Download Introduction to Double-Entry Bookkeeping: Basic Principles and Applications and more Lecture notes Accounting in PDF only on Docsity!

Chapter 3: Double-Entry Bookkeeping^ •Double-entry bookkeeping underpins accounting•A way of systematically recording the financial transactions of acompany so that each transaction is recorded twice.•Basic accounting equation:

Assets = Liabilities + Equity + Profit (Income-Expenses)Assets + Expenses = Liabilities + Equity+ Income

Basic Rules1.

For every transaction there will be a

debit

and

credit entry

These debits and credits will be

equal and opposite

E.g. in bank account all records are

paid in

on

debit side

and

paid

out

on

credit side

•^

The choice of the right account sideis the core of the art of bookkeeping

-^

debiting an account

make an entry on the left-hand side of an

account

-^

crediting an account

make an entry on the right-hand side of an

account

Owner‘s Equity•^

Recall that owner‘s investments and revenues increase owner‘sequity, while owner‘s withdrawals and expenses decrease owner‘sequity.

-^

Frequently separate accounts are kept for these items.(a)

Owner‘s Capital

. This account is affected by, for example,

owner‘s investment.

-^

Increases in owner‘s capital are credited. Decreases in owner‘scapital are debited.

Owner's Capital Debit

Credit

for

for

Decrease

Increase

Owner‘s Withdrawals

(b)

Owner‘s Withdrawals

-^

The owner may, for example, withdraw cash for personal use. Itcould be debited directly to Owner‘s Capital but a separate accountis kept to determine total withdrawals.

-^

Increases in owner‘s withdrawals are debited. Decreases in owner‘swithdrawals are credited.

Owner's Withdrawal^ Debit

Credit

for

for

Increase

Decrease

Balancing off the accountsWhen all entries completed, we need to balanceoff the accounts•^

All Income Statement items will be closed off

-^

All Balance Sheet items brought forward

-^

Balancing off enables us to:1.

Prepare a trial balance

Close down income and expense accounts

Bring forward assets, liabilities and equity

Balancing off the cash account1.

Sum the entries on the larger side below the line

repeat the sum below the line on the other side

strike the balance: insert the amount missing such that the sums ofentries on both sides are equal (i.e. solving the account equation)

enter the counter item to the appropriate account e.g. Trial Balance Beginning balance 100Inflows

400200300

Outflows

400

Cash 1.^1000

4.^

Cash 600

Trial Balance

2.^

1000

3.^

Balance 600

Booking of the counter item (in theory)•^

appropriate account need not be the trial balance–

could be a hierarchically superior closing account, e.g. “cash and cashequivalents”– this could be closed to the balance sheet– in order to reopen accounts for the next period the line item cash andcash equivalents in the balance sheet could be counterbooked to anaccount which is closed by booking out the individual items to therespective accounts, e.g. the cash account for the next period

-^

This is not the practical procedure, this theoretically possibleprocedure shall only make clear the mechanics of double entrybookkeeping

Example

A small company named ZiscoSys. The transactions are stated inchronological order: (1) € 8.000 Owner‘s Investment to start up the business(2) Purchase of equipment for € 4.000 paid in cash(3) Purchase of supplies on credit for € 500(4) € 400 payment of a liability (accounts payable resulting from

delivery of supplies) (5) € 5.000 revenues earned on credit(6) € 3.000 collection of accounts receivable(7) Incurring expenses of € 500 for rent (cash) and € 200 (on credit) for

utility and prepaid insurance of € 1. (8) reception of a down payment of € 2.400 for services to be

performed (unearned revenue or deferred revenue), and (9) Owner‘s withdrawal of € 800.

Accounts Receivable

Revenues

Transaction 5 – services rendered on credit

Increase in accounts receivable is debited; incr. in revenues is credited.

Prepaid Insurance

Cash

Transaction 7 – insurance policy bought

Increase in prepaid insurance is debited; decrease in cash is credited.

Asset Accounts

Cash

Accounts Receivable

Equipment

Supplies

Prepaid Insurance

500

400

(^500) 1.200 800

6.

2.

4.

500

1.

Liability Accounts^ Accounts Payable

Unearned Revenue

400

500

200 300

2.

Owner's Equity Accounts Owner's Investment

Owner's Withdrawal

800

8.

800

Revenues

Expenses

500200

5.

700

Some important accounts commonto most enterprises^ Chart of Accounts for a Small Business

Assets

Liabilities

Revenues

Cash

111

Notes Payable

211

Sales

411

Notes Receivable

112

Accounts Payable

212

Commissions Earned

412

Accounts Receivable

113

Wages Payable

213

Fees Receivable

114

Unearned Revenues

231

Expenses

Office Supplies

115

Prepaid Rent

116

Owner's Equity

Wages Expense

511

Prepaid Insurance

117

Utility Expense

512

Land

141

Capital

311

Telephone Expense

513

Building

142

Withdrawal

312

Insurance Expense

514

Equipment

148

Income Summary

313

Depreciation Expense,

521

EquipmentDepreciation Expense,

522

Building

- For tractability reasons, accounts are numbered!

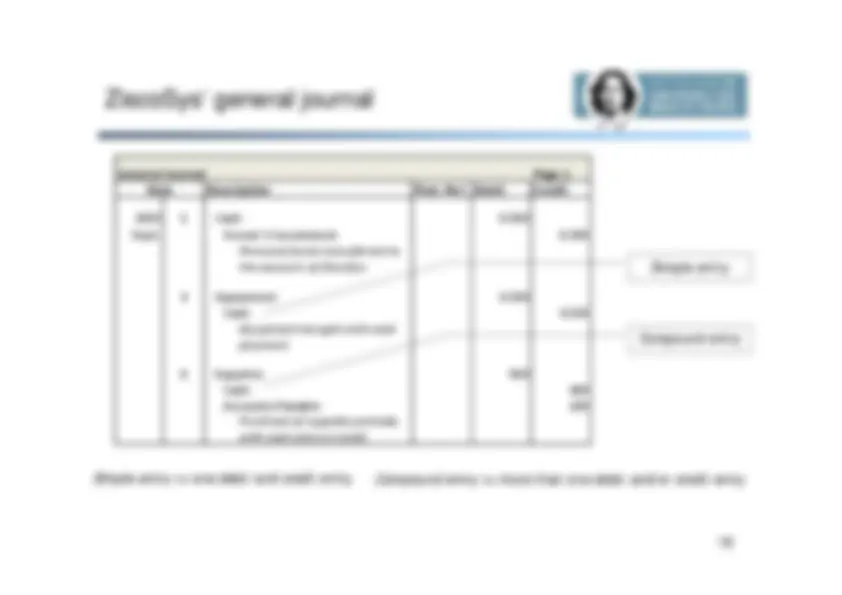

The Recording ProcessStep 1: Journalizing•^

The journal is a complete and chronological list of all transactionsthat occurred.

^

journal is the book of original entry!

•^

common to have more than one kind of journal

special purpose

journals, e.g. cash receipts journal or sales journal

-^

general journal: all transactions are recorded in this journal

-^

a complete entry provides the following information–

date of recording– date of transaction– accounts and amounts to be debited and credited– short explanation of the transaction– number of account (if posted)

Journal: the basic accounting document•^

The journal contains the complete information on transactions thatenter the accounting system–

it is the basic documentation and serves as instrument of evidence inlitigation– it is not allowed to cancel journal entries

-^

mistaken entries have to be reversed by a contra-entry

•^

In electronic accounting systems the journal is the only data base ontransactions–

the system has to assure that once an entry is made, it can no longer beinfluenced or altered by anyone– ledger accounts are „views“ of the data base that are generated online,they are not records in their own right (Principle of data integrity: anyinformation is only stored once)

-^

the system of ledger accounts can thus be altered at any timeaccording to new needs for analysis

-^

A sufficient number of safety copies (mirror images) of the journal haveto be kept up-to-date.

Step 2: Posting•^

all accounts taken together in one file

the ledger

•^

process of transferring journal entries to the ledger accounts

posting

-^

as with journals, there may be more than one kind of ledger

-^

general ledger contains all accounts

general ledger

asset accounts

owner‘s equity accounts

liability accounts

accounts receivable^ prepaid expenses

equipment cash

accounts payable^ unearned revenues

bonds notes payable

owner‘s withdrawal^ expenses

revenues owner‘s capital