Download Predicting 'Turning Points' with Leading Indicators and more Lecture notes Business in PDF only on Docsity!

Fifth Joint European Commission (EC) – OECD workshop on

business and consumer opinion surveys,

Brussels, November 17-18, 2011

Those Unpredictable Recessions…

Sergey V. Smirnov

Higher School of Economics, “Development Center‟ Institute (Moscow, Russia)

Abstract

Contemporary global economic life is measured in days and hours, but most common economic indicators have inevitable lags of months and sometimes quarters (GDP). Moreover, the real-time picture of economic dynamics may differ in some sense from the same picture in its historical perspective, because all fluctuations receive their proper weights only in the context of the whole. Therefore, it’s important to understand whether the existing indicators are really capable of providing important information for decision-makers. In other words, could they be useful in real-time? Why then was it so difficult for the experts to recognize the turning points in real time? What hampers this ability to recognize? Can a turning points’ forecast be entirely objective? The paper answers these questions in terms of three cyclical indicators for the USA (LEI by the Conference Board, CLI by OECD and PMI by ISM) during the last 2008-2009 recession.

Key Words: Business cycle, leading indicators, turning points, biased forecasts

JEL Classification: E32 - Business Fluctuations; Cycles

1. Introduction. A fact and its interpretation

Attempts to predict a recession using various “formal” methods has become commonplace since the Great Depression of 1930s and quite a lot of effort was spent to achieve this goal. But rarely have they been very successful. Various samples of real-time forecasts created by professional forecasters, who use a wide spectrum of methods and all available information, have shown that most experts are too lagging not only in predicting but even in their recognition of recessions (e.g. see [Fels and Hinshaw, 1968], [Steckler, 1968], [McNees, 1987], [McNees, 1992]).

The leading cyclical indicators approach, which became very popular after [Burns and Mitchel, 1946], has also not been able to solve the problem. These indicators usually give a good picture if one looks for a long historical retrospective but they are often not very effective in ‘real-time’, when one deals with observations that are recent. This problem is well known; it was dealt with from time to time by various authors (e.g.: [Alexander, 1958], [Stekler and Schepsman, 1973], [Hymans, 1973], [Zarnowitz and Moore, 1982], [Diebold and Rudebush, 1991], [Koenig and Emery, 1991], [Boldin, 1994], [Koenig and Emery, 1994], [Lahiri and Wang, 1994], [Filardo, 1999], [Diebold and Rudebush, 2001], [Camacho and Perez, 2002], [Filardo, 2004], [McGuckin and Ozyildirim, 2004], [Chauvet and Piger, 2008], [Leamer, 2008], [Nilsson and Guidetti, 2008], [Paap et al, 2009], [Hamilton, 2011] and others).^1

This paper will try to examine the behavior of three popular cyclical indicators for the USA during the recession of 2008-2009. These indicators are: the Leading Economic Indicator (LEI) by The Conference Board; the Composite Leading Index (CLI) by the OECD (in its ‘amplitude adjusted’ form); and Purchasing Managers’ Index (PMI) by the Institute for Supply Management. We shall consider not only their dynamics but also the conclusions made by their producers. On this ground we shall try to answer several interrelated questions. First, did the leading indicators really give signs of the beginning and the end of the 2008-2009 recession in advance? Second, did the experts make correct and timely conclusions concerning the approach of the turning points? Since our answer to the first question is ‘yes’ and ‘no’ to the second, we shall also discuss the reasons why the experts could hardly recognize the turning points (especially the cyclical peak) in real time.

In Section 2 we discuss the methodological approaches for detecting turning points in real time. Then, we take a look at whether the cyclical indicators gave signals in advance during the last recession of 2008-2009 (Section 3). In Section 4, we ascertain a gap between indicators’ signals and experts’ diagnosis (especially in their recognition of the recessions) and discuss the reasons for it. In the final Section we present our conclusions.

2. Data and methods

Peaks and troughs

(^1) The most common conclusion to these papers is that the final version of cyclical indicators draws a favorable

picture and hence one may be misled if he puts himself in the hands of the revised historical time-series. On the other side [Hymans, 1973], [Boldin, 1994], [Lahiri and Wang, 1994], [McGuckin and Ozyildirim, 2004] pointed that real-time data are also useful (as a rule they mentioned historical versions of the modern LEI by The Conference Board).

The total number of combinations of six binary values is C(6,2) = 2^6 = 64. As there are six combinations with five identical directions and one “other” and only one combination with all six identical directions we may conclude that the probability of ‘five (minimum) out of six’ sequence of symmetrically distributed random variable is equal to 7/64 = 11%.

In more formal terms, we may say that in testing a null-hypotheses of no change in trajectory (with an alternative hypothesis of negative/positive tendency) by our “five out of six” rule we have a probability of Type I error (erroneous rejection of null hypothesis or a false turning point) equal to 11%. It’s only slightly more than the usual threshold in statistical check of hypothesis.

We assume that an indicator with ‘high’ absolute score on the eve of a turning point had some anticipatory trend in proper direction and since it was possibly useful for predictions in real time. On the contrary, an indicator with ‘low’ score showed only chaotic oscillations and hence was rather useless for predicting a turning point.

3. Did the leading indicators give signals in real time?

Predicting the ‘peak’ of December 2007

‘Real-time’ picture for all three selected indicators on the eve of the recession is shown on charts in Appendix and most general notes are summarized in Table 1. The preliminary conclusions are quite obvious. The most well known coincident (not leading!) indicator based on business surveys’ (PMI by ISM) gave the most drastic signal for the economical drop in real time. Two composite leading indexes (by The Conference Board and by OECD) also gave strong reasons for anticipations of decline.

Predicting the ‘trough’ of June 2009

In July 2009 the PMI by ISM also gave (see Table 1 and charts in Appendix) the most prominent signals for the end of the recession. On the other hand, its signal was not indisputable: the PMI was still below ‘critical’ 50% level (in fact it was even below 45% level).Two composite leading indexes (by The Conference Board and by OECD) began to grow as of April 2009 and hence before the trough of the crisis. One may decide for himself whether a strong growth of the leading indicators during three consecutive months was really enough to believe the Great Recession was at its end.

Table 1

‘Net’ Score of Ups and Downs (a 6 months span)

Indicator Date of release

R-T/R*

Initial Index

Y-o-Y change Anamnesis On the Threshold of the Peak of December 2007

LEI by TCB 18.01.08 - 2/- 4 - 4/- 4

The real-time net score for the initial LEI is not too impressive; for the Y-o-Y % changes it is more significant. The LEI dropped below the ‘support level’ of the two-years flat trend in November- December of 2007.

CLI by OECD 11.01.08 - 4/- 4 - 4/- 2

The real-time net score for the CLI (as well as for its Y-o-Y % changes) is quite high (note that the net score for the revised % changes is lower). The

negative trend for the indicator and its % changes is obvious in spite of the fact that only November figure (not December figure as in almost all other cases) is available at the moment.

PMI by ISM 02.01.08 -6/-2 0/

In real time it gave a serious signal for the beginning of the 2008 recession: the net score for the index in December 2007 was equal to -6 (the possible minimum) and its level was the least since 2003. On the Threshold of the Peak of June 2009

LEI by TCB 20.07.09 0/0 +2/+

The real-time net score for the initial LEI and for the Y-o-Y % changes is not significant for a 6 month span. But the LEI rose during all the last three months since April 2009.

CLI by OECD 10.07.09 -2/0 0/

The real-time net score for the CLI as well as for its Y-o-Y % changes is quite low. Since only May figure was available at the moment one had only two months of growth since April 2009.

PMI by ISM 01.07.09 +6/+6 +6/+

In real time it gave a serious signal for the end of the 2008 recession: net score for the index in July 2009 was equal to +6 (the possible maximum). At the same time its level was still below 50 points. Notes: * - R-T – real time (January 2008 or July 2009); R – revision of January 2011. A negative net score means that the number of downs (during a 6-months span before a turning point) is greater than the number of ups; for a positive score the opposite is the case.

What did the experts write on the thresholds of turning points?

If one looks at the past from the present moment he may conclude that all three (LEI, CLI, and PMI) cyclical indicators really gave some important signals about the approaching turning points during the 2008-2009 recession though these signals were, for the most part, not entirely definite in real time. Moreover, for the trough at June 2009, they were less expressive than for the peak at December 2007. In any case, since the indexes didn’t give an obvious signal, some final ‘diagnosis’ by an expert who could weight all ‘pros’ and ‘cons’ and propose his personal conclusion were obviously needed. But if one remembered what the experts told us in real time, one would probably be surprised by a high degree of experts’ optimism.^3 The following remark by Victor Zarnowitz - a famous guru in the field of business cycles - illustrates the point: “Some pundits mistake the fears for facts and believe the recession is already with us.” He wrote these words in late February 2008 (see: [Zarnowitz, 2008], p.2), when the recession has already begun. It’s not difficult to find much more quotations like this; this point of view was common. In particular, experts usually predicted the ‘slowing of growth’ just before the drop of the economy (see Table 2).^4

(^3) *Fels and Hinshaw, 1968+ wrote about the 1957 peak: “Many were noncommittal, others optimistic” (p. 30).

[Fintzen and Stekler, 1999] have studied similar issues based on polls of professional forecasters near the beginning of 1990 recession. Not much has changed since then.

(^4) See [Smirnov, 2011] for more details about many other cyclical indicators.

PMI by ISM

02.01.08 “A PMI in excess of 41.9 percent, over a period of time, generally indicates an expansion of the overall economy. Therefore, the PMI indicates that the overall economy is growing [in December 2007] while the manufacturing sector is contracting.”

The conclusion about the growth of the overall economy was held by ISM for ten months up to November 3, 2008 (a month and a half after the Lehman Brothers bankruptcy!). At that moment, ISM mentioned a recession for the first time: “…*T+he PMI *for October 2008+ indicates contraction in both the overall economy and the manufacturing sector.” NBER announced the December 2007 peak only one month later. The trough of June 2009 LEI by TCB

20.07.09 “The recession will continue to ease; and the economy may begin to recover.”

The three months before (in April) The Conference Board predicted: “the contraction in activity could become less severe”; in July they mentioned the possibility of a recovery for the first time; in August they stated that the recession was bottoming out. Thereby, the predictions of the trough by TCB were more or less timely but they were hardly “leading”, and were rather “coincidental”. CLI by OECD

10.07.09 “Possible trough” The sequence of OECD’s growth cycle outlooks was the following: “slowdown” (June 8)/ “Possible trough” (July 10)/ “*Definite+ trough” (August 7). The outlook is quite good except for the fact that OECD presumes a six month lag between CLI and economic activity and this time we could observe a lag around zero. PMI by ISM

01.07.09 “A PMI in excess of 41.2 percent, over a period of time, generally indicates an expansion of the overall economy. Therefore, the PMI indicates growth for the second consecutive month in the overall economy, and continuing contraction in the manufacturing sector.“

The diagnosis for the trough in the overall economy seems almost perfect. Of course it depends decisively on the critical level of 41.2. In real time, one had to decide whether to trust the ‘rule of thumb’ which had shown itself as not very effective on the eve of the recession. One may also notice that the critical level was slightly revised from 41.9 since December 2007; but this is barely important.

4. Why do experts recognize cyclical peaks in real time so rarely?

In fact, we have an even more complex ‘three-compound’ paradox:

- leading indicators lead peaks more than troughs;^6

(^6) For a long time it’s been a well-known fact (see for example [Alexander, 1958]). Forty four years ago [Shiskin,

1967+ wrote: “Long leads at peaks and short leads at troughs have indeed been a characteristic of the behavior of the leading indicators during the four business cycles since 1948” (p. 45). He supposed a special “reverse-trend

- peaks are announced by NBER with less lags than troughs;^7

- in spite of this, peaks are recognized by private experts worse than troughs.

The first and the second propositions are obvious from Table 3; and the third proposition is followed from the discussion in the previous Section. How all these contradictions could be resolved? Why do experts recognize cyclical peaks in real time so rarely?

Table 3

Leads and Lags at Peaks and Troughs (the five US recessions since 1980)

Turning points (dated by NBER)

Leads (-) and Lags (+) of Cyclical Indicators, months NBER's decision LEI turning points CLI turning points PMI turning points Peaks Troughs Peaks Troughs Peaks Troughs Peaks Troughs Peaks Troughs Jan. 80 Jul. 80 5 12 -15 -2 -18 -3 -18 - Jul. 81 Nov. 82 6 8 -8 -10 -8 -6 -8 - Jul. 90 Mar. 91 9 21 -18 -2 -36 -3 -31 - Mar. 01 Nov. 01 8 20 -11 -2 -14 -2 -16 - Dec. 07 Jun. 09 12 15 -5 -3 -6 -4 -43 - Average 8.0 15.2 -11.4 -3.8 -16.4 -3.6 -23.2 -3.

The reasons which have been given for this phenomenon in other papers are as follows:

(1) the transition from expansion to contraction is not often sharp or distinct ([Koening and Emery, 1994+); “We cannot get away from the fact that while peaks are always led by slowdowns, slowdowns do not always lead to a business-cycle peak” (*Alexander, 1958+, p.301);

(2) timely preventive measures may preserve the economy from sliding into recession ([Stekler, 1972], [Anas and Ferrara, 2004]);

(3) “…R+ecessions are hard to predict, in part because they are a result of shocks that are themselves unpredictable “ (Loungani and Trehan, 2002+, p.3); in other words experts have extremely weak expectations prior to a forthcoming slump.

We may also assume the NBER’s unwillingness to “create” a situation of a double dip recession (in 1980- 1981 they announced the trough of July 1980 in July 1981 and this was just a month of a new peak). According to the NBER’s rules, the length of any cyclical phase (contraction as well as expansion) should be no less than 6 months but the length of a whole cycle should be no less than 15 months. Hence, NBER have to wait for at least 6 months to announce a turning point but if the preceding phase was too short they have to wait more. Usually a contraction is the shortest phase, so the lag before trough’s announcement turns out to be longer.

adjustment” to eliminate this asymmetry. This adjustment was incorporated into the methodology of the LEI for years. We ought better to recognize this phenomenon not only as a statistical distortion but a real economical fact. [Harris and Jamroz, 1976], [Paap et al, 2009], [Zarnowitz, 2008], [Tanchua, 2010] confirmed that leading indicators lead peaks more than troughs. See also [Zarnowitz and Moore, 1982], [Emery and Koening, 1992].

(^7) [Novak, 2008] noted that it takes longer for NBER to announce troughs than to announce peaks.

We believe the idea of different losses for different errors (Type I and Type II) for different experts (and

- separately – decision makers from government or business!) and at different phases of the business cycle is the key to the riddle.^10 The weights in the loss function may vary across forecasters because of different factors. For example, the biased forecasts may be quite rational if experts do note only seek accuracy of their estimates (see [Laster et al, 1997], [Stark, 1997], [Lamont, 2002]). The existence of ‘pessimists’ and ‘optimists’ among forecasters is also well established.^11 The idea of using decision-based methods in evaluation of forecasts (see, for example, [Granger and Machina, 2006], [Pesaran and Skouras, 2008]]) also seems fruitful.

To examine all these issues more carefully let’s denote the utility of predicting a recession by an i -expert as URi which takes its values according to Table 5.

Table 5 Utilities Under Each Forecasting Decision and State of Economy

Actual State of Economy Forecasting Decision* Recession No recession Common view: Yes i- expert’s forecast: Yes YRi (Yi| Yc) NRi (Yi|Yc) i - expert’s forecast: No YRi (Ni|Yc) NRi (Ni|Yc) Common view: No i - expert’s forecast: Yes YRi (Yi|Nc) NRi (Yi|Nc) i - expert’s forecast: No YRi (Ni|Nc) NRi (Ni|Nc) Note: * - “Yes” means that according to the forecast there will be a recession; “no” means that there will be no recession.

For example,

URi = YRi (Yi|Yc)

is the utility of the truth forecasting of a recession for an i - expert while “common view” also predicts this recession.

So, our first proposition is that the utilities for being right depend upon “common view” (terms Yc or Nc in all equations). It’s not the same thing to be right while almost everyone else is wrong and to be right while the others are also right. The first is obviously better:

YRi (Yi|Nc) >> YRi (Yi|Yc) and NRi (Ni|Yc) >> NRi (Ni|Nc)

Similarly, to be wrong while almost all others are right is much worse than to be wrong while others are wrong too (we suppose that the utilities of mistaken forecasts are all negative):

(^10) [Okun, 1960], [Lahiri and Wang, 1994], [Schnader and Stekler, 1998], [Fintzen and Stekler, 1999], [Filardo, 1999],

[Chin et al, 2000], [Dueker, 2002], [Anas and Ferrara, 2004], [Galvao, 2006] wrote on these issues but their results are still underestimated and scarcely explored in the context of business cycles indicators.

(^11) [McNees, 1992 ] noted that one of only two persons (out of forty forecasters!) who correctly predicted the

recession in July 1990 had given the same forecast since 1987 (see p.19). Indeed, if you forecast some person to die, your forecast will come true somewhere along in the future.

YRi (Ni|Yc) << YRi (Ni|Nc) and NRi (Yi|Nc) << NRi (Yi|Yc).

Our second proposition is that the utilities of being right and being wrong – if in accord with all others - are almost the same, because all of them are near zero (of course, the first is slightly positive and the second is slightly negative):

YRi (Yi|Yc) ≈ 0; YRi (Ni|Nc) ≈ 0; NRi (Ni|Nc) ≈ 0; and NRi (Yi|Yc) ≈ 0.

Our third proposition is very simple: utilities for various i and j may be quite different. For risk aversion forecasters there would be a tendency to some average (consensus) level; on the contrary, for forecasters with high risk appetite there would be a tendency for extremes. But, as it is well known, the majority prefers not to lose something rather than to gain the same additional thing.^12 Since the ordinary state of economy is growth (not decline) the ‘no recession’ forecast would prevail.^13 In other words, an expert loses almost nothing if he is a ‘no recession’ forecaster:

YRi (Ni|Yc) > NRi (Yi|Nc).

But of course, he doesn’t gain anything “special” this way either; he will never be a star. If somebody has such an ambition, he has to forecast recessions more often. For him the utility of his “personal” Type I error (false signal) is more than a utility of his “personal” Type II error (missed signal):

NRi (Yi|Nc) > YRi (Ni|Yc). 14

This is because he hopes that NRi (Yi|Nc) will at some point transmute into YRi (Yi|Nc) with its great award.

Note, that in practice one may make the name only by forecasting recessions, not expansions. Using the notifications from Table 5 but substituting E (expansion) instead of R (recession) we may write:

YRi (Yi|Nc) >> YEi (Yi|Nc).

The first reason for this asymmetry is a short duration of a typical recession. According to NBER the average period of expansion was more than five times longer than the average period of contraction ( months compared with 11 months for 11 cycles after 1945). This means that experts usually predict a trough shortly after the beginning of a recession and their error is not large in this case. Hence, there is little chance to be distinguished against such background.

But we believe that the second reason also exists, and this reason is a “wishful bias”. It is not an absolutely new issue. In March 2001 [The Economist, 2001] asked a tricky question: “Are the economic forecasters wishful thinkers or wimps?” In more scientific context [Ito, 1990] revealed that the

(^12) “…*P+eople typically reject gambles that offer a 50/50 chance of gaining or losing money, unless the amount that

could be gained is at least twice the amount that could be lost (e.g., a 50/50 chance to either gain $100 or lose $50).” (see *Tom et al, 2007+, p. 515.

(^13) As [Leonhardt, 2002] noted: ”Economists know that optimism is usually the best bet because the economy

grows more often than it shrinks.”

(^14) YRi (Ni|Nc) and NRi (Ni|Nc) are also errors of Type I and Type II respectively but we have assumed that they are

around zero because of their inconspicuousness.

recession is equal to x%, a decision-maker has to multiply this value by 1.5-2.5 and only then decide if the recession is probable.

Chart 1

“Anxious Index” According to the Survey of Professional Forecasters by FRB of Philadelphia

Note: “Anxious Index” is a probability of decline in real GDP in the following quarter (1968:Q4-2011:Q3) Source: FRB of Philadelphia.

6. Conclusions. Predicting of turning points: could and would it be fully non-subjective?

‘Historical’ and ‘real-time’ dynamics of business cycle indicators are two different things. While all producers of cyclical indicators would ever seek to improve their indicators’ ‘historical’ quality (and this is quite natural), only monitoring of a recession in a real time – as a crash test for automobiles - would reveal the proper worth of different indicators. With satisfaction, we may state that during the 2008- 2009 recession, all three cyclical indicators could be really useful in foreseeing turning points in real time: they (or their growth rates) have really changed their trajectories in the opposite direction some months before a turning point. These changes could be effectively caught by “five (minimum) out of six” rule of thumb. The LEI by the Conference Board, the CLIs by OECD, and the PMI by ISM could be quite informative at the threshold of the peak as well as at the threshold of the trough.^17

(^17) Our analysis tells us that the trust for the critical 50% level of PMI as an adequate indicator for an increase or

decrease of manufacturing sector (or 42.5% for the USA economy as a whole) is unwarranted. The 2008- 2010 history showed that the existence of a definite and prolonged tendency of PMI – aside its absolute level - is an important factor per se.

The prominent alarm signal (which is not simply a change in direction but a change of a definite steadiness) from cyclical indicators was hardly leading, but rather coinciding. This is not bad, however. Geoffrey Moore in 1950 wrote, "If the user of statistical indicators could do no better than recognize contemporaneously the turns in general economic activity denoted by our reference dates, he would have a better record than most of his fellows."^18 Our results confirm that in real time, an alarm signal which is synchronized with an approaching recession is the ‘maximum’ which one could hope for. On the other hand, it means that not only leading but also coincident cyclical indicators may be suitable for turning points detection in real time.

One of the main reasons for experts’ delays in peaks recognition is their psychological “dependence” on GDP statistical news-releases. Almost nobody among experts believe in Okun’s rule of two quarters of decline in real GDP in theory but many of them adapt their diagnosis for this rule in practice. But GDP has quarterly (not monthly) frequency and long publications lags! Hence, any business or political decision based on GDP would rather be delayed. Even if the 2Q rule would be ideal in historical retrospective it is far from ideal in real time.

In any case, between the moment of ‘technical’ calculation (and publication) of a cyclical indicator and the moment of an expert’s diagnosis of a turning point (especially of a peak) some gap will always exist. Interestingly, not only in historical perspective but also in real-time, leads before peaks are usually longer than leads before troughs but the recognition of peaks is obviously more difficult and a more time consuming process than recognition of troughs. A hypothesis of a ‘wishful bias’ crosses one’s mind as an explanation for this phenomenon: most of private experts don’t want to become a messenger of bad news. On the other hand, lags for the NBER’s announcements are larger for troughs, not for peaks: in the NBER’s loss-function the weight of an improper dating of a trough is obviously more than that of a peak. It’s evident from all this that the forecasting of turning points is dependent not only on ‘objective’ data and methods but rather on ‘subjective’ conclusions of experts and/or decision makers with their own internal loss-functions. As *Berge and Jordà, 2011+ wrote: “Agents facing different preferences and constraints will make different decisions from the same reading of an index”.^19

Evidently, some “wishful bias” in forecasted probabilities of a recession exists. On the average it is equal to 1.5-2.5: if the “anxious index” for the SPF by FRB of Philadelphia is equal to 20% one may understand that the real probability is around 50%; if the “anxious index” is greater than 50% in reality the probability of recession is 75% and even more. Of course, this is true “on average”. Some individual forecasters are more accurate, others are less. In any case we may ask a question: what is the nature of turning points forecasting? One may say it’s a product of art *Jordà, 2010++, others may seek for formal procedures ([Leamer, 2008] and many others). We believe even the best formal procedures are only instruments for experts with all their experiences and intuitions.

(^18) See [Fels and Hinshaw, 1968], p.47. This unpretentious aim was approved by many scholars of authority (e.g.:

[Moore, 1961], [Fels and Hinshaw, 1968], [Greenspan, 1973], [Chaffin and Talley, 1989], [Koenig and Emery, 1991], [Koening and Emery, 1994], [Lahiri and Wang, 1994], [Layton, 1997], [Fintzen and Stekler, 1999], [Layton and Katsuura, 2001+, *Peláez, 2005+, *Hamilton, 2010+).

(^19) See p.275.

Filardo, Andrew (2004). The 2001 US Recession: What Did Recession Prediction Models Tell Us? // Bank for International Settlements, Working Paper No 148.

Fintzen, David and H.O. Stekler (1999). Why Did Forecasters Fail to Predict the 1990 Recession? // International Journal of Forecasting. Vol. 15 pp. 309– 323

Galvão, Ana Beatriz C. (2006). Structural Break Threshold VARs for Predicting US Recessions Using the Spread // Journal of Applied Econometrics. Vol. 21, p. 463–487 (2006)

Hamilton, James D. (2011). Calling Recessions in Real Time // International Journal of Forecasting. Vol. 27, p. 1006-1026.

Harris, Maury N. and Deborah Jamroz (1976). Evaluating the Leading Indicators // Federal Reserve Bank Of New York. Monthly Review, June 1976, pp. 165-171.

Hymans, Saul H. (1973). On the Use of Leading Indicators to Predict Cyclical Turning Points // Brookings Papers on Economic Activity, Vol. 1973, No. 2, pp. 339-

Granger, Clive W.J. and Mark J. Machina (2006). Forecasting and Decision Theory // In: Elliott, Graham, Clive W.J. Granger and Allan Timmermann (eds.). Handbook of Economic Forecasting, Volume 1. – Elsevier, 2006, pp.81-98.

Greenspan, Alan (1973). A Comment on Saul H. Hymanis (1973) // Brookings Papers on Economic Activity, Vol. 1973, No. 2, pp. 376-378.

Ito, Takatoshi (1990). Foreign Exchange Rate Expectations: Micro Survey Data. // American Economic Review. June 1990. P. 434-449.

Jordà, Òscar (2010). Diagnosing Recessions // FRBSF Economic Letter. 2010 no 5 (February 16, 2010)

Koenig, Evan F. and Kenneth M. Emery (1991). Misleading Indicators? Using the Composite Leading Indicators to Predict Cyclical Turning Points // Federal Reserve Bank of Dallas. Economic Review. July

- P. 1-

Koenig, Evan F. and Kenneth M. Emery (1994). Why the Composite Index of Leading Indicators Does not Lead // Contemporary Economic Policy; Jan 1994; Vol 12 no 1; p. 52-

Lahiri, K. and J. G. Wang (1994). Predicting Cyclical Turning Points with Leading Index in a Markov Switching Model // Journal of Forecasting. Vol 13 No 3, p. 245-263.

Lamont, Owen A. (2002). Macroeconomic Forecasts and Microeconomic Forecasters // Journal of Economic Behavior and Organization (2002), pp. 265–280. First published as NBER Working Paper No 5284 (October 1995).

Laster, David, Paul Bennett, and In Sun Geoum (1997). Rational Bias in Macroeconomic Forecasts. // The Quarterly Journal of Economics. Vol. 114, No. 1, Feb., 1999. P. 293-

Layton, Allan P. (1997). Do Leading Indicators Really Predict Australian Business Cycle Turning Points? // The Economic Record. Vol. 73. No 222 (September 1997), p. 258-269.

Layton, Allan P. and Masaki Katsuura (2001). Comparison of Regime Switching, Probit and Logit Models in Dating and Forecasting US Business Cycles // International Journal of Forecasting 17 (2001) 403– 417

Leamer, Edward E. (2008). What's a Recession, Anyway?// NBER Working Paper No 14221.

Leonhardt, David (2002). Forecast Too Sunny? Try the Anxious Index //The New York Times. September 1, 2002.

Loungani, Prakash and Bharat Trehan (2002). Predicting When the Economy Will Turn // FRBSF Economic Letter. Number 2002-07, March 15, 2002, pp. 1-

McGuckin, Robert H. and Ataman Ozyildirim (2004). Real-Time Tests of the Leading Economic Index: Do Changes in the Index Composition Matter? // Journal of Business Cycle Measurement and Analysis. Vol. 1, No. 2. P. 171-191.

McNees, Stephen K. (1987). Forecasting Cyclical Turning Points: The Record in the Past Three Recessions // New England Economic Review. March/April 1987, p. 31-

McNees, Stephen K. (1992). The 1990-91 Recession in Historical Perspective // New England Economic Review. January/February 1992, p. 3-

Moore, Geoffrey H. (1961) Leading and Confirming Indicators of General Business Changes // In: Geoffrey H. Moore, ed. Business Cycle Indicators, Vol. 1. NBER, 1961, p.45-

Nalewaik, Jeremy J. (2010). The Income- and Expenditure-Side Estimates of US. Output Grow // Brookings Papers on Economic Activity. Spring 2010, pp.71-106.

Nilsson, Ronny and Emmanuelle Guidetti (2008). Predicting the Business Cycle: How Good are Early Estimates of OECD Composite Leading Indicators? // OECD Statistics Brief No. 14 (February 2008).

Novak, Jason (2008). Marking NBER Recessions with State Data // Federal Reserve Bank of Philadelphia. Research Rap Special Report. April 2008.

Okun, Arthur M. (1960). On the Appraisal of Cyclical Turning-Point Predictors // Journal of Business of the University of Chicago. Vol. 33 No. 2, pp. 101-20.

Paap, Richard, Rene Segers, and Dick van Dijk (2009). Do Leading Indicators Lead Peaks More Than Troughs? // Journal of Business & Economic Statistics. Vol. 27, No. 4 (October 2009), p.528-543.

Peláez, Rolando F. (2005). Dating Business-Cycle Turning Points // Journal Of Economics And Finance. Vol. 29. No. 1 Spring 2005 p. 127-

Pesaran, M. Hashem and Spyros Skouras (2008). Decision-Based Methods for Forecast Evaluation // In: Clements, Michael P. and David F. Hendy (eds.) Companion to Economic Forecasting. Wiley, 2008, pp. 241-267.

Schnader, M. H. and Stekler, H. O. (1998). Sources of Turning Point Forecast Errors // Applied Economics Letters. Vol .5 No. 8, pp. 519 — 521

Shiskin, Julius (1967). Reverse Trend Adjustment of Leading Indicators // The Review of Economics and Statistics, Vol. 49, No. 1 (Feb., 1967), pp. 45-

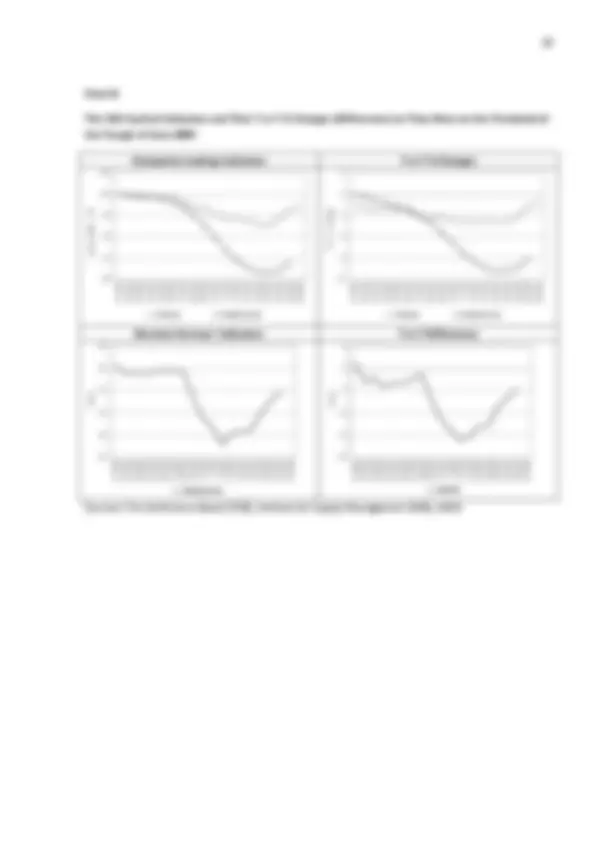

Appendix

Chart A

The USA Cyclical Indicators and Their Y-o-Y % Changes (Differences) as They Were on the Threshold of the Peak of December 2007

Composite Leading Indicators Y-o-Y % Changes

97

98

99

100

101

102

01.2006 02.2006 03.2006 04.2006 05.2006 06.2006 07.2006 08.2006 09.2006 10.2006 11.2006 12.2006 01.2007 02.2007 03.2007 04.2007 05.2007 06.2007 07.2007 08.2007 09.2007 10.2007 11.2007 12.

January 2006 = 100

TCB-LEI OECD-CLI-AA

0

1

2

3

01.2006 02.2006 03.2006 04.2006 05.2006 06.2006 07.2006 08.2006 09.2006 10.2006 11.2006 12.2006 01.2007 02.2007 03.2007 04.2007 05.2007 06.2007 07.2007 08.2007 09.2007 10.2007 11.2007 12.

Y-o

TCB-LEI OECD-CLI-AA Business Surveys’ Indicators Y-o-Y Differences

46

48

50

52

54

56

58

01.2006 02.2006 03.2006 04.2006 05.2006 06.2006 07.2006 08.2006 09.2006 10.2006 11.2006 12.2006 01.2007 02.2007 03.2007 04.2007 05.2007 06.2007 07.2007 08.2007 09.2007 10.2007 11.2007 12.

Points

ISM-PMI

0

2

4

01.2006 02.2006 03.2006 04.2006 05.2006 06.2006 07.2006 08.2006 09.2006 10.2006 11.2006 12.2006 01.2007 02.2007 03.2007 04.2007 05.2007 06.2007 07.2007 08.2007 09.2007 10.2007 11.2007 12.2007 01.

Points

ISM-PMI

Sources: The Conference Board (TCB); Institute for Supply Management (ISM); OECD.

Chart B

The USA Cyclical Indicators and Their Y-o-Y % Changes (Differences) as They Were on the Threshold of the Trough of June 2009

Composite Leading Indicators Y-o-Y % Changes

88

91

94

97

100

103

01.2008 02.2008 03.2008 04.2008 05.2008 06.2008 07.2008 08.2008 09.2008 10.2008 11.2008 12.2008 01.2009 02.2009 03.2009 04.2009 05.2009 06.

January 2008 = 100

TCB-LEI OECD-CLI-AA

0

3

01.2008 02.2008 03.2008 04.2008 05.2008 06.2008 07.2008 08.2008 09.2008 10.2008 11.2008 12.2008 01.2009 02.2009 03.2009 04.2009 05.2009 06.

Y-o

TCB-LEI OECD-CLI-AA Business Surveys’ Indicators Y-o-Y Differences

30

35

40

45

50

55

01.2008 02.2008 03.2008 04.2008 05.2008 06.2008 07.2008 08.2008 09.2008 10.2008 11.2008 12.2008 01.2009 02.2009 03.2009 04.2009 05.2009 06.2009 07.

Points

ISM-PMI (RHS)

0

5

01.2008 02.2008 03.2008 04.2008 05.2008 06.2008 07.2008 08.2008 09.2008 10.2008 11.2008 12.2008 01.2009 02.2009 03.2009 04.2009 05.2009 06.2009 07.

Points

ISM-PMI

Sources: The Conference Board (TCB); Institute for Supply Management (ISM); OECD