Uniform CPA Examination

Practice Analysis

NASBA Annual Meeting

October 2013

Colleen Conrad, CPA and Craig Mills, Ed.D.

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

The Uniform CPA Examination and its purpose to assess important knowledge and skills required for entry-level CPAs. It covers the criteria for determining exam content, skills required of entry-level CPAs, and the greatest strengths and weaknesses of recent graduates. The document also explores potential changes to the CPA Exam, including a focus on analytical and communication skills, performance testing, and new question formats.

Typology: Study Guides, Projects, Research

1 / 24

This page cannot be seen from the preview

Don't miss anything!

Purpose of the CPA Exam ! To assess important knowledge and skills required for entry- level CPAs for the protection of the public interest ! Criteria for determining knowledge/skills included on CPA Exam:

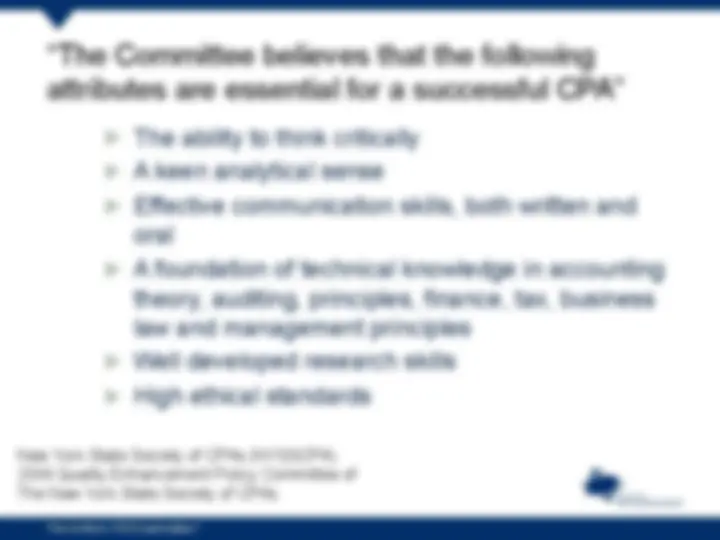

“The Committee believes that the following attributes are essential for a successful CPA”

4 New York State Society of CPAs (NYSSCPA). 2008 Quality Enhancement Policy Committee of The New York State Society of CPAs

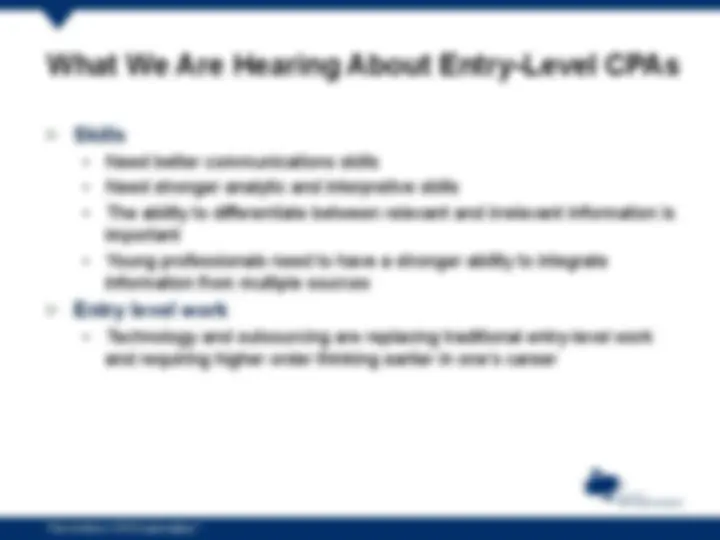

Greatest Strength/Weakness of Recent Graduates?

Valerie C. Milliron THE ACCOUNTING EDUCATORS’ JOURNAL, Volume XXII 2012 pp. 43- Report from a forum and survey sponsored by California Society of CPAs

Did you feel prepared immediately after graduation in each of the following areas: YES NO Item Description 93% 7% Ability to work in teams 92% 8% Ethical standards 87% 13% Work ethic 86% 14% Energy level 78% 22% Communication skills 75% 25% Information technology skills 67% 33% Analytical thinking 58% 42% Global cultural awareness 57% 43% Technical accounting knowledge Valerie C. Milliron THE ACCOUNTING EDUCATORS’ JOURNAL Volume XXII 2012 pp. 43- Report from a forum and survey sponsored by California Society of CPAs

What Does This Make Us Think?

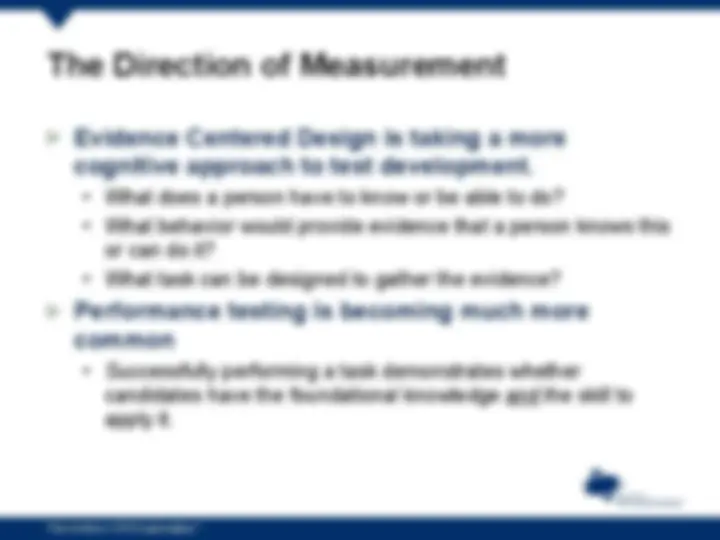

The Direction of Measurement

New Question Formats ! AICPA is researching new question formats

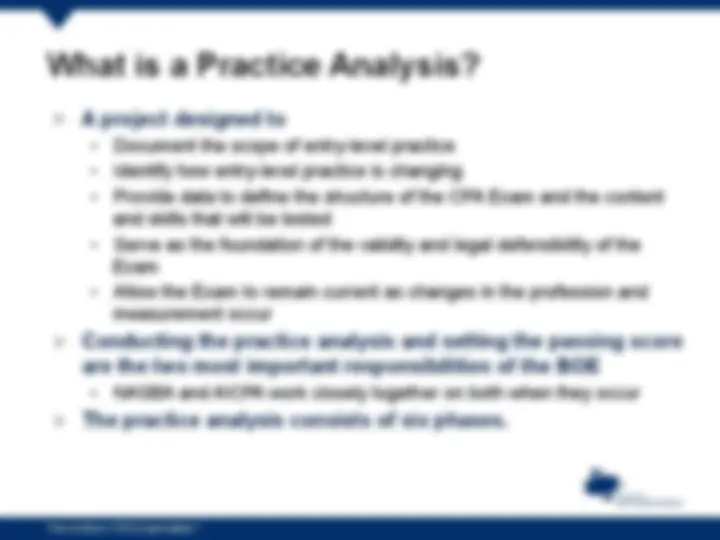

What is a Practice Analysis? ! A project designed to

Phases of the Practice Analysis

v Interviews, focus groups, and other activities ü Understand activities performed by entry-level CPAs ü Identify skills required to perform the activities ü Learn which skills are increasing and decreasing in importance ü Provide data to define the subset of skills to be tested

v Survey supervisors to verify the findings from Exploration v Leveraging NASBA’s ALD when possible

Phases of the Practice Analysis

v Develop Exposure Draft and invite comments

v Evaluate comments and revise design as needed

v Structure v Length v Test Specifications v (knowledge and skills to be tested) v Psychometric Model

Exploration Takes a Broad View

Public Protec5on Not Public Protec5on CPA Exam

Practice Analysis - Staff Project Team

BOE Governance ! BOE Sponsor Group