Name: Jannah Mae A. Nene

Course and Year: BSA-2

Subject: ACCTG233

Date: October 8, 2020

Deadline of submission: October 9, 2020 at 3:30 PM thru LMS Moodle or email [email protected]

Topic 11 – Management Control and Strategic Performance Measurement

Exercise 1 (Evaluation of an Investment SBU)

The Cling Division has the following operating data:

Operating assets P400,000

Operating income 100,000

Minimum required rate of return 16%

Required:

(1) Compute the ROI and RI for this division

(2) Assume that the Cling Division is presented with an investment product yielding a 20 percent

return on its investment requiring a cash outlay of P60,000. Would the manager of the Cling

Division accept this investment under the ROI approach? How about under the RI approach?

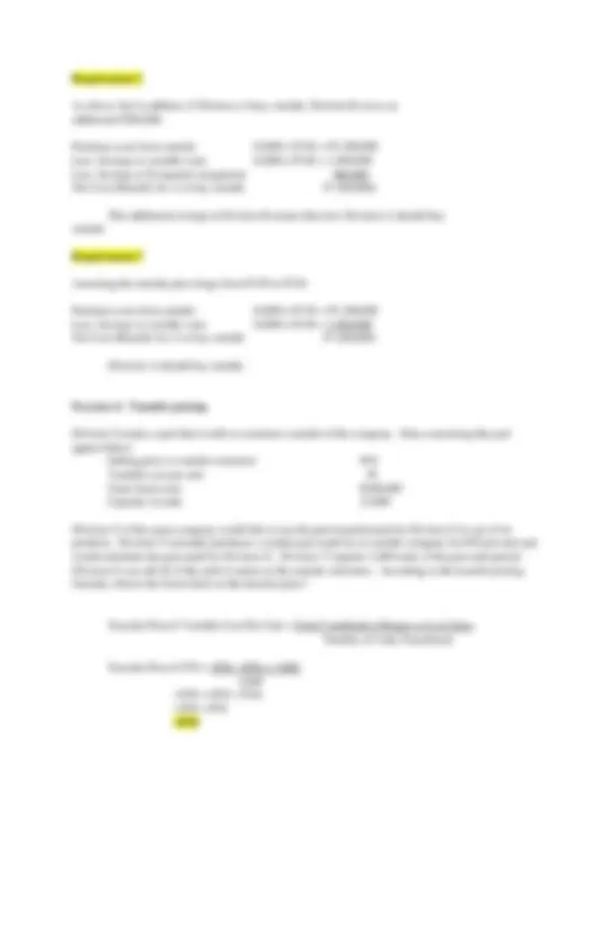

Requirement 1

ROI RI

Operating Assets P400,000 P400,000

Operating Income P100,000 P100,000

ROI (P100,000P400,000) 25%

Minimum required income

(16% x P400,000) P64,000

RI (P100,000 - P64,000) P36,000

Requirement 2

The manager of the Cling Division would not accept this project under the ROI approach since

the division is already earning 25%. Accepting this project would reduce the present divisional

performance, as shown below:

Present New Project Overall

Operating assets P400,000 P60,000 P460,000

Operating income P100,000 P12,000* P112,000

ROI 25% 20% 24.35%

* P60,000 x 20% = P12,000

Under the RI approach, on the other hand, the manager would accept this project since the new

project provides a higher return than the minimum required rate of return (20 percent vs. 16 percent). The

new project would increase the overall divisional residual income, as shown below:

Present New Project Overall

Operating assets P400,000 P60,000 P460,000

Operating income P100,000 P12,000* P112,000

Minimum required

return at 16% 64,000 9,600* 73,600

RI P 36,000 P 2,400 P 38,400

* P60,000 x 16% = P9,600