DECENTRALIZATION

AND LOCAL

GOVERNANCE

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Its about the decentralization and local governance in the philippines

Typology: Slides

1 / 20

This page cannot be seen from the preview

Don't miss anything!

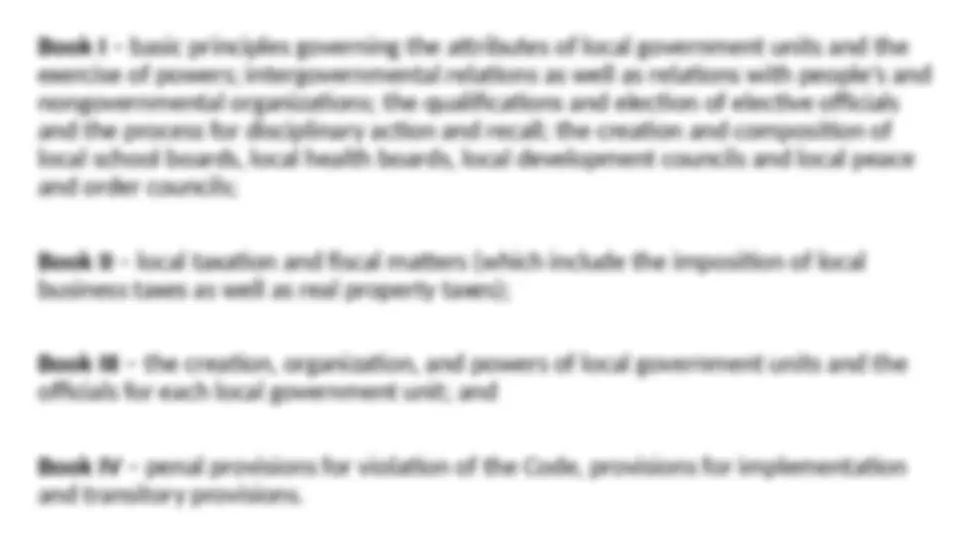

1991 Local Government Code of the Philippines: An Overview

Decentralization Decentralization refers to the transfer of powers from central government to local levels in a political-administrative and territorial hierarchy. This process allows the participation of the people and the local government. Decentralization hands over political, financial and administrative authority from central to local governments, so that the government can facilitate and guarantee better public services for the people. Decentralization strengthens the principle of transparency and accountability. The principle of accountability works best at local level, devolution of power makes government more accountable for the implementation of its tasks. (^) Decentralization also increases the level of citizen participation in making major decisions and directly affecting the community.

Indicators of Fiscal Decentralization: A. The dependency of the cooperating LGUs on national funds is reduced by generating additional Funds. B. Improved fiscal systems, especially just taxation for a measurable and transparent improvement of tax revenues; and C. The participating institutions (LGUs, selected government departments) on national, regional and municipal level present coordinated, harmonized and gender-sensitive development plans and budgets are properly implemented. Impact of Fiscal Decentralization: Fiscal Decentralization improved financial management including qualification of participants in areas of financial management, strengthening cooperation on different levels, promoting exchange of experiences, formulating strategies for an improved integration of the business sector and civil society in social and economic programs. A large part of the operations of the fiscal decentralization focused on the optimization of administrative processes and the standardization of the application of the law for local taxes with the help of information technology. Also known as the DE bureaucratization - Involves the harnessing of the private sector and non-governmental organizations in the delivery of services through various modalities including contracting out, private-public partnership and joint ventures. Focus: Training staff members of partner organizations - promoting collaboration among the participating Institutions- monitoring the development of the programs and projects being implemented - clarify roles and responsibilities of government institutions - national and local - enable efficient and effective interaction among government, private sector and civil society

3. Institutional Decentralization

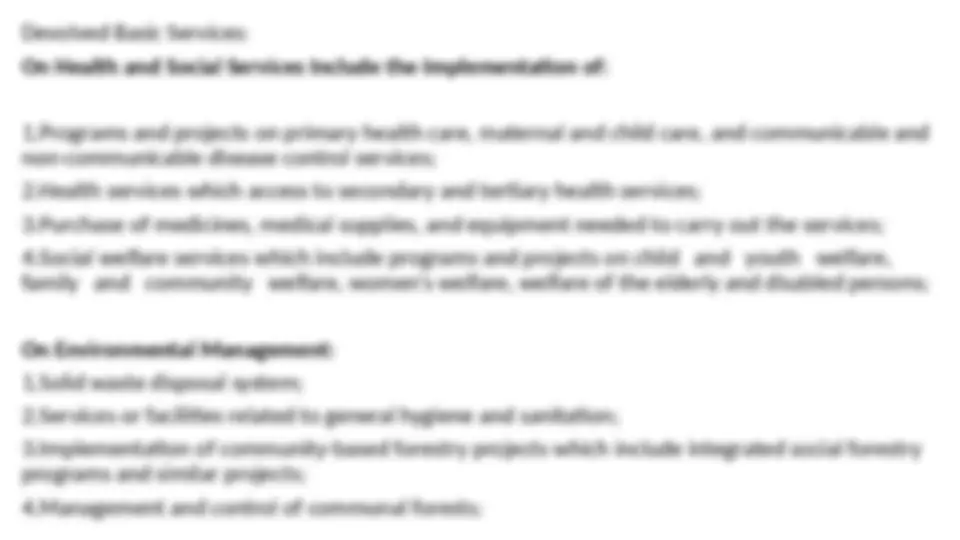

On Agriculture: 1.Inter -Barangay irrigation system; 2.Water and soil resource utilization and conservation projects; 3.Enforcement of fishery laws in municipal waters including the conservation of mangroves; On Infrastructure: 1.Maintenance and Rehabilitation of the following: A. roads and bridges B. school buildings and other facilities for public elementary and secondary schools C. clinics, health centers and other health facility D. small water impounding projects E. fish ports; artesian wells, spring development, rainwater collectors and water supply systems F. seawalls, dikes, drainage and sewerage, and flood control G. traffic signals and road signs and similar facilities.

Powers, Duties, Functions and Compensation (Sec. 447. of LGC of 1991) Organizational Structure and Staffing Pattern Every local government unit shall design and implement its own organizational structure and staffing pattern taking into consideration its service requirements and financial capability, subject to the minimum standards and guidelines prescribed by the Civil Service Commission.

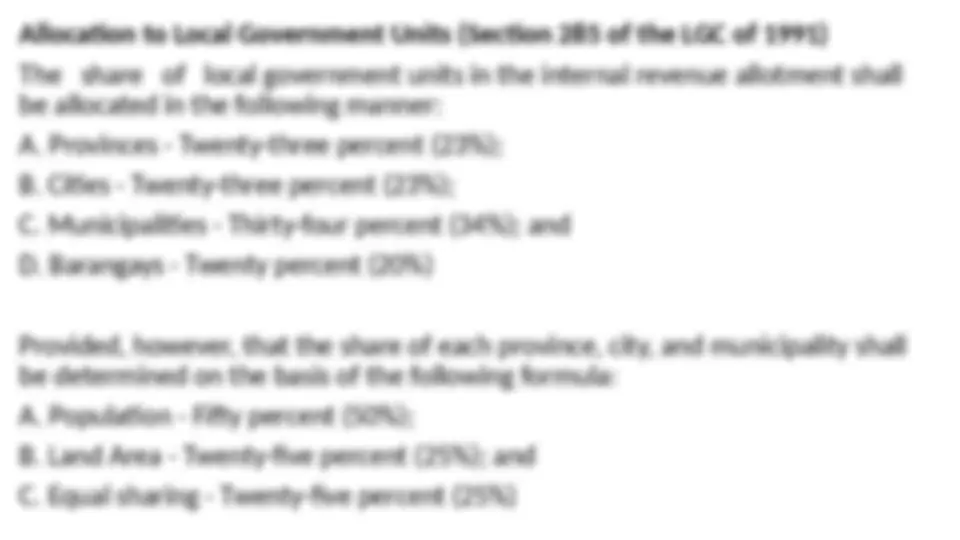

Provided, further, that the share of each Barangay with a population of not less than one hundred (100) inhabitants shall not be less than Eighty thousand pesos (P=80,000.00) per annum chargeable against the twenty percent (20%) share of the Barangay from the internal revenue allotment, and the balance to be allocated on the basis of the following formula: A. On the first year of the effectivity of this Code: 1. Population - Forty percent (40%); and 2. Equal Sharing - Sixty percent (60%); B. On the second year: 1. Population - Fifty percent (50%); and 2. Equal Sharing - Fifty percent (50%); C. On the third year and thereafter: 1. Population - Sixty percent (60%); and 2. Equal Sharing - Forty percent (40%) Provided, finally, that the fiscal requirements of barangays created by local government units after the effectivity of this Code shall be the responsibility of the local government unit concerned.

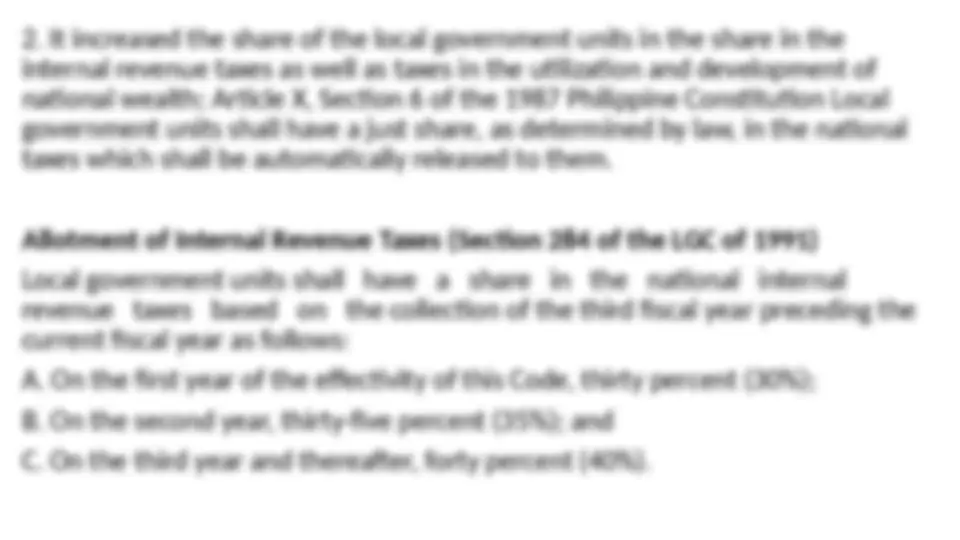

Amount of Share of Local Government Units (Section 290 of the LGC of 1991) Local government units shall, in addition to the internal revenue allotment, have a share of forty percent (40%) of the gross collection derived by the national government from the preceding fiscal year from mining taxes, royalties, forestry and fishery charges, and such other taxes, fees, or charges, including related surcharges, interests, or fines, and from its share in any co-production, joint venture or production sharing agreement in the utilization and development of the national wealth within their territorial jurisdiction. Sources of Revenue 1.National Government 2.Internal Revenue Allotment 3.Share from taxes, fees and charges collected from the development and utilization of national wealth 4.Other grants and Subsidies 5.Debt Relief Program Locally Generated 6.Real Property Taxes 7.Business Taxes 8.Other Local Taxes 9.Regulatory Fees 10.Operation of Local Economic Enterprises 11.Tolls and Users Charges.

Linkages with People's and Non-Governmental Organizations (Section 35 of the LGC of 1991) Local government units may enter into joint ventures and such other cooperative arrangements with people's and nongovernmental organizations to engage in the delivery of certain basic services, capability-building and livelihood projects, and to develop local enterprises designed to improve productivity and income, diversify agriculture, spur rural industrialization, promote ecological balance, and enhance the economic and social well-being of the people. Credit Financing: The Issues/ Concerns

References: https://www.sciencedirect.com/science/article/pii/S https://www.peoplehum.com/glossary/decentralisation