Download Accounting Concepts and Principles: Current Assets Calculation and more Study notes Mathematics in PDF only on Docsity!

A. C.

B. D.

A. C.

B. D.

A

B. C. D.

- Arrrr

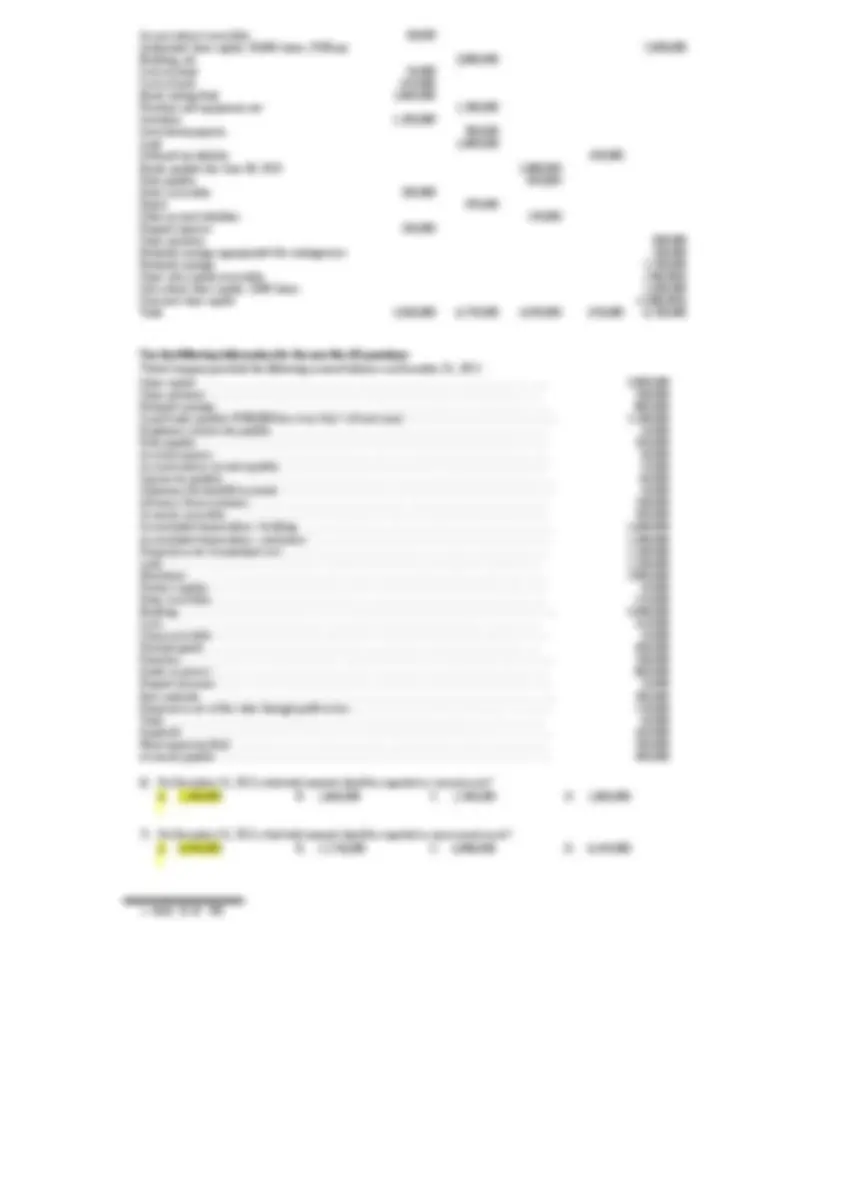

Use the following information for the next two (2) questions: Presented below is the statement of financial position of Simple Corporation prepared by the chief accountant for the current year,

Simple Corporation Statement of Financial Position December 31, 2020 Current assets P 435, Investments 640, Property plant, and equipment 1,720, Intangible assets 305, P3,100,

Current liabilities P 330, Long-term liabilities 1,000, Shareholders’ equity 1,770, P3,100,

Consider the following information:

(a) The current assets section includes: cash P100,000, accounts receivable P170,000 less P10,000 for allowance for doubtful

accounts, inventories P180,000, and unearned revenue P5,000. The cash balance is composed of P114,000, less a bank overdraft of P14,000. Inventories are stated on the lower of FIFO cost or market.

(b) The investments section includes: the cash surrender value of a life insurance contract P40,000; investment in ordinary shares, short-term (trading) P80,000 and long-term (available-for-sale) P270,000; and bond sinking fund P250,000. The cost and fair value of investments in ordinary shares are the same.

(c) Property, plant, and equipment includes: buildings P1,040,000 less accumulated depreciation P360,000; equipment P450, less accumulated depreciation P180,000; land P500,000; and land held for future use P270,000.

(d) Intangible assets include: a franchise P165,000: goodwill P100,000; and discount on bonds payable P40,000.

(e) Current liabilities include: accounts payable P90,000; notes payable - short term P80,000 and long - term P120,000: and taxes payable P40,000.

(f) Long - term liabilities are compose solely of 10% bonds payable due 2027.

(g) Shareholders' equity has: preference shares, no par value, authorized 200,000 shares, issued 70,000 shares for P450,000; and ordinary shares, P1.00 par value, authorized 400,000 shares, issued 100,000 shares at an average price of P10. In addition, the corporation has retained earnings of P320,000.

Compute the adjusted amount to be reported on the company’s statement of financial position as of December 31, 2020:

- Current assets

A .

548,000 B. 574,000 C. 534,000 D. 588,

- Current liabilities A .

224,000 B. 229,000 C. 210,000 D. 215,

- Therry Company is preparing interim financial statements for the first quarter ended March 31.

Expenses in the first quarter totaled P5,000,000 of which 25% was variable

The fixed expenses included property tax for the year of P1,600,000 and depreciation expense P800,000 for the year for an equipment that was available for use on January 1. What amount should be reported as total expenses for the first quarter ended March 31? A .

5,000,000 B. 2,600,000 C. 3,800,000 D. 3,200,

- Yasmin Company is completing the preparation of the financial statements for the year ended December 31, 2023. The financial

statements are authorized for issue on March 31, 2024.

On March 15, 2024, a dividend of P1,800,000 was declared and a contractual profit share payment of P400,000 was made, both based on the profit for the year ended December 31, 2023. On February 1, 2024, a customer went into liquidation having owned the entity P300,000 for the past 5 months. On March 20, 2024, a manufacturing plant was destroyed by fire resulting in a financial loss of P2,600,000.

What total amount should be recognized in profit or loss for the year ended December 31, 2023 to reflect adjusting events after the end of reporting period? A .

1,800,000 B. 2,500,000 C. 2,600,000 D. 700,

Use the following information for the next two (2) questions:

Share capital............................................................ 5,000, Waitz Company provided the following account balances on December 31, 2022:

Cash and cash equivalents...... 500,

Accounts receivable 800, Inventory 1,700, Prepaid expenses 250, Property, plant and equipment 8,800, Accumulated depreciation 800, Accounts payable 1,350, Accrued expenses 250, Bonds payable 3,150, Share capital 6,000,

Retained earnings 2,700,

A P600,000 note payable to bank, due on June 30, 2024, was deducted from the balance on deposit n the same bank. Gabrielle

recorded checks of P200,000 in payment of accounts payable on December 31, 2023. These checks were still on hand on January

20, 2024. An advance payment of P150,000 from a customer for goods to be delivered in 2024 was deducted from accounts

receivable. The share capital included redeemable preference shares of P1,000,000 due for redemption on October 31, 2024.

- What total amount should be reported as current asset on December 31, 2023?

A .

3,450,000 B. 3,600,000 C. 4,200,000 D. 4,050,

- What total amount should be reported as current liabilities on December 31, 2023?

A .

2,400,000 B. 3,550,000 C. 3,400,000 D. 2,550,

- Transcend Company operates two major lines of business namely, candle manufacturing and clothing retailing. On December

31, 2023, in response to an unsolicited offer, Transcend Company disposed of its candle-making operations for P1,000, when the carrying amount of the operation’s asset were – factory building, P400,000; machinery, P00,000 and trademark, P200,000. The candle-making operations has no other assets and has no liability, but as a result of the disposal the company has an income tax payable of P30,000 related to the gain on disposal. The candle-making has profit before tax of P300,000 for the year ended December 31, 2023. In the statement of comprehensive income, what single amount should Transcend Company disclose related to the discontinued operation? A .

280,000 B. 300,000 C. 370,000 D. 400,

Accounts receivable...... 400, Thanos Company provided the following account balances on December 31, 2022:

Accounts payable, P125,000; Accrued taxes, P50,000; Cash surrender value of life insurance, P30,000; Ordinary share capital, P1,000,000; Share dividend payable-ordinary, P150,000; Mortgage payable (P200,000 due in six months), P1,200,000; Notes payable-20%, due on January 2, 2024, P1,500,000; Share premium-ordinary, P250,000; Preference liability, P450,000; Accumulated profits-December 31, 2023, P550,000; Unearned rent income, P25,000; Dividends payable-preference liability, P100,000. How much should McGraw report as Shareholders’ equity on December 31, 2023? A .

1,900,000 B. 1,950,000 C. 2,050,000 D. 2,500,

- The following accounts are taken from the unadjusted trial balance of Flower Company on December 31, 2023:

Cash, P340,000; Accounts receivable, P850,000; Allowance for bad debts, P8,000; Notes receivable, P360,000; Prepaid rent expense, P20,000; Trading security investment, P300,000; Merchandise inventory, P600,000; Accounts payable, P500,000; Notes payable, P700,000;

Additional information: Cash consists of Cash in Bank per book (outstanding checks, P24,000) 334,

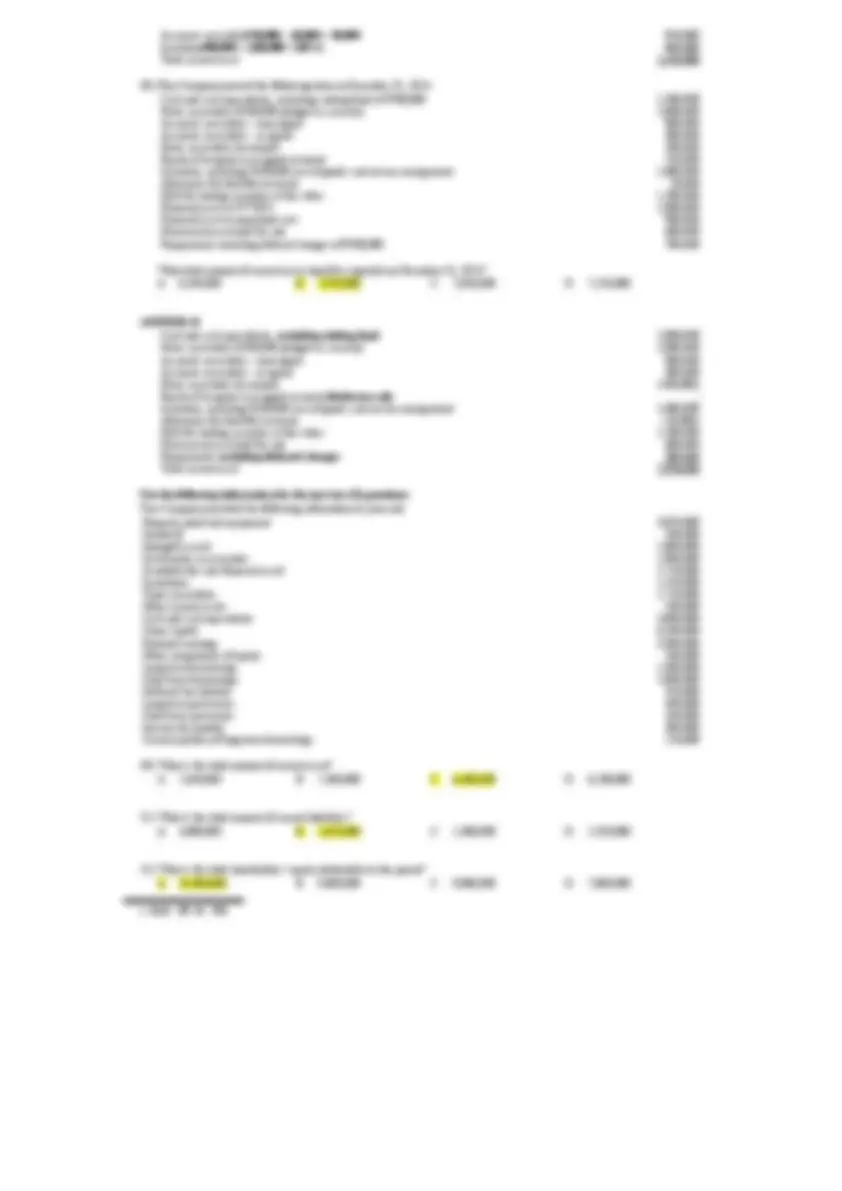

Use the following information for the next four (4) questions:

Babes Company provided the following trial balance on December 31, 2020 which has been adjusted except for income tax expense:

Debit Credit

Building...... 5,000,

Accounts receivables 14,000, Inventory 10,000, Property, plant and equipment 25,000, Accounts payable 12,000,

Income tax payable............................................................ 60,

Ordinary share capital 15,000, Share premium 4,000, Retained earnings 1/1 8,000, Net sales and other revenue 80,000, Costs and expenses 60,000, Income tax expense 11,000,. 125,000,000 125,000,

- What amount should be reported as adjusted retained earnings on December 31, 2020?

A .

29,000,000 B. 22,000,000 C. 14,000,000 D. 17,000,

- The correcting entry to adjust income tax includes which of the following?

A. Debit income tax expense P6,000,000 C. Debit income tax payable P6,000, B. Credit income tax expense P5,000,000 D. No correction is necessary

- What amount should be reported as total current liabilities on December 31, 2020?

A .

12,000,000 B. 13,000,000 C. 18,000,000 D. 33,000,

- What amount should be reported as total shareholders’ equity on December 31, 2020?

A .

19,000,000 B. 36,000,000 C. 41,000,000 D. 46,000,

Use the following information for the next two (2) questions:

Use the following information for the next two (2) questions: Casio Company reported the following current assets on December 31, 2022:

Cash 5,000, Accounts receivable 2,000, Inventory, including goods received on consignment P200,000 800, Bonds investment at fair value through other comprehensive income 1,000, Prepaid expenses, including a deposit of P50,000 made on inventory to be delivered in 18 months 150,

Total current liability 1,120,

Cash in general checking account 3,500, Cash fund to be used to retire bonds payable in 2024 1,000, Cash held to pay value added taxes 500, Total cash 5,000,

- What is the correct amount of cash balance to be reported as current asset?

A .

5,000,000 B. 4,500,000 C. 4,000,000 D. 3,500,

- What total amount of current assets should be reported on December 31, 2022?

A .

6,750,000 B. 6,700,000 C. 7,700,000 D. 7,750,

Use the following information for the next four (4) questions:

Babes Company provided the following trial balance on December 31, 2020 which has been adjusted except for income tax expense:

Debit Credit Cash 5,000, Accounts receivables 14,000, Inventory 10,000, Property, plant and equipment 25,000, Accounts payable 12,000,

Income tax payable............................................................ 60,

Ordinary share capital 15,000, Share premium 4,000, Retained earnings 1/1 8,000, Net sales and other revenue 80,000, Costs and expenses 60,000, Income tax expense 11,000,. 125,000,000 125,000,

- What amount should be reported as adjusted retained earnings on December 31, 2020?

A .

29,000,000 B. 22,000,000 C. 14,000,000 D. 17,000,

- The correcting entry to adjust income tax includes which of the following?

A. Debit income tax expense P6,000,000 C. Debit income tax payable P6,000, B. Credit income tax expense P5,000,000 D. No correction is necessary

- What amount should be reported as total current liabilities on December 31, 2020?

A .

12,000,000 B. 13,000,000 C. 18,000,000 D. 33,000,

- What amount should be reported as total shareholders’ equity on December 31, 2020?

A .

19,000,000 B. 36,000,000 C. 41,000,000 D. 46,000,

Use the following information for the next two (2) questions:

Quake Company reported the following current assets on December 31, 2022:

Cash 4,500, Accounts receivable 7,500, Noes receivable, net of discounted note P500,000 2,000,

Building............................................................ 4,000,

Total 18,000,

An analysis disclosed that accounts receivable comprised the following:

Trade accounts receivable 5,000,

Allowance for doubtful accounts............................................................ 50,

Selling price of Quake Company’s unsold goods sent to Tar Company on consignment at 150% of cost and excluded from Quake’s ending inventory 3,000, Total 18,000,

- What is the net realizable value of accounts receivable?

A .

7,500,000 B. 4,500,000 C. 5,000,000 D. 6,500,

- On December 31, 2022, what amount should be reported as total current assets?

A .

17,000,000 B. 17,500,000 C. 15,000,000 D. 16,000,

- Bane Company reported the following current asset at year-end:

Cash 3,200, Accounts receivable 3,000, Inventory 2,800, Deferred charges 200, Total current assets 9,200,

The accounts receivable consisted of the following: Customers’ accounts 1,420, Employees’ account-current 240, Advances to subsidiary 260, Allowance for uncollectible accounts (120,000) Subscription receivable, not collectible currently 1,200, Total accounts receivable 3,000,

What total amount should be reported as current asset at year-end? A .

8,000,000 B. 9,200,000 C. 7,740,000 D. 7,540,

- What is the amount of current assets on December 31?

A .

220,000 B. 130,000 C. 90,000 D. 40,

- What is the shareholders’ equity on December 31? A .

1,170,000 B. 1,110,000 C. 1,050,000 D. 1,080,

- What is the amount of noncurrent liabilities on December 31?

A .

540,000 B. 480,000 C. 620,000 D. 750,

Use the following information for the next five (5) questions: Dr. Strangest Company provided the following account balances on December 31, 2022:

Accounts payable 1,000, Accounts receivable, net of allowance for doubtful accounts P50,000 600, Accrued taxes 50, Accrue interest receivable 30, Authorized share capital, 50,000 shares, P100 par 5,000, Building, net of accumulated depreciation of P2,500,000 3,000, Cash on hand 50, Cash in bank 650, Bond sinking fund 2,000, Furniture and equipment, net of accumulated depreciation of P900,000 1,500, Inventory 1,200, Investment property 700,

Equipment...... 1,000,

Deferred tax liability 650, Bonds payable due June 30, 2023 2,000, Note payable 850, Notes receivable 200, Patent 370, Other accrued liabilities 150, Prepaid expenses 100, Share premium 300,

Retained earnings appropriated for contingencies 200,

Retained earnings 2,700,

Share premium............................................................ 500,

Subscribed share capital, 2,000 shares 1,000,

Preference share capital...... 2,000,

- On December 31, 2022, what total amount should be reported as current assets?

A .

4,830,000 B. 2,830,000 C. 2,830,000 D. 2,870,

- On December 31, 2022, what total amount should be reported as non-current assets?

A .

7,870,000 B. 8,570,000 C. 6,570,000 D. 5,870,

- On December 31, 2022, what total amount should be reported as current liabilities?

A .

4,050,000 B. 2,050,000 C. 2,700,000 D. 3,900,

- On December 31, 2022, what total amount should be reported as non-current liabilities?

A .

2,650,000 B. 650,000 C. 1,500,000 D. 0

- On December 31, 2022, what is the total shareholder’s equity?

A .

6,700,000 B. 7,700,000 C. 7,200,000 D. 8,700,

CA NCA CL NCL SHE

Accounts payable 1,000, Accounts receivable, net 600, Accrued taxes 50,

Share subscription receivable (500,000)

Use the following information for the next five (5) questions:

- On December 31, 2022, what total amount should be reported as current assets?

A

- On December 31, 2022, what total amount should be reported as non-current assets?

A

Allowance for doubtful accounts............................................................ ............................................ (50,000)

Accumulated depreciation – building............................................................ 1,600,

Use the following information for the next five (5) questions:

- Accrue interest receivable 30,

- Authorized share capital, 50,000 shares, P100 par 5,000,

- Building, net 3,000,

- Cash on hand 50,

- Cash in bank 650,

- Bond sinking fund 2,000,

- Furniture and equipment, net 1,500,

- Inventory 1,200,

- Investment property 700,

- Land 1,000,

- Deferred tax liability 650,

- Bonds payable due June 30, 2023 2,000,

- Note payable 850,

- Notes receivable 200,

- Patent 370,

- Other accrued liabilities 150,

- Prepaid expenses 100,

- Share premium 300,

- Retained earnings appropriated for contingencies 200,

- Retained earnings 2,700,

- Subscribed share capital, 2,000 shares 1,000,

- Total 4,830,000 6,570,000 4,050,000 650,000 6,700, Unissued share capital (2,000,000)

- Share capital............................................................ 5,000, Waitz Company provided the following account balances on December 31, 2022:

- Share premium............................................................ 500,

- Retained earnings............................................................ 880,

- Serial bonds payable (P500,000 due every July 1 of each year)............................................................ 2,500,

- Employees income tax payable............................................................ 20,

- Note payable............................................................ 100,

- Accrued expense............................................................ 30,

- Accrued interest on note payable............................................................ 10,

- Income tax payable............................................................ 60,

- Allowance for doubtful accounts............................................................ 50,

- Advances from customers............................................................ 100,

- Accounts receivable............................................................ 500,

- Accumulated depreciation – building............................................................ 1,600,

- Accumulated depreciation – machinery............................................................ 1,300,

- Financial assets at amortized cost............................................................ 1,500,

- Land............................................................ 1,500,

- Machinery............................................................ 2,000,

- Factory supplies............................................................ 50,

- Notes receivable............................................................ 150,

- Building............................................................ 4,000,

- Cash............................................................ 420,

- Claim receivable............................................................ 20,

- Finished goods............................................................ 400,

- Franchise............................................................ 200,

- Goods in process............................................................ 600,

- Prepaid insurance............................................................ 20,

- Raw materials............................................................ 200,

- Financial assets at fair value through profit or loss............................................................ 250,

- Tools............................................................ 40,

- Goodwill............................................................ 100,

- Plant expansion fund............................................................ 500,

- Accounts payable............................................................ 300,

- 2,560,000 B. 2,660,000 C. 2,760,000 D. 2,860,

- 6,940,000 B. 12,740,000 C. 6,980,000 D. 6,440,

- Accounts receivable............................................................ 500,

- Factory supplies............................................................ 50,

- Notes receivable............................................................ 150,

- Cash............................................................ 420,

- Claim receivable............................................................ 20,

- Finished goods............................................................ 400,

- Goods in process............................................................ 600,

- Prepaid insurance............................................................ 20,

- Raw materials............................................................ 200,

- Financial assets at fair value through profit or loss............................................................ 250,

- Total current asset 2,560,

- Financial assets at amortized cost............................................................ 1,500, Accumulated depreciation – machinery............................................................ (1,300,000)

- Land............................................................ 1,500,

- Machinery............................................................ 2,000,

- Building............................................................ 4,000,

- Franchise............................................................ 200,

- Tools............................................................ 40,

- Goodwill............................................................ 100,

- Plant expansion fund............................................................ 500,

- Total noncurrent asset 6,940,

- Serial bonds payable – current portion 500,

- Employees income tax payable............................................................ 20,

- Note payable............................................................ 100,

- Accrued expense............................................................ 30,

- Accrued interest on note payable............................................................ 10,

- Income tax payable............................................................ 60,

- Advances from customers............................................................ 100,

- Accounts payable............................................................ 300,

- Total current liability 1,120,

- Serial bonds payable non current portion 2,500,000 – 500,000 2,000,

- Accounts receivable...... 400, Thanos Company provided the following account balances on December 31, 2022:

- Advances to officers – not currently collectible...... 100,

- Sinking fund...... 400,

- Building...... 5,000,

- Long term refundable deposit...... 50,

- Cash and cash equivalents...... 500,

- Cash surrender value...... 60,

- Equipment...... 1,000,

- Lease rights...... 100,

- Accrued interest on notes receivable...... 10,

- Inventories...... 1,300,

- Land...... 1,500,

- Land held for speculation...... 500,

- Notes receivable...... 250,

- Computer software...... 3,250,

- Prepaid expenses...... 70,

- Financial assets held for trading...... 280,

- Unearned rent income... 40,

- Share premium – preference...... 500, Retained earnings (deficit) (1,800,000)

- Premium on bonds payable...... 1,000,

- Preference share capital...... 2,000,

- Share premium – ordinary...... 200,

- Note payable...... 300,

- SSS payable...... 10,

- Accounts payable...... 400,

- Accrued salaries...... 100,

- Accumulated depreciation – building...... 2,000,

- Accumulated depreciation – equipment...... 200,

- Allowance for doubtful accounts...... 20,

Bonds payable...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... 5,000, Dividends payable...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... 120, Ordinary share capital...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ... 5,000, Withholding tax payable...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... 30, Preference share redemption fund...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... .... 350,

- On December 31, 2022, what total amount should be reported as current assets?

A .

3,290,000 B. 2,890,000 C. 2,790,000 D. 2,810,

- On December 31, 2022, what total amount should be reported as non-current assets?

A .

10,110,000 B. 10,010,000 C. 9,760,000 D. 9,610,

- On December 31, 2022, what total amount should be reported as current liabilities?

A .

960,000 B. 1,000,0000 C. 940,000 D. 880,

- On December 31, 2022, what total amount should be reported as non-current liabilities?

A .

6,000,000 B. 5,000,000 C. 6,120,000 D. 5,120,

- On December 31, 2022, what is the total shareholder’s equity? A .

2,700,000 B. 1,900,000 C. 5,500,000 D. 5,900,

Accounts payable...... 400,

Cash and cash equivalents...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... 500,

Accrued interest on note payable............................................................ 10,

Inventories...... 1,300,

Notes receivable...... 250,

Prepaid expenses...... 70,

Financial assets held for trading...... 280,

Allowance for doubtful accounts...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ..... (20,000)

Total noncurrent asset 6,940,

Advances to officers – not currently collectible...... 100,

Sinking fund...... 400,

Building...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... 5,000,

Long term refundable deposit...... 50,

Cash surrender value...... 60,

Equipment...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... 1,000,

Lease rights...... 100,

Land...... 1,500,

Land held for speculation...... 500,

Computer software...... 3,250,

Accumulated depreciation – machinery............................................................ 1,300,

Accumulated depreciation – equipment...... 200,

Preference share redemption fund...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... .... 350, Total noncurrent asset 10,110,

Note payable...... 300,

SSS payable...... 10,

Accounts payable...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... 400,

Accrued salaries...... 100,

Dividends payable...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... 120, Withholding tax payable...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... 30, Total current liabilities 1,000,

Bonds payable...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... ...... 5,000,

Premium on bonds payable...... 1,000,

Total noncurrent liability 6,000,

Total asset 2,790,000 + 10,110,000 12,900, Total liability 1,000,000 + 6,000,000 (7,000,000) Shareholders’ equity 5,900, Use the following information for the next five (5) questions: Dr. Stranger Company provided the following information on December 31, 2022:

RE appropriated for contingencies 100, Share capital 3,000,

Share premium 300,

Retained earnings unappropriated 1,250, Trademark 150, Secret process and formula 200, Bank loan payable – due June 30, 2024 500, Total 2,250,000 7,250,000 2,250,

- The ledger of Husky Company as of December 31, 2021 includes the following:

Asset Cash 5, Trade accounts receivable (net of P5,000 credit balance in accounts) 20, Held for trading securities 40,

Financial assets at amortized cost............................................................ 1,500,

Investment in equity securities at FVOCI 35, Investment in bonds measured at amortized cost (due in 3 years) 30, Prepaid assets 5, Deferred tax asset (expected to reverse in 2022) 6, Investment in associate 18, Investment property 23, Sinking fund 19, Property, plant, and equipment 50, Goodwill 14, Total 280,

How much is the total current assets? A .

125,000 B. 96,000 C. 95,000 D. 90,

- The ledger of Wagg Company as of December 31, 2021 includes the following:

Liabilities Bank overdraft 5, Trade accounts payable (net of P5,000 debit balance in accounts) 20, Note payable (due in 20 semi-annual payments of P2,000) 40, Interest payable 15, Bonds payable (due on March 31, 2022) 35, Discount on bonds payable (15,000) Dividends payable 5, Share dividends payable 6, Deferred tax liability (expected to reverse in 2022) 18, Income tax payable 22, Contingent liability 50, Reserve for contingencies 14, Total 860,

How much is the total current liabilities? A .

96,000 B. 114,000 C. 146,000 D. 90,

Use the following information for the next three (3) questions:

The ledger of Poly Company in 2021 includes the following:

January 1, 2021 December 31, 2021 Current assets 600,000? Noncurrent assets 2,000,000? Current liabilities 450,000 500, Noncurrent liabilities? 1,500,

Additional information:

- Rottweiler’s working capital as of December 31, 2021 is twice as much as the working capital as of January 1, 2021.

- Total equity as of January 1, 2021 is P850,000. Profit for the year were P1,200,000 while dividends declared amounted to

P500,000. There were no other changes in equity during the year.

- How much is the noncurrent liabilities as of January 1, 2021?

A .

1,300,000 B. 1,325,000 C. 1,350,000 D. 1,250,

- How much is the current assets as of December 31, 2021?

A

800,000 B. 900,000 C. 850,000 D. 200,

- How much is the noncurrent assets as of December 31, 2021?

A .

3,000,000 B. 2,250,000 C. 2,750,000 D. 2,000,

- Selected information from the accounting records of Mabini Company is as follows: Accounts receivable at January 1 1,200, Accounts receivable at December 31 1,100, Account receivable turnover 6 to 1 Inventory at January 1 800, Inventory at December 31 1,400, Inventory turnover 5 to 1

What was the gross margin for end of year? A .

1,400,000 B. 1,300,000 C. 1,200,000 D. 1,500,

- The following unadjusted account balances have been reported on the financial statements by Tarlac Trucking Company on December 31, 2012:

Cash in bank 4,000,000 Petty cash fund 70, Notes receivable 3,000,000 Accounts receivable 5,000, Inventory 2,000,000 Deferred charges 350,

Cash in bank is net of a checking account’s bank overdraft amounting 250,000. Petty cash expenses have not been replenished for 20,000. Notes receivable includes discounted note of 800,000 while Accounts receivable balance is net of accounts with credit balances of 650,000. The total current assets for the Balance Sheet as of December 31, 2012 should be A .

12,950,000 B. 14,150,000 C. 12,850,000 D. 13,200,

- The following unadjusted account balances have been reported on the financial statements by Marilag Biscuit Company on

December 31, 2012:

Cash in bank 4,000,000; Notes receivable 3,000,000; Accounts receivable 5,000,000; Inventory 2,000,000; Deferred charges 350,000; Accounts payable 2,500,000; Notes payable 4,000,000; Accruals 1,500,000;

Cash in bank is net of a checking account’s bank overdraft amounting 250,000. Notes receivable includes discounted notes of 800,000 while Accounts receivable balance is net of accounts with credit balances of 650,000. Accounts payable is also net of accounts with debit balances of 500,000. The total current liabilities to be reported as of December 31, 2012 should be A .

8,900,000 B. 8,500,000 C. 8,000,000 D. 9,400,

- The following accounts came from the adjusted trial balances of Davao Pacific Company at December 31, 2012: Cash 750,000,

Accounts receivable, net 1,800,000, Prepaid taxes 400,000 Other Assets 110,000 Accounts payable 140,

During the year, the company granted special payment terms to a customer that requires the latter to pay equal semi annual installments of 150,000 for a 600,000 worth of goods and services. Installment dates are due every March 1 and September 1 starting year 2013. Estimated corporate tax payable of 400,000 was charged to prepaid taxes during the year. The corporate tax rate is 35%. There were no adjustments between financial and taxable income.

What is the amount of current assets that company should show in the financial statements? A .

2,550,000 B. 2,250,000 C. 2,950,000 D. 3,060,

- Jen Company is completing the preparation of its draft financial statements for the year ended December 31, 2009. The

financial statements are authorized for issue on March 31, 2010.

- The effective tax rate is 40%. No taxes have been paid.

- What is the net income for 2022?

A .

69,750 B. 55,050 C. 46,380 D. 41,

- What is the total current assets at year-end?

A .

220,000 B. 198,000 C. 197,700 D. 196,

- What is the total asset at year-end?

A .

417,700 B. 395,700 C. 307,450 D. 197,

- What is the total equity at year-end?

A .

395,700 B. 335,350 C. 307,450 D. 265,

- What is the total current liability at year-end?

A .

90,650 B. 88,250 C. 60,350 D. 48,

Use the following information for the next two (2) questions:

Down Ltd has completed its current year financial statements which reveal, in part, the following information.

- Profit for the year – P110,

- Total comprehensive income – P130,

- Other comprehensive income relates to the revaluation of land and building to fair value.

- Dividends paid – P35,

- Opening equity balances – share capital P300,000, retained earnings P220,000, asset revaluation surplus P60,

- No more share capital was issued during the reporting period

In accordance with PAS 1 Presentation of Financial Statements , determine the amount to be included in the statement of changes in

equity for the current year for the following:

- Closing retained earnings

A .

295,000 B. 315,000 C. 355,000 D. 375,

- Closing total equity

A .

580,000 B. 655,000 C. 675,000 D. 695,

- At December 31, 2022, the following require inclusion in a company’s financial statements:

- On January 1, 2022 the company made a loan of P12,000 to an employee, repayable on January 1, 2023, charging interest at 2% per year. On the due date she repaid the loan and paid the whole of the interest due on the loan that date.

- The company paid an annual insurance premium of P9,000 in 2022, covering the year ending August 31, 2023.

- In January 2023, the company received rent from a tenant of P4,000 covering the six months to December 31, 2022.

For these items, what should be included as current assets in the company’s statement of financial position as at December 31, 2022? A .

22,240 B. 19,240 C. 18,240 D. 15,

ANSWER: B

Advances to employee 12,000 + (12,000 x 2%) 12, Prepaid insurance 9,000 x 8/12 6, Rent receivable 4, Total current asset 22,

Use the following information for the next two (2) questions: RECHECK

The accounts and their balances appear in an unadjusted trial balance of BB Company as of December 31, 2021:

Cash and cash equivalents 400,000 Inventory 500, Trade and other receivables 2,000,000 Trade and other payables 670, Subscription receivable 375,000 Income tax payable 196,

Additional information:

- Trade and other receivables include long term advances to company officers amounting to P430,000.

- The subscription receivable has the following call dates: June 30, 2022, P200,000; December 31, 2022, P100,000; and June 30,

2023, P75,000.

- Inventory of P500,000 was determined by physical count. At December 31, 2021, goods costing P120,000 are in transit from a

supplier. Terms of purchase of said goods is FOB shipping point. The goods and the related invoice have not been received as of year end.

- Trade and other payable includes dividend payable amounting to P170,000, of which P70,000 is payable in cash P100,000 is

distributable in BB’s own shares.

- What is the total current assets at December 31, 2021?

A .

2,595,000 B. 2,670,000 C. 2,770,000 D. 2,895,

- What is the total current liability at December 31, 2021?

A .

866,500 B. 891,500 C. 766,500 D. 886,

ANSWER: Bonus, C

Cash and cash equivalents 400, Trade and other receivables 2,000,000 – 430,000 + 200,000 + 100,000 1,870, Inventory 500,000 + 120,000 620, Total 2,890,

Trade and other payable 670,000 – 100,000 690, Income tax 196, Total 766,

- The general ledger trial balance of Central Corporation includes the following statement of financial position accounts at December 31, 2021: Inventory (including inventory expected in the ordinary course of operations to be sold beyond 12 months amounting to P70,000) 110, Trade receivable 120, Prepaid insurance 8, Listed investments held for trading purposes at fair value 20, Available for sale investments 80, Cash and cash equivalents 30, Deferred tax asset 15, Bank overdraft 25,

The amount that should be reported as current assets on Central’s statement of financial position is A .

218,000 B. 368,000 C. 288,000 D. 298,

ANSWER: C

Inventory 110, Trade receivable 120, Prepaid insurance 8, Listed investments held for trading purposes at fair value 20, Cash and cash equivalents 30, Total 288,

- The liability section of the statement of financial position of Lalalalalalala Co. on December 31, 2021 showed:

Share dividends declared but not yet paid 50, Dividends in arrears on preference shares 25, Income tax withheld 1, Deferred income tax payable 10, Accounts payable, net of P5,000 debit balance in two supplier’s account 55, Bank overdraft with Metro Bank 12, Mortgage loans incurred in 2021 payable in ten annual installments starting July 1, 2022 500,

What amount should the total liabilities be shown? A .

18,500 B. 123,500 C. 173,500 D. 653,

- What is the total non-current liabilities at December 31, 2014? A .

1,000,000 B. 2,525,000 C. 2,550,000 D. 2,725,

- What is the total shareholders’ equity at December 31, 2014?

A .

1,700,000 B. 1,725,000 C. 2,500,000 D. 2,525,

ANSWER: A, C

Mortgage payable noncurrent portion 1,000,

Retained earnings, January 1, 2014 550, Profit for the year 500, Dividends declared (250,000) Retained earnings, December 31, 2014 800, Ordinary share capital, P100 par 1,000, Preference share capital, P200 par 450, Share premium – ordinary 250, Total shareholders’ equity 2,500,

- Jomilyne Inc. furnishes you with the following list of accounts:

Accounts payable 66, Accounts receivable 40, Accumulated depreciation 44, Advances to sales personnel 10, Advertising expense 72, Allowance for uncollectible accounts 10, Bonds payable 80, Cash 22, Certificates of deposit 16, Ordinary share capital, P10 par 100, Deferred tax liability 46, Equipment 215, Inventory 55, Investment in Dog Company (40% of outstanding) 76, Investment in Cat Company (held for trading) 21, Share premium 42, Premium on bonds payable 6, Prepaid insurance 6, Rent revenue 37, Rent revenue received in advance 12, Retained earnings 97, Taxes payable 10, Tools 52,

How much is the company’s working capital? A .

72,000 B. 66,000 C. 62,000 D. 46,

ANSWER: A

Current Asset Current Liability Working Capital Accounts payable 66, Accounts receivable 40, Advances to sales personnel 10, Allowance for uncollectible accounts (10,000) Cash 22, Certificates of deposit 16, Inventory 55, Investment in Cat Company (held for trading) 21, Prepaid insurance 6, Rent revenue received in advance 12, Taxes payable 10, 160,000 88,000 72,

Use the following information for the next four (4) questions:

The account balances shown below were gathered from Rica Mae Company’s adjusted trial balance.

Wages payable 250,000 Discount on bonds payable 48, Cash 175,000 Investment in associates 1,020,

Bonds payable 600,000 Taxes payable 228, Dividends payable 140,000 Accounts payable 248, Prepaid expenses 136,000 Accounts receivable 366, Inventory 820,000 Property, plant and equipment 1,200, Long-term funds 525,000 Goodwill 450, Trading securities 153,000 Advances from affiliated companies 900, Accumulated depreciation – PPE 400,000 Investment in equity securities, measured through OCI 300,

- What it the total current assets of the company?

A .

1,950,000 B. 1,650,000 C. 1,560,000 D. 830,

- What is the total current liabilities of the company?

A .

866,000 B. 726,000 C. 686,000 D. 638,

- What is the total non-current assets of the company?

A .

3,995,000 B. 3,950,000 C. 3,095,000 D. 2,795,

ANSWER: B, A, C

Current asset

Current liability

Noncurrent asset Wages payable 250, Cash 175, Bonds payable Dividends payable 140, Prepaid expenses 136, Inventory 820, Long-term funds 525, Trading securities 153, Accumulated depreciation – PPE (400,000) Discount on bonds payable Investment in associates 1,020, Taxes payable 228, Accounts payable 248, Accounts receivable 366, Property, plant and equipment 1,200, Goodwill 450, Advances from affiliated companies 900, Investment in equity securities, measured through OCI - - - Total 1,650,000 866,000 3,995,

Use the following information for the next two (2) questions:

Danica Company had the following assets at December 31, 2014:

Cash (of which P25,000 is earmarked for the acquisition of equipment) 490, Trading securities (including P200,000 investment in noncurrent available-for-sale securities) 380, Accounts receivable, net (including P500,000 due from an officer; no due date specified) 1,250, Non-trade notes receivable (due in equal semi-annual installments of P50,000 every March 1 and September 1) 300, Merchandise inventory 900, Prepaid expenses 80, Plant and equipment, net 3,750,

- How much is Danica Company’s total current asset?

A .

2,475,000 B. 2,425,000 C. 3,400,000 D. 2,745,

- How much is Danica Company’s total non-current assets?

A .

3,750,000 B. 4,675,000 C. 4,725,000 D. 4,750,

- Abigail Corporation is preparing its December 31, 2014 statement of financial position. The following items may be reported as

either current or non-current liability:

- On December 15, 2014, Abigail declared a cash dividend of P2.50 per share to shareholders of record on December 31. The dividend is payable on January 15, 2015. Abigail has issued 1,000,000 ordinary shares, of which 50,000 shares are held in treasury.