Financial Statement Analysis

Course: 2020/2021

2nd Semester

Baptiste Colas

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Prepara tus exámenes

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Prepara tus exámenes con los documentos que comparten otros estudiantes como tú en Docsity

Encuentra los documentos específicos para los exámenes de tu universidad

Estudia con lecciones y exámenes resueltos basados en los programas académicos de las mejores universidades

Responde a preguntas de exámenes reales y pon a prueba tu preparación

Consigue puntos base para descargar

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Comunidad

Pide ayuda a la comunidad y resuelve tus dudas de estudio

Ebooks gratuitos

Descarga nuestras guías gratuitas sobre técnicas de estudio, métodos para controlar la ansiedad y consejos para la tesis preparadas por los tutores de Docsity

The concept of creative accounting, its definition, causes, consequences, and methods of detection. Creative accounting refers to the manipulation of financial statements by accountants to improve or worsen the financial results of a business. the incentives for creative accounting, the six principal areas where it can occur, and the ways to manage earnings. It also covers the accounting principles that should be respected, the consequences of creative accounting, and the methods to identify it.

Tipo: Diapositivas

1 / 39

Esta página no es visible en la vista previa

¡No te pierdas las partes importantes!

Course: 2020 / 2021 2 nd Semester Baptiste Colas

Economic environment Accountanting framework (accountants):

Earnings management (or creative accounting) is a process whereby accountants use their knowledge of accounting rules to manipulate the figures reported in the accounts of a business Economic environment Accountanting framework (accountants):

Manipulation Real Accounting Out of the norm Crime Crime Within the norm Out of the accounting framework (called « real earnings management ») Earnings management (Creative accounting)

Optimistic :

The potential for creative accounting (earnings management) is found in six principal areas:

Three categories of incentives for creative accounting:

Optimistic (↗) :

Pessimistic (↘) :

Focus on creative accounting in the area of financial accounting (i.e. for external users) External users Shareholders Creditors Unions/Public bodies Profitability Risk Liquidity Solvency Profitability

17 Profitability Risk Liquidity Solvency Income statement Balance sheet Classification shifting Earnings management Classification shifting Change in balance sheet items

From the income statement point of view: ∆Earnings = ∆Revenues - ∆Expenses To ↗ Earnings (∆Earnings> 0 ) you can either have

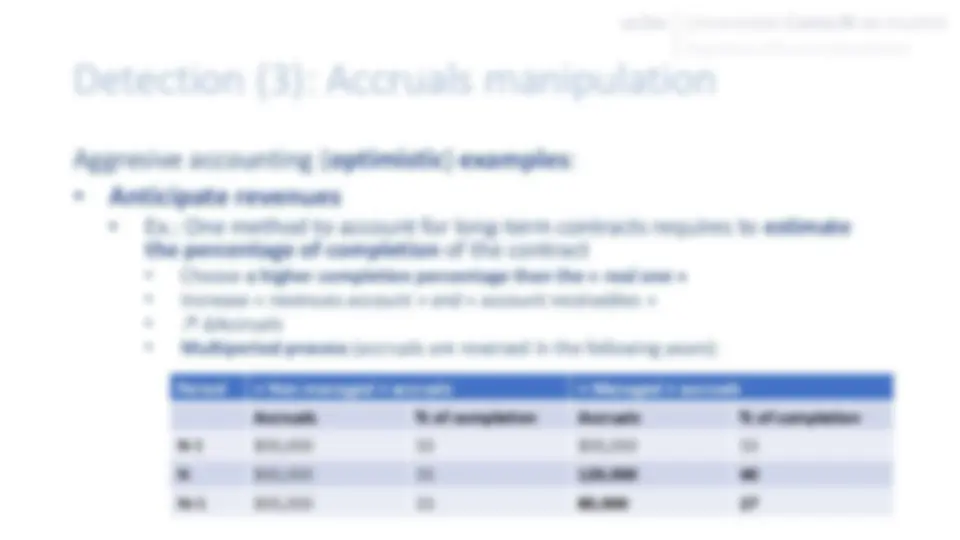

Managers can change the timing of certain transactions to manage earnings: