Download Cost Accounting: Understanding Costs and Their Classification and more Study notes Management Accounting in PDF only on Docsity!

MANAGEMENT ACCOUNTING

Course outline. 1.0 Introduction management accounting a) Accounting branches. b) Nature of management accounting. c) Roles of a management accounting. d) Common terms used in management accounting 2.0. Understanding costs and their nature a) Definition of costs and cost elements. b) Classification of costs. c) Costs relevant for decision making. d) Behavior of costs. e) Separation of cost using the High low range method. 3.0 Resources management Materials a) Essentials of a good material control system. b) Purchasing function and procedure. c) Dangers of overstocking and under stocking. d) Management of Stock and supplies quantities. e) Valuation of materials using FIFO, LIFO, AVCO/WACO and standard price. Labour. a) Labor related records b) Labor remuneration i. -Time basis ii. -Output basis iii. -Incentive schemes (premium + group schemes) iv. -Characteristics of a good remuneration scheme c) Overtime and idle time d) Labor turnover and associated problems. 4.0 Accounting for Overheads ( 6 hours) a) Nature and need for accounting for overheads b) Allocation and apportionment of overheads at primary stage c) Secondary redistribution of overheads d) Overhead absorption or recovery rates ( over or under recovery)

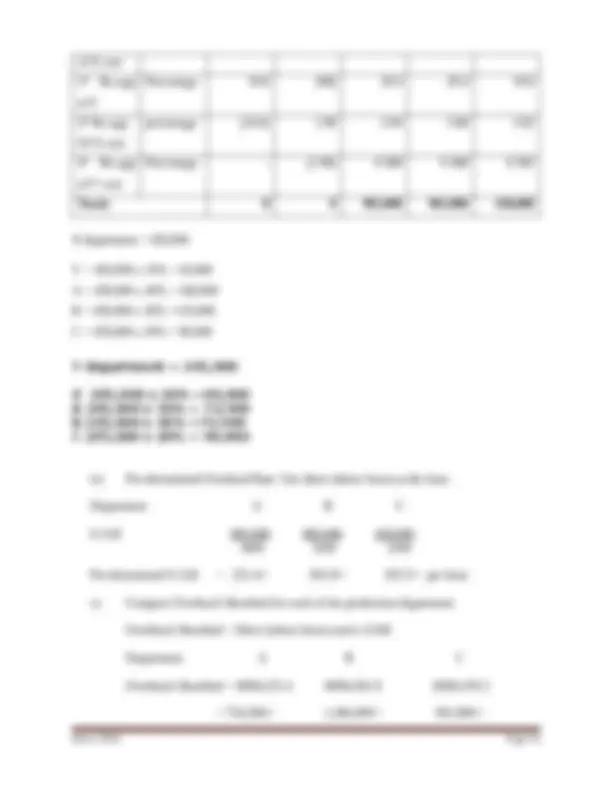

5.0 Activity Based Costing

- Reasons for the development of ABC

- Steps followed in implementing ABC

- Advantages and disadvantages of ABC

- Similarities and differences between ABC and the traditional costing system

- Determining costs and prices using ABC and the traditional costing system 6.0 Budgeting and Budgetary control techniques ( 6 hours) a) Budgeting and budgetary control b) Usefulness of budgeting and associated problems c) Budget committees and manuals d) Common terminologies in budgeting e) Stages in budgeting f) Budgets in the control process ( fixed and flexed budgets) g) Functional budgets h) Approaches to budgeting 7.0 Management accounting and Costing Methods a) Absorption costing b) Costing methods [Job Costing, Contract Costing, Process costing, Service costing] c) Marginal costing d) Standard Costing and Variance Analysis [material cost variances, labour cost variances, overheads cost variances, mix and yield variances, total cost variances; sales variances] 8.0 Decision making and planning a) Cost volume profit statements i. Assumptions ii. Accountants’ and economists views iii. Break even charts and profit volume charts iv. Algebric Method of CVP v. Planning CVP levels (margin of safety, target levels). 9.0 Relevant costs and Short run tactical decisions i) Make or Buy Decision ii) Operate or Shut down decision iii) Product Mix under Limiting Factor Decision iv) Accept or Reject Special order decision

- Any other management accounting book or reading material.

1.0 INTRODUCTION

Decision making in any business organization is primarily a function of management. In modern times, management in the atmosphere of uncertainty takes most of the business decisions. The decisions taken by management on the basis of intuition of trial and error do not give good results. Therefore, in order to make scientific decisions, management requires a lot of information. The financial statements prepared by accountants are an important treasure of facts and information but in their traditional form they are unable to convey any meaningful information. In order to be of use to the busy management, this financial information is to be re-arranged relatively. Therefore, management accounting performs this function. NATURE / CHARACTERISTICS OF MANAGEMENT ACCOUNTING.

- Management Accounting is of selective nature. It picks up only that data from balance sheet and profit and loss accounts, which is relevant and useful. In the same way, only important information is communicated to the management, which is helpful in decision- making.

- It provides data not the decisions. It can inform but cannot prescribe. It depends upon the efficiency and wisdom of management to and what extend they can make use of this information.

- Management Accounting is concerned with future. It helps planning for the future because decisions are always taken for future course of Action. All management accounting techniques are concerned with forecasting the future.

- Stress on the study of cause and effect relationship. Management accounting studies the causes of profit or loss. It analyses the effect of different variables on the projects and profitability of the business.

- Management Accounting does not show set rules and formats like Financial Accounting. The necessary accounting information is provided in the shape of various statements or reports as it suits to the management. The basic task of management accounting is to motivate management action. Therefore, the stress in management accounting is on the utility of information and not on the formats and legal presentation of the information as required in financial accounting.

- Highly sensitive to management needs; It is basically an internal information system, which helps the management in managing better. It assists management but does not replace it. 7. Management Accounting is a decision making system

1.1 FUNCTIONS OF MANAGEMENT ACCOUNTING

Management accounting functions may be said to include all activities, with collecting, processing, interpreting and presenting information to management.

- Forecasting and planning. The first and foremost function of management accounting is to make short term and long term forecasts and planning the future operations of the business. This is possible with the use of probability; trend study, correlation and regression techniques of statistics, funds flow statement, budgeting, standard costing, and marginal costing e.t.c.

- Organizing. Organizing human and non human resources of the business is second function. Management accounting helps management in performing this function by analysing the different functions and assigning specific responsibilities on different people. The organization of finance and accounting functions on the most modern lines is an important function of Management accounting.

- Coordinating. Management accounting provides the different tools of coordination e.g. budgeting, financial reporting, financial analysis and interpretation etc. it helps management in preparing budgets and setting the standard costs.

- Controlling. In carrying out the control function managers seek to ensure that the plan is being followed. This is done through feedback and performance reports.

- Directing and motivating. Overseeing day-to-day activities and keep the organization functioning smoothly, requires the ability to motivate and effectively direct people. Managers assign tasks to employees, arbitrate disputes, answer questions, solve on the spot problems, and make many small decisions that affect customers and employees.

- Decision-making. The manager of a profit making business has to decide on the manner of implementation of the objectives of the business. A non-profit making enterprise will be making decisions on resource allocation so as to be economic, efficient and effective in its use of finance. Decisions will be about resources, which may be people, products, services, long term and short-term investments.

- Financial analysis and interpretation. This is a technical job. Yet the top management on the other hand may not be well versed in accounting techniques. Management accounting performs this technical service.

- Communication. Management accounting is a medium of communication. The reporting mechanism is a typical example of communicating results to the superiors. The management accountant prepares and submits various reports for this purpose. He also communicates to, share holders.

- Other functions. Supplies useful information to different functional authorities.

MANAGEMENT AND COST ACCOUNTING COMPARED

Management accounting provides the information requirements of management thereby helping the management team to run the affairs of the business. It is primarily concerned with gathering data, analysing, processing, interpreting and communicating the resulting information for use within the organisation so that management can effectively plan, make decisions and control operations. Cost accounting deals with attaching a cost on a product or service or operation. It is primarily concerned with accumulating, summarising, and reporting cost data for the preparation of financial reports for external parties (shareholders, bankers, government agencies, creditors, consumers, financial analysts). Such information is key to decisions concerning the following: Whether a given product or service should be produced; What price should be charged for the items offered; How much should be produced to break even; What impact a change in the level of out put will have on the cost. The information generated therefrom is important for the internal management of the organisation. 2.0 COSTS AND THEIR NATURE - KEY CONCEPTS A central problem facing organisations is how to identify and evaluate the relevant costs and benefits resulting from the various available alternatives. The cost concepts and terms will be of help in demonstrating the multiple purposes of cost accounting systems. COSTING It is the ascertainment of costs. Costing includes techniques (principles and rules applied for ascertaining costs of products or serviced) and processes of ascertaining costs. This refers to the classification, recording, and appropriate allocation of expenditure in order to determine the costs of products or services. COST Accountants usually define cost as a resource sacrificed or foregone to achieve a specific objective. Other researchers (Jack Gray & Don Ricketts) define a cost as the total resources consumed to accomplish a specific objective.

COST OBJECT

To guide decisions, managers need the cost of something. This something can be referred to as the cost object which is anything for which a separate measurement of cost is desired. Examples of cost objects include: a product, service, a project, a customer, a brand category, an activity, a department, and a program. Cost objects are chosen to guide in decision making. COST UNIT It is a unit of a product or service to which costs are ascertained by means of allocation, apportionment and absorption. It is a useful measurement of costs for comparative purposes. COST DRIVER This is any factor that affects costs. That is a change in the cost driver will cause a change in the total cost of a related cost object. Business function Examples of cost drivers Research and Development - No. of projects

- Personnel hours on a project

- Technical complexity of a project Design of products, services and processes - No. of products

- No. of parts per product

- No. of engineering hours Production - No. of units produced

- No. of set-ups [process]

- No. of engineering change orders

- Direct manufacturing labour cost Marketing - No. of advertisements run

- No. of sales personnel. Distribution - No. of items distributed

- No. of customers

- Weight of items RELEVANT RANGE This is the range of the cost driver in which a specific relationship between cost and the driver is valid.

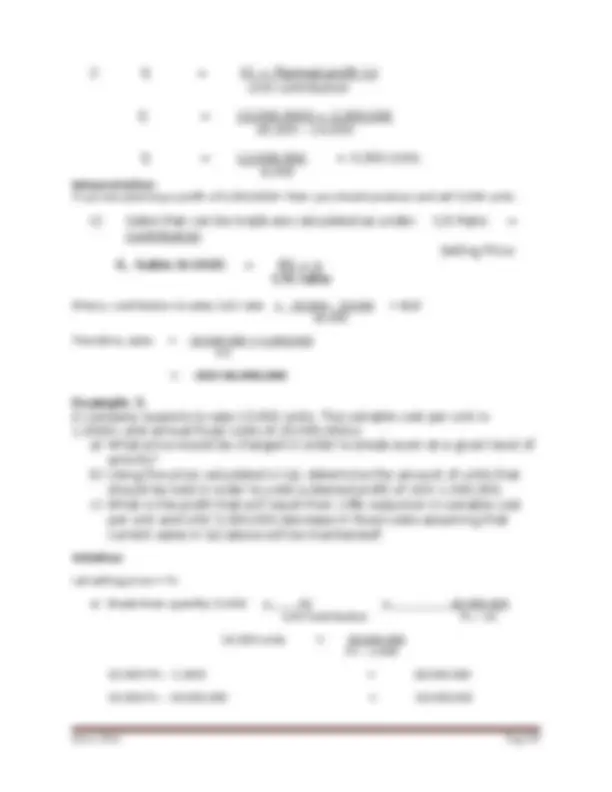

Example; A manufacturing company produces a single product, the widget. It has established that its costs are as follows. Direct materials $4 per unit Direct labour, 20 minutes per unit. Direct labour is paid at $6 per hour Production overheads consist of fixed costs of $60,000 each month and variable costs of $0.90 per direct labour hour. Administration overheads are fixed, $20000 per month Sales and distribution overheads are fixed costs of $30000 per month plus variable selling costs of $2 per unit sold During a given month, 10,000 widgets were produced and sold. What should be the total costs in the month? Solution $ $ Direct materials (10000 x $4) 40, Direct labour (10000 x $6 x 20/60) 20, Production Overhead Variable (10000 x $0.90 x 20/60) 3, 63, Fixed 60, Administration overhead 20, Sales and distribution overhead Variable (10000 x $2) 20, Fixed 30, 50, Total costs 193, 1.1.1.2 The need to know about cost behaviour Understanding cost behaviour is essential for forecasting or budgeting, and for controlling costs and monitoring performance. Budgeting Once a decision has been taken about how much to produce and sell during the budget period, all costs (and revenues) have to be budgeted for that activity level. These budgeted cost figures are obtained by adding the total of all expected variable costs and fixed costs, so that the cost budget is built up from its component elements.

Control of costs A common method for controlling costs and monitoring performance is to compare budgeted figures with actual and seek explanations for differences. Clearly, if any differences are to be meaningful, the figures used as ‘yardsticks’ must take account of actual activity level (not that originally budgeted for). Such adjustments to the original budget for changes in the activity level can only be done if managers understand what happens to costs as the activity level changes. 1.1.1.3 Factors affecting cost behaviour There are several major factors which affect cost behaviour either singly or in combination. Some of these are discussed below. Volume or activity level Many costs are affected by the level of activity. But there is more than one volume measure that affects costs and it is vital that the correct activity is identified as the basis of variability of costs. For example, selling costs may vary with either the volume or value of sales, distribution costs may vary with volume, size, weight or value of sale, whilst production costs may vary with the number of units produced, or the number of hours worked. Nature of the cost The nature of a cost will often aid in predicting its likely amount. For example, if the maintenance of machines is a single overhaul each year, then maintenance is a fixed cost. If the maintenance is needed once every so many units of output, it is a variable cost. Similarly, by their nature, electricity and telephone costs are mixed costs, having a fixed element (or standing charge) and a variable element that changes with the amount of use. Nature of the production process As production processes become more automated and less labour intensive so a higher proportion of costs can be expected to be fixed rather than variable, because depreciation (which is a fixed cost) replaces the variable cost of direct wages. Production methods may change as output level increases and cost behaviour will also reflect such changes. The existence of spare capacity If an organisation is working at less than full capacity, an increase in output may result in little change in costs. But where the increase in output necessitates a change in capacity, all costs will alter. Other factors

The main objective of this classification is to determine the cost of each function and to foster cost control. In addition, it may serve as a way of justifying the existence of a certain function visa-a-vis the benefits derived from them. Natural Classification This grouping is done according to what the costs are: the nature of the costs. Costs can be categorised naturally into 3 groups. (a) Materials (b) Labour (c) Expenses Materials - inputs to be worked on directly or indirectly in the process of producing output. Labour - human effort to product. Expenses - costs that cannot fall under materials or labour. The natural classification is further subdivided into two: Direct costs and indirect costs. Direct costs These are costs that are attributed to a particular cost object or cost pool. These are costs that are avoidable if the cost object in question is not produced. These costs include: (a) Direct materials - e.g. raw materials (b) Direct labour - e.g. production wages (c) Direct expenses - e.g. royalties, carriage inwards, subcontracting Indirect costs These are costs that are incurred in an organisation for its wellbeing but cannot be attributed to a particular cost object or cost pool. These costs are referred to as overheads. They include: (a) Indirect materials - e.g. sand paper (b) Indirect labour - e.g. administrative salaries (c) Indirect expenses - e.g. rent and rates, electricity, telephone. Indirect expenses. These are the expenses that can not be linked to a particular product or job. For example the cost of hiring plant and machinery that is going to be used on various contracts is an indirect expense. Materials Labour Expenses Direct Indirect Direct Indirect Direct Indirect

Prime cost overheads. Prime cost is the summation of direct materials, direct labour and direct expenses while overheads is the summation of indirect materials , indirect labour and indirect expenses. N.B .: Although indirect costs (overheads) cannot be easily identified with particular cost objects, they are part of costs incurred in the production of output. They are supposed to be charged to output (cost object) and cost pools through a process known as overhead analysis. Costs in manufacturing and service organisations The costs in a manufacturing concern are as result of natural classification. We shall therefore entail much on the elements and the format of the manufacturing cost statement. The elements of cost can be illustrated below Indirect costs Material Labour Expenses Figure 1 : Elements of cost Prime cost Absorbed overhead Under/over- Absorbed overhead Production cost Profit and Trading Account Loss Account COST Production overheads Direct costs Materials Labour Expenses Overhead Costs Production Distribution Costs Administration Costs

(f) Preparing budgets. Cost information helps in forecasting the materials, labour and overhead cost that will be needed in the next period using the past information Illustrations: FIXED AND VARIABLE COSTS (a) Characteristics of Variable Costs: (i) Total Variable Costs (TVC) vary in direct proportion to Volume; (ii) Unit Variable Cost (UVC) remains constant as Volume changes; (iii) Variable costs are easier to assign to products and departments; (iv) Variable costs are controllable at any level. Example 1: Assume UVC is $20 per piece: UVC VOLUME TVC $20 100 $2, $20 200 $4, $20 400 $8, Example 2: Assume UVC is $30 per piece: UVC VOLUME TVC $30 150 $4, $30 300 $9, $30 600 $18, (b) Characteristics of Fixed Costs: (i) Total Fixed Costs (TFC) remain constant as volume increases or decreases, within the relevant range; (ii) The Unit Fixed Cost (UFC) varies inversely with volume i.e., As volume increases UFC decreases; As volume decreases UFC increases; Example: Assume TFC is $12,000. Volume UFC 2,000 $6 12000/2000 = 6 4,000 $3 12000/4000=

(iii) Assignment of FC to products and departments is difficult and arbitrary; (iv) Control of FC rests with the top management ; (v) Examples of types of FC are on page 9 - 12. (c) Revenue vs Capital Expenditure: A capital expenditure is intended to benefit future periods and is classified as an asset; A revenue expenditure benefits the current period and is termed an expense. An expenditure ( capital expenditure) classified originally as an asset will flow into the expense (will expire into an expense) stream when an asset is either consumed or used or charged off or written off ( Cfr, the five cases of asset expirations). PREPARATION OF STATEMENT OF COST OF GOODS MANUFACTURED AND COST OF GOODS SOLD: (a) Statement of cost of goods manufactured : $ Direct Materials used 60 Add: Direct labor 15 Prime costs 75 Add : Indirect materials 5 Indirect labor 2 Other indirect costs 3 Total Factory Overheads 10 Total manufacturing costs 85 Add: Opening W.I.P Less: Closing Work In Progress 0 Cost of Goods Manufactured 85 (b) Statement of cost of goods sol: Opening balance of finished goods 20 Add: Cost of goods manufactured (supra) 85 Goods Available for Sale (GAS) 105 Less : Closing balance of Finished goods 015 Cost of Goods Sold 90

- Budgetary control: Any procurement of materials should have been budgeted for. There should be adequate resources for the budgeted / intended purchases.

- Purchase initiation. The person / department requesting for materials should raise a purchase requisition form and send it to the purchasing department. The storekeeper can also raise the purchase requisition if the items have gone to a re-order level. The purchasing department should verify whether the materials are actually required.

- Tendering Process. The purchasing department having received the purchase requisitions from various departments should advertise and invite tenders. Opening and evaluation of the tenders should be in a transparent way.

- Purchase order: When the supplier has been selected, the purchasing department issues a purchase order form to the successful supplier. For local purchasers a document called a local purchase order (LPO) is raised. It’s a document that authorizes the suppliers to go ahead and supply. For internal control purposes the LPO should be authorized by more than one person. [Letters of Credit]

- Receipt of Materials. The supplier usually sends the materials with the delivery Note. On receiving the materials the delivery Note should be reconciled with the Purchase Order to know whether what was received is what was ordered for. The items should then be physically counted, measured or weighed at that point. The inspection team should be comprised of among others officers from the user department. An inspection Note containing stock observation of the conditions of goods should be raised. If the quality and quantity of goods is satisfactory a Goods Received Note is raised and signed.

- Payment. After delivery the suppliers raises an invoice demanding for payment. On the receipt of the Invoice it should be sent to the accounts officer for approval who then sends this to the accounts department for payment. In the accounts department all documents related to the purchase should be merged together checked for arithmetic errors and the payment voucher is prepared before a cheque is issued. The cheques are compared and signed against the voucher together with other documents which are sent to the internal audit department for examination. Payments may be by crossed cheques and after payments all documents related to the purchase are stamped PAID. STORE KEEPING AND STOCK CONTROL. Store keeping means the keeping of materials and store records. It’s the responsibility of the stores department to receive the materials and hold them until they are required by the production department. The department also maintains adequate records relating to these materials. The records show the receipts, issues and stock balance of materials. A bin card is used for this purpose this is a simple record of receipts, issues, and balances of stock at hand kept by the store keepers. MAIN FEATURES OF EFFECTIVE & STOREKEEPING.

- Immediate location of materials.

- Keeping correct and up to date records of receipts, issues and stock balances of materials

- Speedy receipt and issue of materials

- Full identification of materials at all times

- Protection of materials against fire & theft

- Protection of materials against deterioration

- Economical use of storage space. STOCK CONTROL This means making sure that the business has the right quantity of stocks, in the right place and at the right time. The stock level must neither be too high nor too low because of the associated costs. Too high levels of stock imply increased carrying costs like storage charges, lighting, and security e.t.c. A very low level of stock is associated with stock out costs like failure to meet the production demands which would result in loss of customers. STOCK CONTROL TERMINOLOGY

- Lead / Procurement time – period of time between ordering (externally or internally) and replenishment i.e. when the goods are available for use.

- Economic Ordering Quantity (EOQ). This as a calculated re-orders quantity which minimizes the balances of costs between carrying costs and ordering costs.

- Buffer stock / Minimum / Safety stock – a stock allowance to cover errors in forecasting the lead time or the demand during the lead time.

- Maximum stock level – A stock level calculated as the Maximum desirable which is used as an indicator to management to show when stock have risen too high.

- Re-order level – The level of stock (usually free stock) at which a further replenishment order should be placed. Re-order level is dependant on the lead time and the rate of during the lead time.

- Re-order quantity – The quantity of the replenishment order frequently but not always the EOQ. Formulae. Minimum stock level= Reorder level –( average rate of consumption x average lead time) Maximum stock level = Reorder level +EOQ –(minimum consumption x minimum lead time) Reorder level= maximum usage x maximum lead time. Example: Suppose the usage of x-ray films is 2000 units during the 100 day period. Ordering costs is 100/= per order, carrying costs is 10/=. Determine the optimal economic order quantity.