TRIAL BALANCE

Samir K Mahajan

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Trial balance is a statement which shows debit balances and credit balances of all accounts in the ledger. Since, every debit.

Typology: Slides

1 / 26

This page cannot be seen from the preview

Don't miss anything!

Samir K Mahajan

Trial balance is a statement which shows debit balances and credit balances of all accounts in the ledger. Since, every debit should have a corresponding credit as per the rules of double entry system, the total of the debit balances and credit balances should tally (agree). In case, there is a difference, one has to check the correctness of the balances brought forward from the respective accounts. Trial balance can be prepared in any date provided accounts are balanced. Methods A trial balance can be prepared in the following methods. i. The Total Method :According to this method, the total amount of the debit side of the ledger accounts and the total amount of the credit side of the ledger accounts are recorded. ii. The Balance Method :In this method, only the balances of an account either debit or credit, as the case may be, are recorded against their respective accounts. The balance method is more widely used, as it supplies ready figures for preparing the final accounts. Sundry Debtors and Sundry Creditors: In the ledger there are many personal accounts, some of them may show debit balances, some others may show credit balances. If all the names are to be written in the trial balance it will be unduly long. Therefore, a list of names with the debit balances is prepared. This list is known as ‘Sundry Debtors’ (Sundry means ‘many’). Similarly, a list of names with the credit balances is prepared. This list is known as ‘Sundry Creditors’.

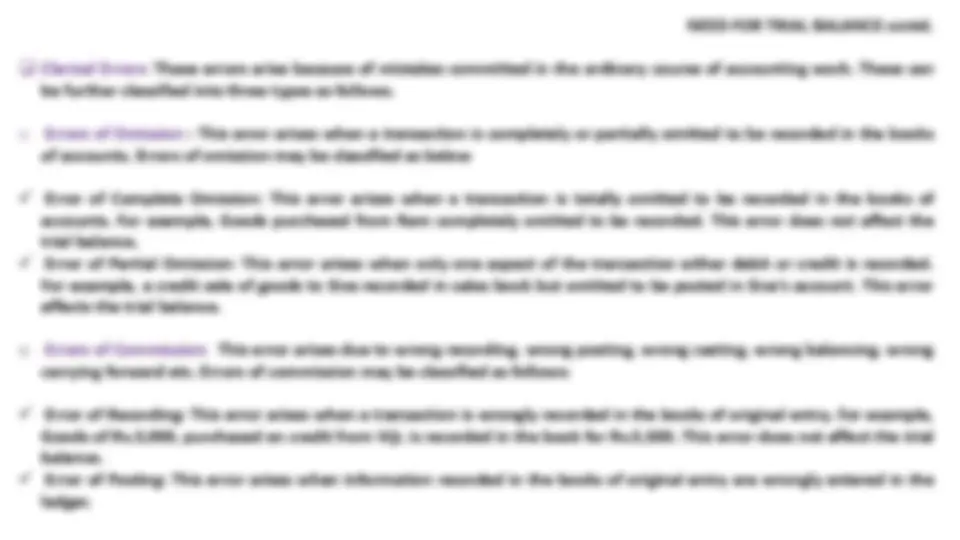

NEED FOR TRIAL BALANCE contd. Clerical Errors: These errors arise because of mistakes committed in the ordinary course of accounting work. These can be further classified into three types as follows. o Errors of Omission : This error arises when a transaction is completely or partially omitted to be recorded in the books of accounts. Errors of omission may be classified as below Error of Complete Omission: This error arises when a transaction is totally omitted to be recorded in the books of accounts. For example, Goods purchased from Ram completely omitted to be recorded. This error does not affect the trial balance. Error of Partial Omission: This error arises when only one aspect of the transaction either debit or credit is recorded. For example, a credit sale of goods to Siva recorded in sales book but omitted to be posted in Siva’s account. This error affects the trial balance. o Errors of Commission: This error arises due to wrong recording, wrong posting, wrong casting, wrong balancing, wrong carrying forward etc. Errors of commission may be classified as follows: Error of Recording: This error arises when a transaction is wrongly recorded in the books of original entry. For example, Goods of Rs. 5 , 000 , purchased on credit from Viji, is recorded in the book for Rs. 5 , 500. This error does not affect the trial balance. Error of Posting: This error arises when information recorded in the books of original entry are wrongly entered in the ledger.

Error of Casting (Totalling) :This error arises when a mistake is committed while totalling the subsidiary book. For example, instead of Rs. 12 , 000 it may be wrongly totalled as Rs. 13 , 000. This is called overcasting. If it is wrongly totalled as Rs. 11 , 000 , it is called undercasting. Error of Carrying Forward :This error arises when a mistake is committed in carrying forward a total of one page to the next page. For example, Total of purchase book in page 282 of the ledger Rs. 10 , 686 , while carrying forward the balance to the next page it was recorded as Rs. 10 , 866. Compensating Errors: The errors arising from excess debits or under debits of accounts being neutralised by the excess credits or under credits to the same extent of some other account is compensating error. Since the errors in one direction are compensated by errors in another direction, arithmetical accuracy of the trial balance is not at all affected in spite of such errors. For example, If the purchases book and sales book are both overcast (excess totalling) by Rs. 10 , 000 , the errors mutually compensate each other. This error will not affect the agreement of trial balance. NEED FOR TRIAL BALANCE contd.

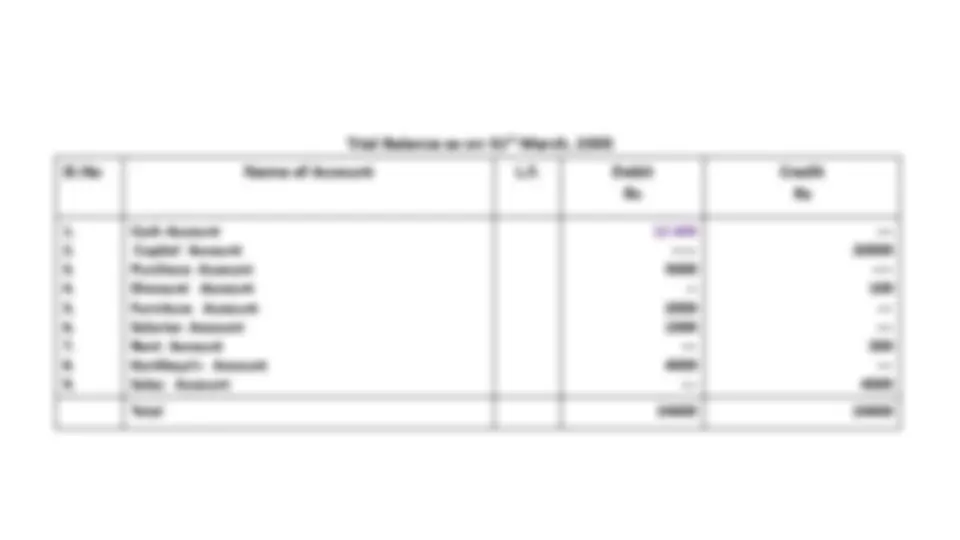

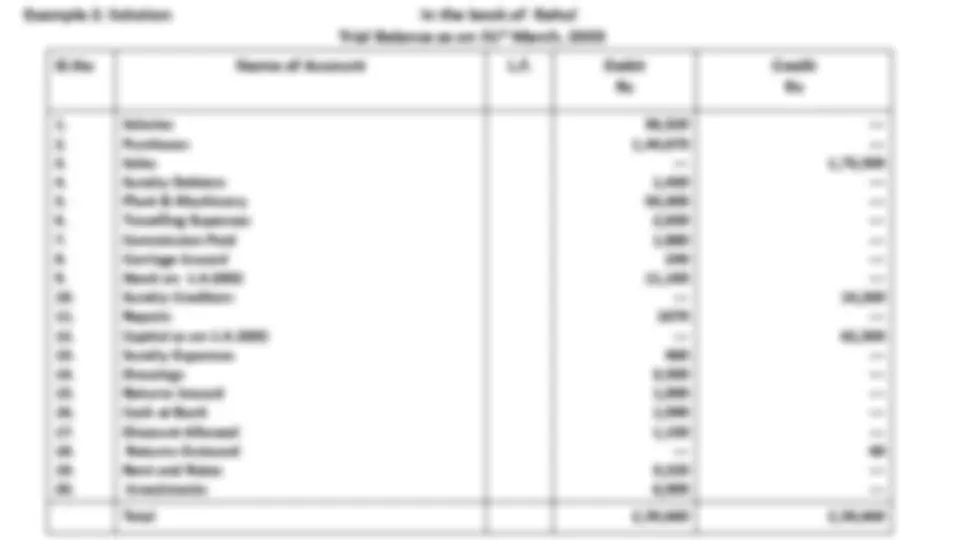

Format : Trial Balance Trial Balance of ABC as on ………………. Sl.No Name of Account L.F. Debit Rs Credit Rs Note: i. Date on which trial balance is prepared should be mentioned at the top. ii. Name of Account column contains the list of all ledger accounts. iii. Ledger folio of the respective account is entered in the next column. iv. In the debit column, debit balance of the respective account is entered. v. Credit balance of the respective account is written in the credit column. vi. The last two columns are totalled at the end.

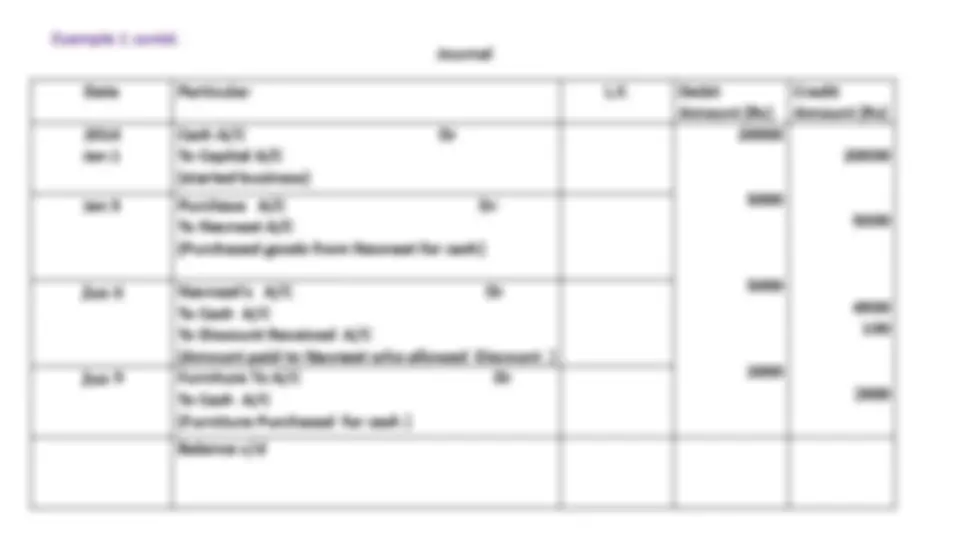

Example 1: Pass the following journal entries and post them in ledger account and prepare a trial balance. 2005 Jan 1: Started business with cash Rs 20, 000 Jan 3: Purchased goods from Navneet Rs 5000 Jan 6: Paid to Navneet Rs 4900 Discount Allowed Rs 100 Jan 9: Purchased Furniture Rs 2000 Jan 12: paid salaries Rs 1000 Jan 15 : Rent received Rs 500 Jan 18: Sold goods To Kartikeya Rs 4000

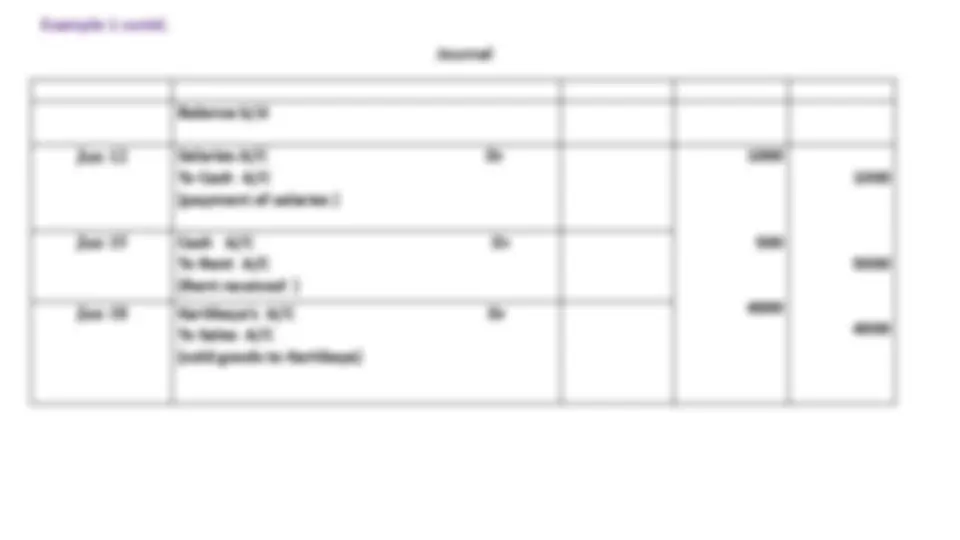

Balance b/d Jan 12 Salaries A/C^ Dr To Cash A/C (payment of salaries )

Jan 15 Cash A/C Dr To Rent A/C (Rent received ) Jan 18 Kartikeya’s A/C Dr To Sales A/C (sold goods to Kartikeya) Journal Example 1 contd.

Cash Account Dr Cr Date Particulars J.F. Amount (Rs) Date Particulars J.F. Amount (Rs) 2005 Jan Jan 15 Feb 1 To Capital A/C To Rent A/C To Balance b/d

Jan 6 Jan 9 Jan 12 Jan 31 By Navneet A/C By Furniture A/C By Salaries A/C By Balance c/d

Example 1 contd. Ledger posting from Journal Ledger

Purchase Account Dr Cr Date Particulars J.F. Amount (Rs) Date Particulars J.F. Amount (Rs) 2005 Jan 3 Feb 1 To Navneet’s A/C To Balance b/d

Jan 31 By Balance c/d 5000 5000 5000 5000 Example 1 contd.

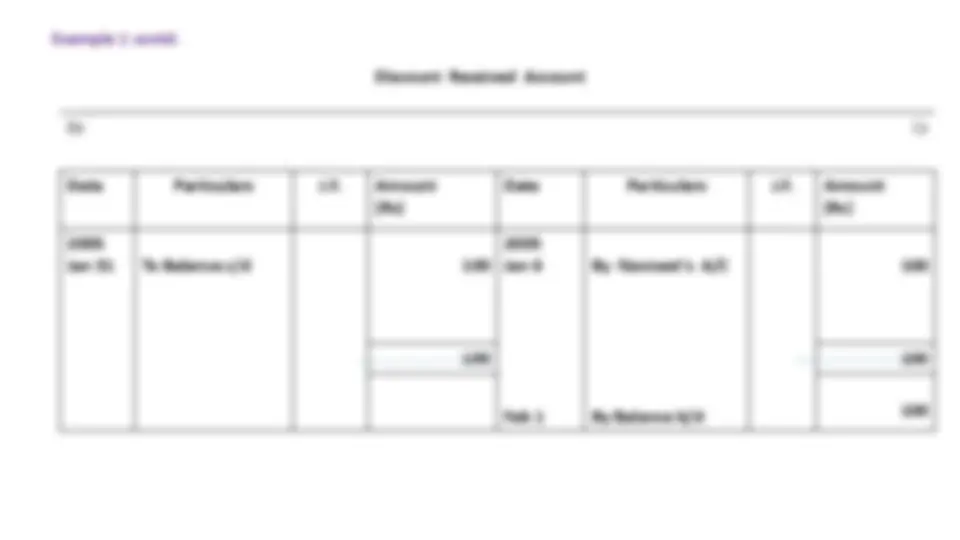

Navneet’s Account Dr Cr Date Particulars J.F . Amount (Rs) Date Particulars J.F. Amount (Rs) 2005 Jan6 To Cash A/C To Discount Received A/C

Jan 3 By Purchase A/C 5000 5000 5000 Example 1 contd.

Furniture Account Dr Cr Date Particulars J.F. Amount (Rs) Date Particulars J.F. Amount (Rs) 2005 Jan 9 Feb 1 To Cash A/C To Balance b/d

Jan 31 By balance c/d 2000 2000 2000 2000 Example 1 contd.

Salaries Account Dr Cr Date Particulars J.F. Amount (Rs) Date Particulars J.F. Amount (Rs) 2005 Jan 12 Feb 31 To Cash A/C To Balance b/d

Jan 31 By balance c/d 1000 1000 1000 1000 Example 1 contd.

Kartikeya’s Account Dr Cr Date Particulars J.F. Amount (Rs) Date Particulars J.F. Amount (Rs) 2005 Jan 18 Feb 1 To Sales A/c To Balance b/d

Jan 31 By Balance c/d 4000 4000 4000 4000 Example 1 contd.

Sales Account Dr Cr Date Particulars J.F. Amount (Rs) Date Particulars J.F. Amount (Rs) 2005 Jan 31 To Balance c/d 4000

Jan 18 Feb 1 By Kartikeya’s A/C By Balance b/d

Example 1 contd.