Guide to taxation of Married

Couples and Civil Partners

IT 2

RPC004657_EN_WB_L_1

ver 14.06

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

An overview of the tax treatment of married persons or civil partners in Ireland, explaining the concepts of Joint Assessment and Separate Assessment, and outlining the process for allocating tax credits and standard rate bands between spouses or civil partners. It also includes examples to illustrate the differences in tax liability under each assessment method.

Typology: Slides

1 / 10

This page cannot be seen from the preview

Don't miss anything!

RPC004657_EN_WB_L_

ver 14.

This leaflet explains the tax treatment of married persons or civil partners in the year of marriage or in the year of registration of a civil partnership and in subsequent years.

Once married or registered in a civil partnership, you should advise your Revenue office of the date of your marriage or civil partnership registration and quote your own and your spouse’s or civil partner’s Personal Public Service (PPS) numbers.

For tax purposes, both parties continue to be treated as two single persons in the year of the marriage or the year the civil partnership was registered. However, if the tax you pay as two single persons in that year is greater than the tax which would be payable if you had been taxed as a couple in a marriage or civil partnership, a refund of the difference can be claimed. Any refund due is only from the date of marriage or registration of civil partnership and will be calculated at the end of that tax year.

A refund of tax for the year of marriage or registration of civil partnership would normally only arise where a couple are taxed at different tax rates and one spouse or civil partner could benefit from the unused standard rate band or from some of the unused tax credits of the other spouse or civil partner. See example on page 7.

The following options are available:

You may choose the method of taxation which is best suited to your circumstances. To help you decide, each method is described in detail in the following paragraphs.

Joint Assessment is usually the most favourable basis of assessment for couples in a marriage or civil partnership. It is automatically given by your Revenue office once you have advised them of your marriage or civil partnership registration, but this doesn’t prevent you from electing for either of the other options.

Under Joint Assessment, the tax credits and standard rate band can be allocated between spouses or civil partners to suit their circumstances. For example:

Where the Revenue office does not receive a request for the allocation of tax credits and reliefs in a particular way, it will normally give all the tax credits (other than the other spouse’s or civil partner’s PAYE and expense tax credits) to the assessable spouse or nominated civil partner. See paragraph on standard rate band on page 5 for information.

Yes. If both spouses or civil partners are in employment, a tax credit certificate is issued to each spouse or each civil partner. All of the tax credits and reliefs due to a couple in a marriage or civil partnership, where Joint Assessment applies, are shown on both spouses’ or civil partners’ certificates. Both certificates state the amount of tax credits and standard rate band allocated to each spouse or civil partner. Where either spouse or civil partner has multiple sources of PAYE income, the amount of tax credits and standard rate band allocated to each employment or pension is also shown on the certificate.

Under Separate Assessment your tax affairs are independent of those of your spouse or civil partner. The following tax credits are divided equally between you:

The balance of the tax credits are given to each of you in proportion to the cost borne by you. The PAYE tax credit and employment expenses, if any, are allocated to the appropriate spouse or civil partner. Any tax credits, etc. other than the PAYE tax credit and employment expenses, which are unused by one spouse or civil partner may be claimed by the other spouse or civil partner. The tax credits may not generally be adjusted until after the end of the tax year.

Any unused tax credits (other than the PAYE tax credit and employment expenses) and standard rate band up to €41,800 can be transferred to the other spouse or civil partner, but only at the end of the tax year. The increase in the standard rate band of up to €23,800 is not transferable between spouses or civil partners. If you think you have unused tax credits or standard rate band, you should contact your Revenue office for a review after the end of the tax year. It is important to note that, overall, the amount of the tax payable under Separate Assessment is the same as that payable under Joint Assessment. See example on page 8.

Separate Assessment can be claimed either verbally or in writing. The claim can be made by either spouse or civil partner, and must be made in the six months between the 1 October of the preceding year and the 31 March in the year of the claim. It cannot be backdated to a previous year and it lasts until withdrawn. Whichever spouse or civil partner initially makes the claim must also be the one to withdraw it.

Each spouse or civil partner may complete a separate return of their own income. However, their Revenue office will accept one joint return (which can be made by either spouse or civil partner) if it includes the income of both spouses or civil partners.

Under Separate Treatment each spouse or civil partner is treated as a single person for tax purposes. Separate Treatment should not be confused with Separate Assessment.

Both spouses or civil partners:

One spouse or civil partner cannot claim relief for payments made by the other and there is no right to transfer tax credits or standard rate band to each other.

Separate Treatment can be claimed either verbally or in writing. Either spouse or civil partner can make the claim and the election lasts until withdrawn by the spouse or civil partner who claimed it. A claim for Separate Treatment, if required, must be made within the tax year (preferably at the beginning).

This basis of assessment can be unfavourable in some circumstances because any unused tax credits or standard rate band cannot be transferred. Home Carer Tax Credit cannot be claimed in respect of a spouse or civil partner who cares for a dependent person and who may otherwise qualify for the relief. See example of Separate Treatment on page 9.

The standard rate band for couples in a marriage or civil partnership for 2013 is €41,800 subject to an increase of up to €23,800 where both spouses or civil partners are working. The increase is limited to the lower of €23,800 or the amount of the income of the spouse or civil partner with the smaller income. This increase is not transferable between spouses or civil partners. The increase in the standard rate band is not allowable where a couple are claiming the Home Carer Tax Credit. However, if the increased standard rate band is more beneficial, you can claim the increased standard rate band instead of the Home Carer Tax Credit. In practice your Revenue office will grant you whichever is the more beneficial. Leaflet IT 66 ‘Home Carer Tax Credit’ gives further information and examples to help you calculate which is the most beneficial.

It is very important that you have the correct tax credits and standard rate band as otherwise you will not pay the correct amount of tax.

You are the assessable spouse or nominated civil partner and you earn €46,000 in 2013. Your spouse or civil partner has a Social Welfare pension of €8,500. The income is taxable as follows:

Self €41,800 @ 20% €4,200 @ 41% Spouse or Civil Partner €8,500 @ 20%

You and your spouse or civil partner entered a marriage or civil partnership on 10/7/2013. You earned €48,000 in 2013 and your spouse or civil partner earned €24,000.

Tax payable by you and your spouse or civil partner as Single People: Self Spouse or Civil Partner € € Income 48,000 24, Standard Rate Band 32,800 x 20% = 6,560 24,000 x 20% = 4, 15,200 x 41% = 6, 12, Tax Credits Personal Tax Credit 1,650 1, PAYE Tax Credit 1,650 1, 3,300 3,300 3,300 3,

Tax Payable 9,492 1,

Combined Tax Payable Self 9, Spouse or Civil Partner 1, 10,

Tax payable by you and your spouse or civil partner under Joint Assessment as a Couple in a Marriage or Civil Partnership would be: € Income Self 48, Spouse or Civil Partner 24, Total 72,

Standard Rate Band € Self 41,800 x 20% = 8, 6,200 x 41% = 2, Spouse or Civil Partner 23,800 x 20% = 4, 200 x 41% = 82 15, Tax Credits Married or Civil Partners Tax Credit 3, PAYE Tax Credit x 2 3, 6,600 6, Tax Payable 9,

The difference between the tax payable by you and your spouse or civil partner as single persons and the tax payable by you both as a couple in a marriage or civil partnership is €1,848, i.e. €10, less €9,144. This amount of €1,848 is apportioned by the number of months for which you have been married or registered in a civil partnership in the tax year, i.e. €1,848 x 6/12 = €924.

You and your spouse or civil partner can claim a refund of this €924 after the end of the tax year. The refund is apportioned between you both in proportion to the tax payable by each of you as follows:

The amount to be repaid to you is: €924 x €9,492 = €797. €10,

The amount to be repaid to your spouse or civil partner is: €924 x €1,500 = €126. €10,

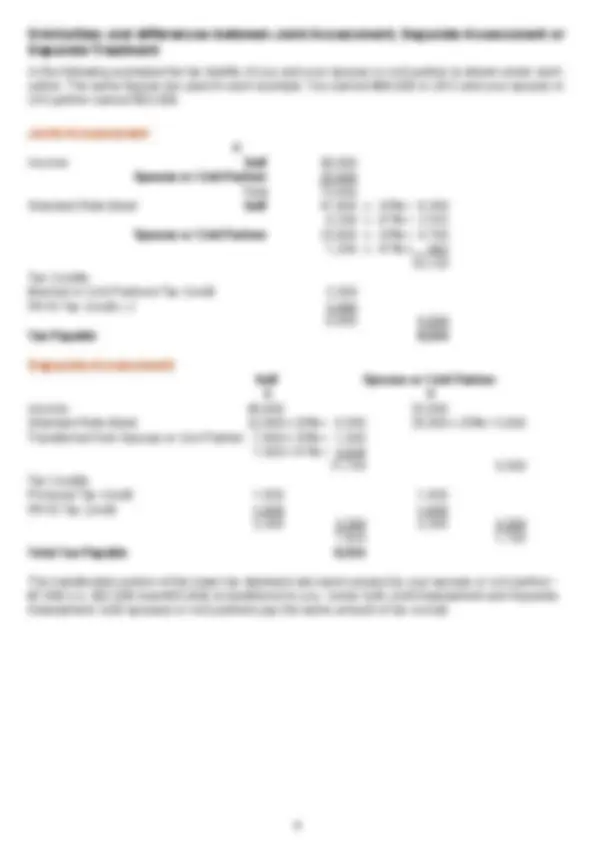

In the following examples the tax liability of you and your spouse or civil partner is shown under each option. The same figures are used in each example. You earned €48,000 in 2013 and your spouse or civil partner earned €25,000.

Income Self 48, Spouse or Civil Partner 25, Total 73, Standard Rate Band Self 41,800 x 20% = 8, 6,200 x 41% = 2, Spouse or Civil Partner 23,800 x 20% = 4, 1,200 x 41% = 492 16, Tax Credits Married or Civil Partners Tax Credit 3, PAYE Tax Credit x 2 3, 6,600 6, Tax Payable 9,

Self Spouse or Civil Partner € € Income 48,000 25, Standard Rate Band 32,800 x 20% = 6,560 25,000 x 20% = 5, Transferred from Spouse or Civil Partner 7,800 x 20% = 1, 7,400 x 41% = 3, 11,154 5, Tax Credits Personal Tax Credit 1,650 1, PAYE Tax Credit 1,650 1, 3,300 3,300 3,300 3, 7,854 1, Total Tax Payable 9,

The transferable portion of the lower tax standard rate band unused by your spouse or civil partner - €7,800 (i.e. €32,800 less €25,000) is transferred to you. Under both Joint Assessment and Separate Assessment, both spouses or civil partners pay the same amount of tax overall.

This leaflet is for general information only. For further information you can visit www.revenue.ie or contact your Regional PAYE LoCall Service whose number is listed below (within the Republic of Ireland only).

Please note that the rates charged for the use of 1890 (LoCall) numbers may vary among different service providers.

If calling from outside the Republic of Ireland, please telephone + 353 1 702 3011.

Time Limit for Repayment Claims A claim for repayment of tax must be made within four years after the end of the tax year to which the claim relates.

Accessibility If you are a person with a disability and require this leaflet in an alternative format the Revenue Access Officer can be contacted at [email protected]

This leaflet is intended to describe the subject in general terms. As such, it does not attempt to cover every issue which may arise in relation to the subject. It does not purport to be a legal interpretation of the statutory provisions and consequently, responsibility cannot be accepted for any liability incurred or loss suffered as a result of relying on any matter published herein.

Revenue Commissioners June 2014 Designed by the Revenue Printing Centre