INTERNAL AUDIT

PROCESS & RISK REFERENCE COMPENDIUM

Covering 8 Sectors | 15+ Process Cycles | Risks, Controls & Audit Observations

FMCG | Healthcare | Real Estate | Hospitality | Green Energy | IT/ITES | Manufacturing | Education

Prepared for Prashant Pal | CA | Internal Audit & Risk Advisory

CONTENTS

1. Common / Cross-Sector Process Cycles

2. FMCG (Fast Moving Consumer Goods)

3. Healthcare & Pharmaceuticals

4. Real Estate & Construction

5. Hospitality (Hotels & Restaurants)

6. Green / Renewable Energy Generation

7. Information Technology & ITES

8. Manufacturing & Engineering

9. Education & EdTech

HOW TO USE THIS DOCUMENT

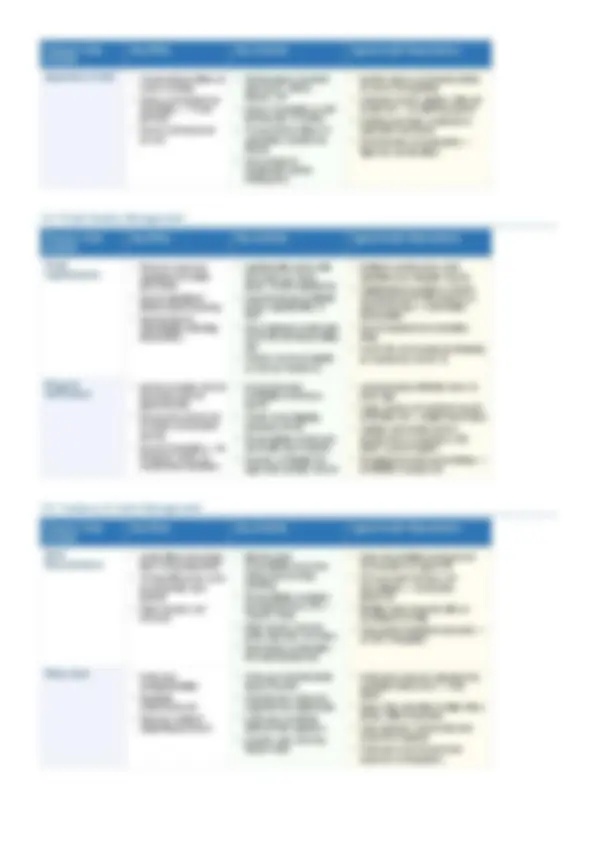

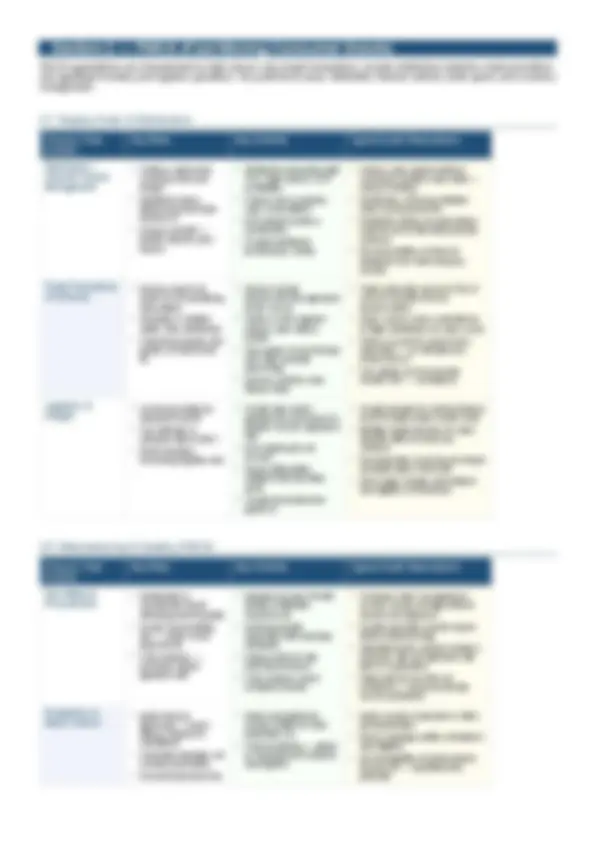

Each sector section contains a four-column matrix: Process / Sub-process → Key Risks → Key Controls → Typical Audit

Observations. This is structured to mirror a risk-and-control matrix (RCM), which is the working document used in every internal

audit and IFC engagement.

Process column: The business process or sub-process being audited (e.g. Vendor Onboarding, Revenue Recognition).

Key Risks column: The significant risks that could materialise if controls fail — financial, operational, compliance, or

reputational.

Key Controls column: The controls expected to mitigate the risks — preventive, detective, automated, or manual.

Audit Observations column: Typical findings raised in practice — what auditors commonly discover when controls are absent

or ineffective.