Download Valuing Private Companies: Methods and Challenges and more Lecture notes Lease Finance and Investment Banking in PDF only on Docsity!

PRIVATE COMPANY VALUATION

Aswath Damodaran

Aswath Damodaran 124

Process of Valuing Private Companies

¨ The process of valuing private companies is not different from

the process of valuing public companies. You estimate cash

flows, attach a discount rate based upon the riskiness of the

cash flows and compute a present value. As with public

companies, you can either value

¤ The entire business, by discounting cash flows to the firm at the cost of

capital.

¤ The equity in the business, by discounting cashflows to equity at the

cost of equity.

¨ When valuing private companies, you face two standard

problems:

¤ There is not market value for either debt or equity

¤ The financial statements for private firms are likely to go back fewer

years, have less detail and have more holes in them.

Aswath Damodaran

125

2. Cash Flow Estimation Issues

¨ Shorter history: Private firms often have been around for

much shorter time periods than most publicly traded firms.

There is therefore less historical information available on

them.

¨ Different Accounting Standards: The accounting statements

for private firms are often based upon different accounting

standards than public firms, which operate under much

tighter constraints on what to report and when to report.

¨ Intermingling of personal and business expenses: In the case

of private firms, some personal expenses may be reported as

business expenses.

¨ Separating “Salaries” from “Dividends”: It is difficult to tell

where salaries end and dividends begin in a private firm,

since they both end up with the owner.

Aswath Damodaran

127

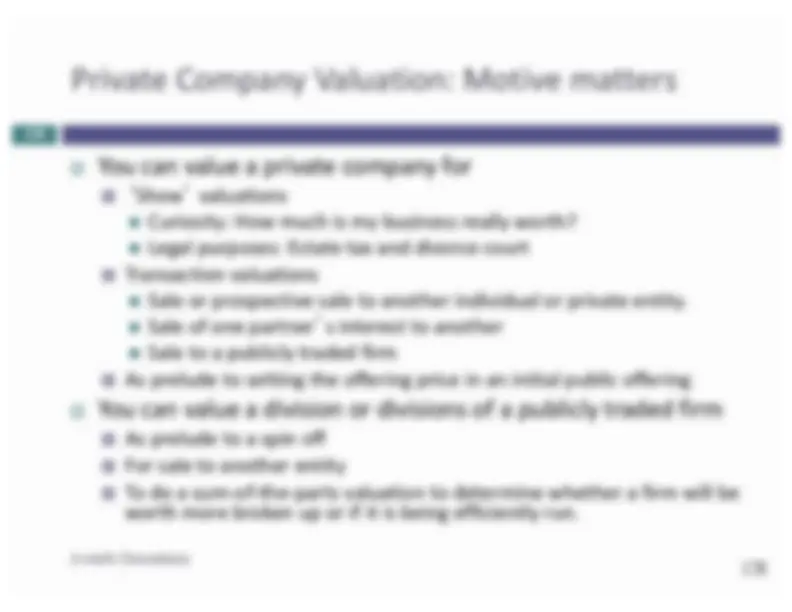

Private Company Valuation: Motive matters

¨ You can value a private company for

¤ ‘Show’ valuations

n Curiosity: How much is my business really worth?

n Legal purposes: Estate tax and divorce court

¤ Transaction valuations

n Sale or prospective sale to another individual or private entity.

n Sale of one partner’s interest to another

n Sale to a publicly traded firm

¤ As prelude to setting the offering price in an initial public offering

¨ You can value a division or divisions of a publicly traded firm

¤ As prelude to a spin off

¤ For sale to another entity

¤ To do a sum-of-the-parts valuation to determine whether a firm will be

worth more broken up or if it is being efficiently run.

Aswath Damodaran

128

I. Private to Private transaction

¨ In private to private transactions, a private business is

sold by one individual to another. There are three key

issues that we need to confront in such transactions:

¨ Neither the buyer nor the seller is diversified. Consequently, risk

and return models that focus on just the risk that cannot be

diversified away will seriously under estimate the discount rates.

¨ The investment is illiquid. Consequently, the buyer of the

business will have to factor in an “illiquidity discount” to

estimate the value of the business.

¨ Key person value: There may be a significant personal

component to the value. In other words, the revenues and

operating profit of the business reflect not just the potential of

the business but the presence of the current owner.

Aswath Damodaran

130

An example: Valuing a restaurant

¨ Assume that you have been asked to value a upscale French

restaurant for sale by the owner (who also happens to be the

chef). Both the restaurant and the chef are well regarded, and

business has been good for the last 3 years.

¨ The potential buyer is a former investment banker, who tired

of the rat race, has decide to cash out all of his savings and

use the entire amount to invest in the restaurant.

¨ You have access to the financial statements for the last 3

years for the restaurant. In the most recent year, the

restaurant reported $ 1.2 million in revenues and $ 400,

in pre-tax operating profit. While the firm has no

conventional debt outstanding, it has a lease commitment of

$120,000 each year for the next 12 years.

Aswath Damodaran

131

Step 1: Estimating discount rates

¨ Conventional risk and return models in finance are built

on the presumption that the marginal investors in the

company are diversified and that they therefore care

only about the risk that cannot be diversified. That risk is

measured with a beta or betas, usually estimated by

looking at past prices or returns.

¨ In this valuation, both assumptions are likely to be

violated:

¤ As a private business, this restaurant has no market prices or

returns to use in estimation.

¤ The buyer is not diversified. In fact, he will have his entire

wealth tied up in the restaurant after the purchase.

Aswath Damodaran

133

No market price, no problem… Use bottom-up betas

to get the unlevered beta

¨ The average unlevered beta across 75 publicly

traded restaurants in the US is 0.86.

¨ A caveat: Most of the publicly traded restaurants on

this list are fast-food chains (McDonald’s, Burger

King) or mass restaurants (Applebee’s, TGIF…) There

is an argument to be made that the beta for an

upscale restaurant is more likely to be reflect high-

end specialty retailers than it is restaurants. The

unlevered beta for 45 high-end retailers is 1.18.

Aswath Damodaran

134

Estimating a total beta

¨ To get from the market beta to the total beta, we need a

measure of how much of the risk in the firm comes from the

market and how much is firm-specific.

¨ Looking at the regressions of publicly traded firms that yield

the bottom-up beta should provide an answer.

¤ The average R-squared across the high-end retailer regressions is 25%.

¤ Since betas are based on standard deviations (rather than variances),

we will take the correlation coefficient (the square root of the R-

squared) as our measure of the proportion of the risk that is market

risk.

¨ Total Unlevered Beta

= Market Beta/ Correlation with the market

Aswath Damodaran

136

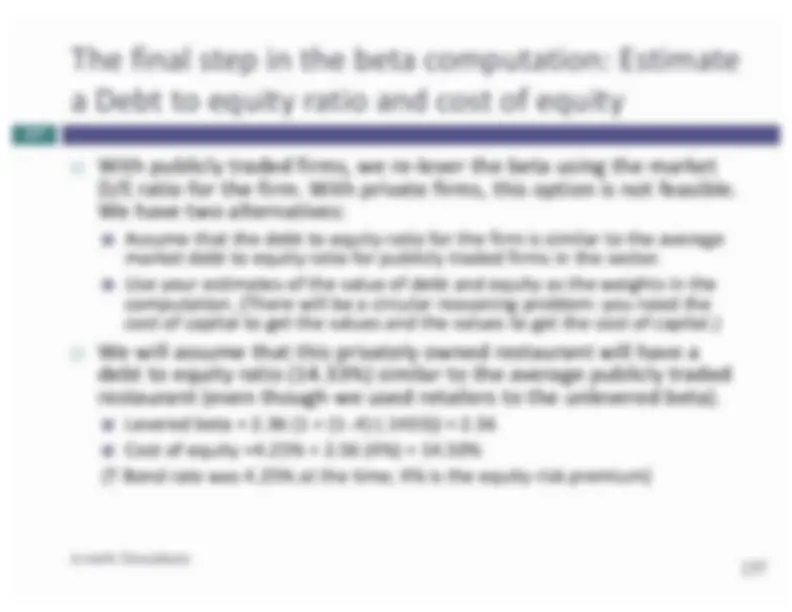

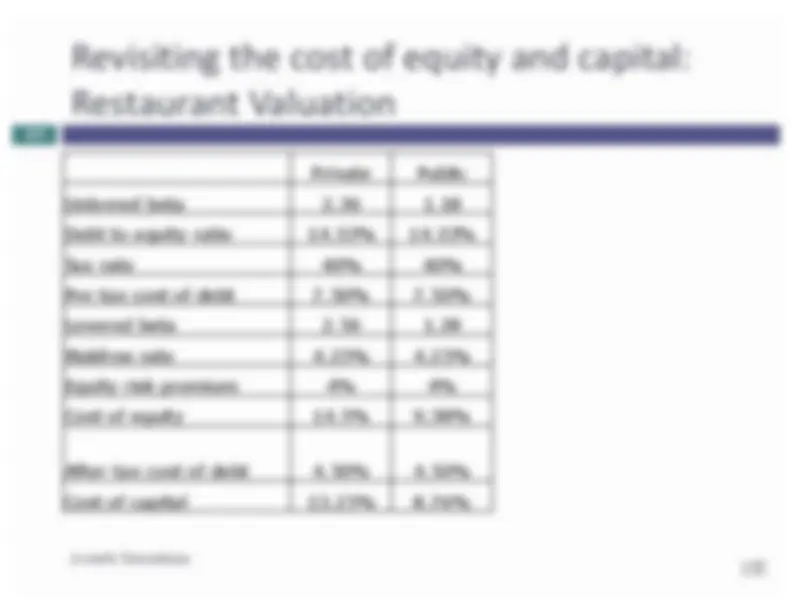

The final step in the beta computation: Estimate

a Debt to equity ratio and cost of equity

¨ With publicly traded firms, we re-lever the beta using the market D/E ratio for the firm. With private firms, this option is not feasible. We have two alternatives: ¤ Assume that the debt to equity ratio for the firm is similar to the average market debt to equity ratio for publicly traded firms in the sector. ¤ Use your estimates of the value of debt and equity as the weights in the computation. (There will be a circular reasoning problem: you need the cost of capital to get the values and the values to get the cost of capital.)

¨ We will assume that this privately owned restaurant will have a debt to equity ratio (14.33%) similar to the average publicly traded restaurant (even though we used retailers to the unlevered beta). ¤ Levered beta = 2.36 (1 + (1-.4) (.1433)) = 2. ¤ Cost of equity =4.25% + 2.56 (4%) = 14.50% (T Bond rate was 4.25% at the time; 4% is the equity risk premium)

Aswath Damodaran

137

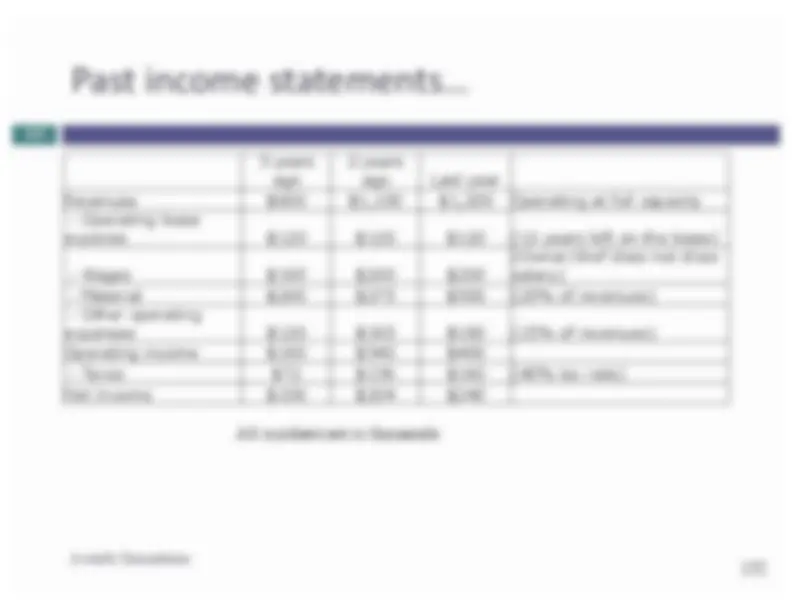

Step 2: Clean up the financial statements

Stated Adjusted Revenues $1,200 $1,

- Operating lease expenses $120 Leases are financial expenses

- Wages $200 $350! Hire a chef for $150,000/year

- Material $300 $

- Other operating expenses $180 $ Operating income $400 $

- Interest expnses $0 $69.62 7.5% of $928.23 (see below) Taxable income $400 $300.

- Taxes $160 $120. Net Income $240 $180.

Debt 0 $928.23! PV of $120 million for 12 years @7.5%

Aswath Damodaran

139

Step 3: Assess the impact of the “key” person

¨ Part of the draw of the restaurant comes from the current chef. It is possible (and probable) that if he sells and moves on, there will be a drop off in revenues. If you are buying the restaurant, you should consider this drop off when valuing the restaurant. Thus, if 20% of the patrons are drawn to the restaurant because of the chef’s reputation, the expected operating income will be lower if the chef leaves.

¤ Adjusted operating income (existing chef) = $ 370,

¤ Operating income (adjusted for chef departure) = $296,

¨ As the owner/chef of the restaurant, what might you be able to do to mitigate this loss in value?

Aswath Damodaran

140

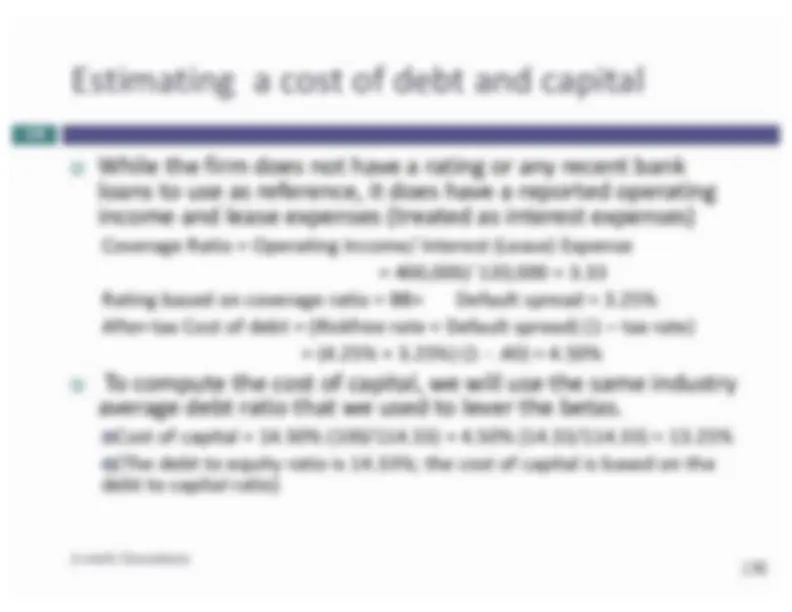

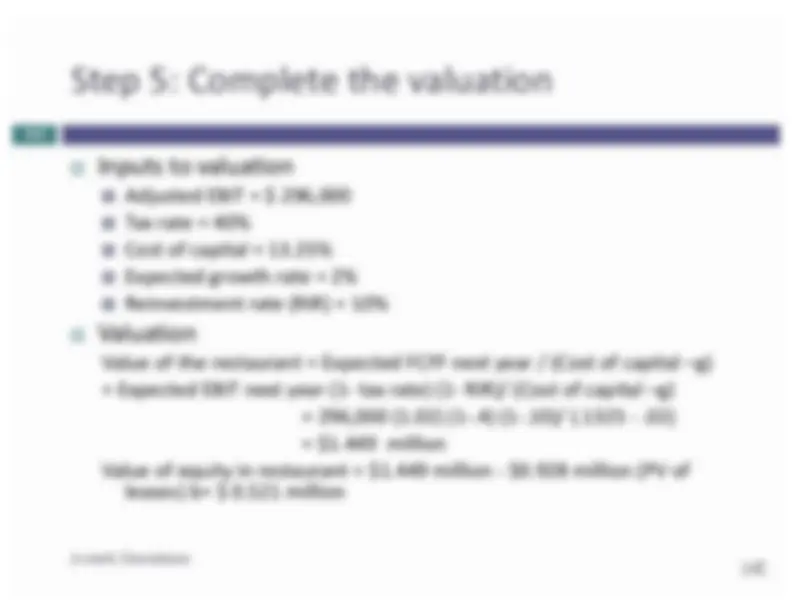

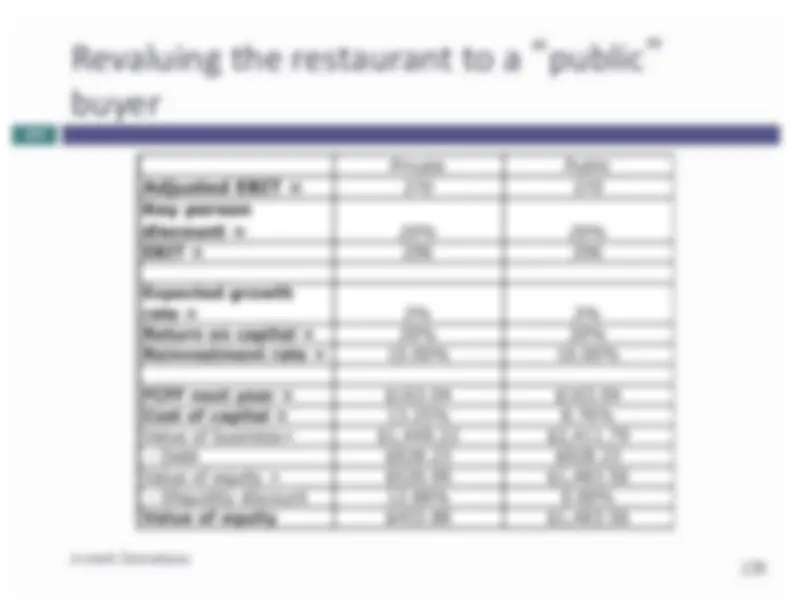

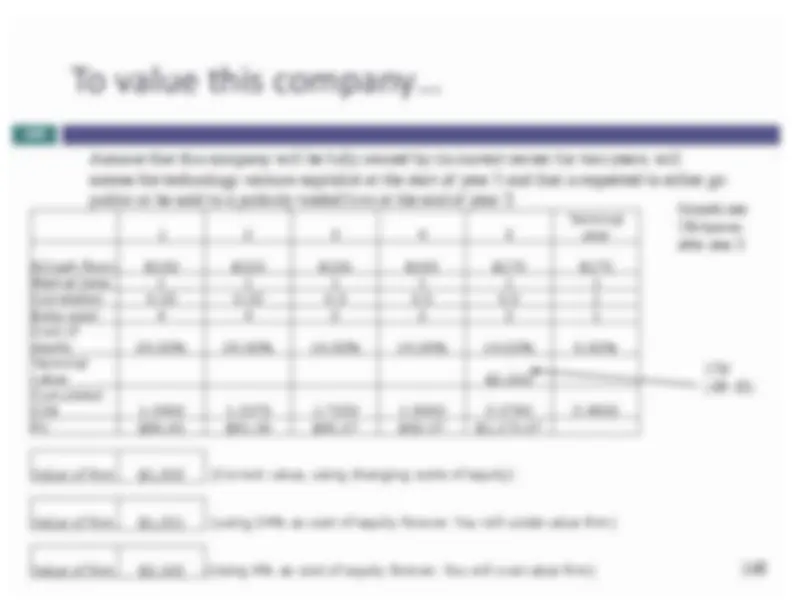

Step 5: Complete the valuation

¨ Inputs to valuation

¤ Adjusted EBIT = $ 296,

¤ Tax rate = 40%

¤ Cost of capital = 13.25%

¤ Expected growth rate = 2%

¤ Reinvestment rate (RIR) = 10%

¨ Valuation

Value of the restaurant = Expected FCFF next year / (Cost of capital –g)

= Expected EBIT next year (1- tax rate) (1- RIR)/ (Cost of capital –g)

= $1.449 million

Value of equity in restaurant = $1.449 million - $0.928 million (PV of

leases) b= $ 0.521 million

Aswath Damodaran

142

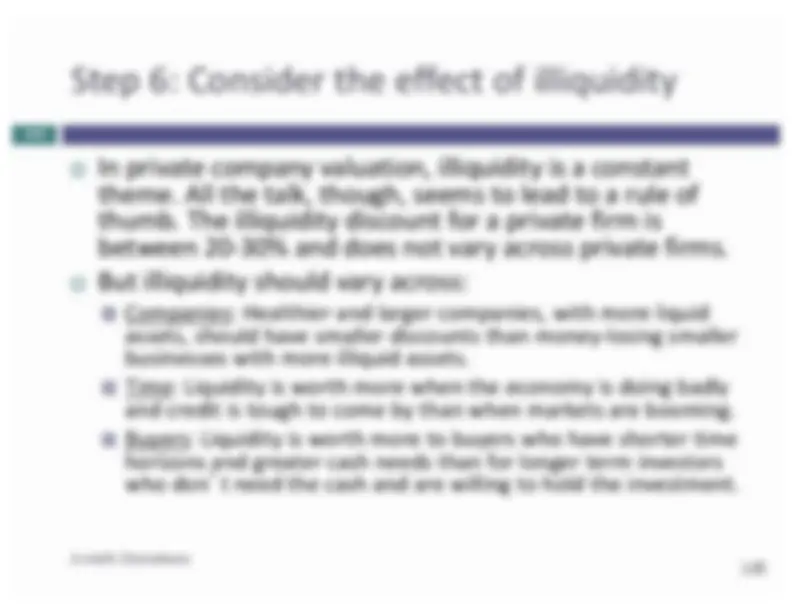

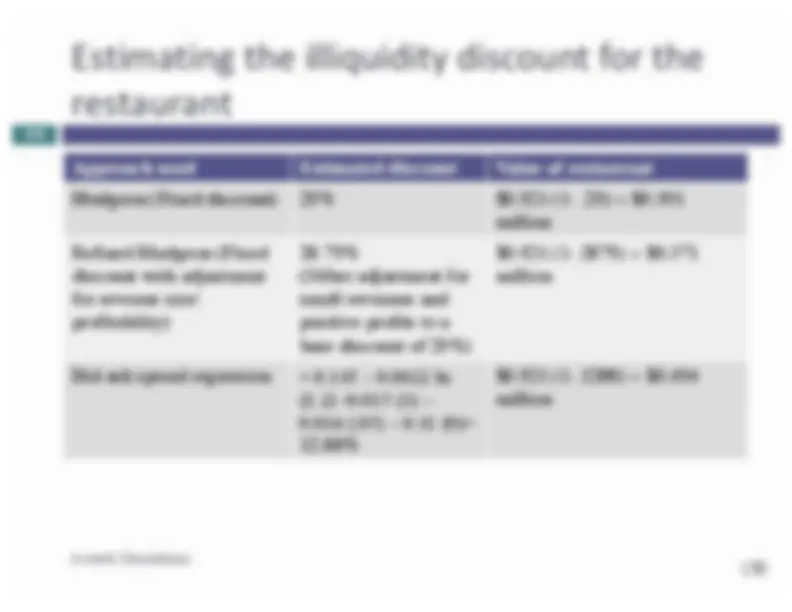

Step 6: Consider the effect of illiquidity

¨ In private company valuation, illiquidity is a constant

theme. All the talk, though, seems to lead to a rule of

thumb. The illiquidity discount for a private firm is

between 20-30% and does not vary across private firms.

¨ But illiquidity should vary across:

¤ Companies: Healthier and larger companies, with more liquid

assets, should have smaller discounts than money-losing smaller

businesses with more illiquid assets.

¤ Time: Liquidity is worth more when the economy is doing badly

and credit is tough to come by than when markets are booming.

¤ Buyers: Liquidity is worth more to buyers who have shorter time

horizons and greater cash needs than for longer term investors

who don’t need the cash and are willing to hold the investment.

Aswath Damodaran

143