¡Descarga Financial Markets and Expectations: Bond Prices, Stock Markets, and Arbitrage y más Apuntes en PDF de Economía solo en Docsity!

I.

FINANCIAL MARKETS

AND EXPECTATIONS

a)

Vocabulary b)

Arbitrage and bond prices)

g^

p

c) Stock market and stock prices d)

Bubbles and Fads

Ch. 15 in Blanchard-Amighini-Giavazzi

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

FINANCIAL MARKETS AND

EXPECTATIONS

Expectations also play an essential role in financial

EXPECTATIONS

markets:

-^

We introduce long-term bonds and stocks in our economyWe introduce long term bonds and stocks in our economy.

-^

How are bond prices and bond yields determined? How arethey affected by future expected interest rates?H

th

i ld

t^

l^

b^

t th

t d

-^

How can we use the

yi

eld curve to

learn about the expected

future interest rate?

-^

How are stock prices affected by expected future profits and interes rates?

-^

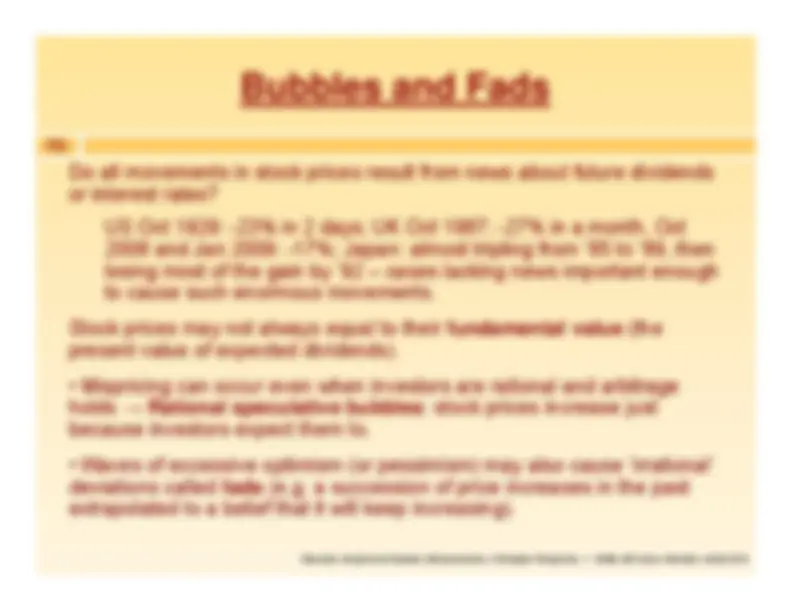

Do stock prices always reflect fundaments or may insteadreflect bubbles or fads?

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

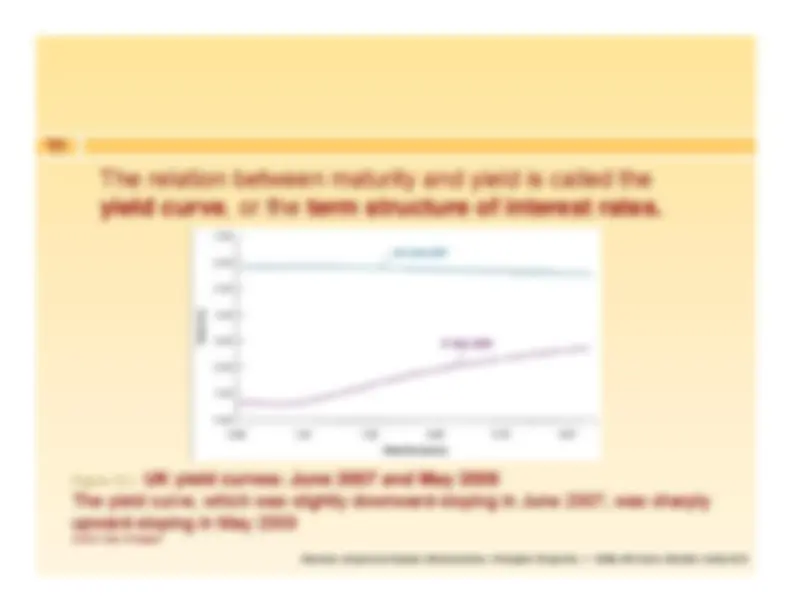

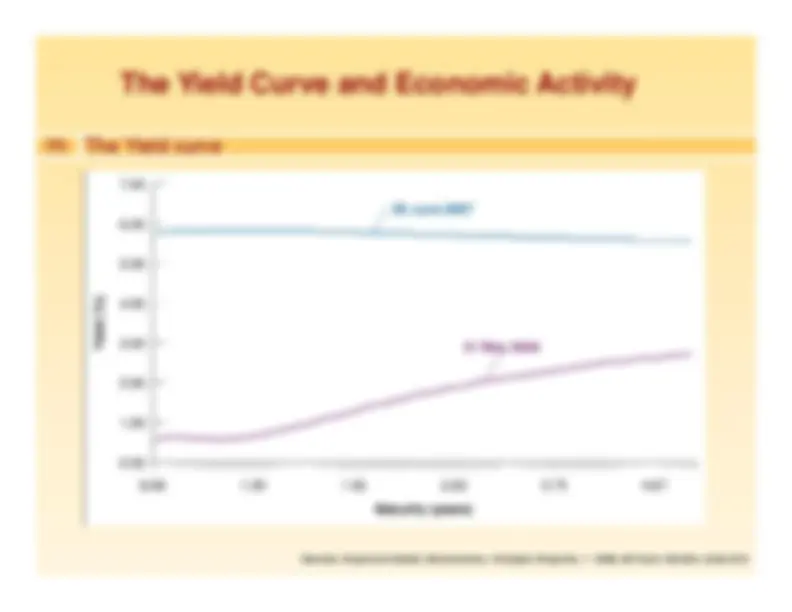

The relation between maturity and yield is called the

y^

y

yield curve

, or the

term structure of interest rates.

Figure 15.

UK yield curves: June 2007 and May 2009

The yield curve which was slightly downward

sloping in June 2007 was sharply

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

The yield curve, which was slightly downward-sloping in June 2007, was sharplyupward-sloping in May 2009 Source

: Bank of England

G

t b

d^

b^

d^

i^

d b

t

•^

G

overnment bonds

are bonds issued by government

agencies. Corporate bonds

are bonds issued by firms.

p^

y

•^

Bond ratings

, issued by Standard and Poor’s, Moody’s,

t^

l^

t^

th i

d f

lt^

i k

etc., evaluate their default risk.The

risk premium

is the difference between the interest

rate paid on a given bond and the interest rate paid on the

p^

g^

p

bond with the highest rating.Bonds with high default risk are often called

junk bonds

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

Th

t^

f th

i t

t^

t^

f^

b^

d i

•^

The correct measure of the interest rate of a bond isneither the coupon rate nor the current yield, but its

yield

to maturity

, roughly the average interest rate paid by the

f

bond over its life.The

life of a bond

is the amount of time left until the bond

matures.

-^

Bonds typically promise to pay a sequence of fixednominal payments However other types of bonds callednominal payments. However, other types of bonds, called indexed bonds

, promise payments adjusted for inflation

rather than fixed nominal payments.

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

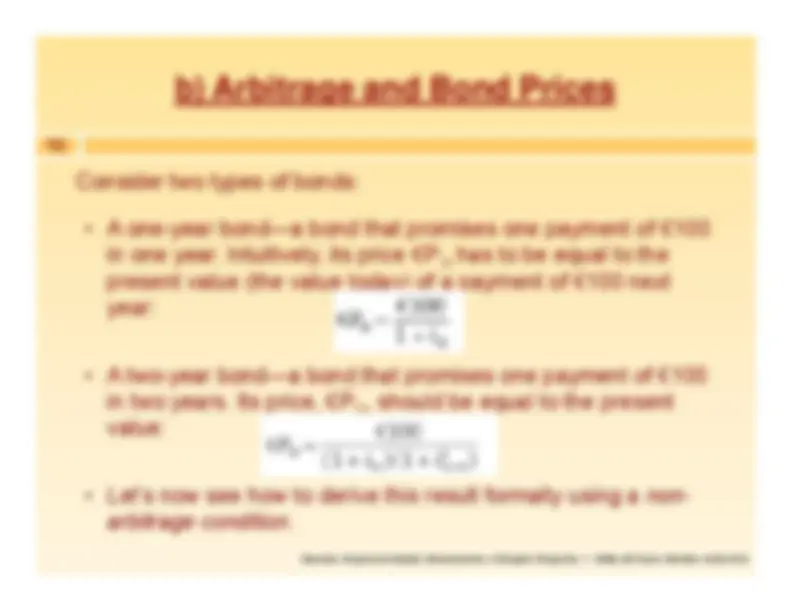

b) Arbitrage and Bond Prices

Consider two types of bonds:

yp

•^

A one-year bond—a bond that promises one payment of €100in one year. Intuitively, its price €P

1t^

has to be equal to the 1t

present value (the value today) of a payment of €100 nextyear:

-^

A two-year bond—a bond that promises one payment of €100in two years. Its price, €P

, should be equal to the present2t^

l value:

-^

Let’s now see how to derive this result formally using a

non

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

Let s now see how to derive this result formally using a

non

arbitrage condition

-^

Suppose financial investors care only about

expected return

.

Arbitrage and Bond Prices

(a simplification: they are likely to care also about risk, which ishigher for a two-year bond, since the price at which you will sell itnext year is uncertain).Th

i^

ilib i

th

t^

b^

d^

t^

ff^

th

t d

-^

Then in equilibrium the two bonds must offer the

same expected

one-year

return

:

Expected returnper euro fromholding a two-year

Return per eurofrom holding aone-year bond for

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

g^

y

bond for one year.

y one year.

Slide15.11^ •

Arbitrage

means that profit opportunities do not go unexploited.

Arbitrage and Bond Prices With risk neutrality, it implies that the expected returns on twoassets are equal (otherwise you could sell one, buy the other andexpect to make a profit).

•^

Arbitrage implies that the price of a two-year bond today is thepresent value of the expected price of the bond next year:

-^

The price of the bond next year is expected to equal the finalThe price of the bond next year is expected to equal the finalpayment discounted by next year expected interest rate:

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

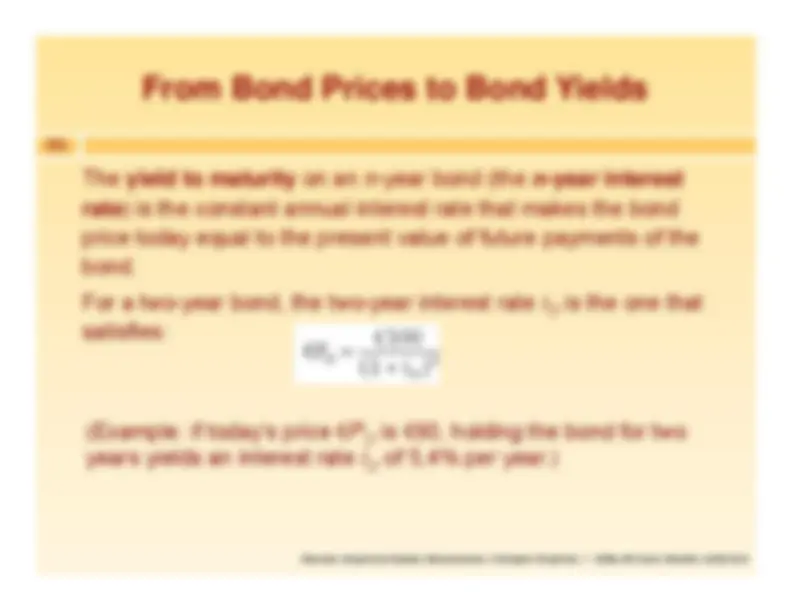

From Bond Prices to Bond Yields

The

y

ield to maturity

on an

n-

year bond (the

n

-year interest

y^

y^

y^

(^

y

rate

) is the constant annual interest rate that makes the bond price today equal to the present value of future payments of thebondbond.For a two-year bond, the two-year interest rate

i^ 2t

is the one that

satisfies:^ (Example: if today’s price

€

P

2t^

is

€

90, holding the bond for two

years yields an interest rate

i^ 2t

of 5,4% per year.)

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

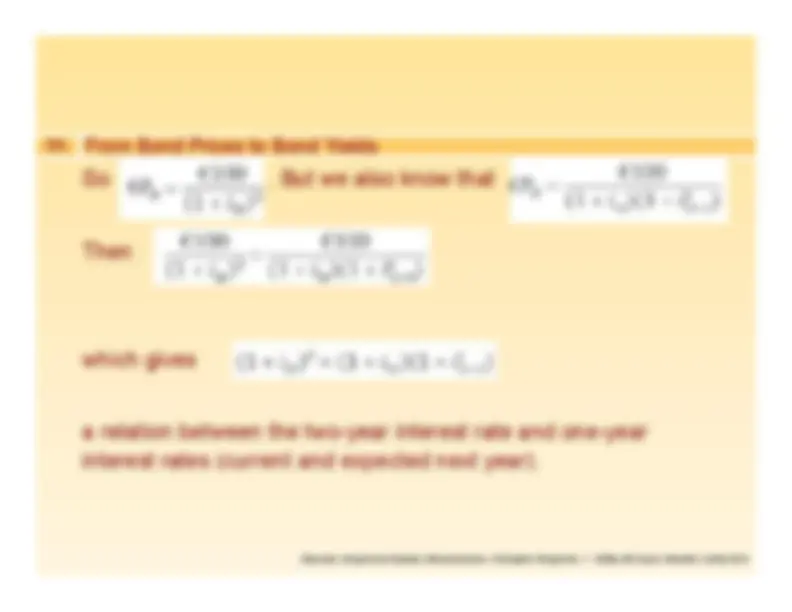

So

. But we also know that

From Bond Prices to Bond Yields Then which gives a relation between the two-year interest rate and one-yearinterest rates (current and expected next year).

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

The slope of the Yield Curve

•^

By looking at yields for bonds of different maturities, we can infer what financial markets expect short-term interest rateswill be in the future.

-^

An upward sloping yield curve means that long-term interestrates are higher than short-term interest rates. Financialmarkets expect short-term rates to be higher in the futuremarkets expect short term rates to be higher in the future.

-^

A downward sloping yield curve means that long-term interest

t^

l^

th

h^

t t

i t

t^

t^

Fi

i l

rates are lower than short-term interest rates. Financialmarkets expect short-term rates to be lower in the future.

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

-^

From

you get

i^

i^

i

e 1

1

2

1

2 ^

(^

e

i^

i^

i

^

The Yield curve

-^

From

you get

to find out what financial markets expect the 1-year interest

i^

i^

i

t^

t^

t

1

1

2

1

2

^

1 1

2

(^1

t

t^

t

i^

i^

i^

^

rate to be 1 year from now. E

l^

(UK

Fi

15 1) O

31 M

2009 th

-^

E

xample

(UK

-Fig.15.1). On 31 May 2009, the one-year

interest rate was 0,66%, the two-year interest rate 1,35%:thus markets expected the one-year interest rate one-year

p^

y^

y

later to be 2,04% (much higher).

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

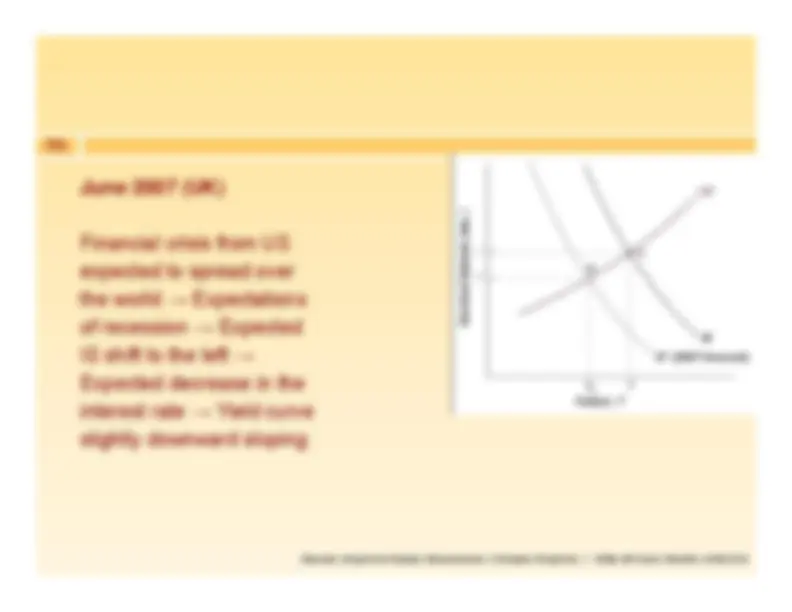

June 2007 (UK)June 2007 (UK) Financial crisis from US

t d t

d

expected to spread overthe world

→

Expectations

of recession

→

Expected

IS shift to the left

→

Expected decrease in theinterest rate

→

Yield curve

slightly downward sloping

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

Slide15.20^ From June 2007 to May 2009

The Yield curve

y

- The adverse shift in spending

was stronger than had been

t d Th

IS

hift d

expected. The

IS

curve shifted

much more to the left, to

IS’’.

- The Bank of England shifted in

g

early 2009 to a policy ofmonetary expansion, leadingto a downward shift in the

LM

to a downward shift in the

LM

curve, which made the interestrate even lower.

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010