1

Unit 4. Internal analysis

Subject: Strategic Management

Degree: Business Administration

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Prepara tus exámenes

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Prepara tus exámenes con los documentos que comparten otros estudiantes como tú en Docsity

Encuentra los documentos específicos para los exámenes de tu universidad

Estudia con lecciones y exámenes resueltos basados en los programas académicos de las mejores universidades

Responde a preguntas de exámenes reales y pon a prueba tu preparación

Consigue puntos base para descargar

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Comunidad

Pide ayuda a la comunidad y resuelve tus dudas de estudio

Ebooks gratuitos

Descarga nuestras guías gratuitas sobre técnicas de estudio, métodos para controlar la ansiedad y consejos para la tesis preparadas por los tutores de Docsity

Asignatura: Direcció estratègica I, Profesor: , Carrera: Administració i Direcció d'Empreses, Universidad: UV

Tipo: Apuntes

1 / 42

Esta página no es visible en la vista previa

¡No te pierdas las partes importantes!

Unit 4. Internal analysis

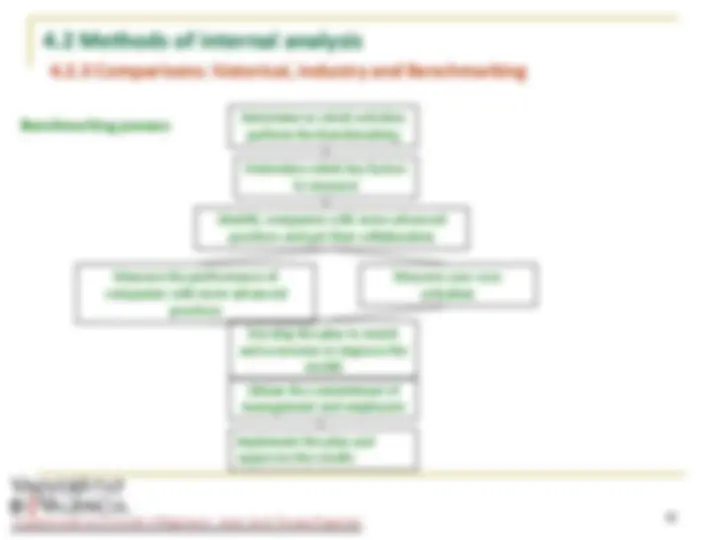

INDEX 4.1 Resources, Capabilities and Competitive Advantage 4.2 Methods of internal analysis 4.2.1 Functional analysis and strategic profile. 4.2.2 Value Chain. 4.2.3 Comparisons: historical, industry and Benchmarking 4.3 External and internal analysis integration 4.3.1 SWOT analysis 4.3.2 Strategic analysis matrix BIBLIOGRAPHY Guerras, L.A. & Navas, J.E. (2007): La Dirección Estratégica de la Empresa. Teoría y Aplicaciones, Thompson-Cívitas, Madrid, 4 th^ ed. Chapter 6 and 7 Johnson, G., Scholes, K. & Whittington, R. (2006): Dirección Estratégica, Prentice Hall, Madrid, 7 th^ ed. Chapter 3.

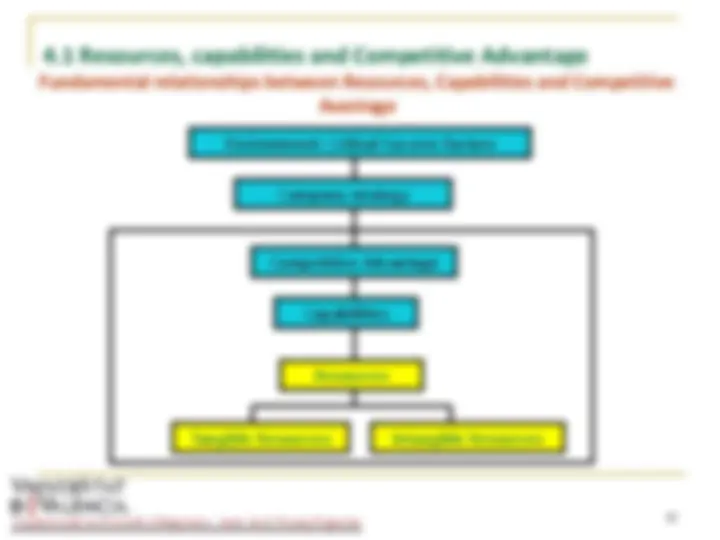

4.1 Resources, capabilities and Competitive Advantage

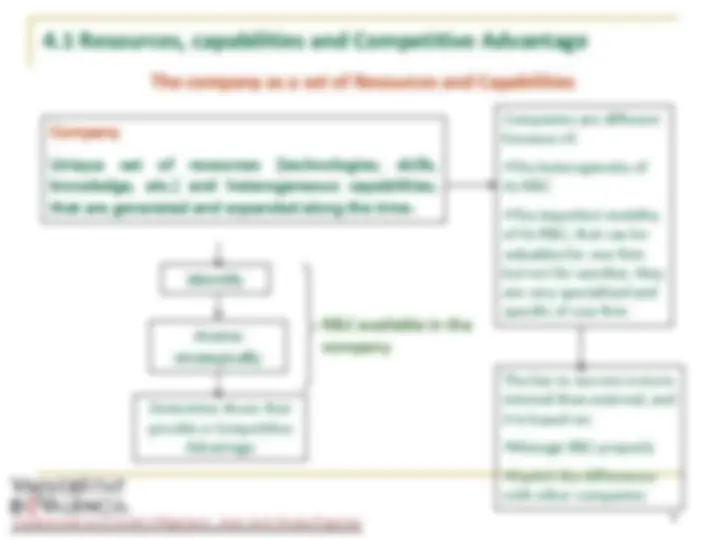

Company Unique set of resources (technologies, skills, knowledge, etc.) and heterogeneous capabilities, that are generated and expanded along the time.

Companies are different because of:

Identify

Assess strategically

Determine those that provide a Competitive Advantage

R&C available in the company The key to success is more internal than external, and it is based on:

The company as a set of Resources and Capabilities

4.1 Resources, capabilities and Competitive Advantage

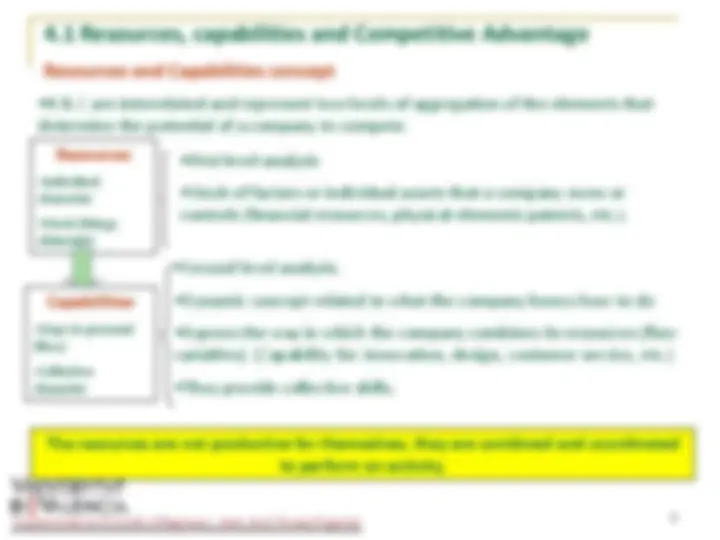

Capabilities

The resources are not productive for themselves, they are combined and coordinated to perform an activity.

Resources and Capabilities concept

4.1 Resources, capabilities and Competitive Advantage

Tangible Resources Analysis

4.1 Resources, capabilities and Competitive Advantage

Characteristics

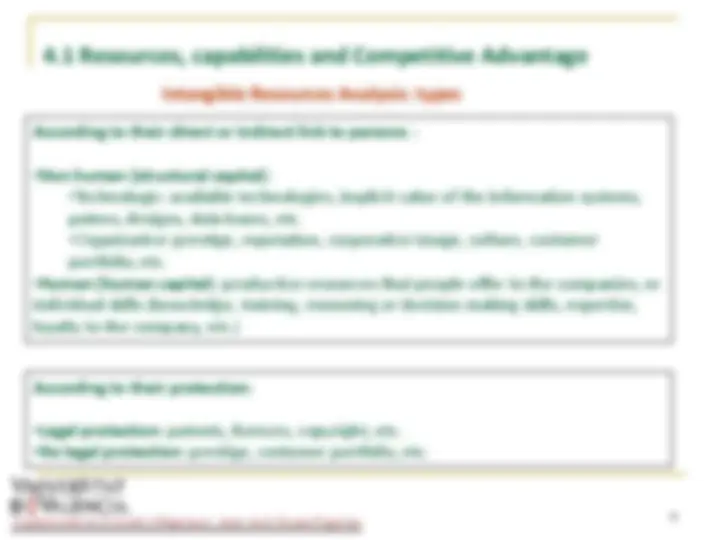

Intangible Resources Analysis

Assets difficult to identify and assess

4.1 Resources, capabilities and Competitive Advantage Capability analysis

Central or distinctive competences (core competences), are capabilities developed by a company, which allows it to perform an activity which is valuable for its costumers and other stakeholders, better than their competitors.

4.1 Resources, capabilities and Competitive Advantage Capability analysis: how resources are integrated?

Resource integration mechanisms:

Non human (financial, technologic, etc.). They are “pasive”. Human (knowledges and skills embodied by people according to their speciality). Mechanisms: Rules and guidelines (through them, specialized knowledge becomes operative practices: tasks normalization, procedure manuals, etc.) Organizational routines (models formed by a sequence of coordinated individual actions). Thus, production, sales, etc., activities are organized through a set of standardized routines. Routines are the basis for the capabilities generation Stablishing routines for the development of particular tasks is the basis for developing distinctive competences.

Most capabilities require both types of coordination mechanisms

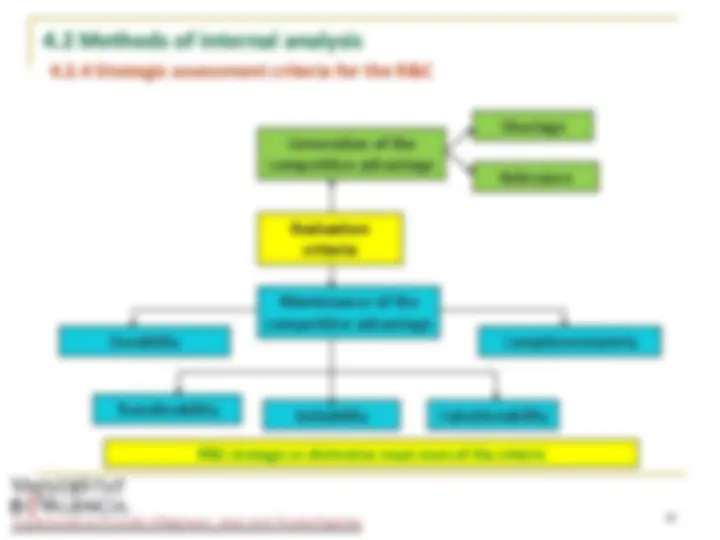

Any characteristic that a company has, and that differenciates itself from its competitors, placing it in a superior relative position to compete. Possession of a sustainable Competitive Advantage allows to get “profits” in excess of normal Without competitive advantages, companies gain only “normal profits”. The company must know what it can do well and which are the sources of competitive advantages. Competitive advantages arise from two origins: low cost position or differentiation / perceived uniqueness.

4.1 Resources, capabilities and Competitive Advantage

Competitive Advantage

4.1 Resources, capabilities and Competitive Advantage

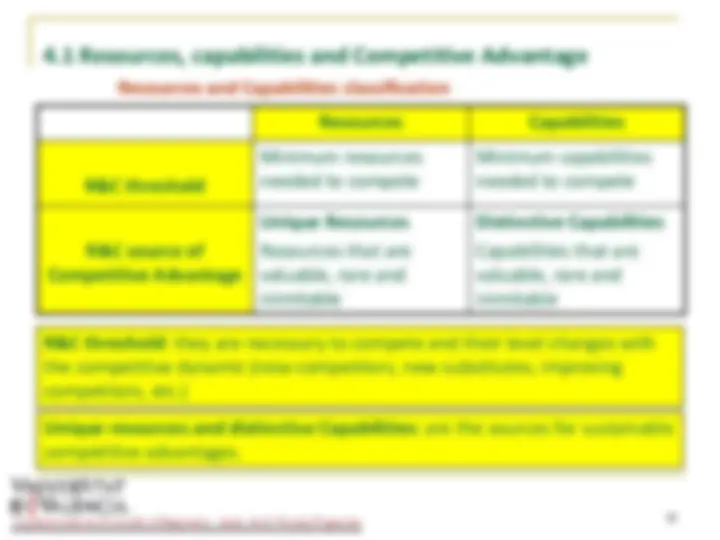

Resources Capabilities

R&C threshold

Minimum resources needed to compete

Minimum capabilities needed to compete

R&C source of Competitive Advantage

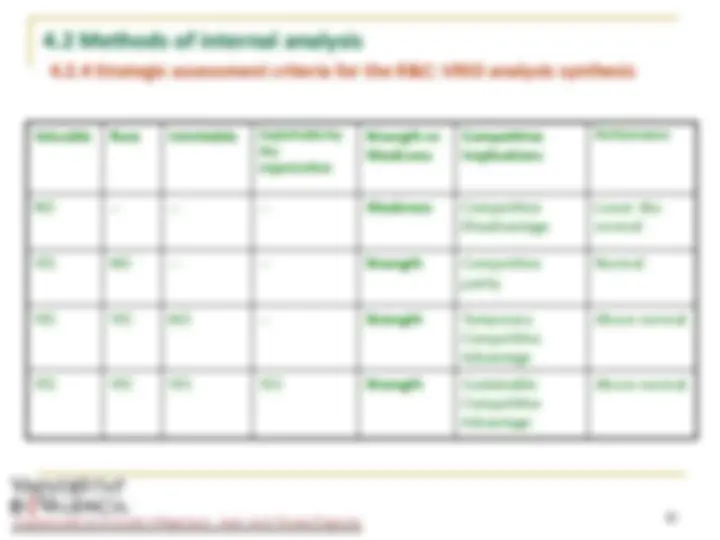

Unique Resources Resources that are valuable, rare and inimitable

Distinctive Capabilities Capabilities that are valuable, rare and inimitable

R&C threshold : they are necessary to compete and their level changes with the competitive dynamic (new competitors, new substitutes, improving competitors, etc.)

Unique resources and distinctive Capabilities: are the sources for sustainable competitive advantages.

Resources and Capabilities classification

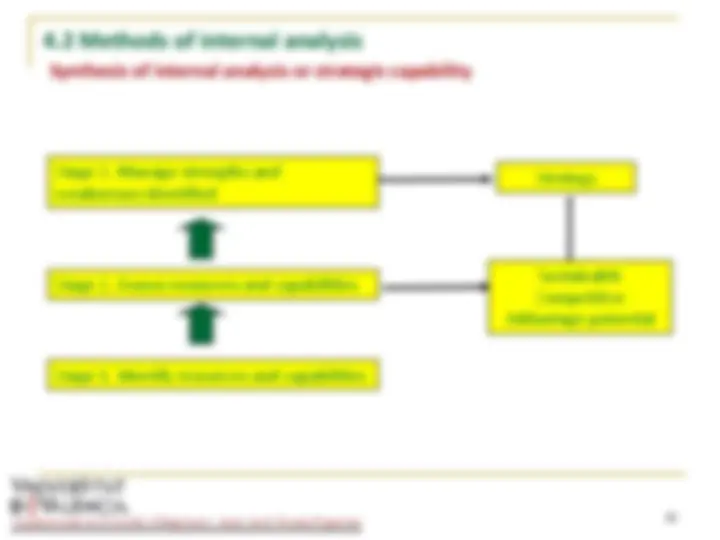

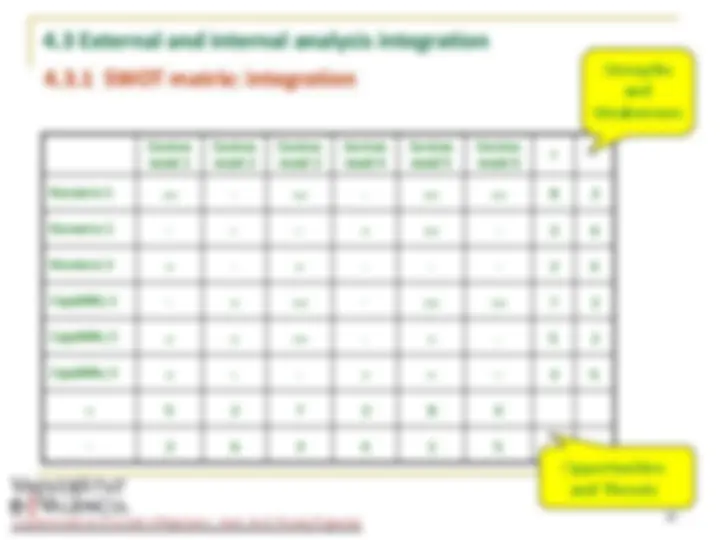

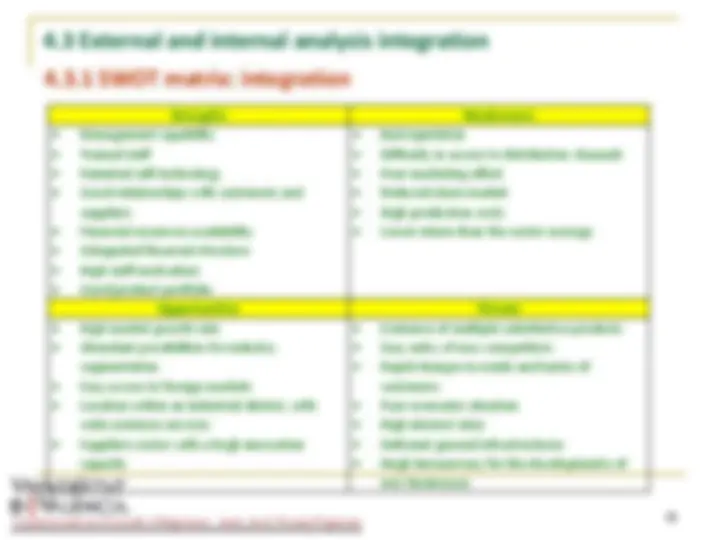

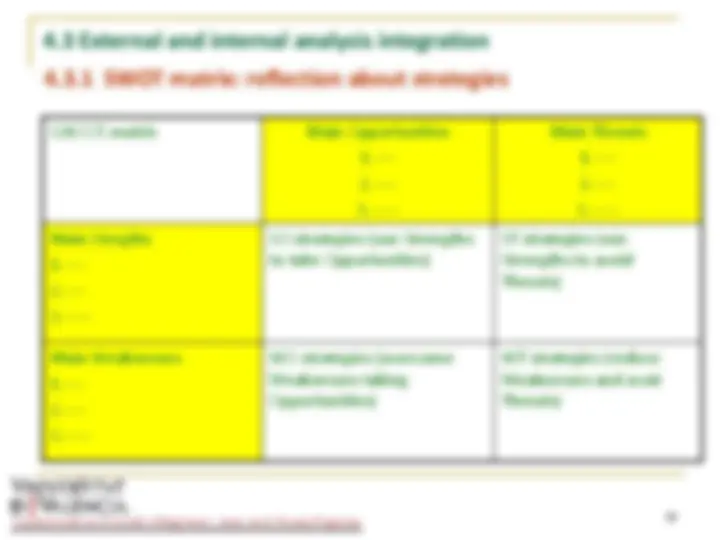

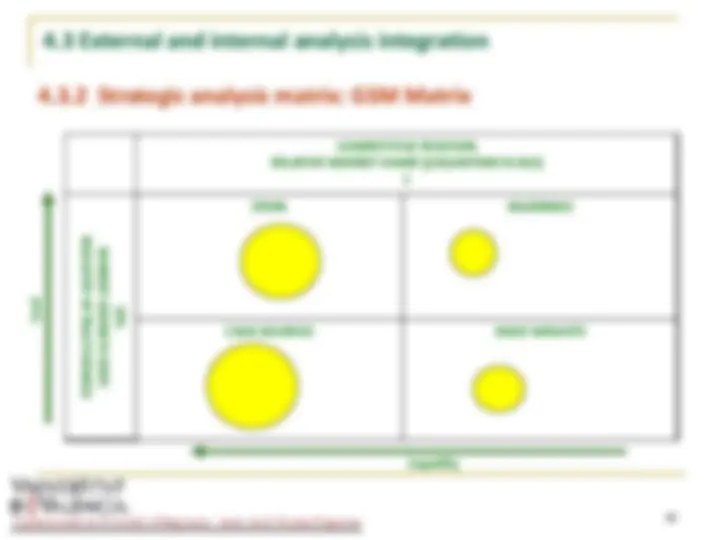

4.2 Methods of internal analysis

4.2.1 Functional analysis and strategic profile

4.2 Methods of internal analysis 4.2.1 Functional analysis and strategic profile: key variables, functional areas

Marketing function Market (market share trends, ..) Product (post-sale service, ...) Price Distribution Promotion and advertising Production function Characteristics of the production process Cost analysis Quality control,... Productivity analysis Equipment status (maintenance policy) Procurement policy Inventory management: sources, timelines,… Plants location Finance Function Financial structure Profitability analysis Risk analysis

Human Resource Function Recruiting system Qualification and training level Conflict level (worked hours vs. nominal hours) Human resource efficiency (measuring absenteeism and its causes) Promotion systems, incentives and rewards, and participation. Security systems in the job

Management function Organizational structure Management Motivation system Information systems Planning-control systems Business culture

4.2 Methods of internal analysis

4.2.1 Functional analysis and strategic profile

4.2 Methods of internal analysis

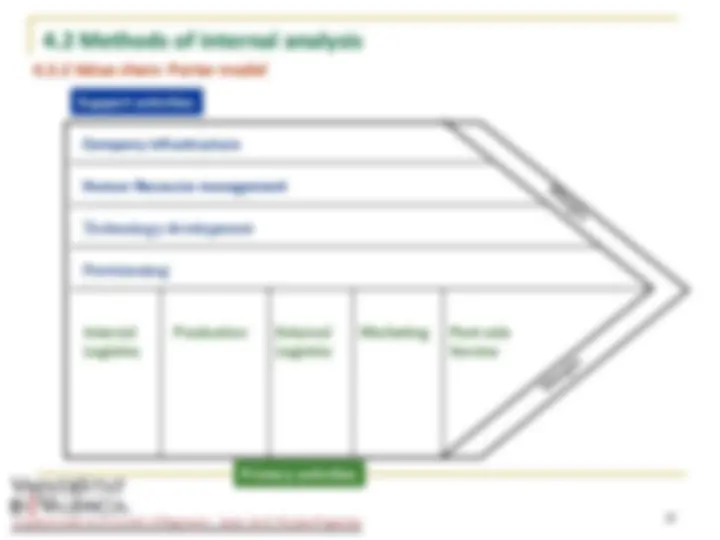

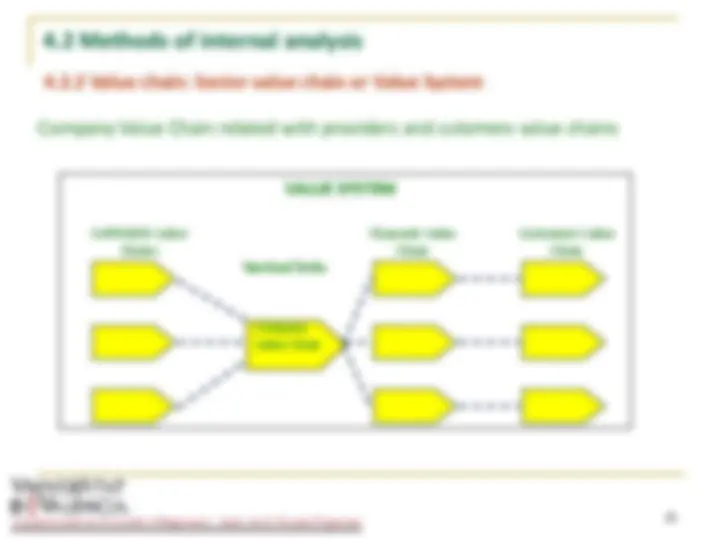

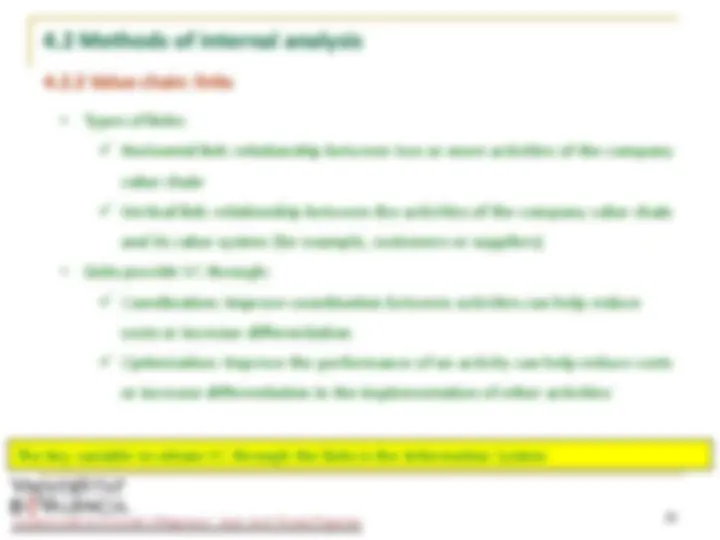

4.2.2 Value chain

Technique that allows a partition of the company in separable activities and learn how each one of them contributes to achieving the desired objectives. It consists of all activities that a company performs to produce and sell a product / service. Lets analyze activities and relationships between them.

Basic activities Interrelations between basic activities (horizontal links) Interrelations within the Value System (vertical links)