¡Descarga LESSON 2 - compulsory contributions y más Diapositivas en PDF de Derecho Financiero y Tributario solo en Docsity!

Lesson 2

Compulsory contributions

Concept and types

Prof. Santiago Ibáñez Marsilla

Universidad de Valencia

Main features

- Ability to pay as a pre-requisite.

- Cannot be confiscatory (31.1 CE).

- It is not a penalty for an infringement.

- It applies not only to nationals, but to whoever has economic dealings with Spain or Spanish territory.

- The most relevant type of public revenue source (of public law nature). - It is an obligation to pay money. - Required by a public Administration - A credit and a public law obligation which is : - An ex lege obligation: it is created by the will of the law (Act of Parliament), and the will of the taxpayer is irrelevant. The taxpayer only decides whether or not fulfill the factual pre- requisites. - Public law: content and regime cannot be altered by the will of individuals; it is pre-determined in the law. - Purpose: finance public expenditure. Prof. Santiago Ibáñez Marsilla

Types of compulsory contributions

ART. 2 LGT

- 1. Fees (“tasas”)

- 2. Special contributions (“contribuciones

especiales”)

Prof. Santiago Ibáñez Marsilla

Types of taxes

- PERSONAL / REAL :

- Wheteher or not the taxable event can be conceived by reference to a specific person (the taxpayer is the nexus between otherwise disconnected economic realities).

- OBJECTIVE / SUBJECTIVE:

- Whether or not the personal circumstances of the taxpayer are taken into consideration in determining the amount of the tax due.

- PERIODICAL / INSTANTANEOUS:

- Whether or not the taxable event refers to a period of time or to an event in time.

- DIRECT / INDIRECT

- Economic distinction (whether or not the tax can be shifted)

- Proposal for an alternative distinction in law.

- FISCAL / NON-FISCAL (“EXTRAFISCALES”)

Prof. Santiago Ibáñez Marsilla

Fees (1)

- A compulsory contribution whose taxable event

consists in either:

- private utilisation or special exploitation of public domain,

- A service or the realisation of activities in public law regime, referred to or giving advantage specifically to the taxpayer when:

- When the request or the reception of the service or the

activity by the taxpayer is not voluntary or

- Are not performed by the private sector. » Services and activities are considered to be in the public law regime when they are performed according to administrative law concerning public services and by a public authority.

Prof. Santiago Ibáñez Marsilla

Fees (3)

- A material concept of compulsion applies.

Thus:

- Fee for an administrative service when the request is compulsory.

- Fee when the service, although not compulsory, is necessary for basic needs of life, either personal or social

- Fee when only the public sector can render the service (legally or as a matter of fact).

Prof. Santiago Ibáñez Marsilla

Public prices (1)

- In 1989 a new legal category was created, “public prices” (“precios publicos”) made of some of the cases where a payment of a fee was previously required. The aim was to avoid the legality principle and its inconvenience.

- A public price had to be paid for:

- Private utilisation or special exploitation of public domain.

- Public postal services.

- Compulsory services or administrative activities.

- Services or activities under public law regime where: » The request or the reception of the services or activities is not compulsory, OR » Can be provided by the private sector

Prof. Santiago Ibáñez Marsilla

Public prices (3)

- Current concept of public prices (“precios públicos”).

- Public prices (24 LTPP and 41 LHL): payment received by a public entity when - The service or activity are voluntarily requested or received AND - Are rendered by the private sector. - There is no compulsion when, simultaneously: » Administrative service whose request is voluntary, » That service is not necessary for basic life needs (either personal or social) and » The public sector is not the only provider available.

Prof. Santiago Ibáñez Marsilla

Public prices (4)

- Differences between fees and public prices.

- Fee is a compulsory contribution, with all its implications – ex lege obligation, public law nature- and, therefore, an economic obligation of public nature in the sense of art. 31.3 Spanish Constitution (subject to the legality principle).

- Public prices are not compulsory contributions nor economic obligations of public nature, since they are created from the free will of the payer –not by the will imposed on him by the law, or ex lege -. Therefore, there is no need to regulate them in an Act of Parliament (the legality principle does no apply).

Prof. Santiago Ibáñez Marsilla

The amount of fees and public prices

- Fees: have an upper limit that must be established in an Act of Parliament (19 LTPP and 24 LHL). - Market value of the private utilisation or special exploitation of public domain - The Act of Parliament will not necessarily specify the amount of the fee; it is enough if it provides sufficient elements as to avoid an indetermination that betrays the legality principle. - Effective or calculated cost of the service or activity; in the absence of such, value of the service or the activity. - Upper limit: cost of the service or activity, including both direct and indirect costs, even financial costs, depreciation and, if any, the costs necessary to maintain the service or activity.

- Public prices must cover, as a minimum, the costs of the service or activity.

Prof. Santiago Ibáñez Marsilla

Special Contributions (1)

- Compulsory contributions whose taxable event

is the taxpayer’s:

- receipt of a benefit or an increase in value of a property as a result of: - the carrying out of public works or - the establishment or expansion of public services (2.2.b) LGT).

Prof. Santiago Ibáñez Marsilla

Economic Obligations of Public Nature (Prestaciones Patrimoniales Públicas)

- 31.3 CE: “Only an Act of Parliament can

establish personal or economic obligations of

public nature ”

- What are EOPN?

- PUBLIC REVENUE = ECONOMIC OBLIGATIONS OF PUBLIC NATURE (EOPN)?

- COMPULSORY CONTRIBUTIONS = ECONOMIC OBLIGATIONS OF PUBLIC NATURE?

Prof. Santiago Ibáñez Marsilla

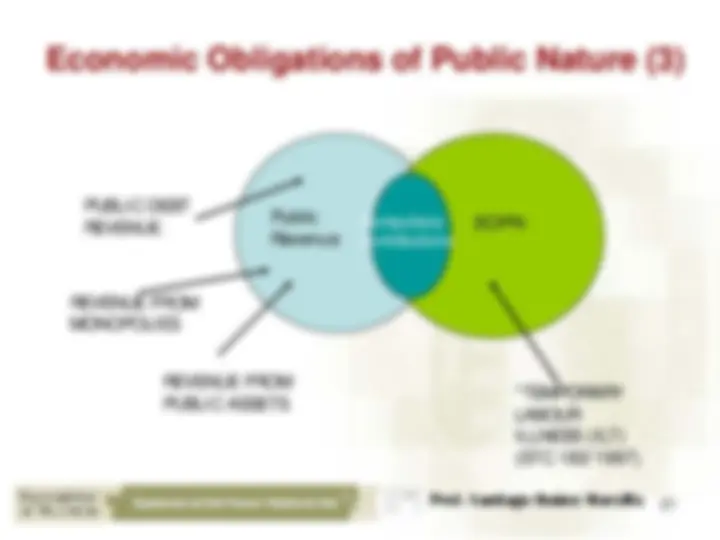

Economic Obligations of Public Nature (2)

- What are EOPN? Two positions:

- 1. They are not the same thing as compulsory contributions (STC 185/1995, 182/1997 and 63/2003). They are public revenue sources that must be provided in an Act of Parliament since they are compulsory.

- Material compulsion:

- Obligation imposed by law.

- Goods, services or activities essential for the private or social life (postal services; public domain goods).

- 2. They are the same thing as compulsory contributions (STC 233/1999 and 106/2000) - They are public revenue sources compulsorily required, without regard to the ability to pay. - The concept of compulsion is too wide. Prof. Santiago Ibáñez Marsilla