Download Double Entry Bookkeeping: Principles, Rules, and Statement Prep and more Exams Business in PDF only on Docsity!

A GUIDE TO DOUBLE ENTRY BOOKKEEPING

BY MATT DAVIES, ASTON BUSINESS SCHOOL

PROJECT LEAD FOR THE FINANCIAL EDUCATION FOR FUTURE

ENTREPRENEURS (FEFE) PROJECT

By the end of this course you will be able to:

- Explain the 3 key principles of double entry bookkeeping

- Explain the rules of debits and credits for recording transactions

- Identify the correct double entry bookkeeping required for simple cash and credit transactions

- Identify the correct accounting required under both the perpetual and periodic inventory systems

- Identify which elements of financial statements typically have debit balances and which typically have credit balances at the end of a period

A Guide to Double Entry Bookkeeping:

Objectives

Double entry bookkeeping is based on 3 key principles:

- The ‘accounting equation’ principle: After every transaction is recorded the accounting equation is in balance: Assets = Liabilities + Equity, or, Assets – Liabilities = Equity

- The ‘dual effect’ principle: The are two effects for every transaction – a debit and credit.

- The ‘separate entity’ principle: The business is treated as a separate entity distinct from its owners.

Double Entry Bookkeeping:

3 Key Principles

The Accounting Equation

ASSETS = LIABILITIES + EQUITY

ASSETS – LIABILITIES = EQUITY

- The ‘general ledger’ (or ‘nominal ledger’) is the name of the book in which transactions are recorded

- The ledger is divided into sections called ‘accounts’

- Double-entry bookkeeping involves recording in the accounts the dual effect of each business transaction

- Each transaction requires a ‘debit’ entry to be made in one account and a corresponding ‘credit’ entry to be made to another account

The General Ledger

- ‘ Accounts’ are used to record the detailed increases and decreases for each item in the financial statements

- The simplest form of ‘account’ has 3 parts:

- The title

- Space for recording increases in the amount of the item

- Space for recording decreases in the amount of the item

- This simplified form of account is known as a ‘T account ’ (sometimes shortened to ‘T a/c’)

‘T Accounts’

- An entry on the DEBIT SIDE (the left hand side):

- an increase in an asset or expense or

- a decrease in a liability, equity or income

- An entry on the CREDIT SIDE (the right hand side):

- an increase in a liability, equity or income or

- a decrease in an asset or expense

- For every debit there must be an equal credit, so each transaction must be entered twice!

Debits and Credits

Rules of Debits and Credits

Accounting

Equation: Assets

= Liabilities^ +^ Equity

Statement of

Financial

Position Debit

Debit

Debit

Credit

Credit

Credit

Expenses Income

Debit

Credit

Debit

Credit

Statement of

Profit or Loss

Recording Cash Transactions

For cash transactions, it is easiest to consider the impact on cash first and the other half of the double entry second:

- An increase in cash (e.g. borrowing money, issuing shares, or the receipt of cash from customers) is recorded as a debit to the cash account

- A reduction in cash (i.e. payments made) is recorded as a credit to the cash account

Debits and Credits and Your Bank

Account

Money going out = a debit A Customer’s Bank Account Money going in = a credit The bank’s liability to the customer increases The bank’s liability to the customer reduces

Recording Credit Transactions

- Credit transactions are non-cash transactions

- Credit purchases involve an increase in a liability: trade payables. For example, the purchase of inventory on credit is recorded as follows: - Dr Inventory - Cr Trade payables

- Credit sales involve an increase in an asset: trade receivables. For example, the sale of goods on credit will be recorded as follows: - Dr Trade receivables - Cr Revenue

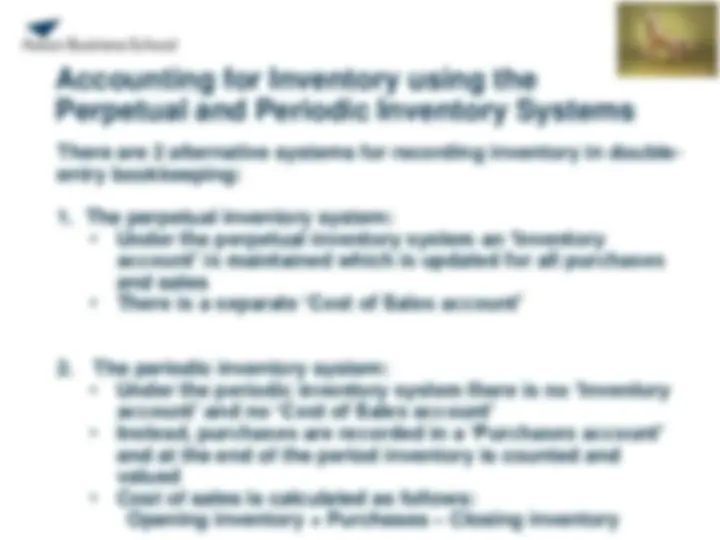

Accounting for Inventory using the

Perpetual and Periodic Inventory Systems

There are 2 alternative systems for recording inventory in double- entry bookkeeping:

- The perpetual inventory system:

- Under the perpetual inventory system an ‘Inventory account’ is maintained which is updated for all purchases and sales

- There is a separate ‘Cost of Sales account’

- The periodic inventory system:

- Under the periodic inventory system there is no ‘Inventory account’ and no ‘Cost of Sales account’

- Instead, purchases are recorded in a ‘Purchases account’ and at the end of the period inventory is counted and valued

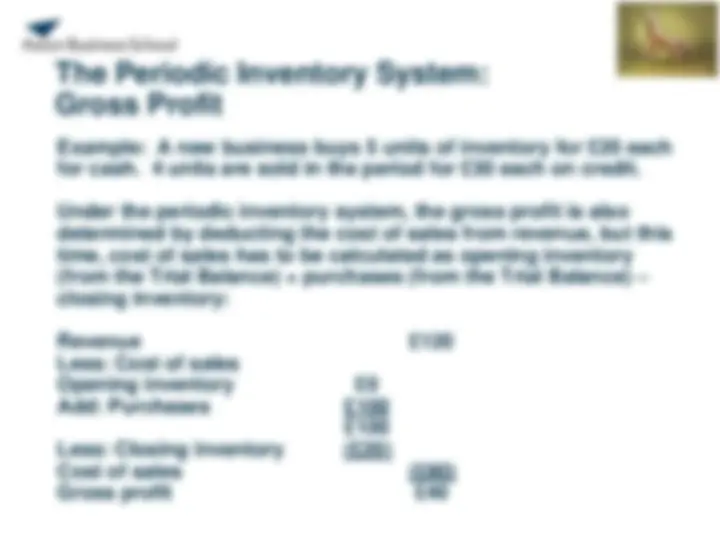

- Cost of sales is calculated as follows: Opening inventory + Purchases – Closing inventory

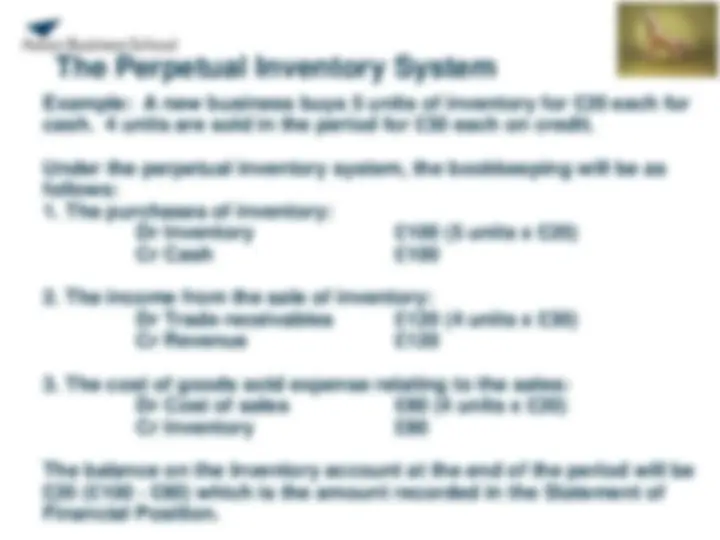

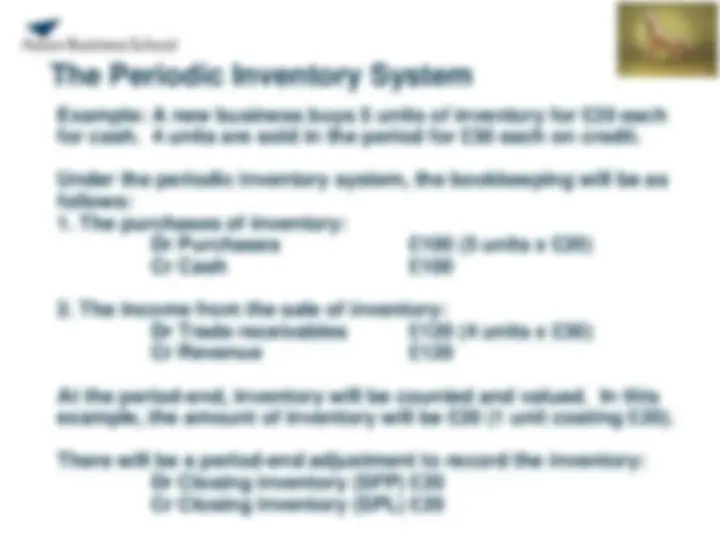

The Perpetual Inventory System

Example: A new business buys 5 units of inventory for £20 each for cash. 4 units are sold in the period for £30 each on credit. Under the perpetual inventory system, the bookkeeping will be as follows:

- The purchases of inventory: Dr Inventory £100 (5 units x £20) Cr Cash £

- The income from the sale of inventory: Dr Trade receivables £120 (4 units x £30) Cr Revenue £

- The cost of goods sold expense relating to the sales: Dr Cost of sales £80 (4 units x £20) Cr Inventory £ The balance on the Inventory account at the end of the period will be £20 (£100 - £80) which is the amount recorded in the Statement of Financial Position.