Download Understanding Farm Financial Statements: Preparing a Balance Sheet and more Study notes Economics in PDF only on Docsity!

Farm Financial Statements

Farm financial statements allow the manager to assess the business=s

financial position and performance and chart its progress.

Farm financial statements are essential for obtaining credit and are used to

answer three critical questions:

Is the farm solvent?

- The ability of a farm business to meet its liabilities.

Is the farm profitable?

- The ability of a farm business to generate more revenues than

expenses (including opportunity cost).

Is the farm liquid?

- The ability of a farm business to generate sufficient cash to meet

its

financial obligations as they come due.

The three most basic financial statements are:

The balance sheet:

- Summarizes the asset values, the liabilities and the net worth

position of the business at a given point in time.

The income (profit and loss) statement:

- Summarizes cash receipts, expenses and inventory schedules

over a

given period of time (most generally one year).

The cash flow statement:

- Provides an overview of the business=s cash flow, including debt

payments, family living expenses, and income tax over a given

period

of time.

Preparing a Balance Sheet

The balance sheet is a snapshot of the business at a given point in time.

The balance sheet summarizes the investments that have been made in the

business (assets) and how these investments are being financed (liabilities

and net worth) as of a given point in time.

ASSETS = LIABILITIES + NET WORTH (EQUITY)

ASSETS

An asset is anything of value owned by a business or person, including

obligations by others to the individual or the business.

In a balance sheet assets are classified as to how easily they can be

converted to cash.

Current Assets are those assets that will be used up within the

next accounting year or that can be easily converted to cash

without affecting the operation of the business.

Non-Current Assets are those assets that support production,

have a life of more than one year and that are not normally sold in

the ordinary course of doing business.

Business Balance Sheet

- includes only those assets and liabilities relating to the business.

Personal Balance Sheet

- includes only those assets and liabilities relating to the family.

Consolidated Balance Sheet

- includes the assets and liabilities of both the business and the family.

The balance sheet can be prepared using either the cost or the market-value

approach.

The cost approach is based on original cost minus depreciation.

These resulting figures are termed “book values” and may not reflect

the true value of the various assets.

The market value approach is based on fair market value rather than

what was paid. These figures are termed Amarket values@ and

reflect the true value of the various assets.

Business Balance Sheet for Frank Pharmer, December 31 Assets Cost Liabilities Cost Current Assets Current Liabilities Cash 2,000 Accounts payable 1, Savings 19,000 Principal due on machine loan

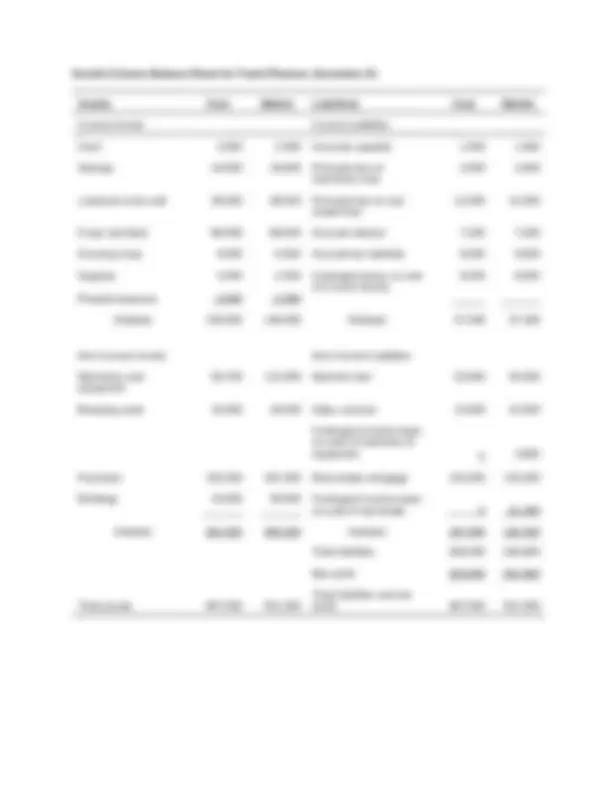

Livestock to be sold 26,000 Principal due on real estate loan

Crops and feed 68,000 Accrued interest 7, Growing crops 6,000 Accrued tax liabilities 9, Supplies Prepaid expenses

Contingent taxes on sale of Current Assets

Subtotal 126,000 Subtotal 37, Non-Current Assets Non-Current Liabilities Machinery and equipment 93,700 Machine loan 25, Breeding stock 16,000 Sales contract 10, Continent income taxes on sale of machinery & equipment

Farmland 155,300 Real estate mortgage 132, Buildings 16,

Contingent income taxes on sale of real estate 0 Subtotal 281.000 Subtotal 167, Total liabilities 204, Net worth 202, Total assets 407, Total liabilities and net worth 407,

Pr in ci p al P a y m e nt 8% interest -------------- $ 800 Interest Payment 5 year repayment $8,295 Remaining Loan Balance Annual P&I payment = $2, Since April 1, 2006, nine months of interest has accrued!! Thus: $800 x 9/12 = $600 of accrued interest as of D ec e m b er 3 1,

2 0 0 6.

EXERCISE 1 Preparing a Balance Sheet Prepare a Acost@ balance sheet as of January 1, 200X with the following information provided: Total machine loan due $ 50, Total real estate loan due 120, Accounts payable 5, Accounts receivable 6, Grain in storage 20, Land value 250, Machine loan principal due in 12 months 10, Real estate loan principal due in 12 months 10, Cash in bank 18, Accrued interest payable 9, Original machinery cost 110, Accumulated machinery depreciation and expensing option deductions 40, Original grain bin cost 20, Accumulated depreciation and expensing option deductions on grain bin 800 Organize the balance sheet under the following headings: current assets; non-current assets; total assets; current liabilities; non- current liabilities; total liabilities; net worth, and total net worth and liabilities.

Exercise 1 Preparing a Balance Sheet January 1, 200X CURRENT ASSETS CURRENT LIABILITIES Total Current Assets Total Current Liabilities NON-CURRENT ASSETS NON-CURRENT LIABILITIES Total Non-Current Assets Total Non-Current Liabilities TOTAL LIABILITIES NET WORTH TOTAL LIABILITIES TOTAL ASSETS + NET WORTH

Exercise 2 Preparing a Balance Sheet January 1, 200X CURRENT ASSETS CURRENT LIABILITIES Total Current Assets Total Current Liabilities NON-CURRENT ASSETS NON-CURRENT LIABILITIES Total Non-Current Assets Total Non-Current Liabilities TOTAL LIABILITIES NET WORTH TOTAL LIABILITIES TOTAL ASSETS + NET WORTH