© University of South Wales

STRATEGIC FINANCIAL

MANAGEMENT

Portfolio Theory

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

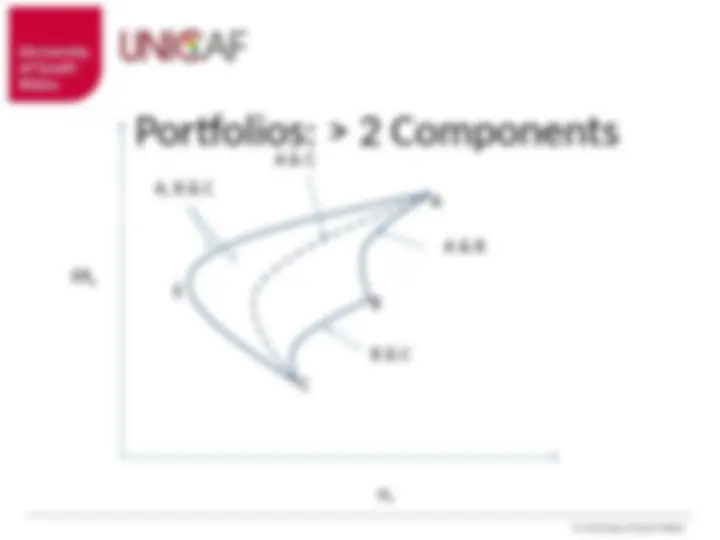

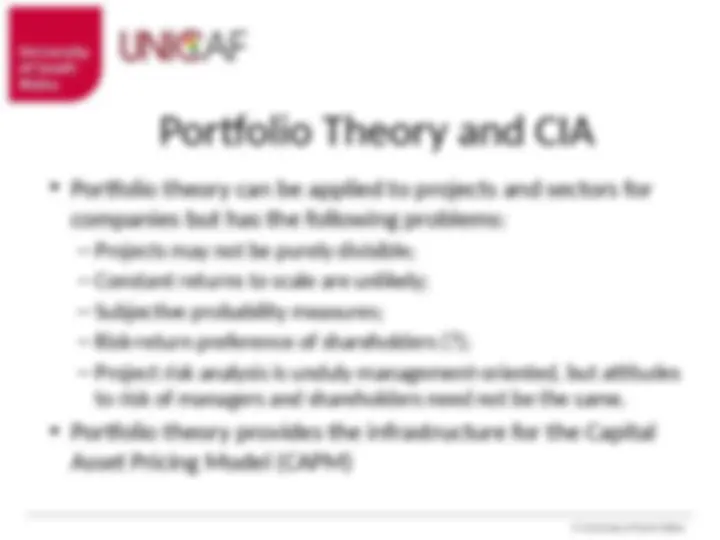

The concept of portfolio theory, emphasizing the importance of diversification in managing risk for investors and companies. It explains how to measure portfolio risk using covariance and correlation coefficients, and discusses the efficient frontier and different degrees of correlation between assets. The document also touches upon the limitations of applying portfolio theory to companies and its connection to the Capital Asset Pricing Model (CAPM).

Typology: Slides

1 / 10

This page cannot be seen from the preview

Don't miss anything!

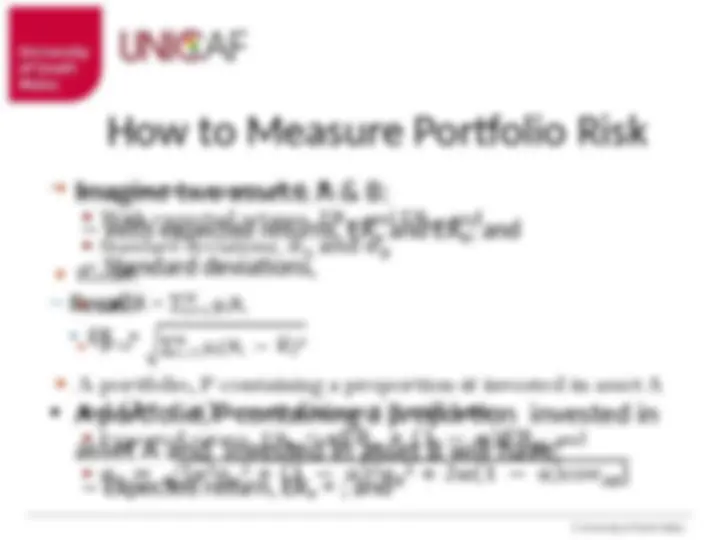

Portfolio Analysis Where Risk and Return Differ Asset Expected Return Standard Deviation Z 15% 20% Y 35% 40% rZY = -0.25 covZY = -0.25 x 20 x 40 = - Portfolio Z weighting Y weighting 100% 0% 15% 20% 75% 25% 20% 16% 50% 50% 25% 20% 25% 75% 30% 29% 0% 100% 35% 40%

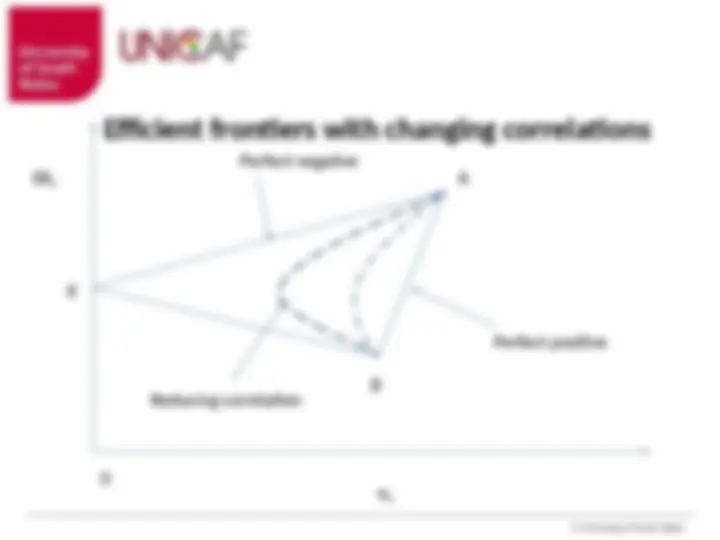

Efficient frontiers with changing correlations ERP 0 σP

Perfect positive Perfect negative Reducing correlation