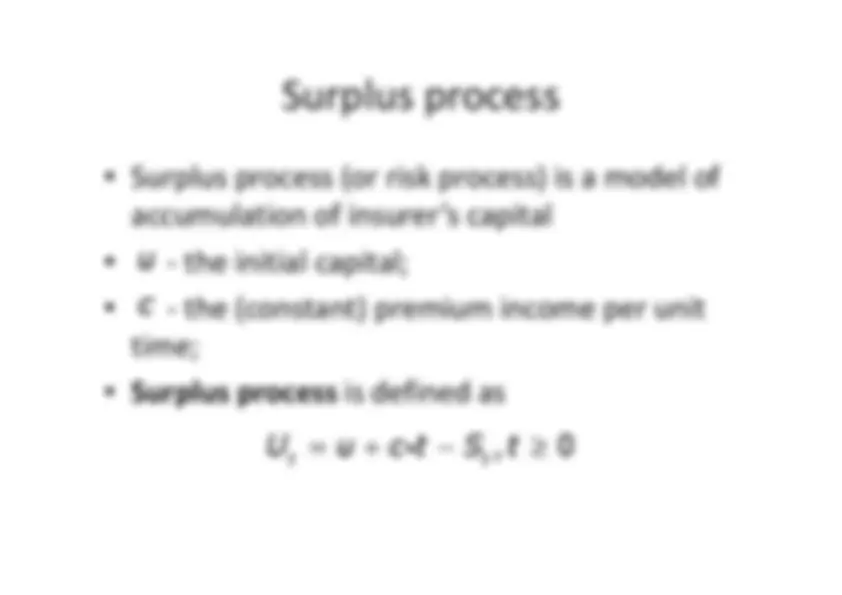

Surplus process

and ruin theory

and ruin theory

Risk theory

Warsaw University of Technology

Summer semester 2009/2010

R. Łochowski

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

The theory of ruin and surplus process in the context of insurance risk management. It covers the concepts of compound Poisson distribution, moment of ruin, ruin probability, loading factor, adjustment coefficient, and Lundberg inequality. The document also includes formulas and equations for calculating ruin probability and adjustment coefficient, as well as a problem related to proving the validity of the equations.

Typology: Assignments

1 / 12

This page cannot be seen from the preview

Don't miss anything!

Compound Poisson distribution

as a distribution of total claim amou

-^

with

1

2 ,^

-^ -^ homogeneous Poisson process

with

intensity

, modelling claims’ arrival (number

of claims between 0 and t)

-^

Total claim amount on time interval [0, t] maybe written as N^ t

1

2

t

t^

N

λ

-^

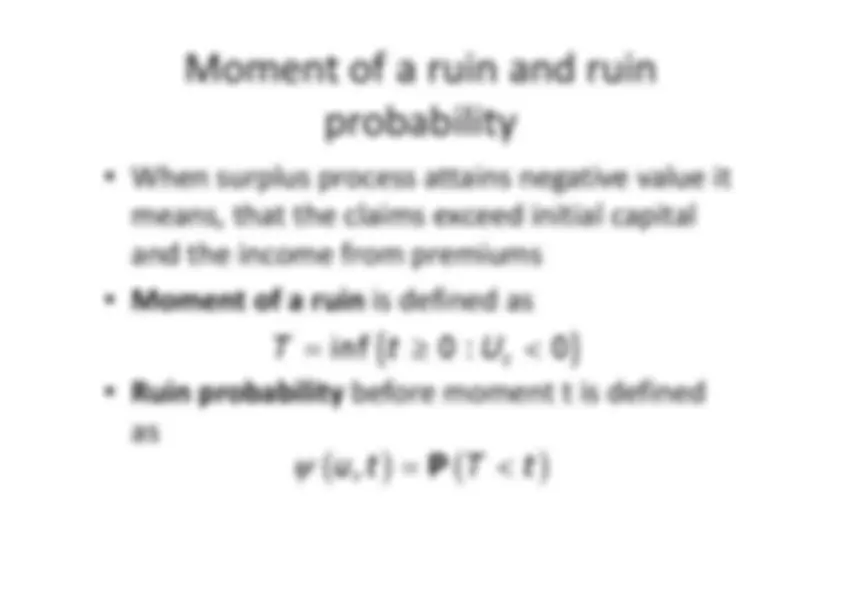

When surplus process attains negative value itmeans, that the claims exceed initial capitaland the income from premiums

-^

Moment of a ruin

is

defined

as

-^

Moment of a ruin

is

defined

as

-^

Ruin probability

before moment t is defined

as

{^

}

inf

t

t^

(^

)^

(^

)

,u t

t

ψ^

-^

When surplus process is observed in discretemoments

t^

= 0,1,2,3,…, we call it a

surplus

process in discrete time

u^

c n

n

i

-^

For

from law of large numbers we get

that almost surely

-^

from which follows

n^

n

u^

c n

n

i

, 1

c^

(^

)^

1

lim

n^

U^ n

n^

c^

→ ∞

(^

)^

(^

)^

(^

)

u^

u^

ψ

ψ =^

-^

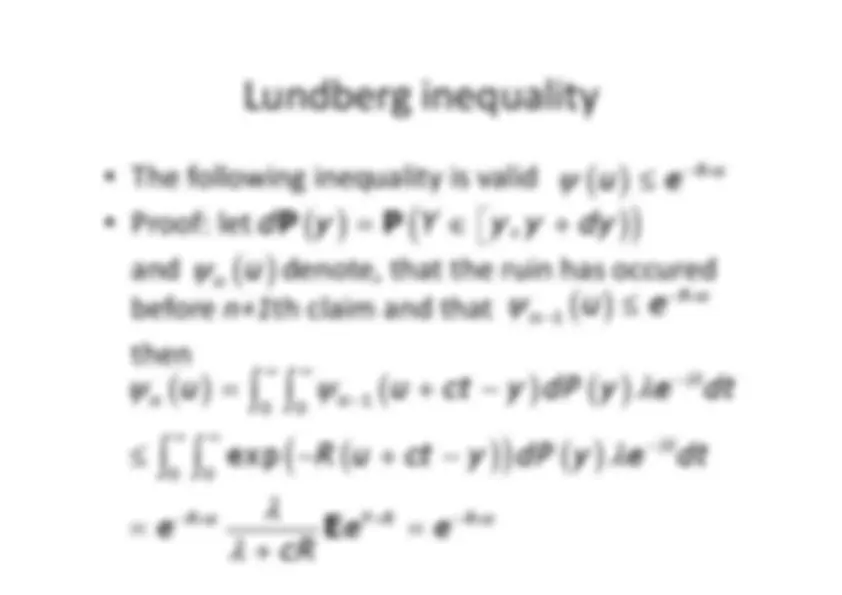

For a positive safety factor, there exists exactlyone positive solution (in R) of the equation

(^

)^

1

1

RS

Rc

S

e^

e

which is called

adjustment coefficient

-^

It may be proved that

(^

) S^1

e^

e

(^

)^

RY

Y

cR

e

λ

λ

λ

-^

Problem (theoretical one): to prove statementfrom the previous slide, i.e. that for thepositive loading factor, adjustment coefficient exists

and

is

uniquely

determined

exists

and

is

uniquely

determined

-^

Problem (computational): calculate theadjustment coefficient in the special casewhen claim sizes have exponential distributionwith parameter

β

-^

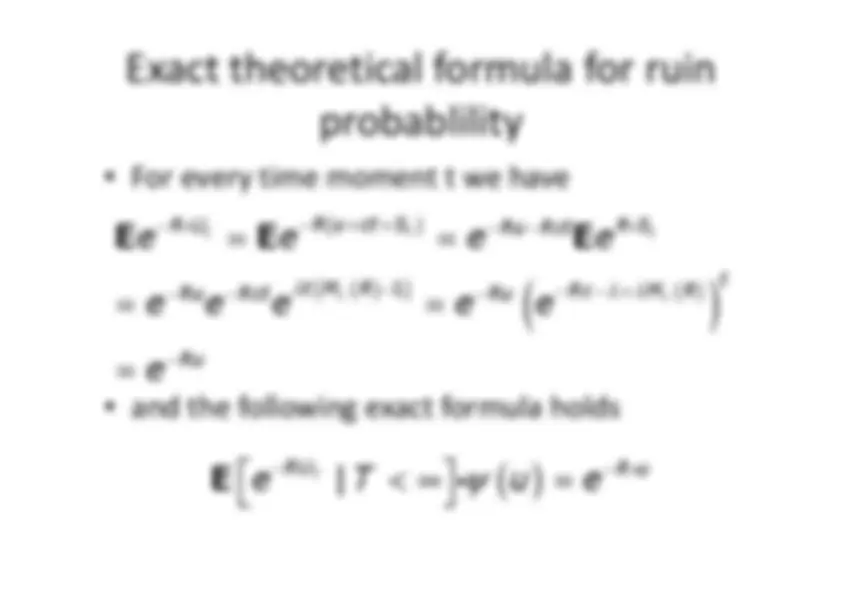

For every time moment t we have

(^

) (^ )

(^ )

t 1

t^

t

Y^

Y

R u

ct

S

R U

R S

Ru

Rct

t

t M

R

Rc

M^

R

Ru

Rct

Ru

e^

e^

e^

e

e^

e^

e^

e^

e

λ

λ^

λ

−^

+^

−^

−^

−

−^

−^

−^

−^

−^

−

=^

=

=^

=

E^

E^

E

i^

i

-^

and the following exact formula holds

(^ )

(^ )

1 Y^

Y

t M

R

Rc

M^

R

Ru

Rct

Ru

Ru e^

e^

e^

e^

e

e

λ

λ^

λ

−^

−^

−^

−^

−^

−

− =^

=

=

T| RU

R u

e^

T^

u^

e

ψ

−^

−

^

< ∞

=

^

E^

i

i

-^

For u<0 let us define

-^

Then we have the following formula

-^

From

the

above

formula

we

derive

(a bit

(^

)^

(^

)^

(^

)

0

0

t

u^

u^

ct

y^

dP

y

e^

λdt

ψ

ψ

λ

∞^

∞^

−

(^

)^

ψ^

-^

From

the

above

formula

we

derive

(a bit

complicated) equation Problem (theoretical): prove the above equation

(^

)^

(^

)^

(^

)^

(^

)

(^

)^

(^

)^

(^

)^

(^

)

0

0

'

u

c^

u^

u^

u^

y^

dP

y

u^

u^

y^

dP

y

u

ψ

ψ

ψ

λ ψ

ψ

∞