1

1

Introduction

Required reading:

IntroNotes.pdf

Suggested readings: Veronesi book pp.

3-7, 9-21, 32-38; Tuckman pp. 4-6, 23-25,

53-59, chapter 15

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Prepara tus exámenes

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Prepara tus exámenes con los documentos que comparten otros estudiantes como tú en Docsity

Encuentra los documentos específicos para los exámenes de tu universidad

Estudia con lecciones y exámenes resueltos basados en los programas académicos de las mejores universidades

Responde a preguntas de exámenes reales y pon a prueba tu preparación

Consigue puntos base para descargar

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Comunidad

Pide ayuda a la comunidad y resuelve tus dudas de estudio

Ebooks gratuitos

Descarga nuestras guías gratuitas sobre técnicas de estudio, métodos para controlar la ansiedad y consejos para la tesis preparadas por los tutores de Docsity

Fixed income introduction course ITAM

Tipo: Monografías, Ensayos

1 / 35

Esta página no es visible en la vista previa

¡No te pierdas las partes importantes!

Required reading:

IntroNotes.pdf

Suggested readings: Veronesi book pp.

3-7, 9-21, 32-38; Tuckman pp. 4-6, 23-25,

53-59, chapter 15

Valuing bonds and fixed income

derivatives

Managing the risk of bonds and fixed

income portfolios

Determining the optimal exercise policy

for the options that are embedded in

many fixed income securities

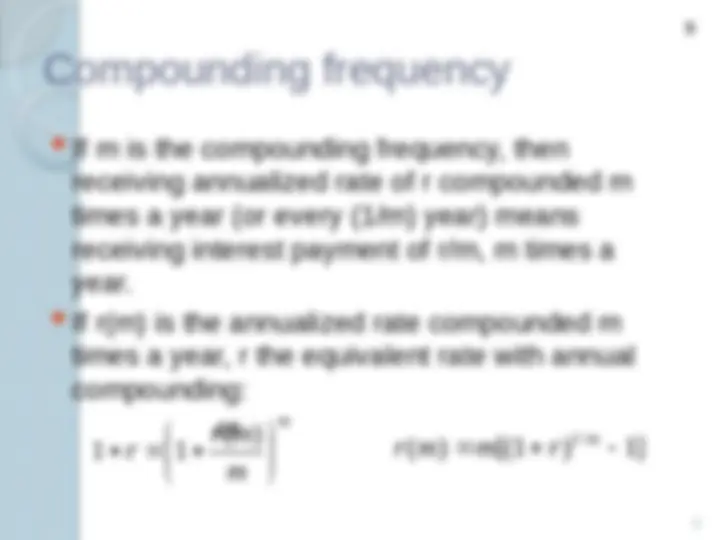

One makes one interest payment of 12%

of principal after one year (e.g. Eurobond)

One makes two coupon payments of 6%

in 6 and 12 months (e.g. corporate bond)

One makes an interest payment of 1%

every month (e.g. mortgage loan)

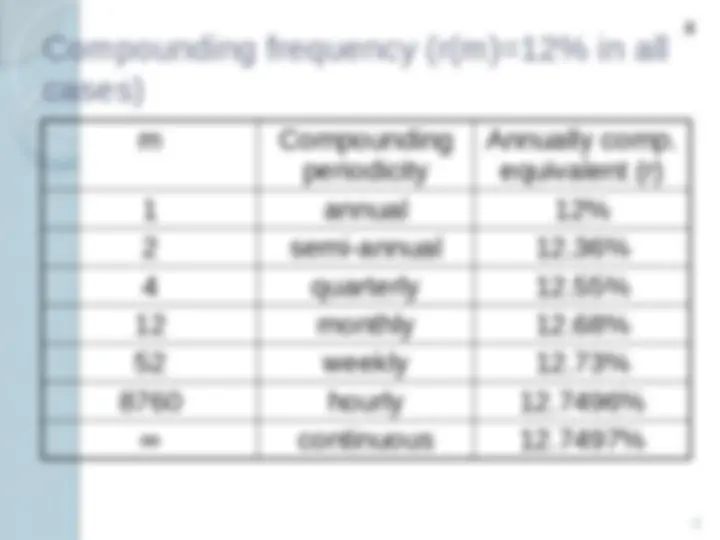

m Compounding

periodicity

Annually comp.

equivalent (r)

1 annual 12%

2 semi-annual 12.36%

4 quarterly 12.55%

12 monthly 12.68%

52 weekly 12.73%

8760 hourly 12.7496%

∞ continuous 12.7497%

In the limit, as m→∞, lim where

e≈2.

So if we define the continuously compounded

rate, r(∞), such that 1+r = e

r(∞)

, or r(∞) = ln (1+r),

where r is the annually compounded rate, we

have equivalent ways to discount a cash-flow of

K occurring at t:

(same result for all m)

r

m

r e

m

r

1 exp

mt

m

r m

r t

t r t

K

Ke

e

K

r

K

( )

( )

( )

1

( 1 )

11

1

2

1

2

1

2

1/

r

1

(∞)+r

2

(∞)

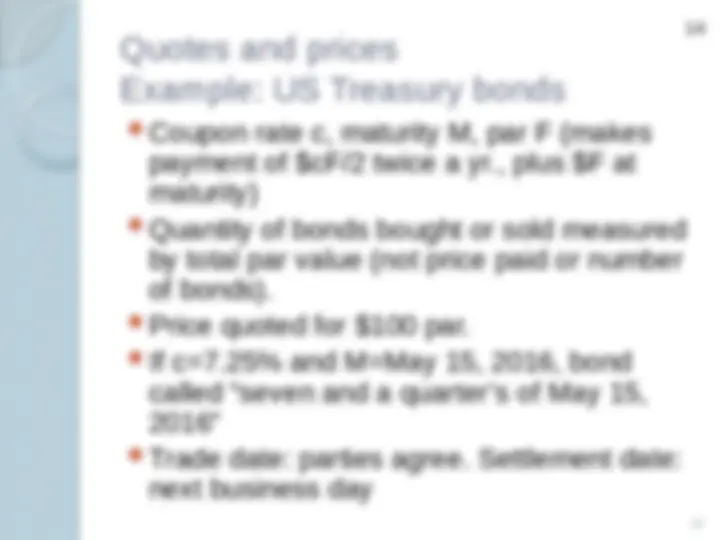

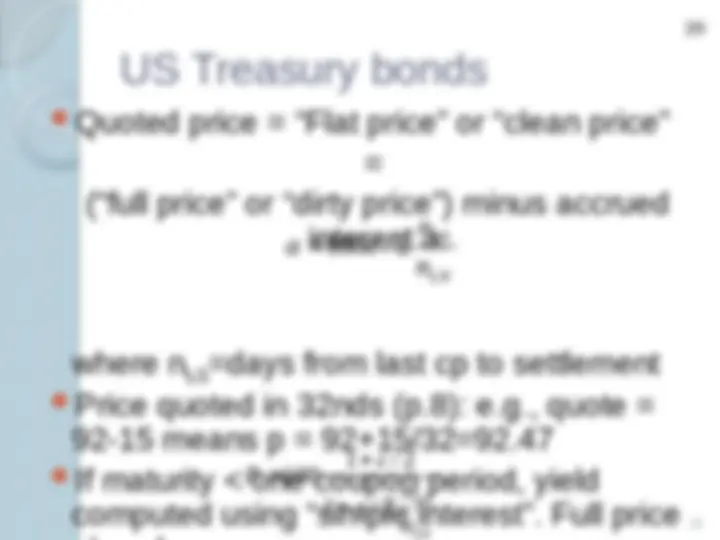

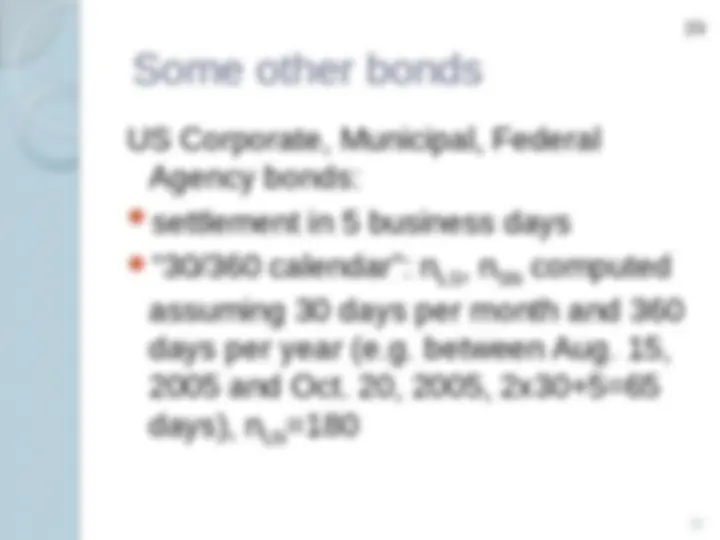

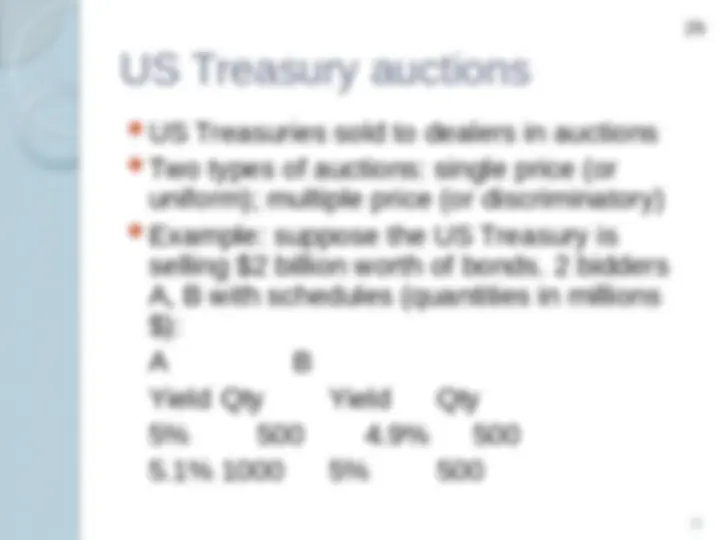

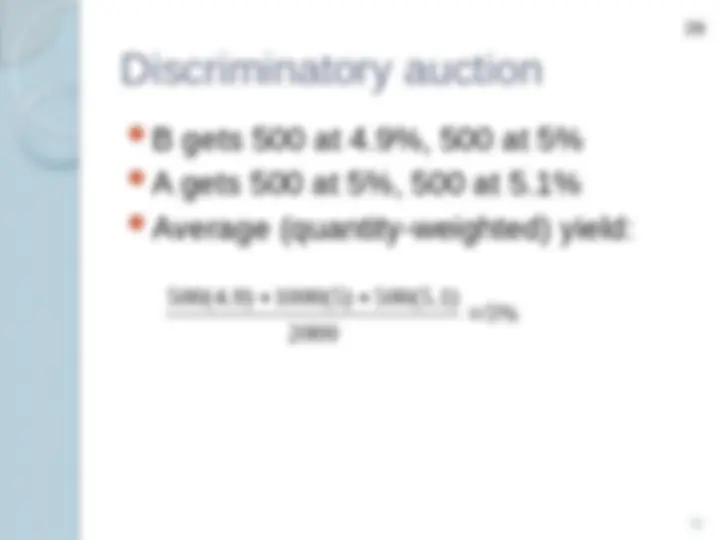

Coupon rate c, maturity M, par F (makes

payment of $cF/2 twice a yr., plus $F at

maturity)

Quantity of bonds bought or sold measured

by total par value (not price paid or number

of bonds).

Price quoted for $100 par.

If c=7.25% and M=May 15, 2016, bond

called “seven and a quarter’s of May 15,

Trade date: parties agree. Settlement date:

next business day

What is the value of the following bond:

coupon=10%, yield=5%, Time to maturity=

years, payments semi-annual, notional amount

Answer: Bond price = 152.

T T

(1 y/ 2 )

(1 y/ 2 )

y/

c/

Bond Value 100 *

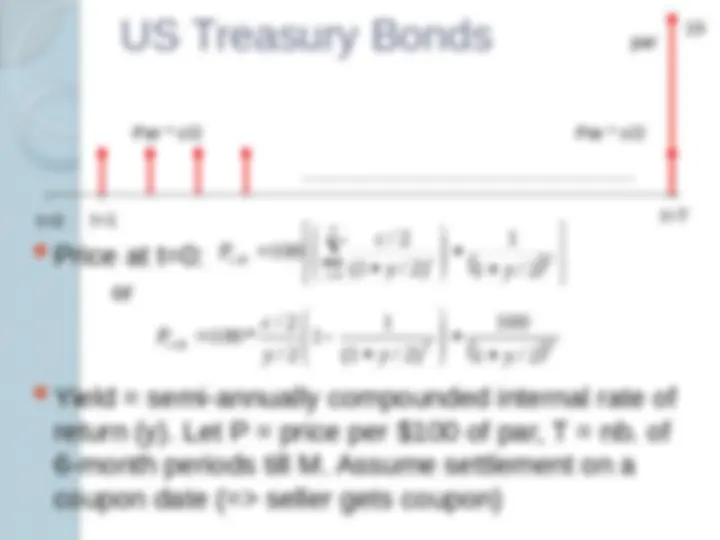

Price at t=today, where today is between

t=0 and t=1:

t=0 ( L ast) t=1 ( N ext)

c/

……………………………

t=today ( S ettlement)

nLN

nLS nSN

SN LN

LN

n LS

n

n n

t

t today t

y

P

P P y

/

1

0

( 1 / 2 )

/

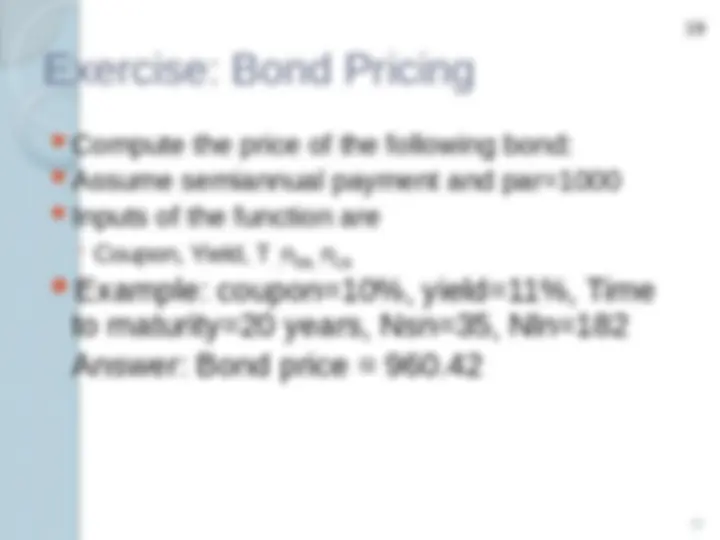

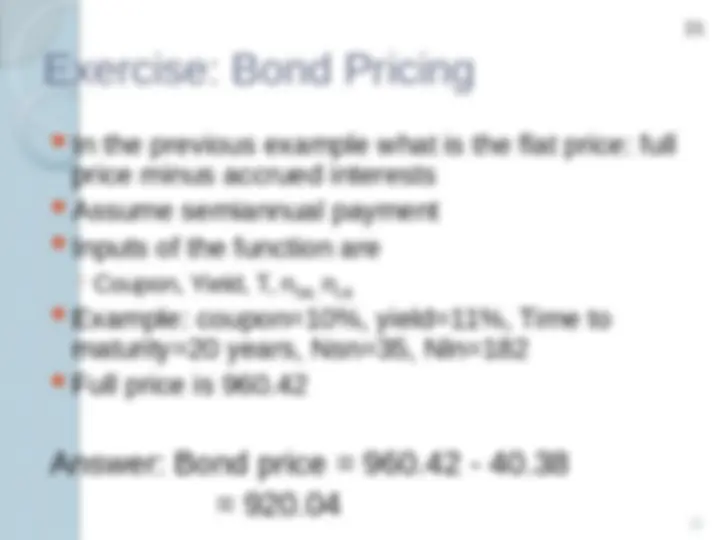

Compute the price of the following bond:

Assume semiannual payment and par=

Inputs of the function are

◦ Coupon, Yield, T

,

n

SN,

n

LN

20

LS

LN

LS

n

n

a 100 c / 2

LN

SN

n

n

y

c

P

1 / 2

1 / 2

100