits onto

state and local governments by increasing subnational expenditure responsibilities without a corresponding increase in revenues. Such critiques are not limited to poor countries—similar complaints have been made about “new federalism” initiatives in the U.S. federal system from Nixon to Clinton, and about recent changes in the Canadian intergovernmental fiscal system.

III. The Conventional Wisdom: Globalization and Decentralization

Demands for Autonomy: Ethnicity and Income Distribution Thus far we have presented distinct arguments about the demand for and supply of fiscal decentralization. The underlying heterogeneity of preferences over redistribution and collective goods might drive the demand for decentralization, but ultimately the supply might be affected by the structure of political institutions. The new literature on economic integration and the vertical distribution of governmental authority builds on demand-driven arguments about the heterogeneity of preferences over government policy. Alesina and Wacziarg (1998) and Alesina and Spolaore (1997) examine a basic tradeoff between the benefits of large jurisdictions and the costs of heterogeneity in large populations. The benefits of size derive from the availability of more efficient forms of taxation, common defense, free trade within the country, economies of scale, and the decreasing per capita cost of non-rival public goods. Large size has a political price, however—the difficulty of satisfying a more diverse population (See also Seabright 1997). Bolton and Roland (1997) emphasize a related trade-off. In their model, the benefits of coordination and economies of scale are traded off against the

centralized governments and enhances demands for government accountability and responsiveness, which can presumably be achieved more easily at the local level.^3

Demands from Investors Decentralization might not only be preferred by voters in the global economy, but by international investors as well. The “market preserving federalism” literature argues that under the right conditions, fiscal decentralization forces governments to compete more fiercely for mobile capital, which creates incentives for politicians to provide good investment environments, keep taxes (and rents) low, and ultimately preserve markets (Weingast 1995). In the same vein, McGillivray and Jensen (2000) argue that political and fiscal decentralization allows countries to make more credible commitments to foreign investors. Moreover, fiscal decentralization found the favor of the World Bank and IMF in the late 1980s and early 1990s, creating an additional external demand for decentralization in some developing countries. If these arguments are correct, and central governments are interested in pleasing investors and multilateral lending agencies, they may face incentives to devolve fiscal authority to subnational governments. Such an argument is intimately related to discussions of globalization and the “race to the bottom.” Globalization is said to increase pressure on central governments to make themselves attractive to creditors and investors, which might induce tax competition and incentives to balance budgets. In a sense, by entering a world of integrated markets and the free flow of capital and finished goods across borders, central

(^3) Though long accepted in the traditional fiscal federalism literature, this latter assumption has recently been challenged by several authors. See, e.g. Bardhan and Mookherjie (1999) and Rodden and Rose-Ackerman (1997).

governments are entering a world to which subnational governments are already accustomed. Thus one might hypothesize that trade integration leads to downward pressure on central government spending without significantly affecting subnational governments. Or returning to an argument made above, in the interest of political expedience, central governments may attempt to deal with these new fiscal pressures by “offloading” responsibilities to subnational governments. Either of these possibilities would lead to a positive relationship between openness and fiscal decentralization.

IV. Globalization and Fiscal Centralization

These arguments in favor of a globalization-decentralization nexus are impressive in numerous respects – the logic underpinning them is straightforward, they have been propounded by influential political economists, and they accord with the stylized fact of increasing decentralization in recent decades. We have no quarrel with some of them. Indeed, economic integration seems to increase the credibility of secession threats in countries with concentrated minority groups (e.g. Russia) or high levels of income inequality between regions (e.g. Italy). When there is sufficient will to hold the country together, it may well be possible to forestall secession by instituting a decentralization program that allows regions to pursue distinctive economic and political strategies. Central governments might introduce local elections, set up regional parliaments, enhance the constitutional protections of subnational governments, or improve their representation in the central government. The central government might loosen its regulation and oversight of subnational governments, transform conditional grants into

capital income flows become more correlated across regions. This task will continue to be primarily the business of government” (p. 91). More specifically, it can only be the business of the central government, which must have wide-ranging authority over tax rates and the geographical distribution of expenditures in order for such schemes to work. Among other factors, capital market imperfections prevent regional and local governments from being able to provide such insurance themselves (von Hagen 1998). In fact, subnational spending is often pro- cyclical—severely so in many developing countries (IADB, 1997). Regional specialization is another likely consequence of economic integration, As regions become more specialized, they become increasingly vulnerable to the vagaries of global markets, and hence have fewer incentives to “go it alone” by relying on themselves to provide insurance. Voters in small, exporting jurisdictions with relatively un-diversified economies (hence, more vulnerable to asymmetric shocks) might not be enthusiastic about fiscal decentralization if it implies a smaller role for the central government. Consider the plight of newly formed “export clusters” in the Brazilian and Indian states. Or consider the U.S. states and Canadian provinces that are dependent on exports of farm products and natural resources. Alternatively, consider the plight of the new East German Länder and the poor “old” Länder like Bremen and the Saarland; in fact a majority of the German states favors a larger, rather than a smaller spending role for the central government (Rodden 1999). The same can probably be said of the Australian states, which have the authority to tap a variety of revenue sources but decline to do so. We believe these examples may be the rule rather than the exception.

A large current literature attempts to trace out with empirical evidence the extent of temporary risk-sharing insurance and more permanent inter-regional fiscal redistribution within countries in response to asymmetric shocks. The motivation for these studies has been to criticize or defend the need for a risk-sharing scheme in the context of the European Monetary Union. While early studies, like Sachs and Sala-I- Martin (1991), may have overestimated the insurance effect in the United States (see the critique of von Hagen 1992), several more recent studies have found evidence of significant inter-regional insurance and redistribution in response to asymmetric shocks in the United States, Canada, France, Germany, and the UK.^4 The logic of fiscal centralization for the purpose of inter-regional risk sharing holds in countries where regional business cycles are not highly correlated. Thus this argument is most plausible in large, diverse countries. Even in smaller countries, however, if globalization increases aggregate risk, voters may demand increased provision of stabilization by the central government. Trade integration reduces the attractiveness and usefulness of monetary policy as a stabilization tool, making fiscal policy more important. The traditional fiscal federalism literature argues that fiscal stabilization can only be successful if firmly under the control of the central government. Except perhaps for very rare cases like the U.S. states and Canadian provinces (even these are debatable), fiscal stabilization is not likely to be successful at lower levels of government. If anything, fiscal decentralization might undermine the center’s ability to provide fiscal stabilization.

(^4) For literature reviews, see von Hagen (1998), Kletzer and von Hagen (2000), and Obstfeld and Peri (1998).

The Demands of Minority Groups Turning the logic of Alesina and Spolaore on its head, regional heterogeneity of preferences might actually create increased spending pressure on the central government in the context of globalization. To the extent that some large, diverse countries like Canada, India, Russia, and Indonesia are able to stay together in spite of demands for secession, globalization might only increase the costs of staying together. Secession threats from a region with distinct preferences may not be credible in an autarchic world, but such threats become much more credible in a world of free trade. Consider the importance of potential trading partners in bolstering the credibility of exit threats made by Estonia, Quebec, the Slovak Republic, or oil-rich Russian republics, or the importance of the European Union to Scottish and Basque independence movements. These newly credible exit threats might be a useful bargaining chip in negotiations over the distribution of central government spending. To the extent that there are benefits to the rest of the country from keeping breakaway regions in the union, the rest of the country may be willing to send disproportionately large transfers to such regions to buy their cooperation (Fearon and Van Houten, 1998). Knowing this, of course, such regions face incentives to amplify their threats. This is a familiar story in post-Soviet Russia (Treisman 1999). Even if subnational governments end up gaining autonomy and spending more, this effect may be overwhelmed by the larger spending role of the central government. If the central government wishes to use public spending to “buy” the loyalty of voters in would-be breakaway regions, it will try to spend the money directly rather than through general-purpose transfers to regional governments. Alternatively, the central government may decide to beef up its spending on the military

and internal security forces in order to quell the threat of regional violence. Either of these possibilities might lead to fiscal centralization. The point of these conjectures is that even if one accepts the Alesina-Spolaore logic about the effects of globalization on the likely breakup of nations, it may well be inappropriate to argue that fiscal decentralization within an existing country is a halfway house to secession. The opposite may be true – in order to forestall secession, the national government may have to centralize fiscal policy so as to deliver benefits (in the form of guaranteed fiscal redistribution) to would-be secessionist localities.^5

Battles Between Rich and Poor Regions

Relatively wealthy and poor regions are likely to have different preferences over the level of fiscal decentralization. Following Persson and Tabellini (1996a), we have argued that to the extent that globalization increases regional risk, wealthy and poor regions alike might be able to benefit from maintaining their membership in a larger risk- sharing pool. Furthermore, we have argued that wealthy regions may prefer national- level stabilization, and in particular may find it beneficial to compensate those who lose from freer trade. Nevertheless, the median voter in a relatively poor region is likely to prefer a more centralized, redistributive fiscal system than the median voter in a relatively

(^5) Our argument about fiscal centralization and globalization should be distinguished from a suggestion made by Diaz-Cayeros (2000), building from Dahl and Tufte (1973) about trade and decentralization.Diaz-Cayeros conjectures that countries that trade more internally (and hence less with other countries as a portion of GDP) require a greater role for subnational governments. It is not clear, however, why moreactive local governments would enhance internal trade. On the contrary, strong subnational governments often distort and undermine rather than facilitate internal trade (see Rodden and Rose-Ackerman 1997).

Regional GDP data have been collected for a sample of 26 countries by Shah and Shankar (2000), who show that regional incomes are quite skewed in virtually every country regardless of levels of fiscal and political decentralization, and regional inequality is growing in most of the developing countries in the sample. The distance between wealthy and poor regions is often staggering, especially in developing countries, and the latter almost always greatly outnumber the former. In many developing countries in fact, the lion’s share of the economic activity is concentrated giants” (Ades and Glaeser, 1995), and this urban concentration has not been reversed by increasing economic integration (Henderson 2000). Add to this the fact that the poor, rural regions are almost always over-represented in the legislature (Samuels and Snyder, 1999), and one has strong reasons to suspect that poor regions can, under a variety of plausible political conditions, expropriate the rich.^7 But even if wealthy regions win the political battle with poor regions and implement a more decentralized fiscal structure, it is not clear that this would result in higher subnational expenditures as a percent of the total. The central government’s spending would likely go down with the reduction in transfers, but under capital mobility, all local governments might be forced to lower their expenditures as well, thus lowering the value of the numerator and the denominator simultaneously.

Rethinking the Race to the Bottom

(^7) If the “urban giant” towers over the rest of the country in population as well as GDP, this relatively wealthy jurisdiction might expropriate the hinterlands through the political process, as expected by Adesand Glaeser (1995), but if the key capital or port cities are not dominant in population or they are underrepresented (e.g. Sao Paulo in Brazil), they may be exploited by the hinterlands.

In addition to arguments about demands for decentralization related to ethnic and income heterogeneity, the previous section also pointed out a potential link between globalization and increasing fiscal pressure on the central government. We wish to call this hypothesis into question as well. Empirical studies have not shown unambiguously that increasing financial openness and trade have created substantial downward pressure on taxation. In fact, it is entirely plausible that even if fiscal competition forces governments to lower tax rates, increases in trade lead to higher private income, and thus unaltered or even faster growth in certain kinds of government revenue. It seems particularly plausible that revenue from income taxes might grow. With only a few exceptions (e.g. the United States, Switzerland, and Canada), income taxation is the domain of the central government. On the whole, subnational taxation is more often limited to property taxes and user fees, which would not likely be affected one way or the other by increasing trade. Though certainly not consistent with the prevailing wisdom, it is plausible that increased trade actually strengthens the fiscal hand of the center in this way.

Summary This section has made a very simple argument: on balance, globalization should lead to increased pressure for fiscal centralization. Economic integration may lower some of the costs of “going it alone” and hence improve the bargaining position of would-be secessionists. But in the vast majority of cases in which secession does not take place, this need not translate into fiscal decentralization. On the contrary, central governments may have to pay more to hold the union together. More generally,