1-1

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

You will be introduce why we have to learn about accounting

Typology: Lecture notes

1 / 38

This page cannot be seen from the preview

Don't miss anything!

The hospitality industry’s heterogeneity becomes apparent when we recognise that its diversity encompasses the following: ● Hotels ● Motels ● Restaurants ● Fast food outlets ● Pubs and bars ● Country and sport clubs ● Cruise liners.. Accounting in hospitality industry

▪ Sales volatility ▪ High product perishability ▪ High fixed component in cost structure ▪ Labour intensive activities Hospitality industry characteristics

Three Activities Illustration 1- The activities of the accounting process The accounting process includes the bookkeeping function. What is Accounting?

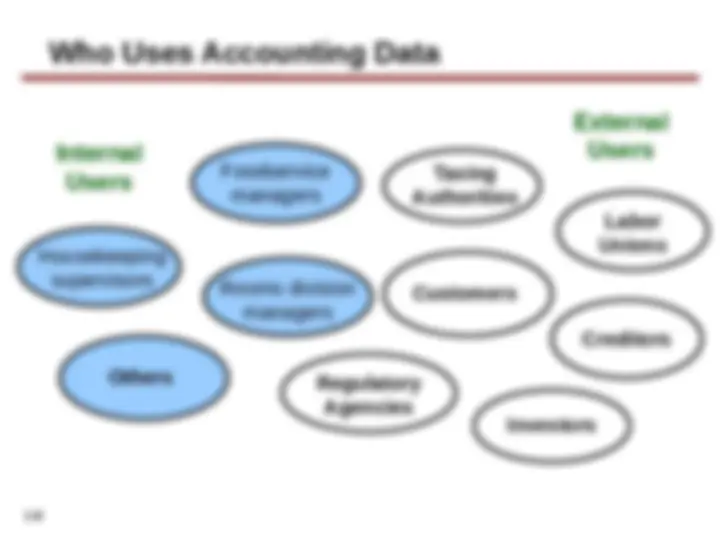

Rooms division managers Foodservice managers Taxing Authorities Labor Unions Regulatory Agencies Others Housekeeping supervisors Investors Creditors Customers Internal Users External Users Who Uses Accounting Data

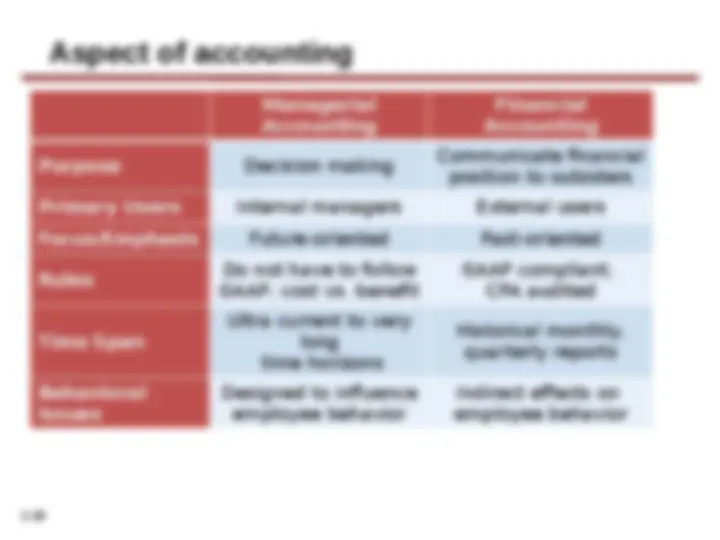

Aspect of accounting Managerial Accounting Financial Accounting Purpose Decision making Communicate financial position to outsiders Primary Users Internal managers External users Focus/Emphasis Future-oriented Past-oriented Rules Do not have to follow GAAP; cost vs. benefit GAAP compliant; CPA audited Time Span Ultra current to very long time horizons Historical monthly, quarterly reports Behavioral Issues Designed to influence employee behavior Indirect effects on employee behavior

companies record assets at their cost.

should be reported at fair value (the price received to sell an asset or settle a liability). Measurement Principles The building blocks of accounting

Proprietorship Partnership (^) Corporation ◆ Owned by two or more persons ◆ Often retail and service-type businesses ◆ Generally unlimited personal liability ◆ Partnership agreement ◆ Ownership divided into shares ◆ Separate legal entity organized under corporation law ◆ Limited liability ◆ Generally owned by one person ◆ Often small service-type businesses ◆ Owner receives any profits, suffers any losses, and is personally liable for all debts Forms of Business Ownership

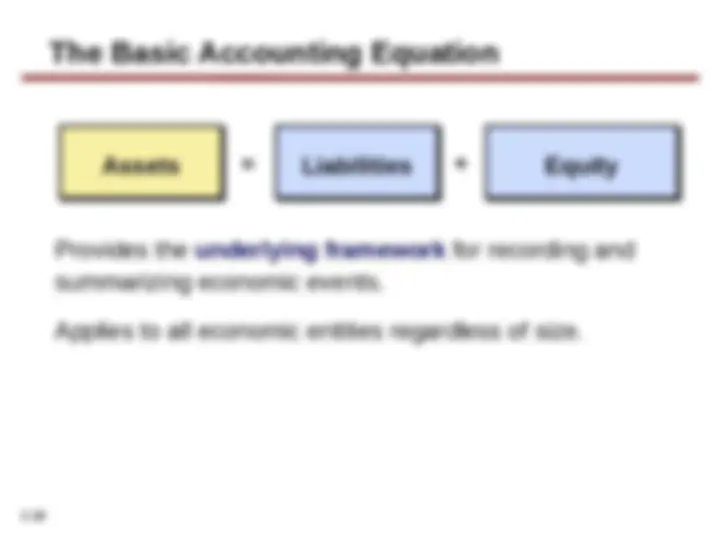

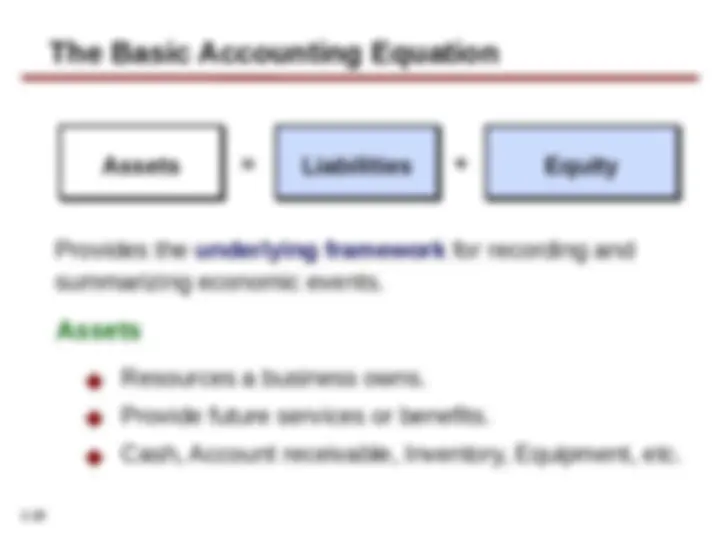

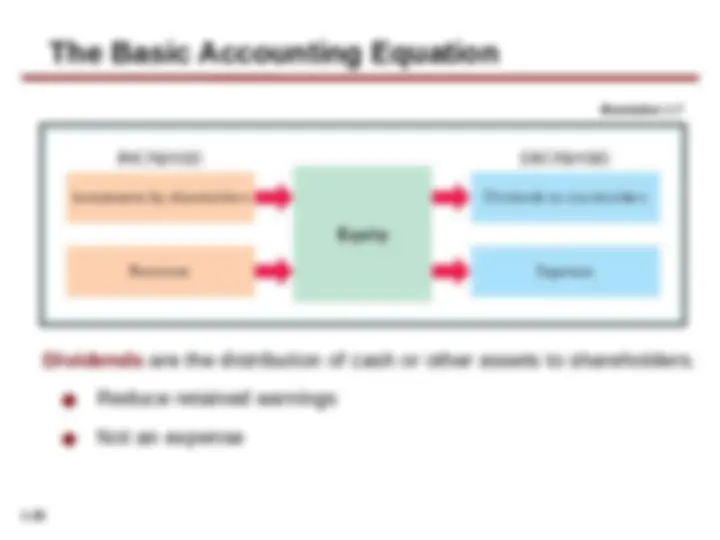

Assets Assets =^ LiabilitiesLiabilities + EquityEquity Provides the underlying framework for recording and summarizing economic events. Applies to all economic entities regardless of size. The Basic Accounting Equation

Provides the underlying framework for recording and summarizing economic events.

Assets Assets =^ LiabilitiesLiabilities +^ EquityEquity The Basic Accounting Equation ◆ Claims against assets (debts and obligations). ◆ Creditors - party to whom money is owed. ◆ Accounts payable, Notes payable, etc.

Provides the underlying framework for recording and summarizing economic events. ◆ Ownership claim on total assets. ◆ Referred to as residual equity. ◆ Share capital-ordinary and retained earnings.

Assets Assets =^ LiabilitiesLiabilities + EquityEquity The Basic Accounting Equation

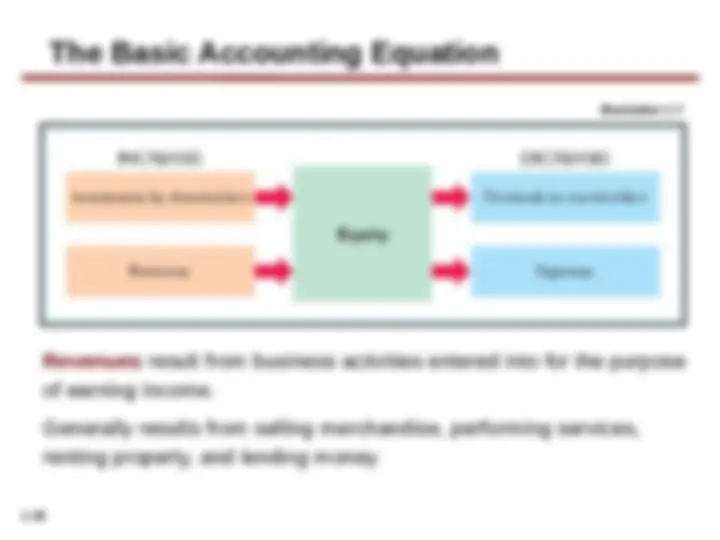

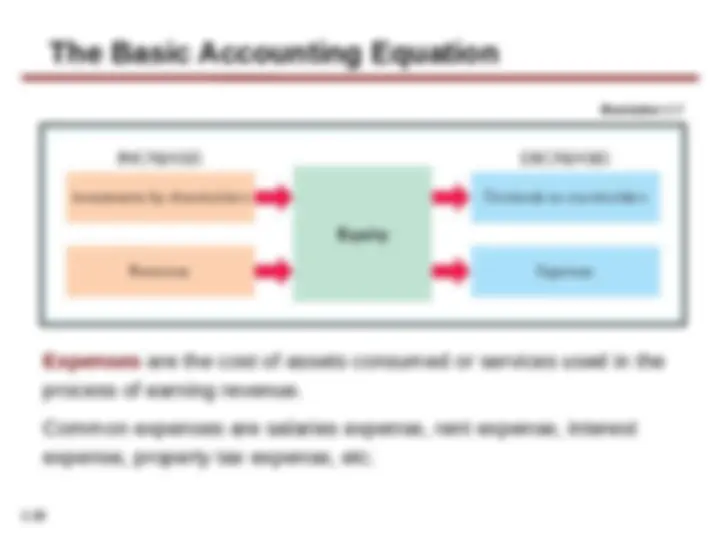

Expenses are the cost of assets consumed or services used in the process of earning revenue. Common expenses are salaries expense, rent expense, interest expense, property tax expense, etc. Illustration 1- The Basic Accounting Equation

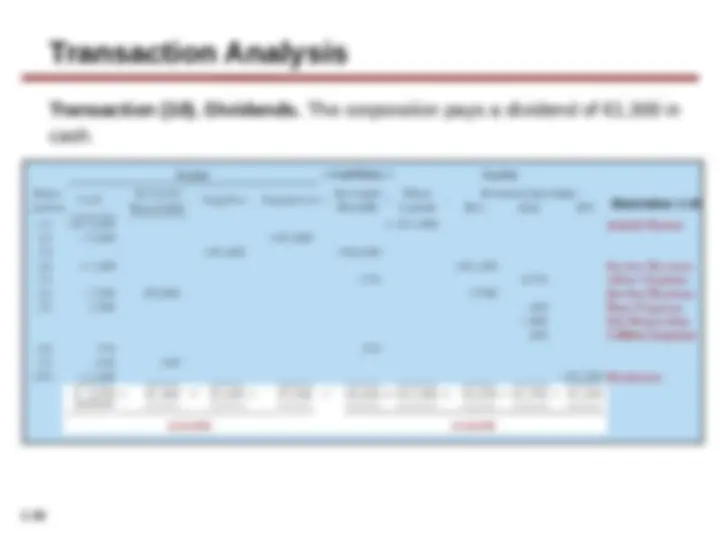

Dividends are the distribution of cash or other assets to shareholders. ◆ Reduce retained earnings ◆ Not an expense Illustration 1- The Basic Accounting Equation