Muhammad Zubair Mughal

Chief Executive Officer

Alhuda centre of Islamic banking and economics

Islamic Microfinance

Product Development

& Country Experiences

Islamic Microfinance

Product Development

& Country Experiences

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

An overview of Islamic microfinance, its basic principles, sources, current status, and future potential. It covers the product development process, the role of Shariah compliance, and the involvement of various parties. The document also highlights major markets for Islamic microfinance and their institutions in Pakistan, Afghanistan, Indonesia, and Yemen.

Typology: Summaries

1 / 20

This page cannot be seen from the preview

Don't miss anything!

Chief Executive Officer Alhuda centre of Islamic banking and economics Islamic Microfinance Product Development & Country Experiences Islamic Microfinance Product Development & Country Experiences

Contents

Islam and Shariah

Sources of Islamic Finance Islamic Banking Product Mechanism

Islamic products and services offered by 2000+ Financial Institutions around the world . United States: 20 - Al Manzil Financial Services - American Finance House - Failaka Investments - HSBC - Ameen Housing Cooperative Germany: - Bank Sepah - Commerz Bank - Deutsche Bank Switzerland: 6 UK: 26 - HSBC Amanah Finance - Al Baraka International Ltd - Takafol UK Ltd - The Halal Mutual Investment Company - J Aron & Co Ltd (Goldman Sachs) Bahrain: 26 - Bahrain Islamic Bank - Al Baraka - ABC Islamic Bank - CitiIslamic Investment Bank Malaysia: 49 2 - Pure Islamic Banks (Bank Islam, Bank Muamalat) Rest - conventional banks Saudi Arabia: 37 - Al Rajhi - SAMBA - Saudi Hollandi - Riyadh Bank UAE: 58 - Dubai Islamic Bank - Abu Dhabi Islamic Bank - HSBC Amanah Qatar: 41 - Qatar Islamic Bank - Qatar International Islamic Kuwait: 9 - Kuwait Finance House Iran: 8 Egypt: 12 - Alwatany Bank of Egypt - Egyptian Saudi Finance Indonesia: 4 Sudan: 9 Pakistan: 76 India: 3 Bangladesh: Turkey: 7 - Faisal Finance Institution - Ihlas Finance House Yemen: 5

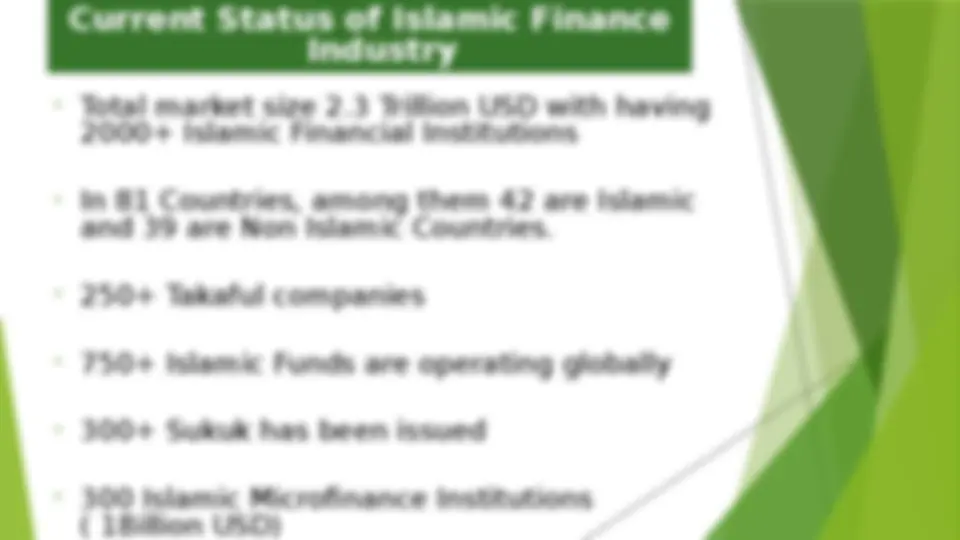

Current Status of Islamic Finance Industry

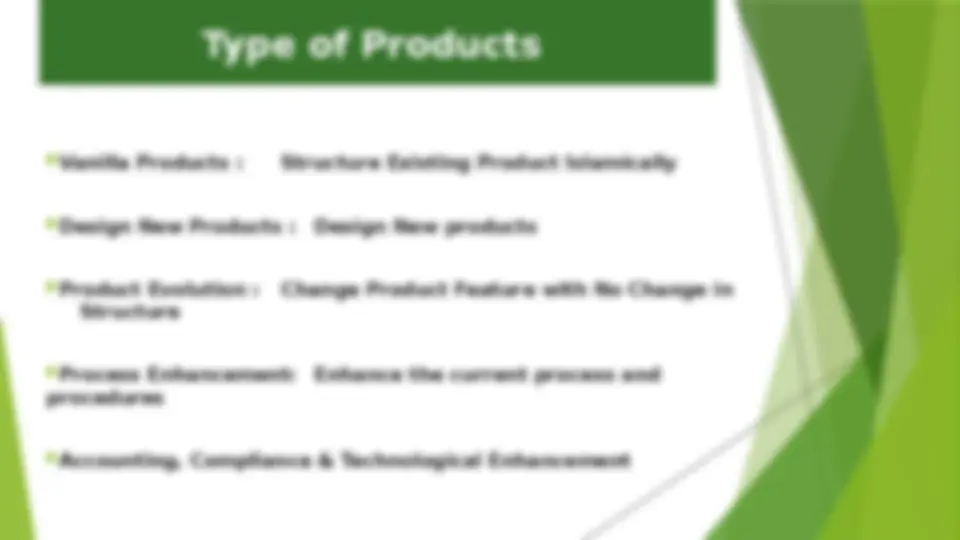

Vanilla Products : Structure Existing Product Islamically Design New Products : Design New products Product Evolution : Change Product Feature with No Change in Structure Process Enhancement: Enhance the current process and procedures Accounting, Compliance & Technological Enhancement Type of Products

BOD CEO/MD Shariah Board/Advisor Product Development Department Marketing Department Accounting & Finance I.T Department HR & Capacity Building Sales Team Role & Internal Involvement for New Product

Phase 1: Product Summery by Product Development Dept. Phase 2: Product Concept Document(PCD), Presentation and approval Phase 3: Legal and Shariah Approval Phase 4: Market Research, Survey’s FGD, SWOT Analysis, External and Internal Environmental Screening etc. Phase 5: Designing of SOP’s, Accounting, Compliance & Technological Enhancement, different forms, HR & Credit Policy Evaluation process, Compliance Mechanism etc. Phase 6: Regulatory Approval (if any), Pilot Testing Phase 7: Trainings, Marketing, sales team development Phase 8: Product Launch ( Sort Launch or Hard Launch ) Phases Involved

(^) Products Manuals (^) Contracts (^) Forms (^) Fatwas (^) Fees and Charges (^) Training Materials (^) Protected Soft Copy and Access right (^) Custodian (^) References/versions Product Documentation

Pakistan & Islamic Microfinance IndustryPakistan & Islamic Microfinance Industry

Muhammad Zubair Mughal Chief Executive Officer AlHuda Centre of Islamic Banking and Economics [email protected] www.alhudacibe.com