Download Krusell-Smith Models and more Exams Law in PDF only on Docsity!

Krusell-Smith Models

Jes´us Fern´andez-Villaverde^1 April 12, 2022 (^1) University of Pennsylvania

A basic model with aggregate uncertainty, I

- We want to deal with models with aggregate uncertainty.

- Why?

- Issues of interpretation (forecasting vs. policy analysis, etc.).

- Internal vs. external propagation.

- Exogenous vs. endogenous risk.

A basic model with aggregate uncertainty, II

- Idiosyncratic labor productivity yt yt ∈ Y = {yu , ye } with yu < ye.

- yu stands for the household being unemployed and ye stands for the household being employed.

- The distribution of yt is correlated with aggregate productivity st.

- Probability of being unemployed is higher during recessions than during expansions.

- Let π be a 4 × 4 matrix with entry π(y ′, s′|y , s) > 0 that gives the conditional probability of individual productivity y ′, aggregate state s′^ tomorrow, conditional on (y , s) today.

Cross-sectional distributions

- Consistency requires that: X

y ′∈Y

π(y ′, s′|y , s) = π(s′|s) all y ∈ Y , all s, s′^ ∈ S

- Law of large numbers: idiosyncratic risk averages out, only aggregate risk determines number of agents in states y ∈ Y.

- Assume that, cross-sectionally, the fraction of the population in idiosyncratic state y = yu is only a function of the aggregate state s. Denote the cross-sectional distribution by Πs (y ).

- This assumption imposes additional restrictions on π(y ′, s′|y , s):

Πs′ (y ′) =

X

y ∈Y

π(y ′, s′|y , s) π(s′|s) Πs (y ) for all s, s′^ ∈ S

Recursive competitive equilibrium, I

A RCE is value function v : Z × S × M → R, household policy functions c, a′^ : Z × S × M → R, firm policy functions K , L : S × M → R, pricing functions r , w : S × M → R, aggregate law of motion H : S × M × S→ M s.t.

- v , a′, c are measurable wrt B(S), v satisfies the household’s Bellman equation and a′, c are the associated policy functions, given r () and w ()

- K , L satisfy, given r () and w ()

r (s, Φ) = FK (K (s, Φ), L(s, Φ)) − δ w (s, Φ) = FL(K (s, Φ), L(s, Φ))

Recursive competitive equilibrium, II

- For all Φ ∈ M and all s ∈ S

K (H(s, Φ)) =

Z

a′(a, y , s, Φ)dΦ

L(s, Φ) =

Z

ydΦ Z c(a, y , s, Φ)dΦ +

Z

a′(a, y , s, Φ)dΦ = F (K (s, Φ), L(s, Φ)) + (1 − δ)K (s, Φ)

- Aggregate law of motion H is generated by exogenous Markov chain π and policy function a′.

Lack of theoretical results

- We do not know about the existence of a recursive equilibrium in which the aggregate state only contains the current shock and the current wealth distribution (in fact, some counterexamples in Kubler and Schmedders, 2002).

- Miao (2006): existence of recursive equilibrium when we also track the cross-sectional distribution of expected payoffs.

- Similarly, we do not know about uniqueness.

- We will compute approximate equilibrium with boundedly rational agents (where approximation is not just due to numerical error).

- No sense as to whether this equilibrium is close to a true recursive equilibrium.

- Recently, idea of self-justified equilibria by Kubler and Scheidegger (2019).

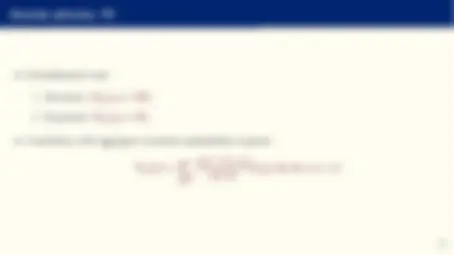

Keeping track of wealth distribution

- Key challenge: wealth distribution Φ is an infinite-dimensional object.

- Why do agents need to keep track of Φ? In order to forecast future capital stock and, with it, future prices.

- But for K ′^ need entire Φ since: K ′^ =

Z

a′(a, y , s, Φ)dΦ

- If a′^ were linear in a, with same slope for all y ∈ Y , exact aggregation obtained and average capital stock today is sufficient statistic for the average capital stock tomorrow.

- Krusell and Smith’s proposal: approximate distribution Φ with a finite set of moments.

Computation, II

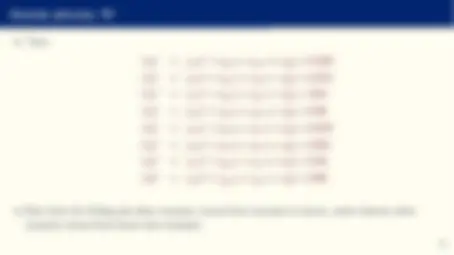

- Krusell and Smith pick n = 1 and pose log(K ′) = as + bs log(K ) for s ∈ {sb , sg }. Here (as , bs ) are parameters that need to be determined.

- Household problem v (a, y , s, K ) = max c,a′≥ 0 {U(c) + β

X

y ′∈Y

X

s′∈S

π(y ′, s′|y , s)v (a′, y ′, s′, K ′)}

s.t. c + a′^ = w (s, K )y + (1 + r (s, K ))a log(K ′) = as + bs log(K )

- Reduction of the state space to a four dimensional space (a, y , s, K ) ∈ R × Y × S × R.

Algorithm, I

- Guess (as , bs ).

- Solve households problem to obtain a′(a, y , s, K ).

- Simulate for large number of T periods, large number N of households:

- Initial conditions for economy (s 0 , K 0 ), for each household (ai 0 , y 0 i).

- Draw random sequences {st }Tt=1 and {y (^) ti }Tt=1^ ,N,i=1, use decision rule a′(a, y , s, K ), perceived law of motion for K to generate {ait }Tt=1^ ,N,i=1.

- Aggregate: Kt = N^1

X^ N i=

ait

Parallelization

- As with Aiyagari Models, there are gains to parallelization.

- Computation of value function and simulation can be parallelized.

- Update of law of motion for moments of distribution is harder to parallelize.

A quantitative example

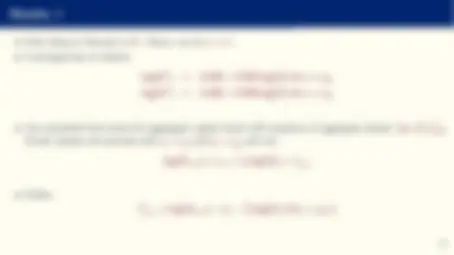

- Model period 1 quarter (business cycle model).

- CRRA utility with σ = 1 (i.e. log-utility).

- The time discount factor β = 0. 994 = 0. 96 , i.e. ρ = 4.1%.

- Capital share α = 0.36.

- Annual depreciation rate δ = (1 − 0 .025)^4 − 1 = 9.6%.

Idiosyncratic shocks

- Two state process: employment and unemployment

Y = { 0. 25 , 1 }

- Unemployed person makes 25% of the labor income of an employed person.

- Transition probabilities: π(y ′|s′, y , s) = π(y ′, s′|y , s) π(s′|s) or π(y ′, s′|y , s) = π(y ′|s′, y , s) ∗ π(s′|s)

- Specify the four 2 × 2 matrices π(y ′|s′, y , s) indicating, conditional on an aggregate transition from s to s′, what the individual’s probabilities of transition from employment to unemployment are.

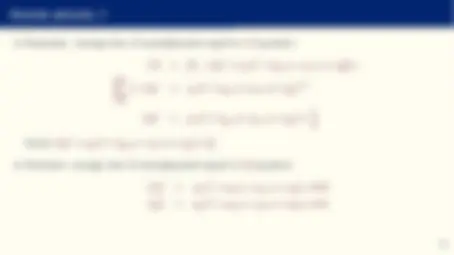

Income process, I

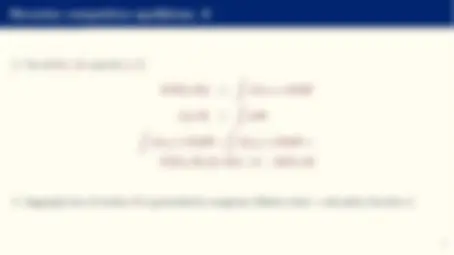

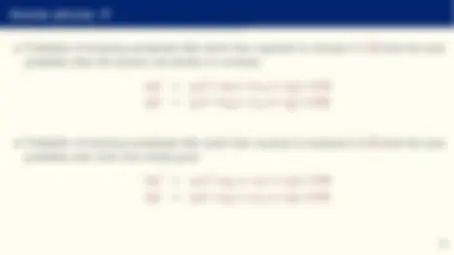

- Expansion: average time of unemployment equal to 1.5 quarters:

- 5 = [1 − π(y ′^ = yu |s′^ = sg , y = yu , s = sg )] ∗ X^ ∞ i=

i ∗ π(y ′^ = yu |s′^ = sg , y = yu , s = sg )i−^1

π(y ′^ = yu |s′^ = sg , y = yu , s = sg ) =^1 3 Hence π(y ′^ = ye |s′^ = sg , y = yu , s = sg ) = 23.

- Recession: average time of unemployment equal to 2.5 quarters:

π(y ′^ = yu |s′^ = sb , y = yu , s = sb ) = 0. 6 π(y ′^ = ye |s′^ = sb , y = yu , s = sb ) = 0. 4