¡Descarga resumen macroeconomia chapter 3 y más Resúmenes en PDF de Macroeconomía solo en Docsity!

CHAPTER 3

National Income: Where It

Comes From and Where It Goes

Notes to the Instructor

Chapter Summary

Chapter 3 presents an important but relatively straightforward classical model of the real side of the economy. Much of the material in the chapter (such as marginal products, factor demands, consumption and investment functions, and the like) is likely to be a review of materials covered in principles courses. The material can probably be presented in two lectures to students with a suitable grounding from principles; three lectures might be more appropriate for less-well- prepared students. The model of the chapter provides a complete description of how the real side of the economy works, in the sense that it explains all the markets and transactions illustrated in the circular flow diagram (Figure 3-1). The model is set up as follows: Production Capital and labor stocks are fixed and, together with the production function, determine GDP. Distribution GDP is paid to factors of production according to their marginal products. Euler’s theorem ensures that these factor payments exactly exhaust GDP. Allocation GDP is allocated to consumption, investment, and government purchases according to a consumption function [ C = C ( Y – T )]), an investment function [ I = I ( r )], and fiscal policy. The real interest rate adjusts to ensure equilibrium in the goods (equivalently the loans) market. The model is long run in the sense that it assumes that prices are flexible and that markets clear. At the same time, however, it presents only a snapshot of the economy at a point in time because it assumes a fixed capital stock, labor force, and technology. The chapter has three primary goals:

- To introduce students to some of the basic terms and concepts that will be used throughout the book, such as the production function, the consumption function, and the investment function.

- To provide long-run answers to four questions: (a) What determines the level of GDP and national income? (b) What determines how national income is distributed to labor and owners of capital? (c) What determines how GDP is allocated to consumption, investment, and government purchases? (d) What ensures equilibrium of the flows in the circular flow diagram?

- To develop a model that is both a basis for further analysis and a benchmark for comparison as the book goes on to consider topics such as the determination of prices 49

50 | CHAPTER 3 National Income: Where It Comes From and Where It Goes (Chapter 5), the open economy (Chapter 6), the Solow growth model (Chapters 8 and 9), and the IS–LM model (Chapters 11 and 12).

Comments

The lecture notes introduce notation for private saving and public or government saving that does not appear in the textbook: S p and S g, respectively. This facilitates presentation of equilibrium in the loans market. Students must clearly understand the distinction between public and private saving. For example, students are often confused by the fact that decreases in taxes decrease saving because they focus on the effect on private saving and miss the effect on the government deficit. The lecture notes emphasize the circular flow as the reference point for the analysis. The household’s budget constraint ( C + S p = Y – T ), the equality of income and output ( Y = Wages + Profits), the definition of the deficit ( S g = –DEF = T – G ), the goods market equilibrium condition ( Y = C + I + G ), and the loans market equilibrium condition ( S = S p + S g = I ) can all be introduced in terms of the circular flow diagram. Like the text, the lecture notes emphasize the loanable funds interpretation of equilibrium. As well as being simple to present and illustrate in terms of a savings/investment diagram, this approach makes it clear why the real interest rate is the key equilibrating variable. The classical model of this chapter provides a benchmark. Many of the other models in the book take this model as a starting point, and we refer back to this analysis many times. Many of the concepts introduced in this chapter (for example, consumption and investment functions) are used throughout the book.

Use of the Website

Since the classical model provides a benchmark, it is probably a good idea to give the students many analytical exercises using this model. The curve-shifting exercises are relatively simple so that the exercises of this chapter allow the students to familiarize themselves with the software.

Use of the Economy.com Website

Use the Economy.com website to download data for the past 40 years on national income, national saving, the government budget surplus, and the current account surplus. Compute private saving by subtracting the government budget surplus and the current account surplus from national saving. Now, express private saving, the government budget surplus, and the current account surplus as a share of national income. Discuss how the shares have changed over time.

Chapter Supplements

This chapter includes the following supplements: 3-1 How Long Is the Long Run? Part I 3-2 What Is Capital? 3-3 Labor’s Share of Output in the United Kingdom 3-4 Economists’ Terminology 3-5 Public and Private Saving 3-6 Wars and Interest Rates

52 | CHAPTER 3 National Income: Where It Comes From and Where It Goes Lecture Notes

Introduction

We now move from measurement to the deeper question of the explanation of the behavior of the economy. This chapter develops a basic model of the long-run behavior of a well-functioning economy (one in which prices are flexible, so all markets are always in equilibrium). This classical model explains Supplement 3-1, “How Long Is the Long Run? Part I”

- The determinants of the level of output (income),

- How income is distributed,

- How output is allocated among alternative uses, and

- What ensures that the supply of and demand for goods are equal. Figure 3- The starting point is the circular flow of income from Chapter 2, complicated somewhat by the addition of the government but kept simple by restricting attention to a closed economy (net exports equals zero). Some accounting relationships from Chapter 2 show up here. From the goods market (remembering that NX = 0), Y = C + I + G. Looking at firms, we have Profits + Wages = Y, and considering the government, we obtain the definition of the government deficit: DEF = G – T. Finally, from the financial markets (letting S p represent private saving), S p = DEF + I.

3-1 What Determines the Total Production of Goods and Services?

The Factors of Production

Supplement 3-2, “What Is Capital?” The economy has certain resources, most notably its labor and its stock of machines and factories (its capital stock). Firms in the economy use labor and capital as inputs to produce goods and services (GDP). To keep things simple, we take K and L as fixed and exogenous ( K^ K L^ ;^ ^ L ). We do not yet wish to explain variations in employment or in the capital stock.

The Production Function

We express the economy’s ability to produce goods and services from its resources as Y = F ( K , L ). This says simply that the amount of GDP an economy can produce depends on its capital stock K and its labor L. More capital or more labor allow the economy to produce more output. An example of a production function is

Lecture Notes | 53 Y = ( KL )1/. Thus, if K = 40 and L = 10, Y = (400)1/2^ = 20. If the economy were suddenly to have exactly twice the amount of all its inputs, we would expect that it could produce exactly twice as much output simply by using the new resources in exactly the same way as the old resources. If a factory can produce 20 automobiles using 40 machines and 10 workers, then it should be possible to produce 40 automobiles with 80 machines and 20 workers simply by building a second factory identical in all respects to the first one. More generally, if the amount of all inputs is increased by some constant percentage, output should be changed by the same percentage. This means that the production function should exhibit constant returns to scale. This is written mathematically as zY = F ( zK , zL ) for any positive number z. Doubling the amount of inputs from the earlier example, so that K = 80 and L = 20, gives Y = (1,600)1/2^ = 40, illustrating that this function does have constant returns to scale.

The Supply of Goods and Services

Since we are supposing that K and L are fixed, it follows that we can calculate GDP immediately from the production function Y F K L ( , ). Y (^) is called the natural rate of output. At any point in time, the long-run or natural rate of output is determined by the available resources and technology.

3-2 How Is National Income Distributed to the Factors of Production?

The overall determination of income is straightforward. More interesting, perhaps, is the question of how this income is divided up between workers, who supply labor and receive wages, and the owners of capital, who supply capital and obtain profits. The modern economic explanation is the neoclassical theory of distribution , which explains how much workers are paid per unit of labor and how much owners of capital are paid per unit of capital.

Factor Prices

Figure 3- As all markets are in equilibrium in the classical model, the markets for labor and capital— factors of production—determine factor prices. The price of each of these factors is determined by demand and supply. Since factor supplies are fixed, the supply curves are vertical, so our main task is to explain factor demands.

The Decisions Facing a Competitive Firm

The demand for factors comes from the firms in the economy that use them to produce goods. We suppose that there are many identical competitive firms. This means that they are small relative to the markets in which they trade, and so they take as given and as outside their control both the price at which they can sell output and the cost of factors of production. Each firm has a production function Y = F ( K , L ).

Lecture Notes | 55

MPK

MPL

So MPK × K + MPL × L = 0.25(40) + 1(10) = 10 + 10 = 20 = Y.

Case Study: The Black Death and Factor Prices

A vivid example of how factor quantities affect factor prices comes from the 1300s, when the bubonic plague was rife in Europe. Within a few years, the population fell by almost one-third. According to the neoclassical theory of distribution, the decline in the amount of labor should have caused real wages to rise, as indeed they did. A peasant who managed to survive the plague ended up prospering financially! And the reduction in labor should have caused the return to land, the other major factor of production at the time, to decline. With fewer workers to farm the land, an additional unit of land would have yielded less additional output. Again, the prediction of the theory is confirmed, as real rents fell by over 50 percent and the landed class experienced reduced incomes.

The Cobb–Douglas Production Function

Figure 3- One feature of U.S. data is that factor shares —the division of income between capital and labor —have been more or less constant over time. Economist Paul Douglas, who later went on to become a U.S. senator from Illinois, noted this constancy of factor shares in 1927. Suppose that the economy is competitive so that factors are paid their marginal products. What production function then implies that factor shares are constant? In other words, what production function implies that the ratio of capital payments to income and the ratio of labor payments to income are constant? The answer supplied by mathematician Charles Cobb was that the function has to be of the form Y = AK α L 1–α, where A is an arbitrary positive constant, so that the factor shares are constant and equal to α and (1 – α): ( MPK × K )/ Y = α MPL × L = (1 – α). Regardless of the actual values of K and L , this function will satisfy these equations. It became known as the Cobb–Douglas production function and is widely used in economics. Since labor’s share of total output in the United States is approximately 0.7, the production possibilities of the U.S. economy can be approximated by the function Y = K 0.3 L 0.7. The earlier example [ Y = ( KL )1/2] is a special case of the Cobb–Douglas production function, where A = 1 and α = 1/2. Going back to that example, we can see that ( MPK × K )/ Y = ( MPL × L )/ Y = 1/2, so it does indeed exhibit constant factor shares.

Case Study: Labor Productivity as the Key Determinant of Real

Wages

Table 3-

56 | CHAPTER 3 National Income: Where It Comes From and Where It Goes The neoclassical theory of distribution states that the marginal product of labor will equal the real wage. The Cobb–Douglas production function has the property that the marginal product of labor is proportional to average labor productivity ( Y/L ). So the theory predicts that growth of real wages should equal growth of average labor productivity. For the United States, the data confirm this prediction. Over the past half century, average labor productivity and real wages have each risen about 2 percent per year. Furthermore, during shorter periods of time, when growth in labor productivity has been higher or lower than the long-term average, real wages likewise have risen in line with productivity.

FYI: The Growing Gap Between Rich and Poor

Supplement 3-3, “Labor’s Share of Output in the United Kingdom” Income inequality between high-wage workers and low-wage workers is much greater today than it was in the 1970s. One explanation argues that skill-biased technological change has increased the demand for skilled workers faster than the education system has supplied such workers. As a result, the wages of skilled workers have grown relative to those of unskilled workers. A recent book by economists Claudia Goldin and Lawrence Katz, discussed in Chapter 3 of the textbook, highlights this explanation. They argue that skill-biased technological progress has continued in recent decades similar to what had happened throughout much of the twentieth century but educational attainment has slowed, putting upward pressure on the relative wages of skilled workers.

3-3 What Determines the Demand for Goods and Services?

So far, we have looked at the top part of the circular flow and found that, given factor supplies K and L , total output is Y = F ( K , L ) and the real wage and real rental rate of capital are determined by the marginal product of labor and capital. We now examine the demand for output, which, as the circular flow diagram illustrates, comes from consumption, investment, and government spending. To simplify our analysis, we ignore net exports and focus on a closed economy that does not trade with the rest of the world. Chapter 6 extends our framework to the open economy.

Consumption

Consumption is the largest source of demand and so is a natural starting point. Individuals receive wage and profit income totaling Y. Some of this income is paid to government in the form of taxes. The government also gives transfer payments (for example, unemployment insurance, Social Security) to individuals. For aggregate purposes, only the net flow from individuals to the government matters: T = Taxes – Transfer Payments. Disposable income (after-tax income) is Y – T. The consumption decision is a decision between consuming now or saving to consume at some time in the future. Consequently, the decision depends on expectations about future economic conditions as well as on current circumstances. For now, however, we postpone detailed discussion of these issues until Chapter 16 and concentrate on the simplest story of consumer behavior. The primary determinant of consumption is disposable income, and the relationship between consumption and disposable income is known as the consumption function : C = C ( Y – T ).

58 | CHAPTER 3 National Income: Where It Comes From and Where It Goes

Government Purchases

The final component of expenditure is government spending. This is the purchase by federal, state, and local governments of goods and services. It does not include transfer payments; these contribute indirectly to the demand for goods and services through their effect on consumption. Governments’ choices of G and T determine their fiscal policy. One measure of a government’s fiscal policy stance is the deficit (DEF = G – T ). If the government takes actions to increase the deficit (increasing G or decreasing T ), this is known as an expansionary policy; the converse is a contractionary policy. The current analysis takes G and T as exogenous ( G^ G^^ , T^ T^ ).

FYI: The Many Different Interest Rates

The textbook speaks throughout of “the” interest rate. Yet we know that, in the real world, there are many different interest rates. Interest rates differ because of term to maturity, credit risk, and tax treatment. But for most macroeconomic analysis, we can ignore these distinctions because different interest rates tend to move together.

3-4 What Brings the Supply and Demand for Goods and Services into

Equilibrium?

From the circular flow diagram, the supply of goods, Y , equals the demand for goods ( C + I + G ). But Y is determined by the technology, together with the stocks of capital and labor, while C , I , and G depend on the choices of households, firms, and government. What guarantees that supply equals demand? From microeconomics, we should expect that some price will match up supply and demand. A natural candidate for the equilibrating price might seem to be P , since it represents the price of a unit of GDP in terms of dollars. But, in fact, neither the supply nor any component of the demand for goods depends on the general price level because people care about real values. If, say, the price level increases, then everything costs more in dollar terms, but real prices are not affected. Instead, the price that ensures equilibrium in the goods market is actually the real interest rate. (We will see in Chapter 7 that the price level is actually determined in the money market. Since P is the price of goods in terms of dollars, 1/ P is the price of dollars in terms of goods, or the real price of money.)

Equilibrium in the Market for Goods and Services: The Supply

and Demand for the Economy’s Output

The following equations summarize the demand and supply of goods and services for the economy: Since ( ) ( ) ( , ).

Y C I G

C C Y T

I I r G G T T Y F K L Y

Using these equations and noting that G and T are fixed by policy and Y is fixed by the factors of production and the production function, we can derive the following relationship: Y C Y ( T ) I r ( ) G

Lecture Notes | 59 where the supply of output equals the demand for output. Since Y , C , and G are fixed in this equation, equilibrium must be achieved by adjustment of the interest rate. If the supply of goods and services exceeds the demand for goods services, then the interest rate will fall, encouraging investment and increasing the demand for goods and services. Conversely, if the supply of goods and services falls short of the demand for goods and services, then the interest rate will rise, reducing investment and decreasing the demand for goods and services.

Equilibrium in the Financial Markets: The Supply and Demand

for Loanable Funds

We can rewrite the equilibrium condition as Y – C Y – T (^) – G I (^) r . Now add and subtract T^ : Y – C Y – T (^) – T (^) T – G (^) I r . This can be rewritten as

S p S g I r .

In this case, S (^) p Y – C Y – T (^) – T is private saving, and Sg T – G is public saving. Combining the saving terms into national saving, S , we obtain

S I r .

Supplement 3-5, “Public and Private Saving” From this equation, we can see that when the goods market equilibrium condition is rewritten in terms of saving and investment, it has an interpretation in terms of equilibrium in the financial markets. Saving and investment represent the supply of and demand for loanable funds. Individuals and governments save, making funds available for investment. If the interest rate is high, there will not be very much demand for investment, implying too little investment relative to the amount of saving. The interest rate will then fall. The opposite occurs if the interest rate is too low. Figure 3-

Changes in Saving: The Effects of Fiscal Policy

We can now use our simple model to carry out comparative static experiments. Among the most interesting are those that entail a change in government policy variables. Suppose that the government carries out an expansionary fiscal policy by increasing spending or cutting taxes. Then, the government deficit will increase, so S g will fall. To restore equilibrium in the goods market, the interest rate must rise: Since there is a greater demand for goods, but a fixed supply, the interest rate has to rise to decrease investment demand. Expressed in terms of the loans

Lecture Notes | 61 Chapter 3 presents a classical long-run model of the economy in which the level of output is determined by the available technology and the available factors of production. Factor prices adjust to ensure that factor markets are in equilibrium. Adjustment of the real interest rate ensures that the supply of goods equals the demand for goods (or, equivalently, that the supply of loanable funds equals the demand for loanable funds). Much of the rest of the book involves extending or refining this basic model.

62 | CHAPTER 3 National Income: Where It Comes From and Where It Goes LECTURE SUPPLEMENT

3-1 How Long Is the Long Run? Part I

The models of the economy presented in Parts II and III of the book are models of the long run, whereas the models in Part IV are short-run models. So how long is the long run? The answer is that it depends both on the world and on the model. The key feature of the classical model (discussed in Chapter 3) that makes it a long-run model is that prices are flexible. In other words, prices are assumed to adjust in that model to ensure equality of supply and demand in all markets. In the short-run models of Part IV, by contrast, it is often assumed that prices are instead sticky and so do not adjust to equilibrate all markets. The most basic answer to the question is then that the long run is however long it takes for prices to be free to adjust in all markets in the economy. Whereas prices can move instantaneously in some markets, they may be fixed for months (or even years, in the case of labor contracts) in other markets. As a rule of thumb, most economists believe price stickiness is relevant over a time horizon of a few months up to a couple of years, but not over a large number of years.

LECTURE SUPPLEMENT

3-3 Labor’s Share of Output in the United Kingdom

Figure 3-5 in the textbook reveals that the division of U.S. output between capital and labor has been roughly constant for the past 60 years, suggesting that the Cobb–Douglas production function is a useful approximation. This stylized fact can be observed in other countries as well: Figure 1 graphs labor’s share of output in the United Kingdom over the past century and a half. Although labor’s share in the United Kingdom shifted upward in the early twentieth century, it has been relatively stable for the past 70 years. Source: Constructed by Charles Bean from data in B.R. Mitchell, British Historical Statistics (Cambridge, MA: Cambridge University Press, 1988). 64

LECTURE SUPPLEMENT

3-4 Economists’ Terminology

Like all other sciences, economics has a well-developed terminology, or jargon. Such language is important because it allows economists to talk precisely about the economy and to avoid ambiguity. But this terminology presents pitfalls for the uninitiated, since economists have an annoying habit of taking terms that are used in everyday speech and giving them a precise meaning that may not exactly match their everyday meanings. We consider some examples here.

Saving and Investment

In everyday speech, people use the term investment to refer to any purchase of an asset, such as stocks and bonds, works of art, old or new housing, and the like. Macroeconomists usually use the term much more precisely to refer only to certain purchases of newly produced final goods and services. If a firm buys a new machine, or if an individual buys a new house, then that is investment as far as the macroeconomist is concerned. If an individual buys IBM shares or a Renoir painting, that is not investment in the macroeconomic sense; it is rather an individual act of saving. Such purchases merely reallocate existing assets among individuals and do not represent any net change in the assets of society. If a person purchases an existing house, then the transaction represents saving for the purchaser and dissaving for the seller. There is no net change in private saving, and so there will be no change in investment.

Money and Income

In everyday speech, a rich individual might be described as having a great deal of money. To the economist, however, money is not a synonym for income or wealth. Money is the name given to a particular asset or set of assets used for transactions. The detailed definition of money is discussed in Chapter 4, but it is sufficient to think of money as simply being dollar bills and deposits in checking accounts. A person with a large amount of money, to an economist, is someone who walks around with a large number of $100 bills or has a large value of deposits in a checking account. The distinction is important because changes in income and changes in money have very different effects in macroeconomic models. For example, increases in income induce people to consume more, but an individual’s consumption will not be higher simply because he or she holds more money.

Profit

As discussed in Chapter 3, economists distinguish between economic profit and accounting profit. Euler’s theorem tells us that a constant-returns-to-scale production function will imply that economic profit is zero if factors are paid their marginal products. The idea that economists conclude that firms don’t make any profit may seem baffling. Again, this arises because economists’ use of the term profit differs from the everyday use of the term. What is normally counted as profit by a firm the economist thinks of as a payment to a factor of production. In reality, individuals own firms, and firms own capital. Firms hire workers and produce goods using their capital and these workers. The revenue that they have left after they have paid their workers is the accounting profit of the firm, and this is usually not zero. These profits will then be distributed to the stockholders of the firms as dividends. But from the economist’s perspective, these payments to stockholders are simply their return for their ownership of the firm’s capital. In other words, they are a payment to a factor of production and do not represent economic profit. 65

ADDITIONAL CASE STUDY

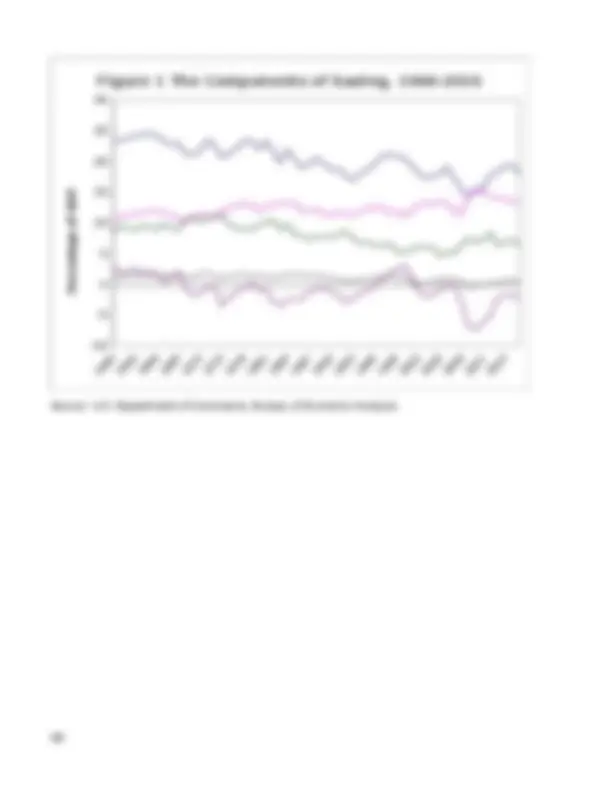

3-5 Public and Private Saving

The classical model of Chapter 3 discusses equilibrium in terms of the equality of investment and national saving. In interpreting this model, it is crucial to remember that national saving includes both private saving and the saving of the government. Private saving can in turn be subdivided into personal saving — the saving of individuals—and business saving , or saving by corporations. Public or government saving can be subdivided into the saving of the federal government and that of state and local governments. Figure 1 shows these components of saving as percentages of GDP for the period 1960–2013. One notable feature of these numbers is that business saving is large. Most of this saving goes to replacement investment , which is the replacement of worn-out or depreciated capital. In 1997, for the first time since the 1970s, the federal government had positive saving. While expenditures of the federal government exceeded current receipts (the federal government had a current budget deficit), this did not exceed the federal government’s expenditures for investment. Macroeconomists tend to focus most on personal saving and the saving of the federal government because these components of saving are most directly affected by macroeconomic policies. In 1996, the Bureau of Economic Analysis revised the way in which it calculated public investment to make it consistent with the manner in which private investment is calculated. Business expenditures on equipment and structures are considered investment. Prior to the 1996 revision, these expenditures, if undertaken by the government, were considered government consumption expenditures. Thus, a new office building purchased by the private sector would increase investment, whereas the same building, if purchased by the government, would not increase investment. Now, expenditures on equipment and structures, regardless of whether they are made by the private sector or public sector, are considered investment expenditures. This change not only treats expenditures by the private and public sectors comparably, but it also makes the calculations of investment and saving more comparable to those of other nations.^0 The revised method of calculating government expenditures raises the amount of gross investment and saving in the economy. Prior to the 1996 revisions, the national income accounts identity was Y – C – G = I. Now, the national income accounts identity can be expressed as Y – C – G C^ = I + G I, where G C^ is consumption expenditures of the public sector and G I^ is investment expenditures of the public sector and G = G C^ + G I. (^0) The United States, however, now lists government purchases of military hardware as investment, while most other countries count these expenditures as consumption. 67

Figure 1 The Components of Saving, 1960-

Percentage of GDP Source: U.S. Department of Commerce, Bureau of Economic Analysis. 68