Download Unit 02 - Planning & Risk Assessment and more Study notes Auditing in PDF only on Docsity!

in l

l

int

is

nil

i's

i

i

is

n 7

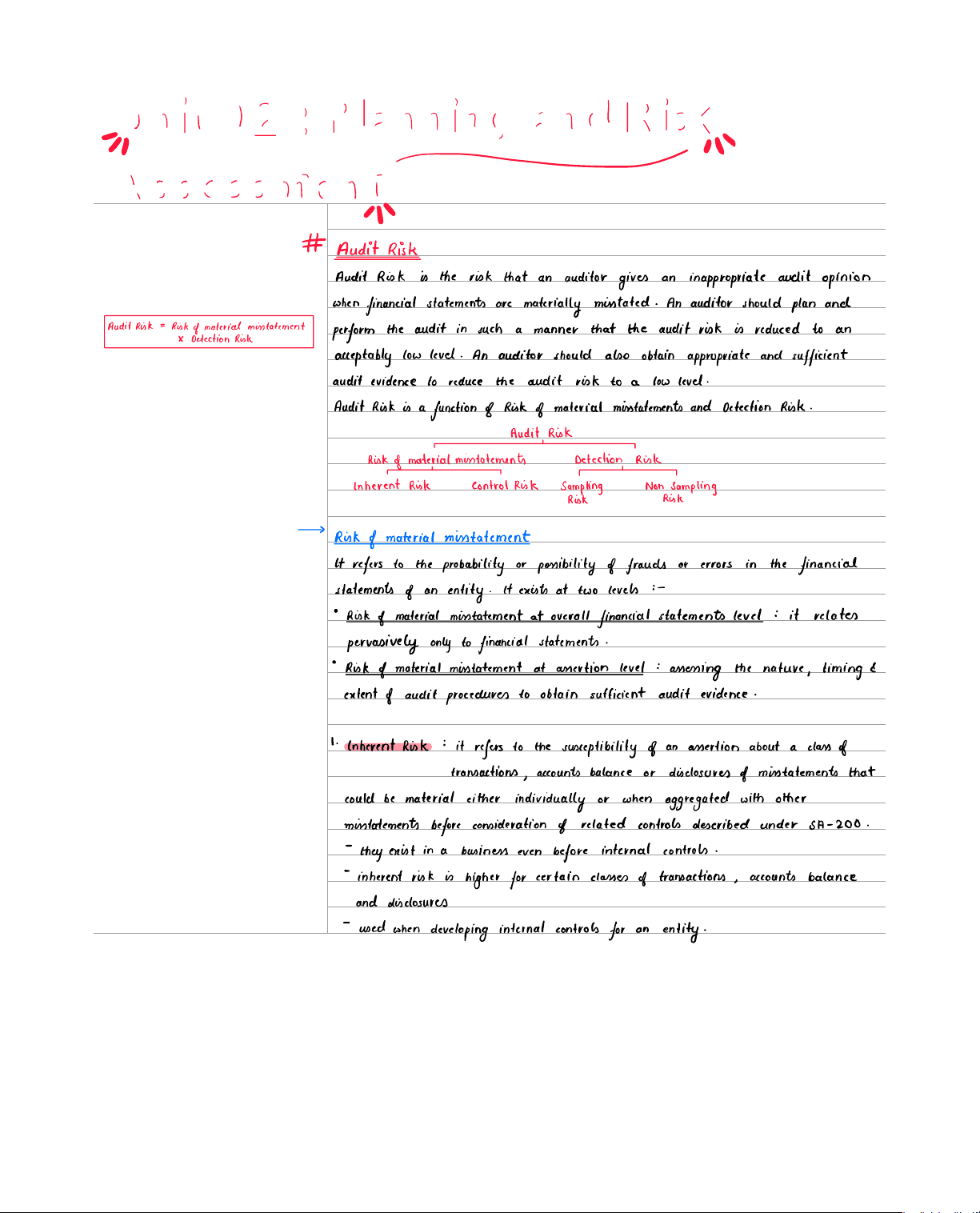

AuditRisk

AuditRisk is

the risk that an

auditor

gives

an

inappropriate audit

opinion

when

financial

statements

are materially

misstated

An

auditor

should

plan

and

perform

theaudit in

such a manner that the auditrisk is

reduced

to an

aditrisk R detection

his

tatement

acceptably low

level

An

auditor

should

also

obtain appropriate and sufficient

audit

evidence

to

reduce the audit risk to

a low

level

AuditRisk is a function

of

Risk

of

material

misstatements

and

Detection

Risk

Audit Risk

Risk

of

material

misstatements Detection

Risk

inherent Risk

control

Risk

sampling Nonp ampling

Risk

of

materialmisstatement

Itrefers to theprobability

or possibility

of

frauds

or errors in the financial

statements

of

an

entity

It

exists

at two

levels

Risk

of

material

misstatement

at

overall financial

statements

level it

relates

pervasively only

to financial

statements

Risk

of

material

misstatement

at

assertion level assessing the

nature

timing

extent

of

auditprocedures

to

obtainsufficient audit

evidence

1

Inherent

Risk it refers to the susceptibility

of

an

assertion about a

class

of

transactions accountsbalance

or

disclosures

of

mintatements

tha

could be

material either

individually

or when aggregated

with

other

mintatements

before

consideration

of

related controls described under

SA

they

exist in

a

business

even before

internal controls

inherent

risk is

higher

for

certain

classes

of

transactions accounts

balance

and

disclosures

used when developing

internal controls

for

an

entity

Control Risk it istherisk

of

misstatement

in an

assertion about

a

class

of

transactions accounts balance or

disclosures

on

misstatements

thatcouldbe

material either

individually

or when aggregated with

other

misstatements

that

cannot be

prevented

detected

or

controlled

on a

timely

manner

by

an entity's

internal

controls

risks not

controllable

by

internalcontrols

In

intis

I

infioiiii.tk

internalcontrols

are inversely

related

to

control risk

Detection

Risk

It refersto

a risk

where the audit procedures performed

by

an auditor

t

reduce

theaudit risk to a considerably

low

level are

unable to

detect a

misstatement

that

exists could be

material either

individually

or as an

aggregate

withother

misstatements

Detection

Risk can be

reduced

by

increasing

area

of

checking

larger

samples

and competent experienced personnel on the

engagementteam

SamplingRisk

occurs when a sample is

not

representative

of

a population and

thus

leading

to

wrong

audit

conclusions

Non Sampling

Risk auditor

reaches

an

erroneous

conclusion

not

related to

sampling

riskbutdueto application

of

inappropriate audit

procedures

Risk

Assessment Procedures

Risk

assessment

forms

the

basis

for

the identification and

assessment

of

risks

of

mater

mintatements

at

a financial

statement

and

assertion level It

involves

all

those audi

procedures employed in

order to

understand

the entity

its

environment internal

controls

andrisks

of

material

misstatements

arising

dueto frauds

orerrors at

a

financial

statement

and

assertion level

Risk

Assessment Procedures

involve

Frauds in

Audit

v

v

EradulentFinancial

Reporting

Misappropriation

of

Assets

understanding

the

entity

and its

environment

Understanding the entity

andits

environment

helps in the identification and

assessment

of

therisks

of

material

misstatements

faced

by

an

entity

It

also helps in forming

a

proper

audit

plan

Understanding

factors

related

to industry

regulation

and

otherexternal

factors

an

auditormust

understand

the industry

conditions where an

entity

is

placed

including

the

competitive

environment

suppliers

customer composition andtechnological

developments

He

should

alsounderstand

theregulatory

framework

legal

political as wellas

external

factors lik

general

economicconditions interest rates inflation andavailability

of

finance

Nature

of

the

entity

operations

organisationand

governance

investments made

by

company

structure

sources

of

finance

Measurement

and

review

of

the companys

financial

performance

includes KPI's

financial

nonfinancial

ratios trends

and operating

statistics

credit

ratingagency

reports

periodonperiod financial

performance analysis

budgeting forecasting

variance

analysis

anddepartmentlevelperformance reports

Selection

and

application

of

accounting policiesand

reasons

for

changes

thereon

evaluate

and

assess

whether

the accounting

policies adopted

by

theentityare

suitable

appropriate

consistent

and

applicable as

per

the legalregulatory

frameworkand

industry

accounting policies

An

entity

objectives strategies and

business

risk

all

the plansand

decisions

made

by

an entity

are

based

on

its

overallobjectives

as

decid

by

the

management Strategies areformulated

by

the entity

in

order to

attainthese objectives

An

understanding

of

the

various

business risks

faced

by

an entity in

its industry helps in

identification and

assessment

of

possible

risksdue to

material

mintatements

at a finance

statement and

assertion level

Materiality

inAudit

Materiality

in

auditstates that

mintatements

including

omissions

are

considered material

if

they

individuallyor

in aggregate reasonably

influencethe

economicdecisions

of

userstaken on

the

basis

of

thefinancial

statements

Judgements

about materiality are

made on the

basis

of

thesurrounding

circumstances affecte

by

size and

nature

of

mintatement

While

planning

the

audit the

auditormakes judgements regardingthesize

of

mintatements

to b

considered material

These judgements

form

the

basis

for

determining

nature

timing

extent

of

risk

assessment

procedures

identifying assessing

risk

of

material

misstatements

determining nature timing

extent

of

further

analytical

procedures

Determination

of

Materiality

Theauditor

hasto apply

his

professional

judgement

in determining materialityand

choos

Planning an

audit

involves

analyticalprocedures

to be applied

determination

of

materiality

involvement

of

experts

generalregulatoryframework governing

the industry

other risk

assessment

procedures

Need

for

Planning

an Audit

performing the

assurance engagement

in a

proper

manner

ensuring

compliance with

professional standards as well as regulatory laws

effectively conducting theaudit

of

an entity

in a

timely

manner

identifying the right

engagement team

based

on

competency expertise

reducing the

auditrisk to

a considerably

lowlevel enhancing quality

of

aud

identifying concerns and how to

address

them

identifying areasthat require greater

attention

and

detail

Planning

Process

Preliminary engagement

activities

applying analytical

procedures

to

assess the

continuance

of

engagement

with a

client

selection

evaluation

ensuring

the compliance

with

ethical requirements

of

independence

clearly

understanding the

terms

of

the engagement to

avoid misunderstandings

2

Planning

Activities

identifying the

overall scope

of

the

responsible

party

ascertaining the reporting

objectives

of

the

entity

bits

ns n m

hitement

I

considering

based

on the

auditors professional judgement changes

that

may

be

ofconcern to the

audit engagementteam

reporting

industry general

changes

identifying the

nature

timing

extent

of

resources required to

carry

out the

engagement

effectively

consider results

of

preliminary engagement

activities

and

k

p

professional

Audit

strategy

Vs Audit

Plan

Audit strategy

Audit Plan

sets the

overall objective

of

the

audit

addresses variousmatters

identified in th

audit strategy

less

detailed

than

audit

plan

more

detailed thanaudit

strategy

determines

scope timing

direction

of

audit

howaudit

strategy

should

be

implemente

Closely

interrelated since

changes

in one

may

leadto

consequential

changes

in

the

other

Audit Programmes

Auditprogrammes are basically

verification procedures applied to financial

statemen

or

accounts

of

a

givenentity for

thepurpose

of

obtaining

sufficient audit

evidence

to

support the informed

opinion

of

an auditor

construction

of

an audit programme

involves

staying

within

thescope

of

theaudit

prepare

a

written audit

programme

determine reasonablybestevidence

available

include

audit

objectives

for

each area

consider

all

possibilities

of

errors

coordinate procedures to be

applied to

related items

more thanoneauditperiod It

includes information thatdoes not change

frequently

andis

relevant

for

continuous

future

audits It

contains

long

term information

abou

the

client

Contents

of

Permanent

AuditFile

include

Accounting policies

internalcontrol procedures

significant

contracts

andagreements

legal

information

MOA AOA COI

organisational

structure

Previous

years

audit reports

Tan and

statutory

information

Minutes

of

Board AGMmeetings

2

current Audit

file

it

contains

all

records and

documentation

of

the audit

proced

Memorandum Audit

file

and

evidence relevant

to the

specific

year

in

which the

audit is being

conducted

It helps the

auditor in expressing

an opinion

on thefinancial

statements

It is

a

working

file

Contents

of

currentAudit

file

audit

programmes

audit

evidence

current

years

financial

statements

significantauditfindings

analytical

procedures

conclusionsreached

inquirieswith

management

checklist minutes

of

meetings

auditmethodology toolsused