Chapter 1

©2010 Worth Publishers

First Principles

Slides created by Dr. Amy Scott

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Prepara tus exámenes

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Prepara tus exámenes con los documentos que comparten otros estudiantes como tú en Docsity

Encuentra los documentos específicos para los exámenes de tu universidad

Estudia con lecciones y exámenes resueltos basados en los programas académicos de las mejores universidades

Responde a preguntas de exámenes reales y pon a prueba tu preparación

Consigue puntos base para descargar

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Comunidad

Pide ayuda a la comunidad y resuelve tus dudas de estudio

Ebooks gratuitos

Descarga nuestras guías gratuitas sobre técnicas de estudio, métodos para controlar la ansiedad y consejos para la tesis preparadas por los tutores de Docsity

An excerpt from an economics textbook that introduces the three principles of economics: individual choice, choice interaction, and economy-wide interactions. It covers the concepts of scarcity, opportunity cost, marginal analysis, gains from trade, equilibrium, and efficiency vs. Equity.

Tipo: Apuntes

1 / 33

Esta página no es visible en la vista previa

¡No te pierdas las partes importantes!

©2010 Worth Publishers First Principles Slides created by Dr. Amy Scott

One must choose

Economics: social science that studies the production, distribution and consumption of goods and services from the Greek oikonomia meaning administration or management of a household (^) Economy: system for coordinating society’s productive activities (^) Market economy: an economy in which decisions about production and consumption are made by individual producers and consumers

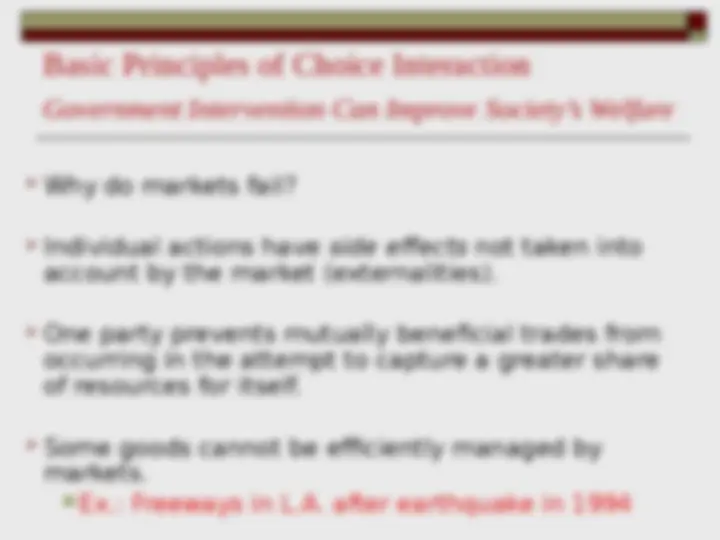

Microeconomics: branch of economics concerned with how people make decisions and how these decisions interact Macroeconomics: branch of economics concerned with the overall economy Market failure: when individual pursuits of self- interest lead to bad results for society

Individual choice is the decision by an individual of what to do, which necessarily involves a decision of what not to do (^) Basic principles behind the individual choices: A. Resources are scarce. B. The real cost of something is what you must give up to get it. C. “How much?” is a decision at the margin. D. People take advantage of opportunities to make themselves

A resource is anything that can be used to produce something else. Ex.: Land, labor (time of workers), capital (machines) Resources are scarce – the quantity available is not large enough to satisfy all productive uses. Ex.: Petroleum, lumber, intelligence

Opportunity cost is about what you have to forgo to obtain your choice. The bumper stickers that say “I would rather be … (fishing, golfing, swimming, etc…)” are referring to the “opportunity cost.” (^) The opportunity cost of attending college is high : it’s the cost of tuition and housing plus the forgone salary you could have earned.

(^) At many cash registers there is a little basket full of pennies. People are encouraged to use the basket to round their purchases up or down. If it’s too small a sum to worry about, why calculate prices that exactly? Why do we have pennies? (^) Sixty years ago, a penny was equivalent to 30 seconds worth of work—it was worth saving a penny if doing so took less than 30 seconds. But wages have risen along with overall prices. Today a penny is therefore equivalent to just over 2 seconds of work—and so it’s not worth the opportunity cost of the time it takes to worry about a penny more or less. (^) The rising opportunity cost of time in terms of

Basic Principles of Individual Choice Marginal Analysis (continued) (^) Making trade-offs at the margin : comparing the costs and benefits of doing a little bit more of an activity versus doing a little bit less. Ex.: Studying one more hour, eating one more cookie, buying one more CD, etc. (^) The study of such decisions is known as marginal analysis.

Basic Principles of Individual Choice Exploiting Opportunities People usually take advantage of opportunities to make themselves better off. People respond to incentives. (^) Ex.: If the price of parking in Manhattan rises, commuters who can find alternative ways to get to their job will save money. Incentives: anything that offers rewards to people who change their behavior.

(^) In 1900, only 6 percent of married women worked for pay outside the home. By 2005, the number was about 60 percent. This change is in part due to changing attitudes, invention, and the growing availability of home appliances, especially washing machines. In pre-appliance days, the opportunity cost of working outside the home was very high: it was something women typically did only in the face of dire financial necessity. With modern appliances, the opportunities available to women changed—and the rest is

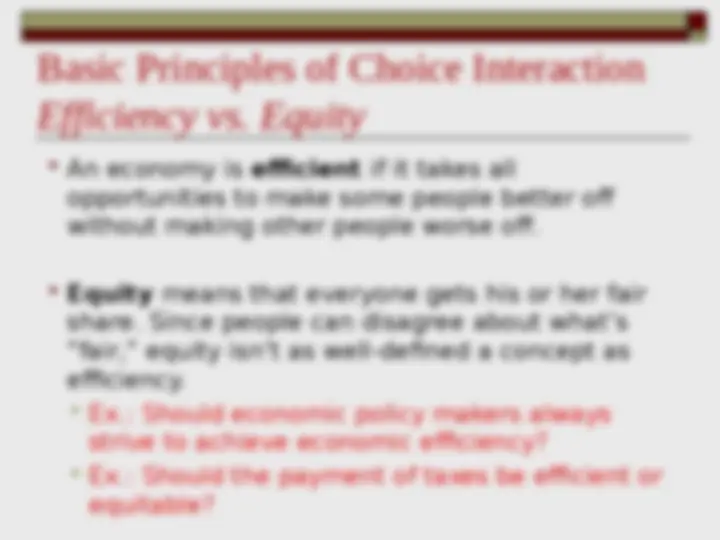

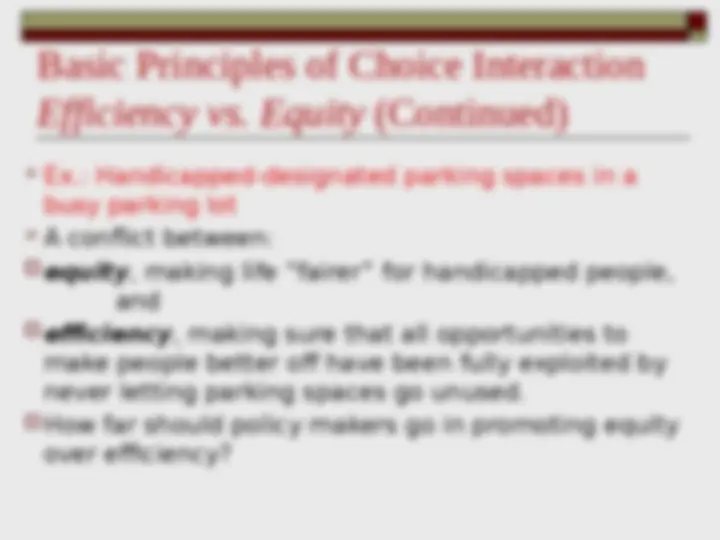

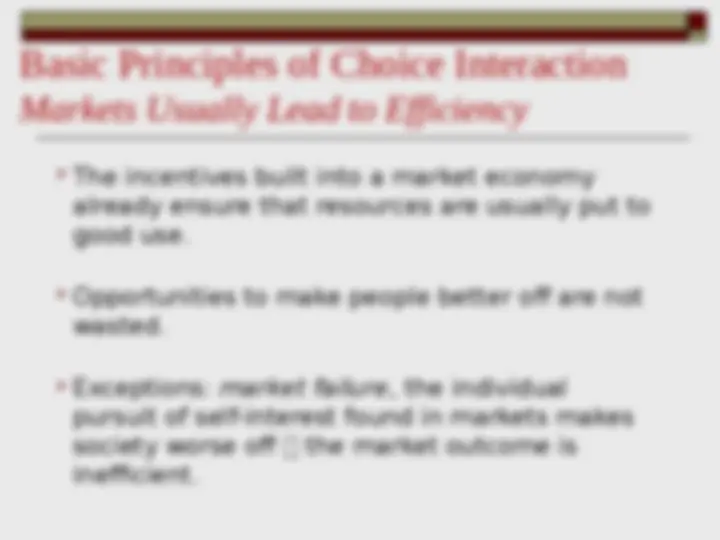

Interaction of choices—my choices affect your choices, and vice versa—is a feature of most economic situations. Principles that underlie the interaction of individual choices: A. There are gains from trade. B. Markets move toward equilibrium. C. Resources should be used as efficiently as possible to achieve society’s goals. D. Markets usually lead to efficiency. E. When markets don’t achieve efficiency, government intervention can improve society’s

This increase in output is due to specialization : each person specializes in the task that he or she is good at performing. © The New Yorker Collection ^1991 Ed Frascino from cartoonbank.com. All Rights Reserved. The economy, as a whole, can produce more when each person specializes in a task and trades with others.

“I hunt and she gathers – otherwise we couldn’t make ends meet.”

Basic Principles of Choice Interaction Equilibrium (^) An economic situation is in equilibrium when no individual would be better off doing something different. Any time there is a change, the economy will move to a new equilibrium.