¡Descarga Quantitative Tactical Asset Allocation: Enhancing Returns with Market Timing y más Apuntes en PDF de Finanzas solo en Docsity!

Electronic copy available at: http://ssrn.com/abstract=

A Quantitative Approach to Tactical Asset Allocation

Mebane T. Faber

May 2006, Working Paper

Spring 2007, The Journal of Wealth Management

February 2009, Update

ABSTRACT

The purpose of this paper is to present a simple quantitative method that improves the risk-adjusted returns across various asset classes. A simple moving average timing model is tested since 1900 on the United States equity market before testing since 1973 on other diverse and publicly traded asset class indices, including the Morgan Stanley Capital International EAFE Index (MSCI EAFE), Goldman Sachs Commodity Index (GSCI), National Association of Real Estate Investment Trusts Index (NAREIT), and United States government 10-year Treasury bonds. The approach is then examined in a tactical asset allocation framework where the empirical results are equity-like returns with bond-like volatility and drawdown.

Mebane T. Faber Cambria Investment Management, Inc.2321 Rosecrans Ave., Suite 4270 El Segundo, CA 90245 310-220- E-mail: [email protected] www.cambriainvestments.com www.mebanefaber.com

Electronic copy available at: http://ssrn.com/abstract=

Updates included in the 2009 paper:

- Results are extended out-of-sample to include the years 2006, 2007, and 2008.

- Results begin in 1973 instead of 1972 to accommodate longer moving averages.

- Sharpe calculations are corrected (T-bill returns over time period vs. static figure).

- Additional commentary and statistics are included.

- Volatility figures now use the annualized standard deviation of monthly returns.

Modern portfolio theory holds that there is a tradeoff for investing in assets – you get paid to assume risk. Exhibit 1 shows the five asset classes we will examine in this paper: U.S. stocks (S&P 500), foreign stocks (MSCI EAFE), commodities (GSCI), REITs (NAREIT), United States government 10-year Treasury bonds (10 YR), and their returns since 1973. While they took different routes to get there, most of the asset classes finished with similar returns over the time period. The exception was bonds, which trailed the other asset classes, an outcome that is to be expected due to their lower volatility and risk. The fact that bonds were even close in absolute performance to the other equity-like asset classes reflects the greater-than-twenty-year bull market that took yields from double-digit levels to near zero today.

Exhibit 1 - Asset Class Returns 1973-2008, log scale

Source: Data sources are cited at the end of the article.

Exhibit 2 shows that, while these are some pretty nice returns, they are coupled with some large drawdowns. With the exception of U.S. government bonds, which declined almost 20% the other four asset classes had drawdowns around 40% to 60%. If an investor were to take the data back further, those drawdowns only get bigger^3.

Exhibit 2 - Asset Class Maximum Drawdowns 1973-

To give the reader a visual perspective of drawdowns, Exhibit 3 shows the drawdowns for stocks for the past 108 years. Drawdowns of 10%-20% are fairly frequent, with 30%- 40% drawdowns less so. The large 1920s bear market dominates the figure with a drawdown over 80%.

Exhibit 3 – S&P 500 Drawdowns, 1900-

(^3) Higher resolution daily data and longer lookback periods can only increase the drawdown amount.

- Simple, purely mechanical logic.

- The same model and parameters for every asset class.

- Price-based only.

Moving-average-based trading systems are the simplest and most popular trend-following systems^5. For those unfamiliar with moving averages, they are a way to reduce noise. The example below shows the S&P 500 with a 10-month simple moving average.

Exhibit 4 – S&P 500 vs. 10-Month Simple Moving Average, 1990-

The most often cited long-term measure of trend in the technical analysis community is the 200-day simple moving average (SMA). In his book Stocks for the Long Run , Jeremy Siegel (2008) investigates the use of the 200-day SMA in timing the Dow Jones

(^5) Taylor and Allen (1992) and Lui and Mole (1998).

Industrial Average (DJIA) from 1886 to 2006. His test bought the DJIA when it closed at least 1 percent above the 200-day moving average, and sold the DJIA and invested in Treasury bills when it closed at least 1 percent below the 200-day moving average.

He concludes that market timing improves the absolute and risk-adjusted returns over buying and holding the DJIA. Likewise, when all transaction costs are included (taxes, bid-ask spreads, commissions), the risk-adjusted returns are still higher when employing market timing, though timing falls short on an absolute return measure. Had the results included 2008 they would favor timing even more.

When applied to the Nasdaq Composite Index since 1972, the market timing system thoroughly outperforms buy-and hold, both on an absolute and risk-adjusted basis. Siegel finds that the timing model outperforms buy and hold by over 4% per year from 1972- 2006 even when accounting for all costs, and with 25% less volatility. Unfortunately, Siegel does not report drawdown figures, which would have further demonstrated the superiority of the timing model. (Note: Siegel’s system is twice as active as the system presented in this paper, thus increasing the transaction costs).

Because we are privy to Siegel’s results before conducting the test, this query should be seen as in-sample. It is possible that Siegel already optimized the moving average by looking back over the period in which it is then tested. To alleviate fears of data-mining, the approach will be applied out-of-sample to four other markets to test for validity.

solution improved compounded returns while reducing risk^7 , all while being invested in the market approximately 70% of the time and making less than one round-trip trade per year.

Exhibit 5: S&P 500 Total Returns vs. Timing Total Returns (1900-2008)

The timing system achieves these superior results while underperforming the index in roughly half of all years since 1900. One of the reasons for the overall outperformance is the lower volatility of the timing system. It is an established fact that high volatility diminishes compound returns. This principle can be illustrated by comparing average returns with compounded returns (the returns an investor would actually realize.) The average return for the S&P 500 since 1900 was 11.20%, while timing the S&P 500 returned 11.49%. However, the compounded returns for the two are 9.21% and 10.45%, respectively. Notice that the buy and hold crowd takes a hit of 199 basis points from the effects of volatility, while timing suffers a smaller decline of 104 basis points. Ed Easterling (2006) has a good discussion of these “volatility gremlins” in John Mauldin’s Book, Just One Thing.

(^7) Volatility is measured as the annualized standard deviation of monthly returns.

Exhibit 6 (logarithmic scale) shows the superiority of the timing model over the past century, largely avoiding the significant bear markets of the 1930s and 2000s. Timing would not have left the investor completely unscathed from the late 1920s early 1930s bear market, but it would have reduced the drawdown from a catastrophic 83.66% to a more manageable 42.24%.

Exhibit 6: S&P 500 Total Returns vs. Timing Total Returns (1900-2008)

Exhibit 7 is charted on a non-log scale to detail the differences in the two equity curves. Examining the most recent 18 years, a few features of the timing model stand out. First, a trend-following model will underperform buy and hold during a roaring bull market similar to the U.S. equity markets in the 1990s. On the flip side, the timing model avoids lengthy and protracted bear markets. Consequently, the value added by timing is evident only over the course of entire business cycles.

approximately .82. This reflects the ability of the timing model to stay long in up markets while exiting the long position during down markets.

Exhibit 8: S&P 500 Ten Worst Years vs. Timing, 1900-

Exhibit 9 is the timing model excess returns over T-bills (rt - rf)^8 , versus excess returns of buy and hold over T-bills (rm – rf). Just from the graph, it can be inferred that there exists a linear relationship for positive returns, while the negative returns are much more scattered.

(^8) rt – timing return, rm – market return, rf – T-bill return.

Exhibit 9: S&P 500 Excess Returns (rm – rf) vs. Timing Excess Returns (rt-rf), 1900-

Exhibit 10 gives a good pictorial description of the results of the trend-following system applied to the S&P 500. The timing system has fewer occurrences of both large gains and large losses, with correspondingly higher occurrences of small gains and losses. Essentially, the system is a model that signals when an investor should be long a riskier asset class with potential upside, and when to be out and sitting in cash. It is this move to a lower-volatility asset class (T-bills) that drops the overall risk and drawdown of the portfolio.

OUT-OF-SAMPLE TESTING

Here we examine the results of a simple trend-following asset allocation model that follows the same timing system presented earlier. In addition to the S&P 500, four diverse asset classes were chosen, including foreign stocks (MSCI EAFE), U.S. bonds (10-year Treasuries), commodities (GSCI), and real estate (NAREIT). Exhibits 11 through 15 present the results for each asset class and the respective timing results.

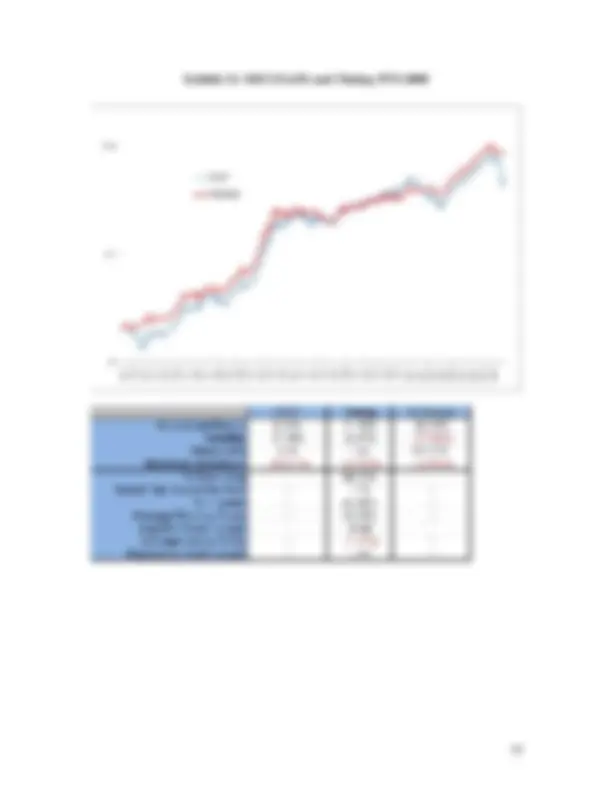

- Exhibit 11: S&P 500 and Timing 1973-

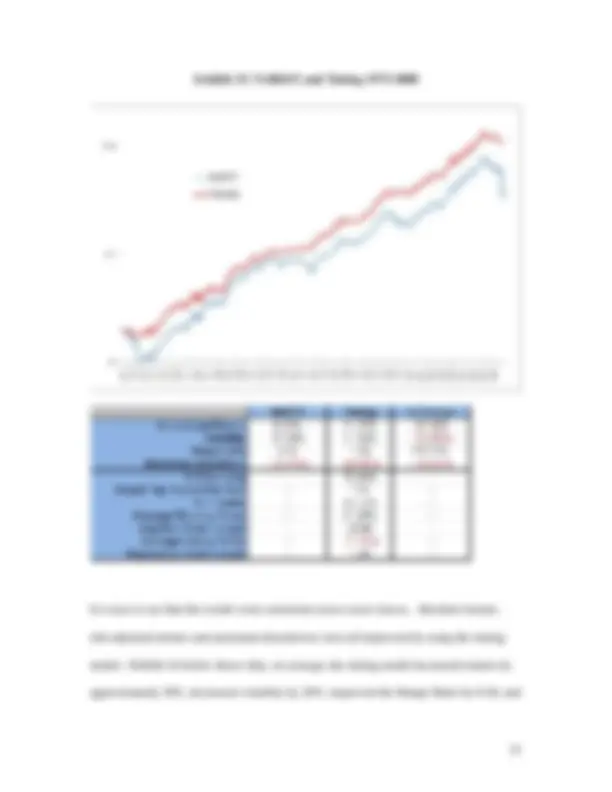

- Exhibit 12: MSCI EAFE and Timing 1973-

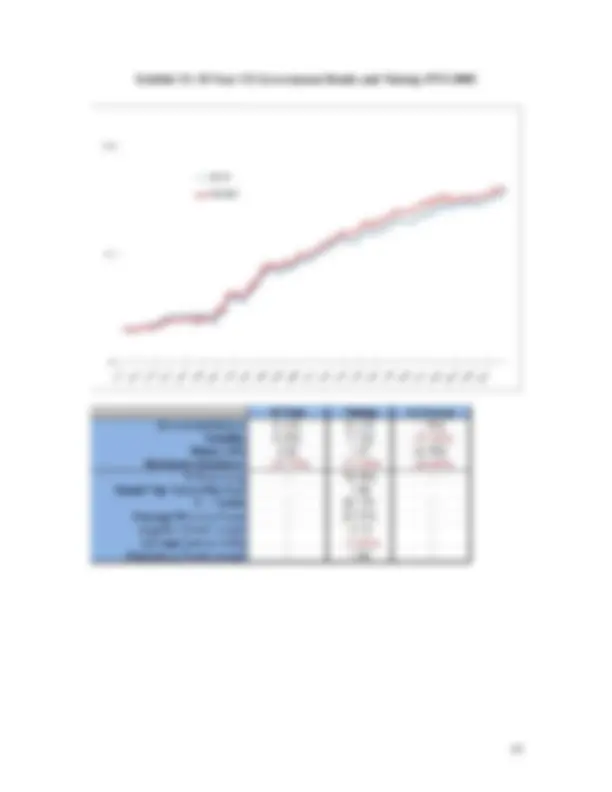

- Exhibit 13: 10 Year US Government Bonds and Timing 1973-

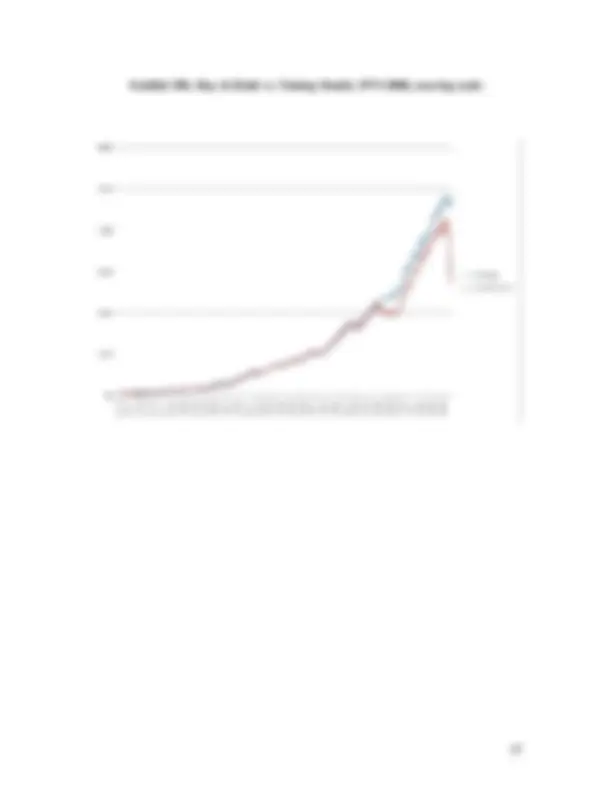

- Exhibit 14: GSCI and Timing 1973-