Download Chapter 12 solutions and more Schemes and Mind Maps Accounting in PDF only on Docsity!

CHAPTER 12

Accounting for Partnerships and

Limited Liability COMPANIES

QUESTION INFORMATION

Number Objective Description Difficulty Time AACSB AICPA SS GL EO12-1 12-1 Easy 5 min Analytic FN-Measurement EO12-2 12-1 Easy 5 min Analytic FN-Measurement EO12-3 12-1 Easy 5 min Analytic FN-Measurement EO12-4 12-1 Easy 5 min Analytic FN-Measurement EO12-5 12-1 Easy 5 min Analytic FN-Measurement EO12-6 12-2 Easy 5 min Analytic FN-Measurement EO12-7 12-3 Easy 5 min Analytic FN-Measurement EO12-8 12-3 Easy 5 min Analytic FN-Measurement EO12-9 12-3 Easy 5 min Analytic FN-Measurement EO12-10 12-3 Easy 5 min Analytic FN-Measurement EO12-11 12-3 Easy 5 min Analytic FN-Measurement EO12-12 12-3 Easy 5 min Analytic FN-Measurement EO12-13 12-3 Easy 5 min Analytic FN-Measurement EO12-14 12-4 Easy 5 min Analytic FN-Measurement EO12-15 12-5 Easy 5 min Analytic FN-Measurement PE12-1A 12-2 Journalize partner's original investment

Easy 5 min Analytic FN-Measurement

PE12-1B 12-2 Journalize partner's original investment

Easy 5 min Analytic FN-Measurement

PE12-2A 12-2 Dividing partnership net income

Easy 5 min Analytic FN-Measurement

PE12-2B 12-2 Dividing partnership net loss

Easy 5 min Analytic FN-Measurement

PE12-3A 12-3 Revalue assets and contribute assets to a partnership

Easy 5 min Analytic FN-Measurement

PE12-3B 12-3 Revalue assets and contribute assets to a partnership

Easy 5 min Analytic FN-Measurement

PE12-4A 12-3 Partner bonus Easy 5 min Analytic FN-Measurement PE12-4B 12-3 Partner bonus Easy 5 min Analytic FN-Measurement PE12-5A 12-4 Liquidating partnerships-gain

Easy 5 min Analytic FN-Measurement

PE12-5B 12-4 Liquidating partnerships-gain

Easy 5 min Analytic FN-Measurement

PE12-6A 12-4 Liquidating partnerships-deficiency

Easy 5 min Analytic FN-Measurement

PE12-6B 12-4 Liquidating partnerships-deficiency

Easy 5 min Analytic FN-Measurement

Ex12-1 12-2 Record partner's original investment

Easy 10 min Analytic FN-Measurement

Ex12-2 12-2 Record partner's original investment

Easy 10 min Analytic FN-Measurement

Ex12-3 12-2 Dividing partnership income

Easy 15 min Analytic FN-Measurement

Ex12-4 12-2 Dividing partnership income

Easy 15 min Analytic FN-Measurement

Ex12-5 12-2 Dividing partnership net loss

Easy 5 min Analytic FN-Measurement

Ex12-6 12-2 Negotiating income- sharing ratio

Moderate 10 min Analytic FN-Measurement

Ex12-7 12-2 Dividing LLC income Easy 10 min Analytic FN-Measurement Ex12-8 12-2, 12-5 Dividing LLC net income and statement of member's equity

Moderate 15 min Analytic FN-Measurement

Ex12-9 12-2, 12-3 Partner income and withdrawal journal entries

Moderate 15 min Analytic FN-Measurement

Ex12-10 12-3 Admitting new partners Easy 5 min Analytic FN-Measurement Ex12-11 12-3 Admitting new partners Moderate 15 min Analytic FN-Measurement Ex12-12 12-3 Admitting new partners who buy an interest and contribute assets

Easy 10 min Analytic FN-Measurement

Ex12-13 12-3 Admitting new partner who contributes assets

Easy 10 min Analytic FN-Measurement

Ex12-14 12-3 Admitting new LLC member

Moderate 15 min Analytic FN-Measurement

Ex12-15 12-3 Admitting new partner with bonus

Moderate 15 min Analytic FN-Measurement

Ex12-16 12-2, 12-3, 12-

Partner bonuses, statement of partners' equity

Moderate 20 min Analytic FN-Measurement Exl

Ex12-17 12-3 Withdrawal of partner Moderate 15 min Analytic FN-Measurement Ex12-18 12-2, 12-3, 12-

Statement of members' equity, admitting new member

Difficult 20 min Analytic FN-Measurement

Ex12-19 12-4 Distribution of cash upon liquidation

Easy 5 min Analytic FN-Measurement

Ex12-20 12-4 Distribution of cash upon liquidation

Easy 5 min Analytic FN-Measurement

Ex12-21 12-4 Liquidating partnerships-capital deficiency

Easy 15 min Analytic FN-Measurement

Ex12-22 12-4 Distribution of cash upon liquidation

Easy 10 min Analytic FN-Measurement

Ex12-23 12-4 Liquidating partnerships-capital deficiency

Easy 5 min Analytic FN-Measurement

Ex12-24 12-4 Statement of partnership equity

Moderate 15 min Analytic FN-Measurement Exl

Ex12-25 12-4 Statement of LLC liquidation

Moderate 15 min Analytic FN-Measurement Exl

Ex12-26 12-2, 12-5 Partnership entries and statement of partners' equity

Moderate 15 min Analytic FN-Measurement Exl

Ex12-27 FAI Financial analysis and interpretation

Easy 10 min Analytic FN-Measurement

Ex12-28 FAI Financial analysis and interpretation

Easy 10 min Analytic FN-Measurement

Pr12-1A 12-2 Entries and balance sheet for partnership

Moderate 1 hr Analytic FN-Measurement Exl KA

Pr12-2A 12-2 Dividing partnership income

Moderate 1 hr Analytic FN-Measurement

EYE OPENERS

1. Proprietorship: Ease of formation and nontaxable entity. Partnership: Expanded owner expertise and capital, nontaxable entity, and ease of formation. Limited liability company: Limited liability to owners, expanded access to capital, nontaxable entity, and ease of formation. 2. The disadvantages of a partnership are its life is limited, each partner has unlimited liability, one partner can bind the partnership to contracts, and raising large amounts of capital is more difficult for a partnership than a limited liability company. 3. Yes. A partnership may incur losses in excess of the total investment of all partners. The division of losses among the partners would be made according to their agreement. In addition, because of the unlimited liability of each partner for partnership debts, a particular partner may actually lose a greater amount than his or her capital balance. 4. The partnership agreement (partnership) or operating agreement (LLC) establishes the income-sharing ratio among the partners (members), amounts to be invested, and buy-sell agreements between the partners (members). In addition, for an LLC the operating agreement specifies if the LLC is owner-managed or manager-managed. 5. Equally. 6. No. Maholic would have to bear his share of losses. In the absence of any agreement as to division of net income or net loss, his share would be one-third. In addition, because of the unlimited liability of each partner, Maholic may lose more than one- third of the losses if one partner is unable to absorb his share of the losses. 7. The delivery equipment should be recorded at $10,000, the valuation agreed upon by the partners. 8. The accounts receivable should be recorded by a debit of $150,000 to Accounts Receivable and a credit of $15,000 to Allowance for Doubtful Accounts. 9. Yes. Partnership net income is divided according to the income-sharing ratio, regardless of the amount of the withdrawals by the partners. Therefore, it is very likely that the partners’ monthly withdrawals from a partnership will not exactly equal their shares of net income. 10. a. Debit the partner’s drawing account and credit Cash. b. No. Payments to partners and the division of net income are separate. The amount of one does not affect the amount of the other. c. Debit the income summary account for the amount of the net income and credit the partners’ capital accounts for their respective shares of the net income. 11. a. By purchase of an interest, the capital interest of the new partner is obtained from the old partner, and neither the total assets nor the total equity of the partnership is affected. b. By investment, both the total assets and the total equity of the partnership are increased. 12. It is important to state all partnership assets in terms of current prices at the time of the admission of a new partner because failure to do so might result in participation by the new partner in gains or losses attributable to the period prior to admission to the partnership. To illustrate, assume that A and B share net income and net loss equally and operate a partnership that owns land recorded at and costing $20,000. C is admitted to the partnership, and the three partners share in income equally. The day after C is admitted to the partnership, the land is sold for $35,000 and, since the land was not revalued, C receives one-third distribution of the $15,000 gain. In this case, C participates in the gain attributable to the period prior to admission to the partnership. 13. A new partner who is expected to improve the fortunes (income) of the partnership, through such things as reputation or skill, might be given equity in excess of the amount invested to join the partnership. 14. a. Losses and gains on realization are divided among partners in the income- sharing ratio.

b. Cash is distributed to the partners according to their ownership claims, as indicated by the credit balances in their capital accounts, after taking into consideration the potential deficiencies that may result from the inability to collect from a deficient partner.

15. The statement of partners’ equity (for a partnership) and statement of members’ equity (for an LLC) both show the material changes in owner’s equity for each ownership person or class for a specified period.

Deduct excess of allowances over income (16,000)*

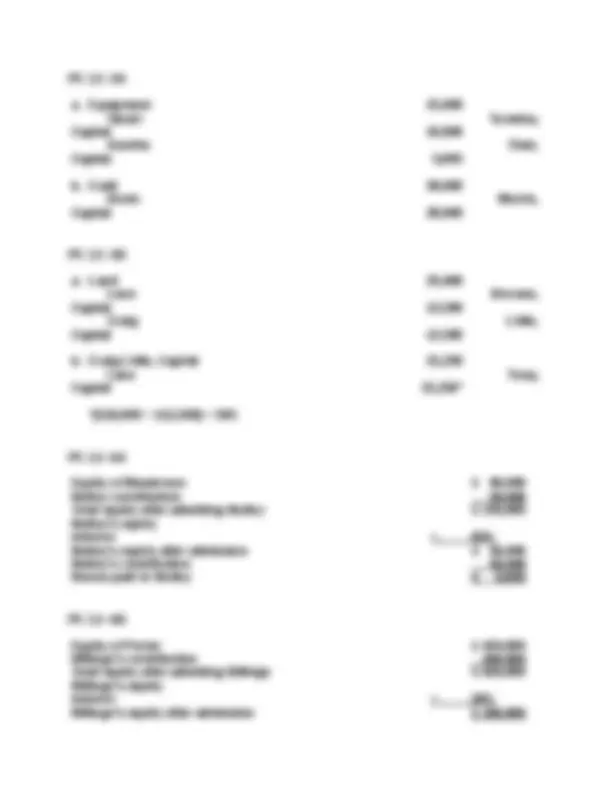

PE 12–3A

a. Equipment 15, Stuart Townley, Capital 10, Ayesha Starr, Capital 5,

b. Cash 28, Devin Morris, Capital 28,

PE 12–3B

a. Land 25, Leon Browne, Capital 12, Craig Little, Capital 12,

b. Craig Little, Capital 15, Lane Tway, Capital 15,250*

*($18,000 + $12,500) × 50%

PE 12–4A

Equity of Masterson $ 90, Nutley contribution 50, Total equity after admitting Nutley $ 140, Nutley’s equity interest × 40% Nutley’s equity after admission $ 56, Nutley’s contribution 50, Bonus paid to Nutley $ 6,

PE 12–4B

Equity of Porter $ 420, Billings’s contribution 200, Total equity after admitting Billings $ 620, Billings’s equity interest × 30% Billings’s equity after admission $ 186,

PE 12–5A

Chow’s equity prior to liquidation $ 1 8,

Realization of asset sales $ 46, Book value of assets ($18,000 + $25,000 + $1,000) 44, Gain on liquidation $ 2, Chow’s share of gain (50% × $2,000) 1 , Chow’s cash distribution $ 1 9,

PE 12–5B

Dickens’s equity prior to liquidation $ 5 5,

Realization of asset sales $ 75, Book value of assets ($55,000 + $45,000 + $10,000) 110, Loss on liquidation $ 35, Dickens’s share of loss (50% × $35,000) ( 17,500) Dickens’s cash distribution $ 3 7,

PE 12–6A

a. Martin’s equity prior to liquidation $ 8 ,

Realization of asset sales $ 5, Book value of assets 28, Loss on liquidation $ 23, Martin’s share of loss (50% × $23,000) ( 11,500)

Martin’s deficiency $ ( 3,500)

b. $5,000. $20,000 – $11,500 share of loss – $3,500 Martin deficiency, also equals the amount realized from asset sales.

PE 12–6B

a. Mee’s equity prior to liquidation $ 4 0,

Realization of asset sales $ 50, Book value of assets 160, Loss on liquidation $110, Mee’s share of loss (50% x $110,000) ( 55,000) Mee’s deficiency $ ( 15,000)

b. $50,000. $120,000 – $55,000 share of loss – $15,000 Mee deficiency, also equal to the amount realized from asset sales.

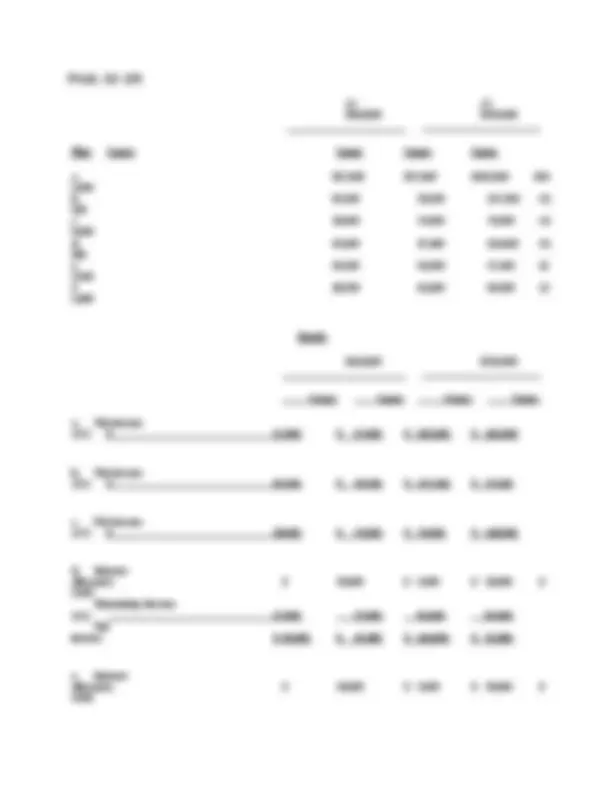

Ex. 12–

Haley Mano s

a. $ 75, $75, b. 112, 37, c. 68, 81, d. 67, 82, e. 73, 76,

Details

Haley Manos Total

a. Net income (1:1) $ 75,000 $ 75,000 $150,

b. Net income (3:1) $112,500 $ 37,500 $150,

c. Interest allowance $ 18,000 $ 6, $ 24, Remaining income (2:3) 50,400 75,600 126, Net income $ 68,400 $ 81,600 $150,

d. Salary allowance $ 45,000 $ 60, $105, Remaining income (1:1) 22,500 22,500^ 45, Net income $ 67,500 $ 82,500 $150,

e. Interest

allowance $ 18,000 $ 6, $ 24,

Salary allowance 45,

60,000 105, Remaining income

(1:1) 10,500 10,500^ 21, Net income $ 73,500 $ 76,500 $150,

e. Interest allowance $ 18,000 $ 6, $ 24, Salary allowance 45,000 60, 105, Remaining income (1:1) 55,500 55,500 111, Net income $118,500 $121, $240,

3. 1 Ex. 12–

Curt Greg Kelly Kaufman^ Total

Salary allowances $ 45,000 $ 30, $ 75, Remainder (net loss, $25,000 plus $75, salary allowances) divided equally (50,000)^ (50,000) (100,000)

Net loss $ (5,000) $ (20,000)

$ (25,000)

Ex. 12–

The partners can divide net income in any ratio that they wish. However, in the absence of an agreement, net income is divided equally between the partners. Therefore, Jan’s conclusion was correct, but for the wrong reasons. In addition, note that the monthly drawings have no impact on the division of income.

3. 2 Ex. 12–

a.

Net income: $132,

Gardner Ross Total

Salary allowance $58,000 $42, $100, Remaining income 19,200 12, 32, Net income $77,200 $54, $132,

Gardner remaining income: ($132,000 – $100,000) × 3/ Ross remaining income: ($132,000 – $100,000) × 2/

b.

(1)

Income Summary 132, L. Gardner, Member Equity 77, L. Ross, Member Equity 54,

(2)

L. Gardner, Member Equity 58, L. Ross, Member Equity 42, L. Gardner, Drawing 58, L. Ross, Drawing 42,

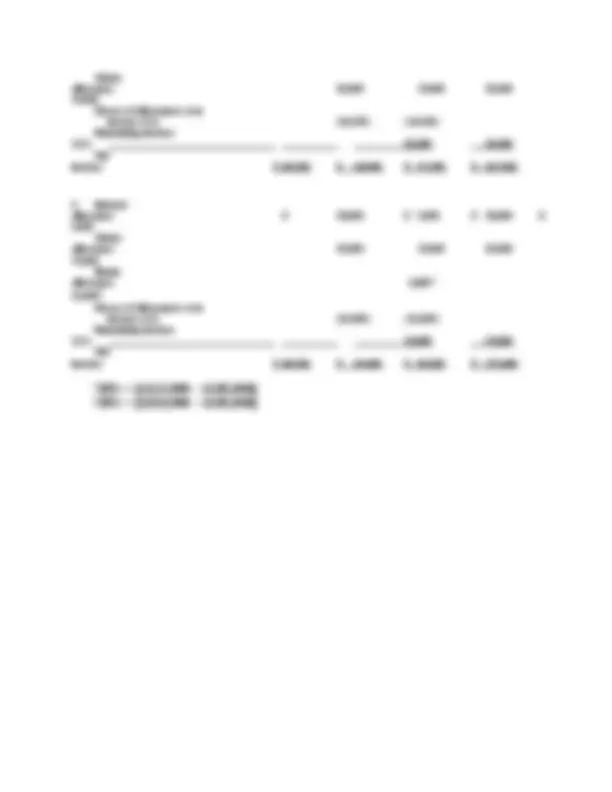

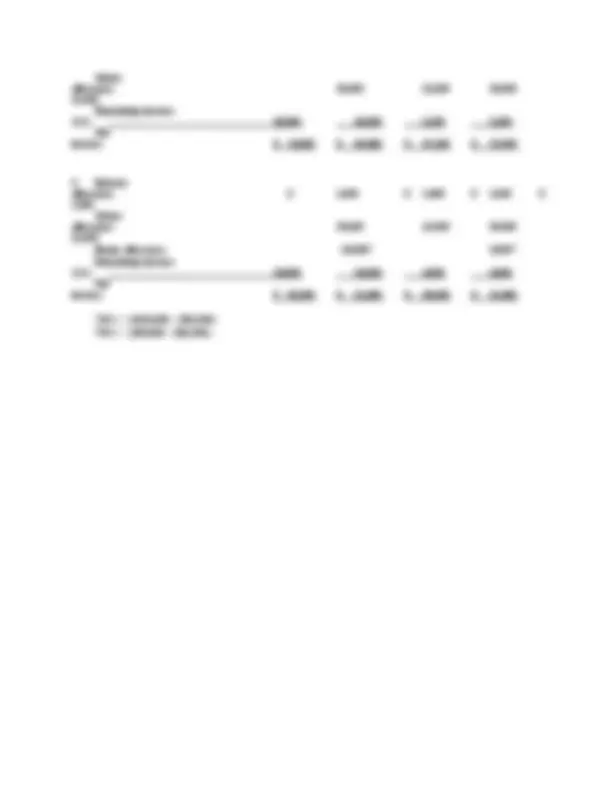

Ex. 12–

a. Daily Sun KXT Radio Rachel Newspaper, Partners Sizemore LLC Total

Salary allowance $139, $139, Interest allowance $ 19,200^1 3,200 2 $ 12,800^3 35, Remaining income (4:3:3) 158,000 118,500 118, 395, Net income $177,200 $261,500^ $131, $570,

(^1) 8% × $240, (^2) 8% × $40, (^3) 8% × $160,

b.

Dec. 31, 2008 Income Summary 570, KXT Radio Partners, Member Equity 177, Rachel Sizemore, Member Equity 261, Daily Sun Newspaper, LLC, Member Equity 131,

Dec. 31, 2008 KXT Radio Partners, Member Equity 19, Rachel Sizemore, Member Equity 143, Daily Sun Newspaper, LLC, Member Equity 12, KXT Radio Partners, Drawing 19, Rachel Sizemore, Drawing 143,

Daily Sun Newspaper, LLC, Drawing 12,

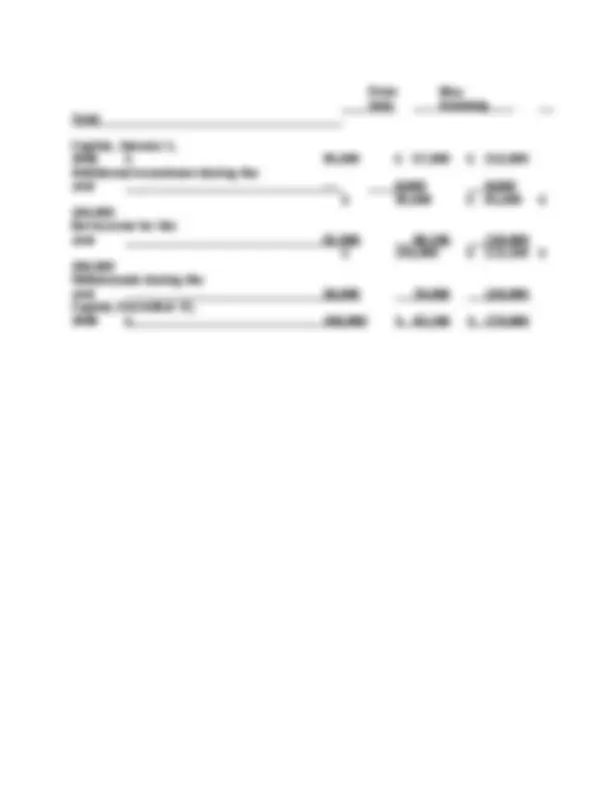

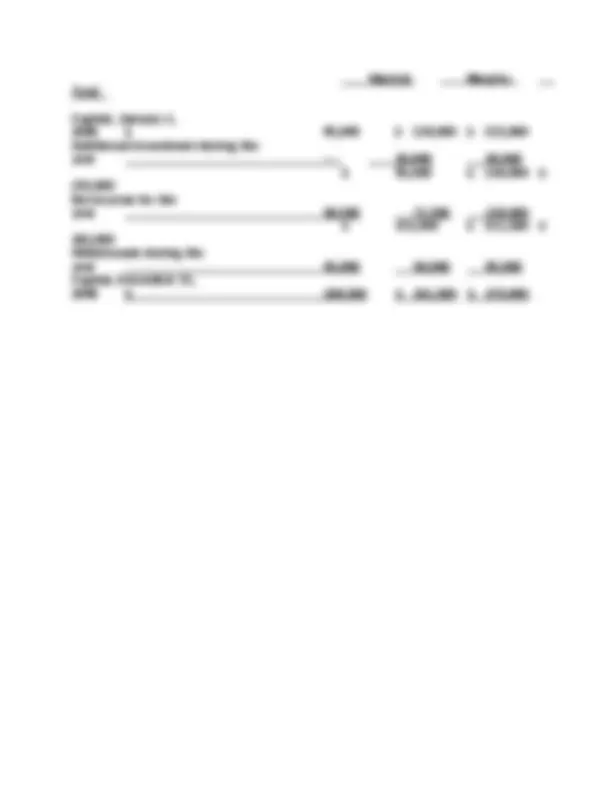

c. Media Properties, LLC Statement of Members’ Equity For the Year Ended December 31, 2008

KXT Daily Sun Radio Rachel Newspaper, Partners Sizemore LLC Total

Members’ equity, January 1, 2008 $240,000 $ 40,000 $160,000 $ 440,

Additional investment during the year 50,000 50, $290,000 $ 40,000 $160,000 $ 490,

Net income for the year 177,200 261,500^ 131,300^ 570, $467,200 $301,500 $291,300 $1,060,

Withdrawals during the year 19,200 143,000^ 12,800^ 175, Members’ equity, December 31, 2008 $448,000 $158,500 $278,500 $ 885,