Forecasting Multiple Variables from

their own Histories

docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

The concept of forecasting multiple variables using vector autoregression (var) systems. It covers the equations for var systems, predictive causality between variables, higher order var systems, determining lag length, and leading indicators. The document also touches upon the use of var models for forecasting and the concept of cointegration.

Typology: Slides

1 / 26

This page cannot be seen from the preview

Don't miss anything!

Forecasting Multiple Variables from

their own Histories

Vector Autoregression (VAR) » equations for several variables where each variable depends not only on its own history, but also the history of all the other variables. » multiple variable extension of an AR model

In principle could specify multiple variable MA or multiple variable ARMA models » in practice such models are difficult to specify » typically low order VARs are adequate to approximate MA or ARMA processes

Says that information in the history of one variable can be used to improve upon the forecasts of a second variable compared to just forecasting from the history of the second variable.

Z has predictive causality for X if b 1 not equal to zero. X has predictive causality for Z if c 1 not equal to zero

Only one lag on X and Z appears in each of the above equations.

Not necessary to limit the size of the forecasting problem to only two variables

One strategy:

Generally are not going to need a lot of lags for seasonally adjusted data

For non-seasonally adjusted data, be careful about autocorrelations at seasonal frequencies

When c 1 = 0.0 then the history of the X variable does not influence the future values of the Z variable (no predictive causality of X for Z)

As long as b 1 not equal to zero, the history of Z has predictive value for future outcomes of X

Question of interest is whether all the coefficient on lagged values on one variable are zero in the regression in which some other variable is the dependent variable?

F test can be used to examine the hypothesis that multiple regression coefficients are jointly equal to zero.

Commerce (or Conference Board) Composite Leading Indicator viewed as a forecasting device for future expansions or recessions.

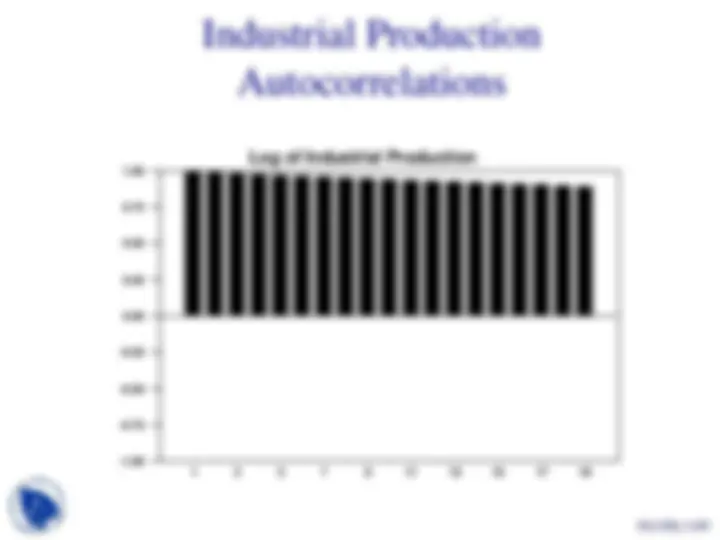

Log of Industrial Production

-1.00 1 3 5 7 9 11 13 15 17 19

-0.

-0.

-0.

0.

0.

0.

0.

1.

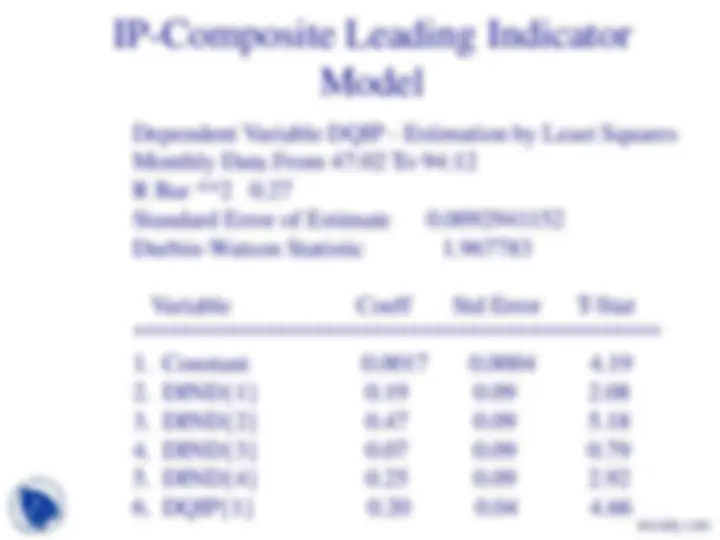

Dependent Variable DQIP - Estimation by Least Squares Monthly Data From 47:02 To 94: R Bar **2 0. Standard Error of Estimate 0. Durbin-Watson Statistic 2.

Variable Coeff Std Error T-Stat

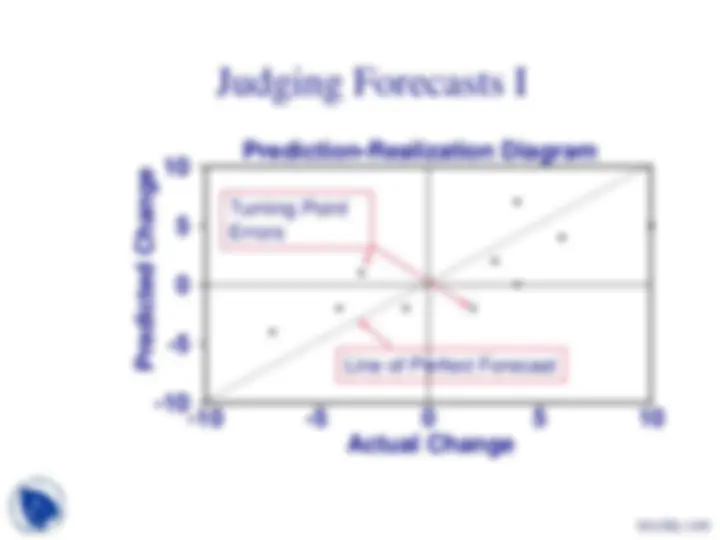

One period ahead forecasts:

Multiple period ahead forecasts:

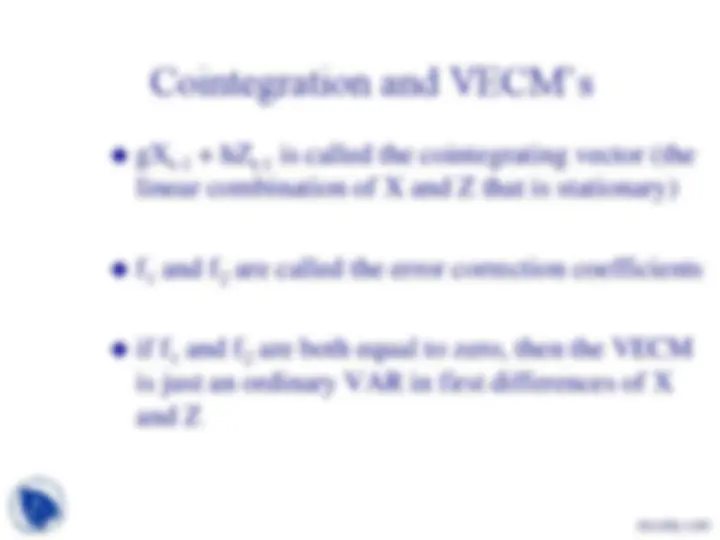

Suppose that you have several variables that are generated by unit root processes

Suppose that such variables are “tied together” - there are linear combinations of the variables that are stationary