Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

1 / 52

This page cannot be seen from the preview

Don't miss anything!

GAIN, GARIS, GASCO, IBON, ICALLA

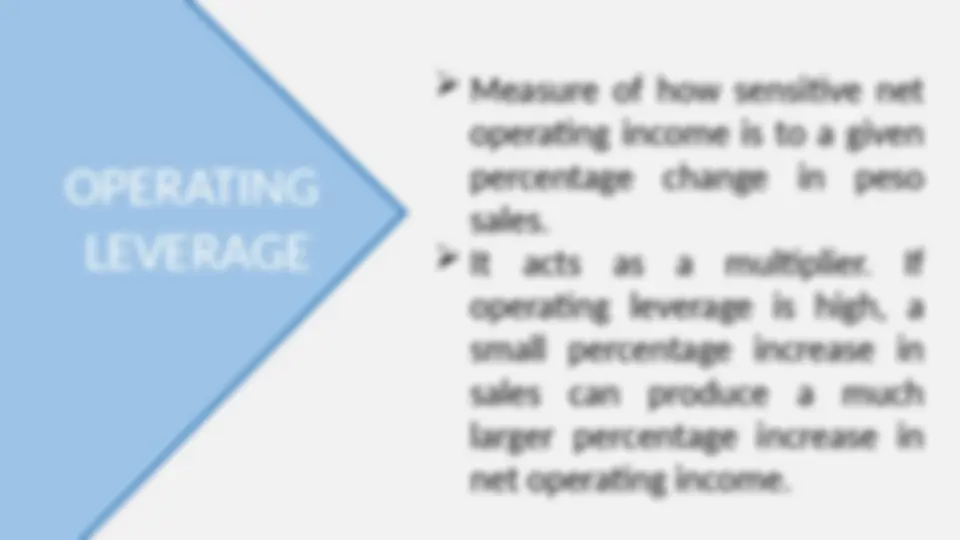

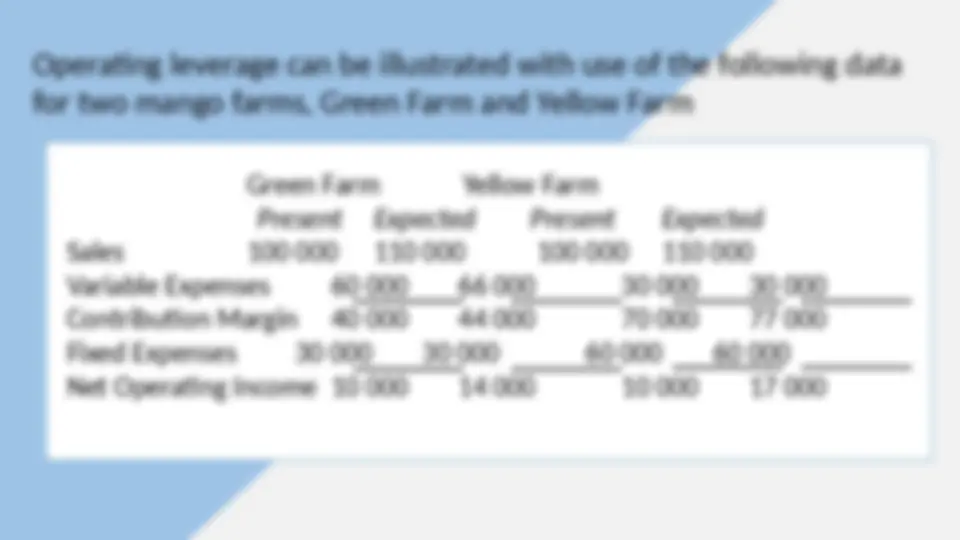

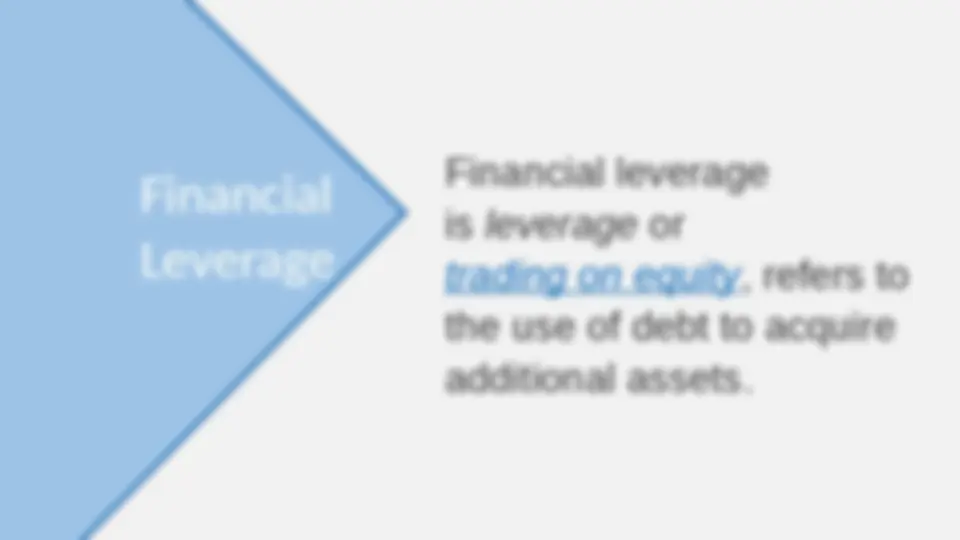

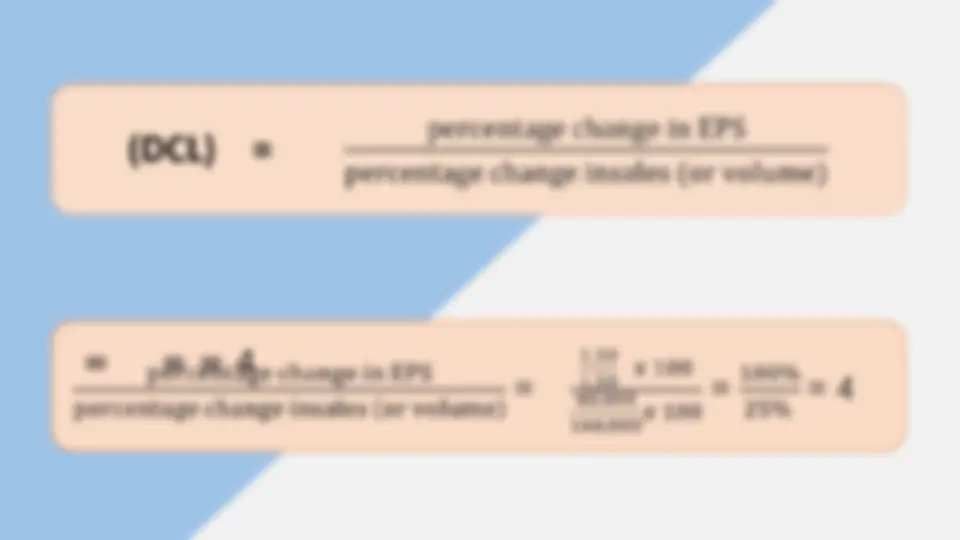

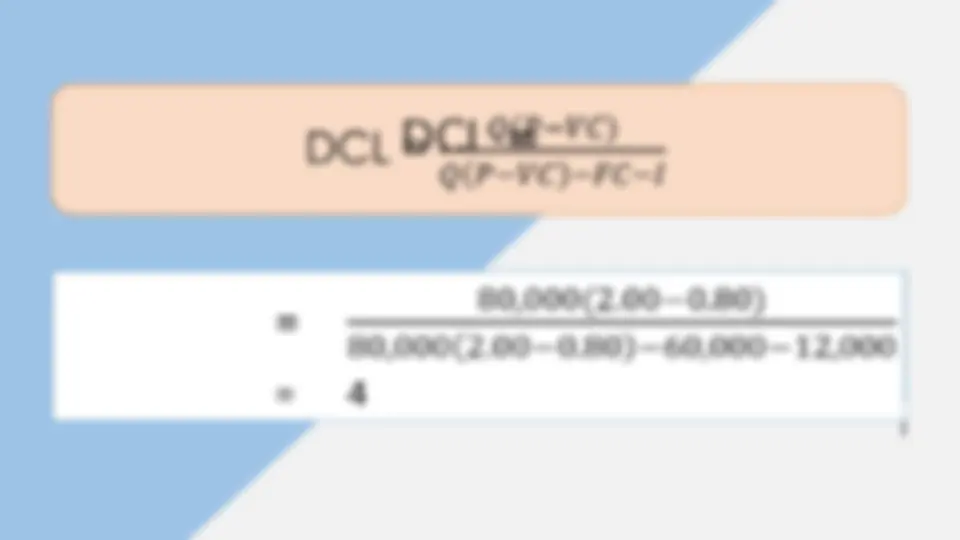

Used of fixed costs items to magnify the firm’s results. Two-edged sword – producing highly favorable results when things go well, and quite the opposite under negative conditions.

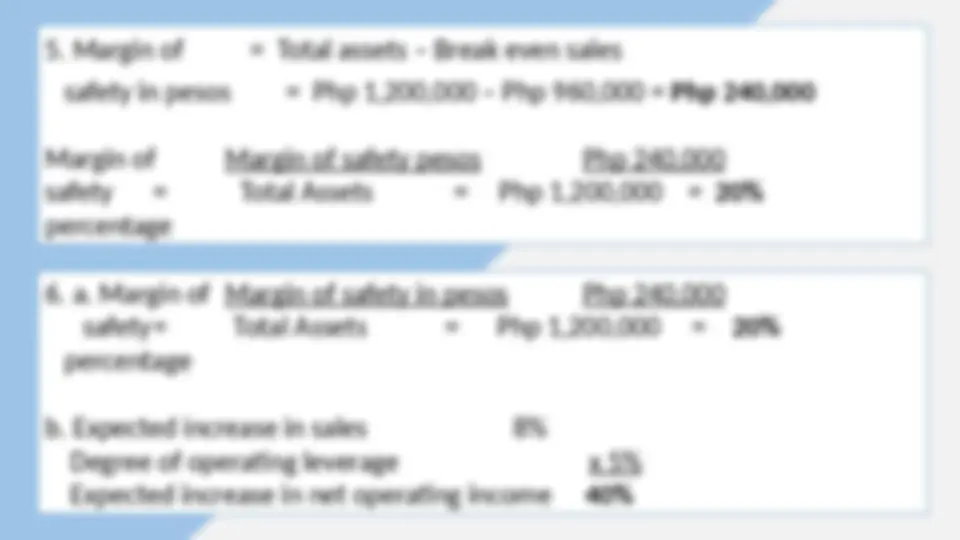

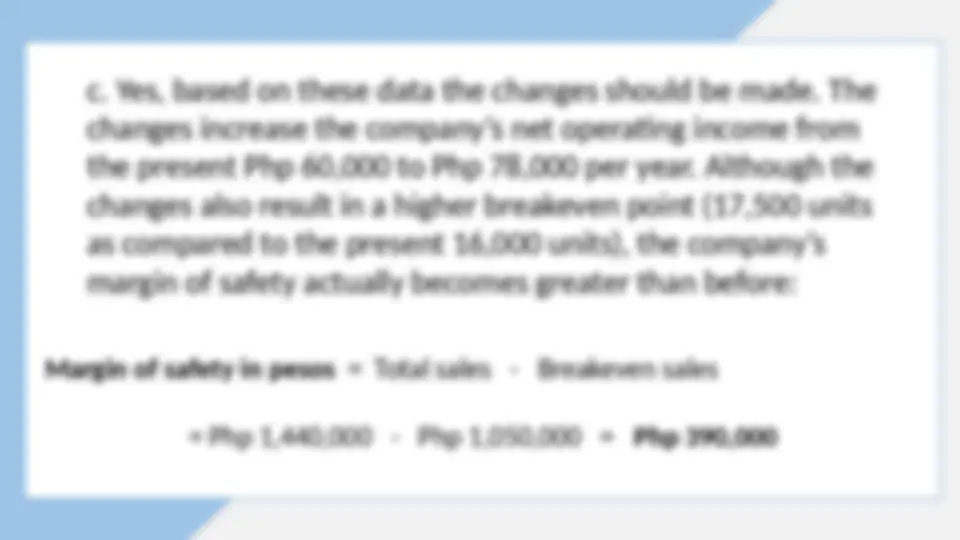

COST-VOLUME-PROFIT (CVP) ANALYSIS Powerful tool and vital in many business decisions because it helps managers understand the relationships among cost, volume and profit. Used to answer a variety of critical questions such as: What is the company’s breakeven volume? (^) What is its margin of safety? (^) What is likely to happen if specific changes are made in prices, costs and volume?

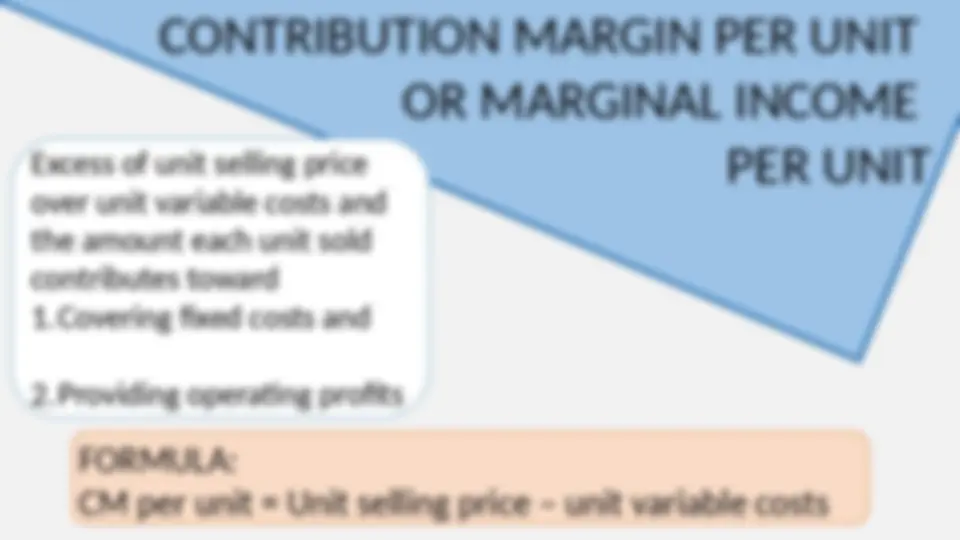

CONTRIBUTION MARGIN PER UNIT OR MARGINAL INCOME PER UNIT Excess of unit selling price over unit variable costs and the amount each unit sold contributes toward 1.Covering fixed costs and 2.Providing operating profits FORMULA: CM per unit = Unit selling price – unit variable costs

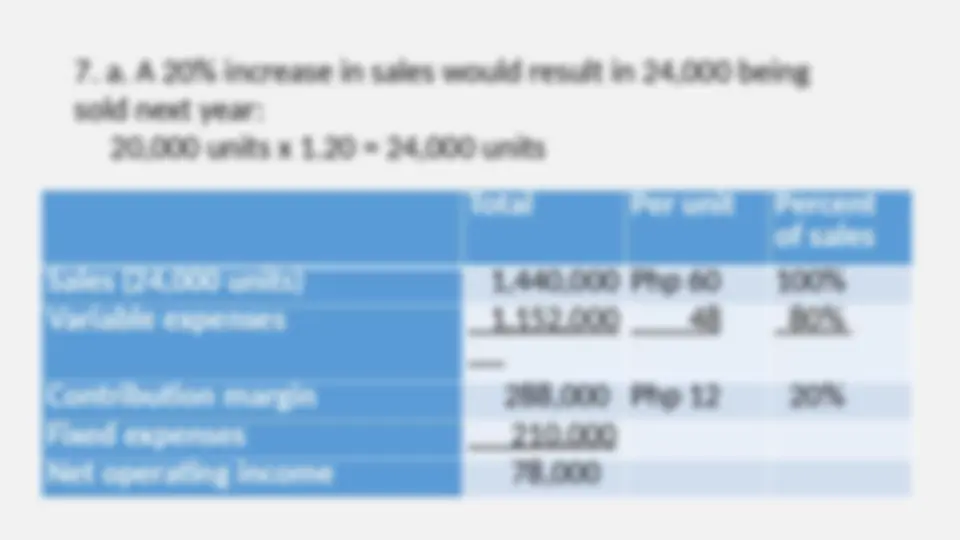

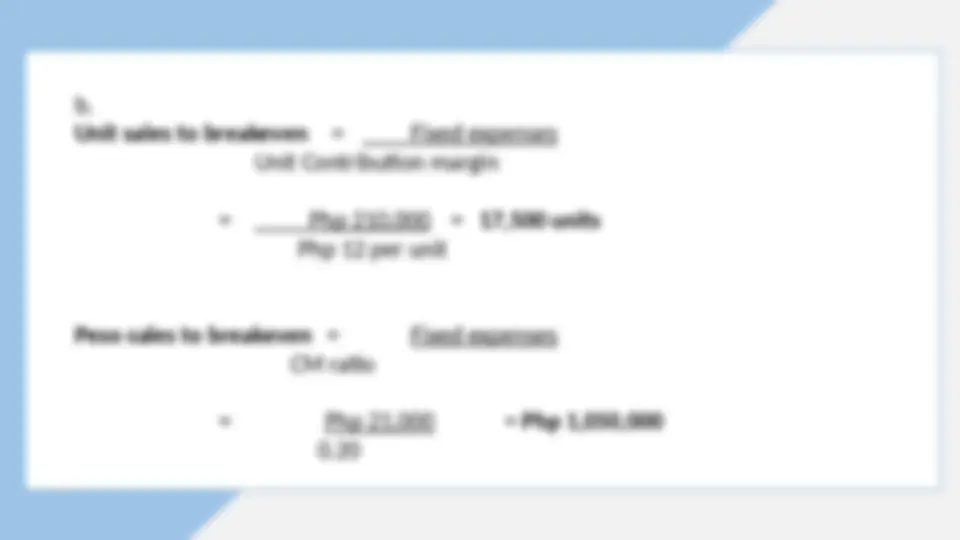

CVP ANALYSIS FOR BREAKEVEN PLANNING Break-even point is the level of sales volume where total expenses are equal, that is, there is neither profit of loss.

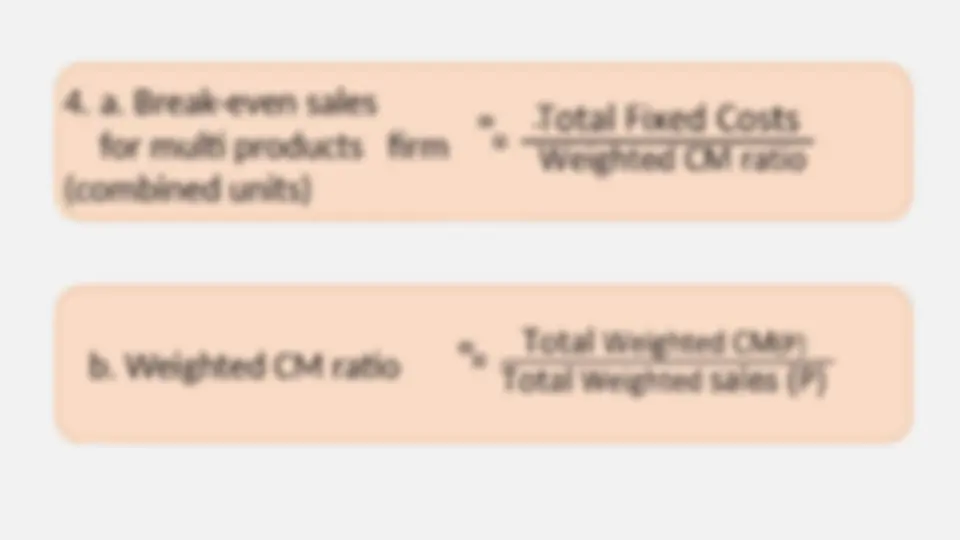

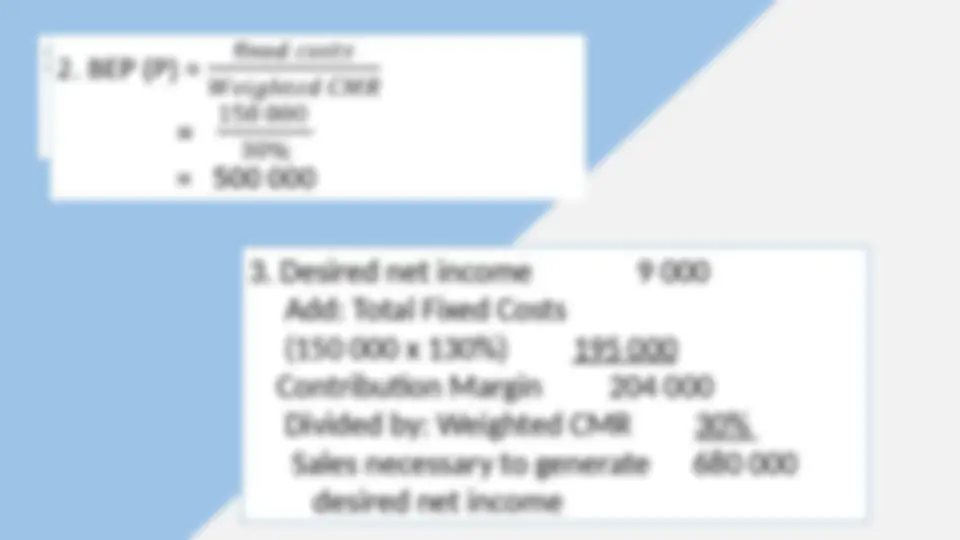

Break-even point can be computed as follows 1.Break-even point (units) =

b. Weighted CM ratio

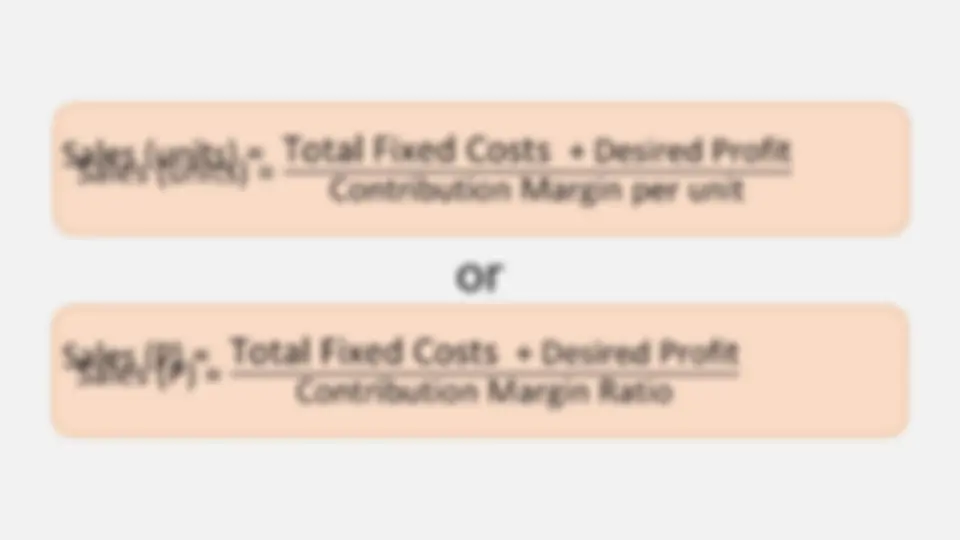

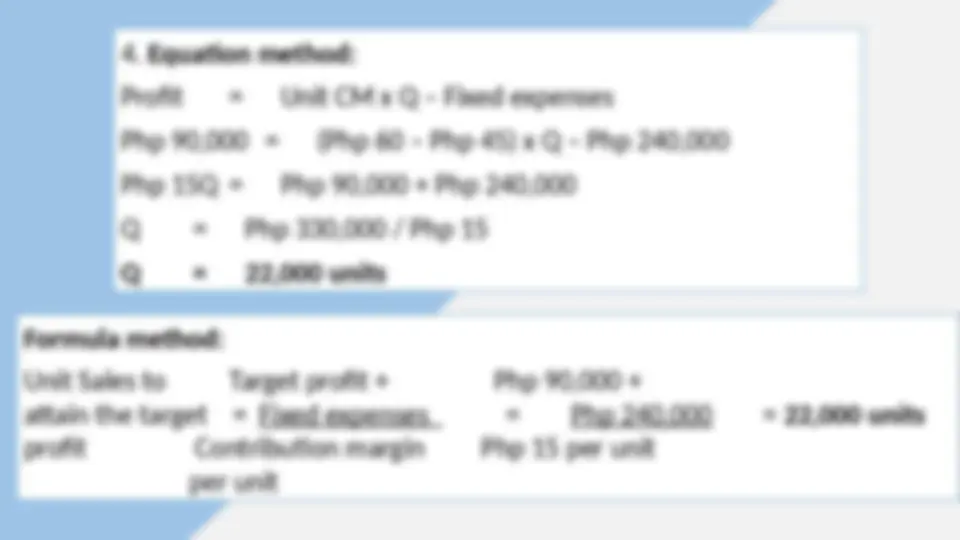

CVP ANALYSIS FOR REVENUE AND COST PLANNING CVP analysis can be used to determine the level of sales needed to achieve a desired level of profit. It assists managers in determining the revenue required to achieve a desired profit level.

SALES MIX Refers to the relative proportions in which a company’s products are sold. The idea is to achieve the combination, or mix that will yield the greatest amount of profits.

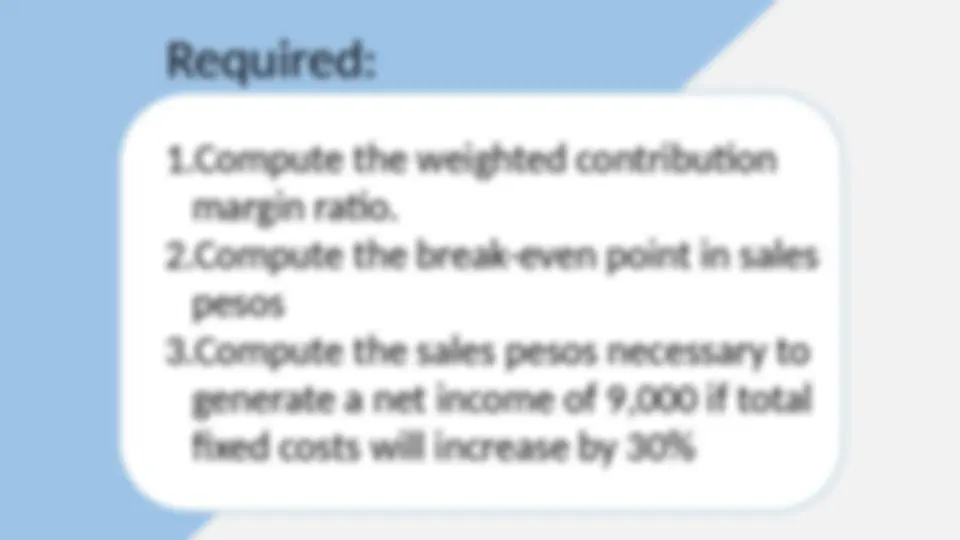

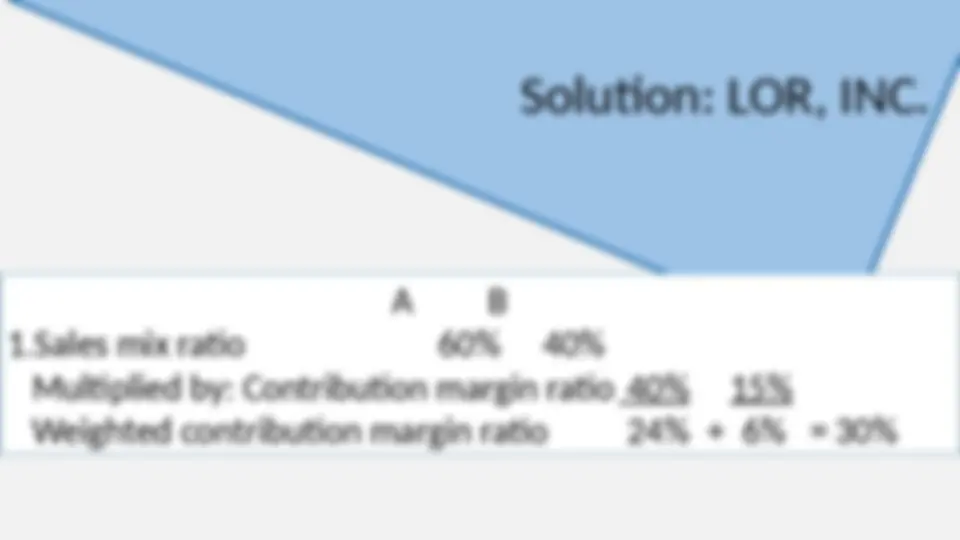

Let’s Try! CVP Analysis for a Multi- Products Firm Lor, Inc. produces only two products, A and B. These account for 60% and 40% of the total sales pesos of Lor’s respectively. Variable costs as a percentage of sales pesos are 60% for A and 85% for B. Total fixed costs are 150, 000. There are no other costs.

Solution: LOR, INC. A B 1.Sales mix ratio 60% 40% Multiplied by: Contribution margin ratio 40% 15% Weighted contribution margin ratio 24% + 6% = 30%