Random Variables and their

Expectation: Part III

Cyr Emile M’LAN, Ph.D.

Random Variable and Expectation: Part III – p. 1/??

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

The joint probability mass function of two discrete random variables and the joint probability density function of two continuous random variables. It also covers the joint distribution function, marginal probability mass/density functions, and conditional distributions. Definitions, theorems, examples, and computations.

Typology: Study notes

1 / 32

This page cannot be seen from the preview

Don't miss anything!

[email protected]^ Random Variable and Expectation: Part III

Random Variable and Expectation: Part III

Let^ X^ and

Y^ be two discrete random variables associated to a random experiment, each assuming values on the samplespace^

Sand^1

S, respectively.^2

The^ joint probability mass

function,

p(x, y)

,^ is defined for each pair of numbers

(x, y)^ in

S^ =^ S^1

⊗ Sby^2

p(x, y) =

P^ (X^ =

x, Y^ =

y)^.

Let^ A^ be any event in the sample space

S, that is, consisting

of pairs

(x, y)^ with

x^ ∈ S^1

and^ y^ ∈ S. Then the probability^2

that the random pair

(X, Y^ )

lies in A is obtained by summing

the joint probability mass function over pairs

(x, y)^ in

A:

[ P (X, Y

]^ ) ∈ A ∑= (x,y)∈ p(x, yA )^.

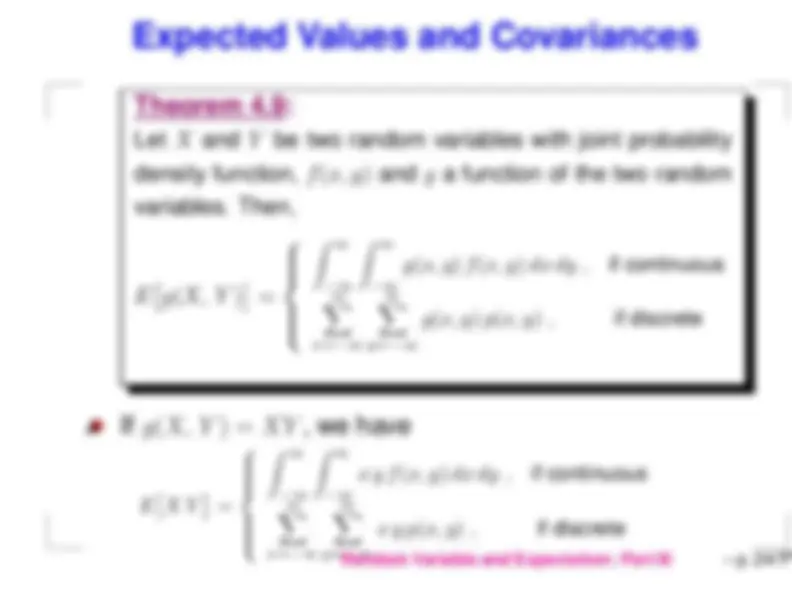

Random Variable and Expectation: Part III

Let^ X^

and^ Y^

be two discrete random variables with joint probability mass function,

p(x, y)

, defined on

S.^ Then, it

must^ p(

x, y)^ must satisfy:1. p(x, y)^ ≥^0

for all^ x

and^ y. ∑2. (x,y) p(x, y∈S ) = 1^.

Let^ X^

and^ Y^

be two discrete random variables with joint probability mass function,

p(x, y)

, defined on

S.^ The

joint

distribution function,

F^ (x, y)

,^ is defined as

F^ (x, y) =

P^ (X^ ≤

x, Y^ ≤

∑ y) =? x ∑ ?≤x y≤y

?? p(x, y )

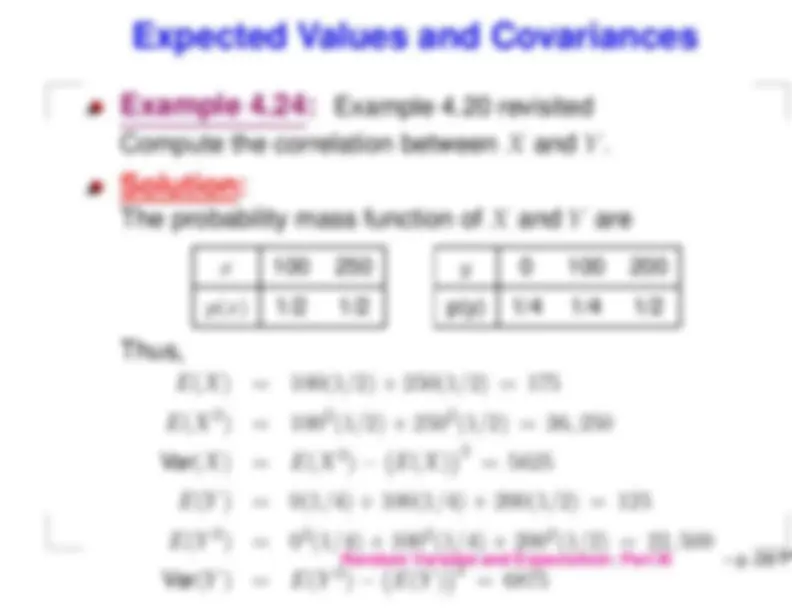

Random Variable and Expectation: Part III

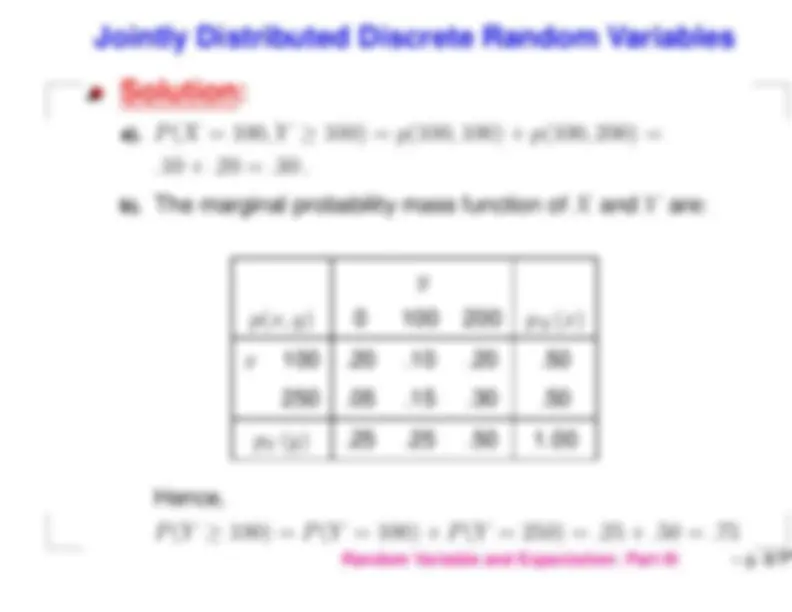

An large insurance agency services a number of customers who have purchased botha homeowner’s policy and an automobile policy from the agency. For each type ofpolicy, a deductible amount must be specified. For an automobile policy, the choicesare $100 and $250, whereas for a homeowner’s policy, the choices are $0, $100, and$200. Suppose an individual with both types of policy is selected at random from theagency’s files. Let

X^ = the deductible amount on the auto policy and

Y^ = the

deductible amount on the homeowner’s policy. Suppose the joint probability massfunction is

y p(x, y)^

0 100

200 x^100

.20^.

.

.^

.

a).^ Find^ P

(X^ = 100

, Y^ ≥^ 100)

.

b).^ Find the marginal probability mass function of

X^ and^ Y^

and^ P^ (Y^

≥^ 100).

Random Variable and Expectation: Part III

a).^ P^ (X

= 100, Y

≥^ 100) =

p(100,^

p(100,^ 200) =

.10 +^ .20 =

.^30. b).^ The marginal probability mass function of

X^ and

Y^ are:

y p(x, y)^

0 100

200

p(x)X^

x^100

.^

.10^.

.

.^ .^

.

p(y)^ Y^

.25^.

.^

Hence, P^ (Y^ ≥

P^ (Y^ = 100) +

P^ (Y^ = 250) =

.25 +^.

50 =^.^75

Random Variable and Expectation: Part III

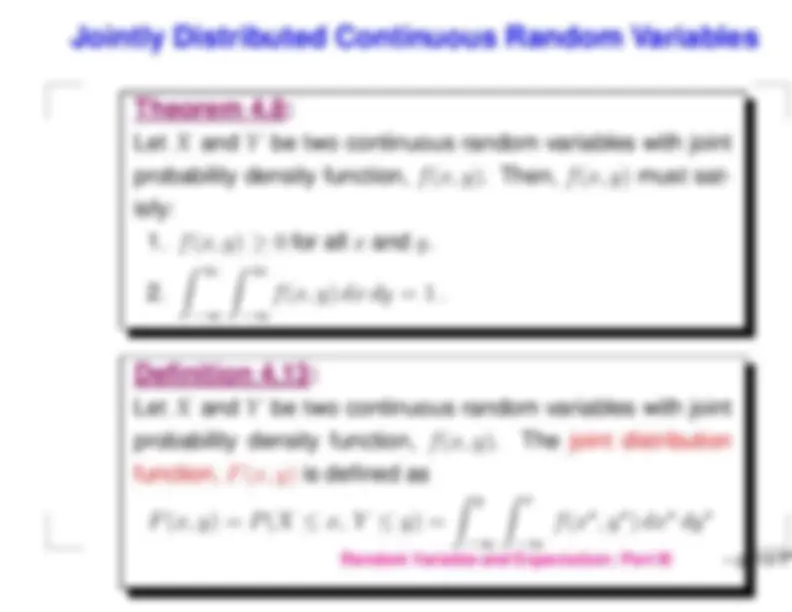

Let^ X^ and

Y^ be two continuous random variables with joint probability density function,

f^ (x, y)

. Then,

f^ (x, y)

must sat-

isfy:1.^ f^ (x, y

)^ ≥^0 for all

x^ and^

y.

∫^ ∞ 2.−∞ ∫^ ∞^ f^ (x, y−∞

)^ dx dy^

= 1^.

Let^ X^ and

Y^ be two continuous random variables with joint probability density function,

f^ (x, y

).^ The

joint distribution

function,

F^ (x, y)

is defined as F^ (x, y) =

P^ (X^ ≤

x, Y^ ≤

∫ y) = ∫^ yx −∞^ −∞

?? f (x, y

?^ ) dxdy ?

Random Variable and Expectation: Part III

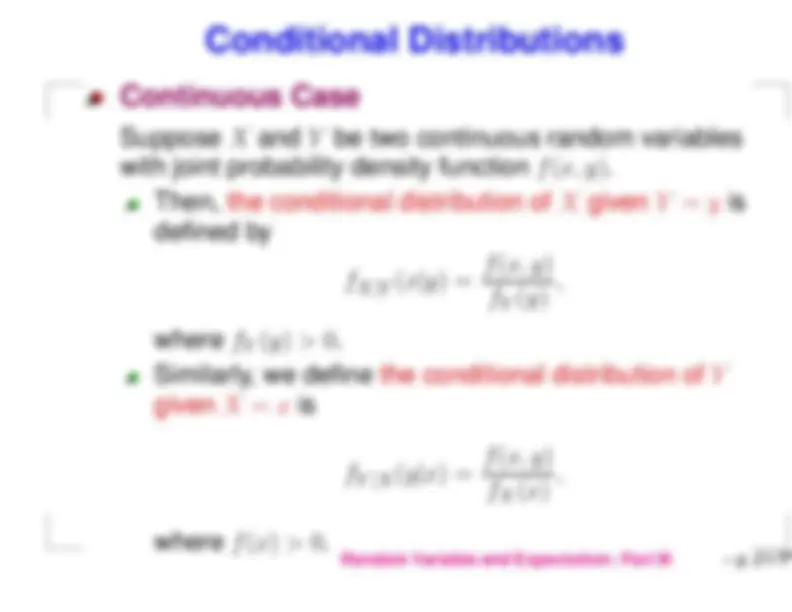

Let^ X^ and

Y^ be two continuous random variables with joint probability density function,

f^ (x, y)

. The^ marginal probability

density functions of

X^ and

Y^ ,^ f(X^

x)^ and^

f(y), respectively,Y^

are given by as

f(x)^ X^

∫^ ∞ =−∞ f^ (x, y)^

dy

f(y)^ Y^

∫^ ∞ =−∞ f^ (x, y)^

dx Random Variable and Expectation: Part III

a).^ We have ∫ ∫^ ∞∞ −∞−∞

f^ (x, y)^ dx dy

∫ = ∫^1165

(^2) (x + y) dx dy ∫ (^6) = 5 ∫^11 x dx dy 00

∫^16 + 50 ∫^12 ydx dy^0

∫ (^6) = 5 1 x dx^ + 0

∫^162 y 50

(^6) dy = 10 (^6) + = 1 15

b).^ We have (^1 P X^ ≤^ , Y^4

) (^1) ≤ 4

∫ (^6) = 5 ∫^1 /^41 / 0

4 2 (x^ +^ y 0

)^ dx dy ∫ (^6) = 5 ∫^1 /^41 / 0

4 x dx dy 0

∫^6 + 5 ∫^1 / 41 /^400 (^2) ydx dy

(^6) = · 20 ∣^ x=1 2 ∣x∣ ∣ 2 /^46 +^20 x==

∣^ y=1 3 ∣y∣· ∣ 3 /^43 =^320 y==

(^1) + = 640 (^7 )

Random Variable and Expectation: Part III

c).^ The marginal density function of

X^ and^

y^ are

f(x)^ X^

∫^ ∞ =−∞ f^ (x, y)^ dy

∫^6 = 5 1 x dy^ + 0

∫^162 y 50 dy

(^6) = x^5

∣ 3 ∣ 6 y∣+ ∣ 53 y=1^ = y==

62 x^ + 5 5

f(y)^ Y^

∫^6 = 5 1 (x^ +^ y 0

2 )^ dx^ =

∫^16 x dx 50

∫^16 + 50 (^2) ydx

6 x = 5 ∣^ x=1 2 ∣∣^ + ∣ 2 x==

662 y= 5 5

(^32) y+ 5

c).^ We have^ P

(^1 ≤^ Y^4

) (^3) ≤ 4

∫^3 / = 4 f(y)^ Y^1 / 4

∫^ dy = (^162 y^5

) (^3) +^ dy 5

37 Random Variable and Expectation: Part III = 80

Two random variables

X^ and

Y^ are said to be

independent

if for any two sets of real number

A^ and^

B

P^ (X^ ∈^

A, Y^ ∈

B) =^ P

(X^ ∈^ A

)^ P^ (Y^ ∈

B)

In other words,

X^ and

Y^ are independent if, for all

A^ and^

B,

the events

E=^ A^

{X^ ∈^ A

}^ and^ F

=^ {Y^ b ∈^ B}^ are indepen-

Random Variable and Expectation: Part III

Random Variable and Expectation: Part III

Random Variable and Expectation: Part III