Download microeconomic........ and more Exercises Microeconomics in PDF only on Docsity!

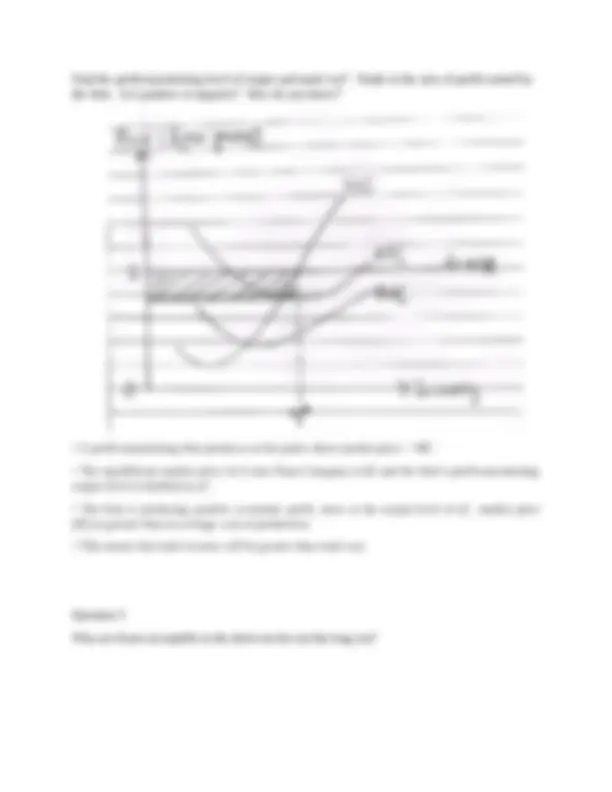

Chapter 8 : Short Run Costs and Output Decisions Question 1 Refer to the graph above. Assume the price of labour is $5.00 and the price of capital is $10. and the firm's fixed costs are $15. What production technique will be used to produce the first unit of output? The second? The third? What are the firm's total variable costs, total costs, and marginal costs of producing one unit of output? Two units of output? Three units of output? Unit of output produced Technique Fixed cost Capital (K) Labour (L) Total cost per unit 1 A 15 2(10)=20 2(5)=10 45 1 B 15 1(10)=10 3(5)=15 40 2 A 15 3(10)=30 3(5)=15 60 2 B 15 2(10)=20 6(5)=30 65 3 A 15 4(10)=40 4(5)=20 75 3 B 15 3(10)=30 6(5)=30 75 Firm will use the technique B to produce the first unit of output, and technique A for the second output to save the cost of produce. For the third output, the firm can choose either technique A or technique B as the cost of produce for two techniques are the same. Unit of output produced Total fixed cost Total variable cost Total cost Marginal cost 1 15 10+15=25 40 25 2 15 30+15=45 60 20 3 15 40+20=60 75 15 Question 2 Given the marginal product curve depicted below draw a marginal cost curve that would likely be the result. Explain why it looks this way.

The curve above draw a declining marginal product curve. It is because every firm is constrained by some fixed input that leads to diminishing returns to variable inputs and limits its capacity to produce. So the marginal product at that time will in a shape of declining because of the limited production. Question 3 You run a firm that produces T-shirts that are sold in a perfectly competitive market. Your firm faces the following cost and revenue schedule: Quantity Price TR T C Profit MR MC FC VC ATC AVC 0 12 5 ----^ ----^5 ----^ ---- 1 12 2 22 3 33 4 45 5 60 6 78 Fill in the table above. What is your firm's profit maximizing level of output?

Question 5 The figure below shows the demand, average total, and average variable cost curve for Pepe's Pet Salon which produces pet haircuts in a perfectly competitive market: Suppose that the firm's manager decides to produce 15 units of output. He asks your opinion of this decision. What would you tell him? A perfectly competitive firm equates its Marginal cost with Price. When output is 15 units, corresponding price is 20 (from P*=MR line). ATC at that output level is 14, so firm will make economic profit since Price > ATC. However, since Price > MC when output is 15, the firm is earning a marginal profit which can be increased by increasing output until Price equals MC at output of 20 units. So, the manager should increase output to 20 units. Question 6 What happens to a firm's profit-maximizing level of output if the price of the product rises? Use a graph to explain your answer.

MR=MC. When the price of product rises, the profit-maximizing level increase. The quantity will also increase when the price of the product rises because firms will produce as long as marginal revenue exceeds marginal cost. This is because producing more output will increase total profits as long as marginal revenue is positive.

Using Figure 9.1, explain what a firm would do in the short run if the market price of its product were at P3 and it produced Q3. Is the firm earning an economic profit? Explain.

- Market price (P3) is equal to Marginal cost (MC) and average total cost (ATC) at the production level Q3.

- The firm will not gain economic profit because the firm operating at a break-even point where the revenue generated exactly covers the total cost incurred.

- The firm would assess its production capacity to determine if it can meet the demand for Q3.

- If the firm has spare capacity, it may continue producing at the current level. However, if it is operating at full capacity or facing production constraints, it may need to make adjustments. Using Figure 9.1, explain what a firm would do in the short run if the market price of its product were at P4 and it produced Q4. Is the firm earning an economic profit? Explain.

- The market price (P4) is higher than the marginal cost (MC), the firm can generate additional revenue by producing more units.

- The firm also can do some expansion of output.

- When the market price is higher than both the marginal cost (MC) and the average total cost (ATC), It shows that the firm is making a profit and covering all of its costs on a per-unit basis.

- The firm will gain an earning an economic profit when price is higher than both the marginal cost (MC) and the average total cost (ATC). Question 2 The Lotsa Pasta Company sells pasta in a perfectly competitive market at a price of $2 per pound. Its marginal cost, average variable cost, and average total cost curves can be seen below:

Find the profit-maximizing level of output and mark it q*. Shade in the area of profit earned by the firm. Is it positive or negative? How do you know?

- A profit-maximizing firm produces at the point where market price = MC.

- The equilibrium market price for Lotsa Pasta Company is $2 and the firm’s profit-maximizing output level is labelled as q*.

- The firm is producing positive economic profit, since at the output level of q*, market price ($2) is greater than its average cost of production.

- This means that total revenue will be greater than total cost. Question 3 Why are losses acceptable in the short run but not the long run?

Regarding the firm's decision to continue producing in the short run, we need to consider whether it can cover its variable costs. In this case, the total variable costs are $175,000, which is greater than the total revenue of $100,000. This means the firm is unable to cover its variable costs, let alone its fixed costs. In the short run, the firm should evaluate whether it's feasible to continue production at a loss or consider shutting down operations temporarily until conditions improve. Long run In the long run, if conditions don't change, the firm should assess whether it can sustain its operations and generate profits. If the losses persist and there are no signs of improvement, the firm might need to consider exiting the market or finding alternative strategies to reduce costs or increase revenue. Long-run sustainability is crucial for the firm's survival and growth. Question 6 The figures below show the supply and demand for a perfectly competitive industry and the cost curves for a representative firm in the industry. Explain what will happen in the long run in this industry. Show your answer in a graph. Firms in the industry are earning positive profits because price is greater than average cost at the profit-maximizing level of output. Therefore, existing firms will increase their scale since there are economies of scale as shown by the fall in the long-run average costs as quantity rises above q*. The industry supply curve will shift right. Price will be driven to the minimum point on the long-run average cost curve. Firms will produce at their optimal scales.