Download Econometrics Handout: Classical Linear & Normal Regression Models and more Study notes Introduction to Econometrics in PDF only on Docsity!

Economics 210 Econometrics

Handout # III The Classical Linear Regression Model

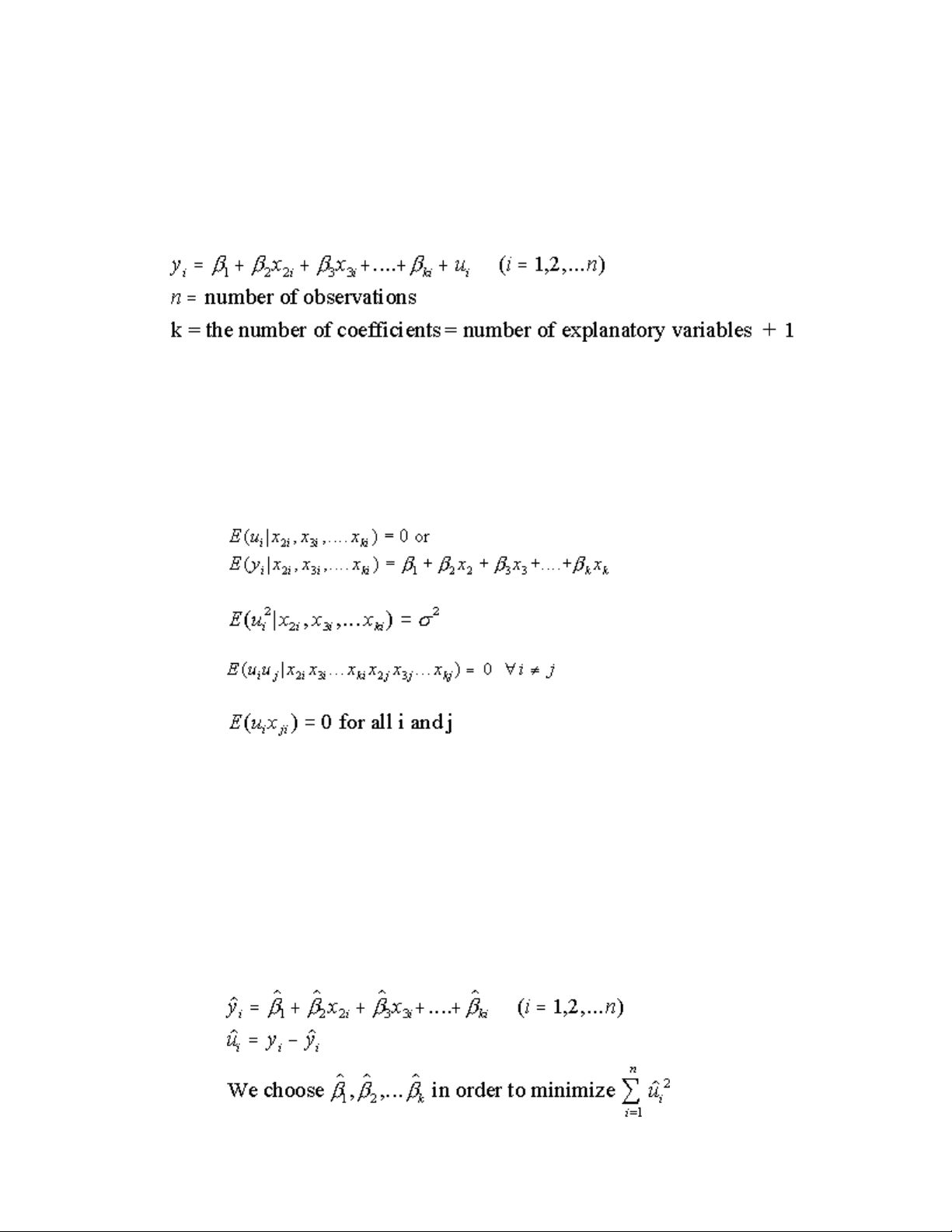

The Classical Linear Regression Model

We make the following assumptions. ( Gujarati pg 65-75):

- The model is linear in parameters.

- The explanatory variables are non-stochastic.

- n > k

- The explanatory variables each have positive finite variance

- The model is correctly specified

- There is no perfect multicolinearity We estimate the model by ordinary least squares: OLS

The estimated coefficients are random variables. It can be readily shown that

This last result says that is the Best Linear Unbiased Estimator, BLUE, of. This can be stated more generally. Let be any linear function of the coefficients for which a linear unbiased estimator exists. Then is the best linear unbiased estimator of.

The Classical Normal Linear Regression (CNLR) model. If in addition to the above assumptions we assume.

we get the classical normal linear regression model. In this case

Substituting an appropriate estimator for we get the t ratio

We use the t-ratio to test hypotheses about and find confidence intervals for the coefficients.

We estimate by

Extensions: Non-linear equations (Linear in parameters).

- Reciprocal

- Polynomial

- Log-log

(Note that in this formulation is the elasticity of Y with respect to xj.)

4 Semi-log

Note: is equal to the percentage change in Y associated with a unit change in xj. This form of the semi-log equation is widely used in applications involving growth and interest. Semi-log

5 Linear trend