Download Ted Baker Plc and more Study notes Communication in PDF only on Docsity!

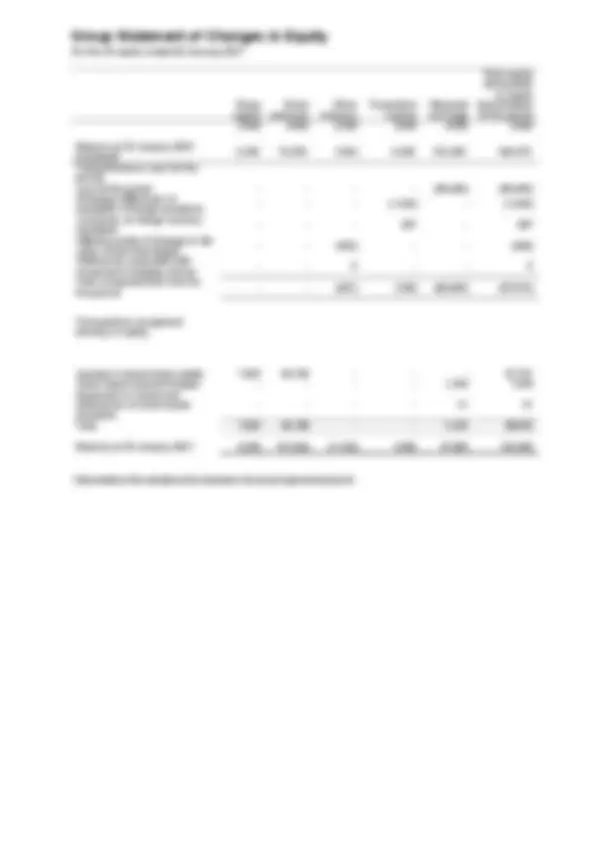

Ted Baker Plc (“Ted Baker”, the “Group”) Preliminary Results Announcement for the 53 weeks ended 30 January 2021 Strategic progress and increasing brand strength position the business for future success Rachel Osborne, Chief Executive Officer, commented: “We are making good progress against our strategic transformation plan and Ted Baker is increasingly well placed to take advantage of the significant growth opportunities ahead of us. The Ted Baker brand has strengthened further, with the number of active customers growing to 1.2m by the end of the year. “While the impact of COVID-19 is clear in our results and has amplified some of the legacy issues impacting the business, Ted Baker has responded proactively and is in a much stronger place than it was a year ago. During the period, we delivered robust cashflow generation, fixed our balance sheet, refreshed our senior leadership team and today we are upgrading our financial targets for the second time since outlining our new strategy last summer. Additionally, we have made good progress with our sustainability strategy, Fashioning a Better Future, including the mapping of all of our factory partners within our supply chain and significantly increasing our usage of cotton from sustainable sources to 69%. “We are a year into Ted Baker’s transformation plan and continue to believe that we have the right strategy and team in place to set the business up for a stronger, more sustainable future.” 53 weeks ended 30 January 2021 52 weeks ended 25 January 2020 (restated^1 ) Change Group Revenue £352.0m (^) £630.5m (44.2)% Underlying (Loss)/Profit Before Tax^2 £(59.2)m (^) £4.8m n/a (Loss)/Profit Before Tax £(107.7)m (^) £(77.6)m 38.8% Basic EPS (56.2)p (153.0)p n/a Underlying^2 EPS (26.0)p 6.7p n/a Dividend^3 nil 7.8p n/a Notes: (1) Details of the restatement are included in the annual report and accounts (2) Before non-underlying items (3) Declared and paid 13 th^ June 2021

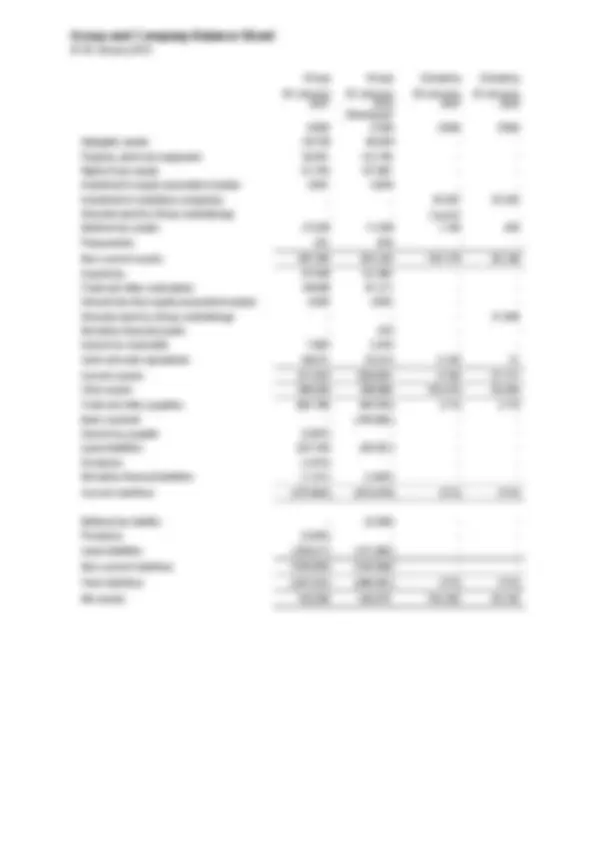

Financial Summary

- This year was a 53-week year and the extra week added 2% to sales. Throughout this document, unless otherwise stated, we will compare sales and profit in the 53 weeks to January 2021 with the 52 weeks in the prior year. Due to the level of disruption in the year, we do not believe comparison on a 52-week basis would be helpful.

- Group revenue down 44.2% (down 44.1% in constant currency) to £352.0m compared to £630.5m in the prior year, driven by the ongoing impact of COVID restrictions on trading globally.

- Underlying loss before tax of £59.2m, primarily driven by lower revenue levels, and partially offset by our cost actions.

- Retail sales including eCommerce down 42.2% (down 42.1% in constant currency) to £254.3m, compared to £439.9m in the prior year.

- ECommerce sales up 22.0% (up 22.1% in constant currency) to £144.9m, compared to £118.7m in the prior year, supported by continued investment in our digital business and significant improvements to our customer journey. Growth in our directly operated eCommerce channels of 30.2%.

- Wholesale sales down 50.3% (down 48.6% in constant currency) to £85.3m, compared to £171.5m in the prior year, reflecting market pressure on our Trustees.

- Improvement in net cash of £193.8m, which exceeds the net proceeds of the equity raise and disposal of the UBB building, representing positive free cash flow generation.

- Net cash of £66.7m at 30 January 2021, well ahead of management’s expectations.

- Upgrade of financial target. We now expect a net cash position at YE2023.

- Renewed Revolving Credit Facility (RCF). The Group has ongoing support from our four existing lending banks, with its facilities extended from August 2022 to November 2023, with a £90m facility until January 2022 and then £80m until November 2023, including a new set of covenants. Operational and strategic highlights In June 2020 we launched our three-year strategic transformation programme, Ted’s Growth Formula. Our progress in executing this plan has been encouraging, despite several of the legacy issues facing the business having been amplified by COVID. Alongside a rapid and effective response to the pandemic, the foundations of our business are now fixed, and we are switching our focus to growth. Key highlights for the period include:

- Brand strength enhanced. The Ted Baker brand remains healthy, notwithstanding the impact of extensive store closures during the pandemic lockdown period. Customers have responded positively to our refreshed social media, campaign imagery and new product. NPS increased during the period and we have 1.2m active digital customers.

- Excellent cash flow management embedded into business. The business has demonstrated cashflow discipline throughout the period, with a tight grip on working capital and the implementation of a new commercial stock cycle.

- Significant cost action taken. The Group commenced a full cost review at the start of the year, which increased in scope and scale during COVID, with £31m of annualised payroll savings and £8m of negotiated rent savings during the year.

- China JV delivered strong growth in first full year of operation. Our Chinese business grew 6% during the year, despite the store closures during Q1. Growth was robust in both stores and online and we have a healthy pipeline of new stores

- Significant cost out programme

- We have made material savings across our central costs and retail store costs. o Central and retail store costs: Annualised savings across both functions will be £31.0m per annum at a cash cost of £3.9m, ahead of previous guidance. o Store estate: We have negotiated and delivered rent savings of £8m during the financial year. We also benefitted from £27.8m of turnover-related rent savings, reflecting the flexible nature of a large amount of our Retail space. We will be continuing our programme of rent renegotiations in the year ahead to reflect the new commercial realities. Current Trading and Outlook The Group is reporting Q1 revenues, for the first 12 weeks to 24 April 2021. Q1 trading as been materially impacted by ongoing COVID restrictions, with lockdowns in place in the UK, Europe and Canada for parts of this period.

- Q1 FY22 Group revenue down 19.9% (down 17.3% in constant currency), driven by ongoing impact of COVID restrictions on trading globally. o eCommerce up 4.5% (up 25.9% vs. Q1 FY20), as the Group starts to take a less heavy promotional stance compared to the prior year. o Retail stores down 40.7% (down 73.1% vs. Q1 FY20). Globally, the Group lost 10 more trading days during the period than the prior year, with 53 days of trading during Q1 FY21 and 83 in Q1 FY20. We are encouraged with how our UK stores have performed since reopening on 12 April, albeit that revenue remains below FY20 levels. Our retail stores in metro cities and travel retail locations accounted for 36% of pre-COVID global store revenues and those stores remain materially below FY20 trading levels. o Wholesale and Licence down 22.4% (down 48.3% vs. Q1 FY20) reflecting cautious ordering from store-based trustees, as well as continued restrictions on store openings in Europe.

- Gross profit margin for eCommerce has increased around 250 bps, reflecting the Group reducing promotional levels.

- eCommerce performance is set against an exceptionally promotional market last year. Our promotional stance in the FY22 quarter remained in line with the market, but we have begun to move towards a more typical promotional schedule.

- Net cash was £29.6m at 24 April 2021. This positive cash position reflects continuing action to manage working capital and reduce expenditure. Revolving credit facilities of £133m remained undrawn throughout the period. The Group is implementing a new reporting calendar, aligned to internal management reporting, Q2 will represent weeks 13-28, Q3 weeks 29-40 and Q4 weeks 41-52. This new calendar will allow greater insights around trading margin and period end cash position. The Group does not intend to report against periods outside this new calendar, which is considered an appropriate level of financial disclosure. Following the successful execution of the five operational targets that were set for Year 1 of the transformation plan, the Group has announced six operational targets for the new financial year, on the assumption of no further major lockdowns in core territories. The targets are as follows:

o Improve Product Proposition: increase full price sales mix in H2 by 500bps o Drive Digital Development: complete eCommerce re-platform launch o Sustain Brand Strength: Maintain top quartile NPS score o Grow Global Footprint: Open 10 new stores in strategic markets o Promote ESG: Increase sustainable cotton use to at least 75% o Continue Property Cost Reduction: Base rent saving of at least 15%, and each renegotiation to deliver at least 50% reduction in base rent Enquiries: Ted Baker Plc Tel: +44 (0) 20 7255 4800 Rachel Osborne, Chief Executive Officer David Wolffe, Chief Financial Officer Tulchan Communications Tel: +44 (0) 20 7353 4200 Jonathan Sibun/Jessica Reid Media images available for download at: http://www.tedbakerplc.com/ted/en/mediacentre/imagelibrary Notes to Editors Ted Baker Plc - "No Ordinary Designer Label" Ted Baker is a global lifestyle brand distributing across five continents through its three main distribution channels: retail (including eCommerce); wholesale; and licensing. Ted Baker has 521 stores and concessions worldwide, comprising 182 in the UK, 99 in Europe, 136 in North America, 95 in the Middle East, Africa and Asia, and 9 in Australasia. We offer a wide range of collections including Menswear; Womenswear; Accessories; Bedding; Childrenswear; Eyewear; Footwear; Fragrance and Skinwear; Gifting and Stationery; Jewellery; Lingerie and Sleepwear; Men’s Underwear and Loungewear; Luggage; Neckwear; Rugs; Suiting; Technical Accessories; Wallpaper; and Watches.

Channel Performance Retail Our retail channel comprises stores, concessions and eCommerce, providing an omni-channel experience. We operate stores and concessions across the UK, Europe, North America and South Africa, and localised eCommerce sites in the UK, continental Europe, the US, Canada and Australia. We also have eCommerce businesses with many of our concession partners. Our stores are important to the success of our digital businesses through supporting brand awareness and showcasing our products. The relatively high number of concession locations and short lease length on our stores (averaging 3.5 years) allow us to maintain a flexible business model. The performance of the Retail business reflects the unprecedented trading conditions across the world, with stores remaining closed to comply with local lockdowns, particularly during the first half of the year. Where they were remained open, footfall was significantly below normal levels. Demand shifted onto online channels, with eCommerce sales increasing to 57.0% (2020: 27.0%) of total retail sales in the year. Store performance improved in the second half as the impact of lockdown and trading restrictions was reduced, particularly in the run-up to the peak Christmas trading period. We have continued to review and refine our store portfolio in line with new trading conditions. Given lower footfall, and despite discussions with landlords to renegotiate rent, we determined that a several locations would no longer be viable to operate and could be exited cost-effectively. We closed four stores during the year, contributing to a reduction in the average retail square footage of 4.8% to 421,435 sq ft (2020: 442,790 sq ft). This follows the transfer in the second half of FY20 of 14 stores in China and Hong Kong to joint ventures and 4 stores in Japan to a license partner. These stores generated £9.0m in sales during 2020. During the first half the Group furloughed store colleagues in response to government-imposed lockdowns. As it became apparent that market demand was likely to remain weak for the remainder of the year, we reviewed the store staffing model and a significant number of roles were made redundant to ensure that stores remained viable. We benefitted from government support, such as business rates holidays and job support schemes, as well as rent savings and waivers through negotiations with landlords and reductions in turnover-related rent. Driving business through our online channels, as well as the highly offer-driven market through the year, necessitated some increased expenditure on marketing and promotions. As a result of all the cost movements combined, retail operating costs excluding non- underlying items decreased by 28.7% to £165.5m (2020: £232.2m). Wholesale Our wholesale business in the UK serves countries across the world, primarily in the UK and Europe, as well as supplying products to stores operated by our territorial

licence partners. In addition, we operate a wholesale business in North America serving the US and Canada. Wholesale sales decreased by 50.3% (48.6% in constant currency^1 ) to £85.3m (2020: £171.5m) as our wholesale trustees’ businesses were also affected by COVID. Margin was adversely affected by the discounts we offered to support a number of key trustee businesses and an increase in the mix of off-price product, which contributed to the reduction in wholesale gross margin to 37.6% (2020: 39.8%) in the period. Licence Income in revenue We operate both territorial and product licences. Our licence partners are carefully selected as experts in their field and share our passion for unwavering attention to detail and firm commitment to quality. Territorial licences cover specific countries or regions in Asia, Australasia, Europe, the Middle East, Africa and Central America, where our partners operate licensed retail stores and, in some territories, wholesale operations. Product licences cover Bedding; Childrenswear; Eyewear; Fragrance and Skincare; Gifting and Stationery; Jewellery; Lingerie and Sleepwear; Men’s Underwear and Loungewear; Luggage; Neckwear; Rugs; Suiting; Ted’s Grooming Rooms; Technical Accessories; Wallpaper; and Watches. Licence income decreased by 34.5% to £12.4m (2020: £19.0m). Product licence income was affected by the challenging trading environment and particularly impacted in formalwear, adversely affected by the increase in working from home, as well as the replacement of existing agreements for watches and childrenswear with new partners. Royalty payments from regional franchise operators were also impacted by the restrictions on trading and lower sales levels, particularly in the Middle East and Asia. Collection Performance Ted Baker womenswear sales decreased by 40.7% to £219.7m (2020: £370.4m) and represented 64.7% (2020: 60.6%) of total sales. Ted Baker menswear sales were down 50.3% to £119.8m (2020: £241.1m) and represented 35.3% of total sales (2020: 39.4%). Demand for more formal styles and occasionwear were particularly affected by lockdown, and these represent a greater proportion of the menswear range.

North America 53 weeks ended 30 January 2021 52 weeks ended 25 January 2020 Variance Constant currency variance^1 Revenue £102.8m £194.6m (47.2%) (46.7%) Total retail revenue £69.9m £129.8m (46.1%) (45.6%) Store revenue £39.7m £107.7m (63.2%) (62.8%) ECommerce revenue £30.3m £22.1m 37.2% 38.3% Average square footage* 137,894 138,152 (0.2%) Closing square footage* 135,215 139,822 (3.3%) Sales per square foot including eCommerce sales

Sales per square foot excluding eCommerce sales

Wholesale revenue £32.8m £64.8m (49.3%) (48.9%) Own stores 35 38 (7.9%) Concessions 64 64 0% Outlets 12 12 0% Partner stores/concessions 25 26 (3.8%) Total 136 140 (2.9%) *Excludes licence partner stores. In comparison to the UK & Europe, disruption to trading in North America stores started later, and the adverse impact on demand from COVID-19 was supplemented by political and social unrest. We closed 3 stores during the year, where the economics of reopening were unattractive, and renegotiated leases to further improve profitability in a number of other locations. This contributed in a drop in Retail sales of 46.1% (45.6% in constant currency^1 ) to £69.9m (2020: £129.8m).Our eCommerce business delivered a strong performance, with sales increasing by 37% to £30.3m (2020: £22.1m), Ecommerce sales represented 43.3% of total retail sales (2020: 17.0%).

Rest of the World 53 weeks ended 30 January 2021 52 weeks ended 25 January 2020 Variance Constant currency variance^1 Revenue £2.4m £13.3m (82.0%) (79.8%) Total retail revenue £2.4m £13.3m (82.0%) (79.8%) Store revenue £2.4m £11.2m (78.7%) (76.1%) ECommerce revenue - £2.1m (100.0%) (100.0%) Average square footage* 7,104 20,105 (64.7%) Closing square footage* 7,104 7,104 0% Sales per square foot including eCommerce sales

Sales per square foot excluding eCommerce sales

Own stores 4 4 0% Concessions 0 0 0% Outlets 0 0 0% Partner stores/concessions 79 83 (4.8%) Joint venture locations 21 15 40.0% Total 104 102 2.0% *Excludes licence partner stores. The reduction in sales outside of our core European and North American businesses reflects the evolution of our distribution strategy. In the second half of FY20, we transitioned our businesses in China (including Hong Kong S.A.R. and Macau S.A.R.) to a joint venture, covering 14 stores and concessions, and eCommerce, with the income from these businesses now reflected in other income. In China, our venture’s expansion plans have been delayed by COVID, but managed to open seven during the period, and now operates 21 stores and concessions across the region (2020: 15 locations). In Japan, we announced an agreement with our licence partner Sojitz Infinity in August 2019, and transitioned operations into the partnership during the second half of FY20. Our partner opened three new stores, and now operates seven stores and concessions across the region (2020: four locations). The joint venture with our Australian licence partner, Flair Industries Pty Ltd, operates nine stores in Australasia (2020: nine stores).

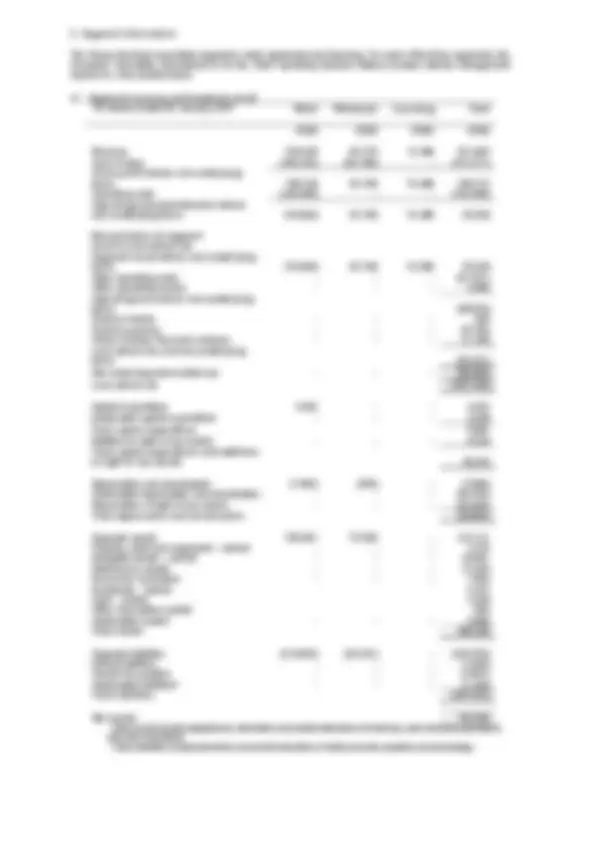

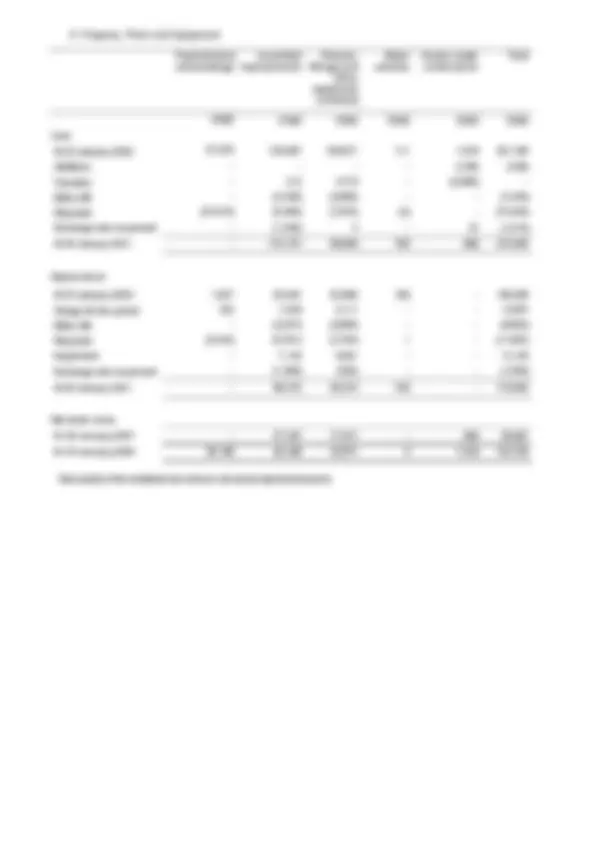

making headcount reductions in store and head office permanent staff, where appropriate, saving £31m on an annualised basis initiating discussions with our landlords to abate fixed rent during the closure periods and reduce rent thereafter to reflect lower levels of footfall. This generated savings of £8.0m in the year. Loss/profit before tax and non-underlying items and Loss/profit before tax The loss before tax was £107.7m (2020: loss of £77.6m). The loss before tax, non- underlying items was £59.2m (2020: profit of £4.8m). Non-underlying items Non-underlying items before tax in the period amounted to £48.6m (2020: £82.4m) and comprised the following items expenses / (income): Note: details of the restatement and of the above items can be found in the notes to the accounts 53 weeks ended 30 January 2021 52 weeks ended 25 January 2020 (Restated) £’000 £’ Included in cost of sales: Inventory changes in estimates (6,065) (32,351) Change to inventory obsolescence provision - (13,539) Onerous contract provision (1,973) - Other 81 2,2 21 Included in Gross Profit (7,957) (43,669) Included in distribution costs: (Loss) on disposal of business - (7,585) Impairment of intangibles, property, plant and equipment and right- of-use assets (45,303)^ (13,969) Other closure costs - (603) Included in administrative costs: Acquisition costs and unwind of fair value accounting adjustments (1,987) (4,710) Reorganisation, restructuring costs and other legal and professional costs (11,415)^ (7,852) Included in Other Operating (Loss)/income: Gain on disposal of business 17,446 - Included in operating profit (49,216) (78,388) Included in share of post-tax profits from joint venture: Unwind of fair value adjustments (7) (989) Included in finance income/(expense): Foreign exchange on the translation of monetary assets and liabilities denominated in foreign currencies 655 (3,026) Non-underlying items (48,568) (82,403)

Finance income and expenses Net finance expenses were £7.7m (2020: £15.5m). The IFRS 16 interest expense for the period was £6.8m (2020: £8.3m). Excluding the impact of non-underlying items, net finance expenses were £8.4m (2020: £12.4m). Taxation The Group tax credit for the period was £21.3m (2020: credit of £9.4m). This effective tax rate is lower than the UK tax rate for the period of 19%, primarily due to the Group being loss making in territories where it has major market operations and due to the utilisation of previously unrecognised tax losses in territories with higher tax rates. Cash Flow We took prompt action to support the Group’s cash position, to ensure it has sufficient resources to trade through an extended period of weak demand while investing in profitable growth. We brought in additional financing through the sale of the Ugly Brown Building for gross proceeds of £77.8m and the issuance of £105.0m new equity (gross). The Group’s working capital position was also reviewed. Actions to maintain cash and manage liquidity included increased sell-through and liquidation of older, excess stock significantly intake reductions to align stock levels with demand agreeing extended payment terms with suppliers deferral of rental payments As a result, net working capital, which comprises inventories, trade and other receivables and trade and other payables, decreased by £68.3m to £34.4m (2020: £102.7m). Continued tight cash management ensured that, despite a second UK lockdown during December and January, net cash outflow was minimal during the second half. Group capital expenditure of £7.0m (2020: £25.8m) has been significantly reduced. We are continuing to invest in systems and infrastructure to support our digital businesses and improve efficiency, but investment on physical locations has been limited only to essential works. Borrowing facilities The Group's net cash balance at 30 January 2020 was £66.7m (2020: net debt £127.1m). On 23 March 2020, the Group announced that its lending bank syndicate agreed to increase the headroom under the Group's revolving credit facilities of £180m (Facility A), by a further £13.5m until 18 December 2020 (Facility B). On 20 May 2020, the lending bank syndicate agreed to increase the headroom under Facility B by a further £11.5m, taking the total Facility B facility to £25m, with a revised Facility B expiry date of 18 January 2022.

the impact of Brexit. To date, the main operational impacts have been the flow of goods into the UK through the ports, and from the UK to stores and customers in Europe. We have set up a customs warehouse in the UK, which became operational in April 2021 and has partially mitigated the impact of higher duties, but there remain a number of other areas outstanding, including rules of origin and reclamation of input VAT. We expect that a full year impact of Brexit on profits will be c.£5m, and anticipate, only to a limited extent, mitigating the extra cost of duties through the reflowing of inventory for our EU stores. Earnings per share and dividends The basic loss per share was 56.2p (2020: loss per share 153.0p). Underlying loss per share, which excludes non-underlying items, changed to a loss of 26.0p (2020: earnings per share 6.7p). Given current trading conditions and the high level of uncertainty about the future, the Board has determined that no final dividend is to be paid (2020: 40.7p). In the long term we remain committed to paying dividends and returning surplus cash to our shareholders. David Wolffe Chief Financial Officer Notes:

- Constant currency comparatives are obtained by applying the exchange rates that were applicable for the period ended 25 January 2020 to the financial results in overseas subsidiaries for the 53 weeks ended 30 January 2021 to remove the impact of exchange rate fluctuations

Principal Risks and Uncertainties

Risk management is a key part of Ted Baker’s business strategy and success. As with any business, we face inherent risks, and we keep these under constant review. At the same time, we consider potential new risks and actions we can take to reduce or where possible eliminate them. Of course, risk management is not an exact science; it is designed to manage the risk of failure to reach our business objectives. Not surprisingly, in a year that has seen heightened risks ranging from COVID- to the recapitalisation of the balance sheet and the stock inventory review, risk has been high on our agenda. As a result, we have reviewed our approach to risk through the year. Important actions included the refresh of the management Risk Committee and developing our Group-wide programme to risk, which lets us identify, analyse and assess risks and then manage, control and monitor them. The Board and the Audit & Risk Committee work together with the management Risk Committee to deal with different aspects of the process. Our ongoing process for identifying, evaluating and managing the significant and emerging risks faced by the Group has been in place throughout the year. Oversight Our risk oversight is designed to give a clear picture of risk from every angle, from Group to operational levels. Board The Board is ultimately responsible for our approach to risk management and internal controls. It is also responsible for reviewing the effectiveness of our management and controls and setting the Group’s appetite for risk. This is done on a regular basis, helping us to identify emerging risk and assess the status of existing risk. Risk management will continue to be a key focus for the Board next year. Audit & Risk Committee The Audit & Risk Committee is responsible for overseeing and reviewing the effectiveness of the Group’s internal control and risk management systems. It reports its findings to the Board regularly through the year and also assesses the findings and recommendations of the Management Risk Committee and the Group’s external and internal audit processes, then looks critically at how the business responds. Executive Team The Executive Team is responsible for the identification and evaluation of significant risks applicable to their areas of the business, along with the design and operation of suitable internal controls. These risks are assessed on an ongoing basis through the year and may be associated with a variety of internal or external sources. Management Risk Committee The management Risk Committee was re-established last year. It reviews risk management and control process for each of our key business areas. Its members include relevant people from the Executive Team and heads of department. This is designed to give more people ownership of risk across the business and to keep risk front of mind on a day-to-day basis. This year, the Audit & Risk Committee reviewed and adopted revised terms of reference which can be found on the Company website www.tedbakerplc.com. The revised terms cover: o The authority, resources and co-ordination of those involved in the identification, assessment and management of significant risks faced by the Group.

Principal Risks Risk category / issue Potential issue Mitigation Change in level of risk Competition A lack of insight around customers and competitors could result in Ted Baker being overtaken by the competition, particularly if our market position isn’t clear. This could reduce our market share and supply chain buying power if we are not seen as competitive with other brands or we fail to offer a competitive and suitably diverse product mix. We regularly review performance, product, price and our competitors to make sure we are best placed to succeed in a competitive market. We continue to invest in our online business, including the appointment of a Chief Customer Officer, Jennifer Roebuck, to steer this activity. Increased, as a result of the global pandemic Changing customer preferences We fail to understand and respond to changes in customer preferences. For example, lack of stock diversity or preferred shopping channel, or lack of influencer recommendation, results in Ted Baker losing its competitive edge. This could lead to a loss of sales, reduced margins, missed opportunities for growth or a poor balance of sales channels We maintain a high level of market awareness and an understanding of consumer trends and fashion so we can respond to changes in consumer preference. We use customer data to develop targeted marketing and promotional activity. We continue to focus on product design, quality and attention to detail Increased, as a result of the global pandemic

Principal Risks Risk category / issue Potential issue Mitigation Change in level of risk Execution of transformation strategy Failing to deliver our corporate transformation strategy could result in Ted Baker not realising the long-term goals of the business. This could be a result of: o The wrong transformation strategy being rolled out to the business (or failing to pivot that strategy if the operating environment changes). o A lack of bandwidth – starting on too many activities without sufficient resource, an inability to focus on future value due to short- term firefighting, an inability to retain and recruit the right talent, confusion around responsibility for individual workstreams, misaligned prioritisation or competing priorities. For example, failing to align our finance strategy with the wider business strategy, inability to deliver strategy due to budget constraints. The Group’s Directors and Executive Team have set up regular reviews to monitor and assess the ongoing progress of the new transformation strategy with detailed execution plans. These plans are designed to successfully deliver the new strategy while reducing any new risk No change