Download Chapter 13 solutions and more Schemes and Mind Maps Accounting in PDF only on Docsity!

CHAPTER 13

CORPORATIONS: ORGANIZATION, STOCK

TRANSACTIONS, AND DIVIDENDS

QUESTION INFORMATION

Number Objective Description Difficulty Time AACSB AICPA SS GL

Q13-1 13-1 Easy 5 min Analytic FN-Measurement

Q13-2 13-1 Easy 5 min Analytic FN-Measurement

Q13-3 13-3 Easy 5 min Analytic FN-Measurement

Q13-4 13-3 Easy 5 min Analytic FN-Measurement

Q13-5 13-3 Easy 5 min Analytic FN-Measurement

Q13-6 13-3 Easy 5 min Analytic FN-Measurement

Q13-7 13-4 Easy 5 min Analytic FN-Measurement

Q13-8 13-4 Easy 5 min Analytic FN-Measurement

Q13-9 13-4 Easy 5 min Analytic FN-Measurement

Q13-10 13-4 Easy 5 min Analytic FN-Measurement

Q13-11 13-5 Easy 5 min Analytic FN-Measurement

Q13-12 13-5 Easy 5 min Analytic FN-Measurement

Q13-13 13-5 Easy 5 min Analytic FN-Measurement

Q13-14 13-6 Easy 5 min Analytic FN-Measurement

Q13-15 13-6 Easy 5 min Analytic FN-Measurement

Q13-16 13-6 Easy 5 min Analytic FN-Measurement

Q13-17 13-6 Easy 5 min Analytic FN-Measurement

Q13-18 13-7 Easy 5 min Analytic FN-Measurement

PE13-1A 13-3 Dividends per share Easy 10 min Analytic FN-Measurement

PE13-1B 13-3 Dividends per share Easy 10 min Analytic FN-Measurement

PE13-2A 13-3 Entries for issuing stock Easy 5 min Analytic FN-Measurement

PE13-2B 13-3 Entries for issuing stock Easy 5 min Analytic FN-Measurement

PE13-3A 13-4 Entries for cash dividends

Easy 5 min Analytic FN-Measurement

PE13-3B 13-4 Entries for cash dividends

Easy 5 min Analytic FN-Measurement

PE13-4A 13-4 Entries for stock dividends

Easy 10 min Analytic FN-Measurement

PE13-4B 13-4 Entries for stock dividends

Easy 10 min Analytic FN-Measurement

PE13-5A 13-5 Entries for treasury stock

Easy 10 min Analytic FN-Measurement

PE13-5B 13-5 Entries for treasury stock

Easy 10 min Analytic FN-Measurement

PE13-6A 13-6 Stockholders' equity section of balance sheet

Easy 5 min Analytic FN-Measurement

PE13-6B 13-6 Stockholders' equity section of balance sheet

Easy 5 min Analytic FN-Measurement

PE13-7A 13-6 Retained earnings statement

Easy 5 min Analytic FN-Measurement

PE13-7B 13-6 Retained earnings statement

Easy 5 min Analytic FN-Measurement

Ex13-1 13-3 Dividends per share Easy 10 min Analytic FN-Measurement

Ex13-2 13-3 Dividends per share Easy 10 min Analytic FN-Measurement

Ex13-3 13-3 Entries for issuing par stock

Easy 10 min Analytic FN-Measurement

Ex13-4 13-3 Entries for issuing no- par stock

Easy 10 min Analytic FN-Measurement

Ex13-5 13-3 Issuing stock for assets other than cash

Easy 5 min Analytic FN-Measurement

Ex13-6 13-3 Selected stock transactions

Easy 15 min Analytic FN-Measurement

Ex13-7 13-3 Issuing stock Moderate 10 min Analytic FN-Measurement

Ex13-8 13-3 Issuing stock Easy 10 min Analytic FN-Measurement

Ex13-9 13-4 Entries for cash dividends

Easy 10 min Analytic FN-Measurement

Ex13-10 13-4 Entries for stock dividends

Moderate 15 min Analytic FN-Measurement

Ex13-11 13-5 Treasury stock transactions

Moderate 15 min Analytic FN-Measurement

Ex13-12 13-5, 13-6 Treasury stock transactions

Moderate 15 min Analytic FN-Measurement

Ex13-13 13-5, 13-6 Treasury stock transactions

Moderate 15 min Analytic FN-Measurement

Ex13-14 13-6 Reporting paid-in- capital

Easy 10 min Analytic FN-Measurement

Ex13-15 13-6 Stockholders' equity section of balance sheet

Easy 10 min Analytic FN-Measurement

Ex13-16 13-6 Stockholders' equity section of balance sheet

Easy 10 min Analytic FN-Measurement

Ex13-18 13-6 Retained earnings statement

Easy 10 min Analytic FN-Measurement

Ex13-17 13-6 Stockholders' equity section of balance sheet

Moderate 15 min Analytic FN-Measurement

Ex13-19 13-6 Statement of stockholders' equity

Moderate 15 min Analytic FN-Measurement Exl

Ex13-20 13-7 Effect of stock split Easy 5 min Analytic FN-Measurement

Ex13-21 13-7 Effect of cash dividend and stock split

Easy 5 min Analytic FN-Measurement

Ex13-22 13-7 Selected dividend transactions, stock split

Moderate 15 min Analytic FN-Measurement

Ex13-23 FAI Dividend yield Easy 5 min Analytic FN-Measurement

Ex13-24 FAI Dividend yield Easy 10 min Analytic FN-Measurement

Ex13-25 FAI Dividend yield Moderate 10 min Analytic FN-Measurement

Pr13-1A 13-3 Dividends on preferred and common stock

Moderate 1 hr Analytic FN-Measurement Exl

Pr13-2A 13-3 Stock transactions for corporate expansion

Moderate 45 min Analytic FN-Measurement KA

Pr13-3A 13-3, 13-4, 13-

Selected stock transactions

Moderate 1 hr Analytic FN-Measurement KA

Pr13-4A 13-3, 13-4, 13-5, 13-

Entries for selected corporate transactions

Difficult 1 hr Analytic FN-Measurement Exl KA

Pr13-5A 13-3, 13-4, 13-5, 13-

Entries for selected corporate transactions

Moderate 1 hr Analytic FN-Measurement Exl KA

Pr13-1B 13-3 Dividends on preferred and common stock

Moderate 1 hr Analytic FN-Measurement Exl

EYE OPENERS

1. Each stockholder’s liability for corporation

debts is limited to the amount invested in the

corporation. A corporation is responsible for

its own obligations, and therefore, its

creditors may not look beyond the assets of

the corporation for satisfaction of their

claims.

2. The large investments needed by large

businesses are usually obtainable only

through the pooling of the resources of

many people. The corporation also has the

advantages over proprietorships and

partnerships of transferable shares of

ownership, and thus the continuity of

existence, and limited liability of its owners

(stockholders).

3. No. Common stock with a higher par is not

necessarily a better investment than com-

mon stock with a lower par because par is

an amount assigned to the shares.

4. The broker is not correct. Corporations are

not legally liable to pay dividends until the

dividends are declared. If the company that

issued the preferred stock has operating

losses, it could omit dividends, first, on its

common stock and, later, on its preferred

stock.

5. Factors influencing the market price of a

corporation’s stock include the following:

a. Financial condition, earnings record, and

dividend record of the corporation.

b. Its potential earning power.

c. General business and economic

conditions and prospects.

6. No. Premium on stock is additional paid-in

capital.

7. a. Sufficient retained earnings, sufficient

cash, and formal action by the board of

directors.

b. February 6, declaration date; March 9,

record date; and April 5, payment date.

8. The company may not have had enough

cash on hand to pay a dividend on the com-

mon stock, or resources may be needed for

plant expansion, replacement of facilities,

payment of liabilities, etc.

9. a. No change.

b. Total equity is the same.

10. a. Current liability

b. Stockholders’ equity

11. a. Unissued stock has never been issued,

but treasury stock has been issued as

fully paid and has subsequently been

reacquired.

b. As a deduction from the total of other

stockholders’ equity accounts.

12. a. It has no effect on revenue or expense.

b. It reduces stockholders’ equity by

13. a. It has no effect on revenue.

b. It increases stockholders’ equity by

14. The primary advantage of the combined

income and retained earnings statement is

that it emphasizes net income as the

connecting link between the income

statement and the retained earnings portion

of stockholders’ equity.

15. The three classifications of restrictions on

retained earnings are legal, contractual, and

discretionary. Appropriations are normally

reported in the notes to the financial

statements.

16. Such prior period adjustments should be

reported as an adjustment to the beginning

balance of retained earnings.

17. The statement of stockholders’ equity is

normally prepared when there are significant

changes in stock and other paid-in capital

accounts.

18. The primary purpose of a stock split is to

bring about a reduction in the market price

per share and thus to encourage more in-

vestors to buy the company’s shares.

2 PRACTICE EXERCISES

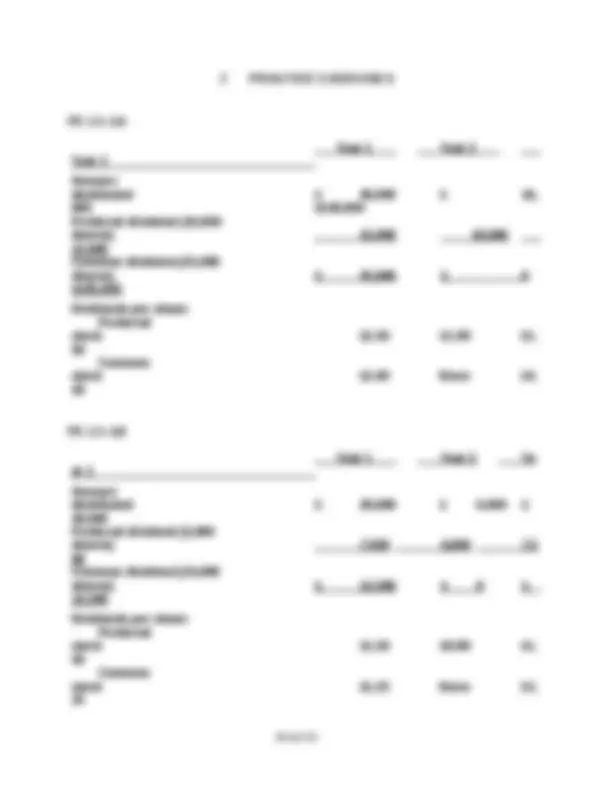

PE 13–1A

Year 1 Year 2 Year 3

Amount distributed $ 40,000 $ 10, 000 $120, Preferred dividend (10, shares) 15,000 10, 15, Common dividend (25, shares) $ 25,000 $^0 $105,

Dividends per share: Preferred stock $1.50 $1.00 $1. 50 Common stock $1.00 None $4. 20

PE 13–1B

Year 1 Year 2 Ye ar 3

Amount distributed $ 20,000 $ 4,000 $ 40, Preferred dividend (5, shares) 7,500 4,000 7, 00 Common dividend (10, shares) $ 12,500 $^0 $ 32,

Dividends per share: Preferred stock $1.50 $0.80 $1. 50 Common stock $1.25 None $3. 25

PE 13–2B

July 6Cash 960, Common Stock 960, (800,000 shares × $1.20).

Aug. 30 Cash 500, Preferred Stock 500, (10,000 shares × $50).

Oct. 14Cash 405, Preferred Stock 375, Paid-In Capital in Excess of Par 30, (7,500 shares × $54).

2. 2 PE 13–3A

July 16Cash Dividends 48, Cash Dividends Payable 48,

Aug. 15No entry required.

Sept. 30Cash Dividends Payable 48, Cash 48,

2. 3 PE 13–3B

Oct. 1Cash Dividends 90, Cash Dividends Payable 90,

Nov. 1No entry required.

Dec. 24Cash Dividends Payable 90, Cash 90,

PE 13–4A

Feb. 13Stock Dividends (300,000 × 3% × $63) 567, Stock Dividends Distributable (9,000 × $40) 360, Paid-In Capital in Excess of Par— Common Stock ($567,000 – $360,000) 207,

Mar. 14No entry required.

Apr. 30Stock Dividends Distributable 360, Common Stock 360,

PE 13–6A

Stockholders’ Equity Paid-in capital: Common stock, $80 par (30,000 shares authorized, 25,000 shares issued) $ 2,000, Excess of issue price over par 315,000 $ 2,315, From sale of treasury stock 33, Total paid-in capital $ 2,348, Retained earnings 1,112, Total $ 3,460, Deduct treasury stock (2,000 shares at cost) 180, Total stockholders’ equity $ 3,280,

PE 13–6B

Stockholders’ Equity Paid-in capital: Common stock, $75 par (50,000 shares authorized, 45,000 shares issued) $ 3,375, Excess of issue price over par 485,000 $ 3,860, From sale of treasury stock 18, Total paid-in capital $ 3,878, Retained earnings 1,452, Total $ 5,330, Deduct treasury stock (5,000 shares at cost) 420, Total stockholders’ equity $ 4,910,

PE 13–7A

DYNAMIC LEADERS INC. Retained Earnings Statement For the Year Ended July 31, 2008

Retained earnings, August 1, 2007 $ 988, Net income $325, Less dividends declared 125, Increase in retained earnings 200, Retained earnings, July 31, 2008 $ 1,188,

PE 13–7B

MAXIMA RETRACTORS INC. Retained Earnings Statement For the Year Ended October 31, 2008

Retained earnings, November 1,

2007 $

2,906,

Net income $553,

Less dividends declared 300,

Increase in retained

earnings

253,

Retained earnings, October 31, 2008 $ 3,159,

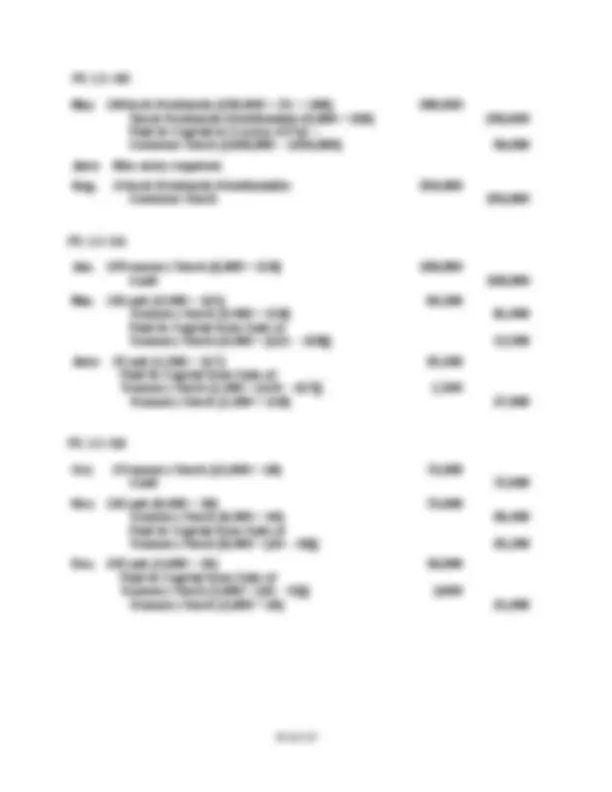

Ex. 13–

a. Feb. 4 Cash 1,920, Common Stock 600, Paid-In Capital in Excess of Par— Common Stock 1,320,

Mar. 31 Cash 1,620, Preferred Stock 1,350, Paid-In Capital in Excess of Par— Preferred Stock 270,

b. $3,540,000 ($1,920,000 + $1,620,000)

Ex. 13–

a. July 17 Cash 5,400, Common Stock 750, Paid-In Capital in Excess of Stated Value 4,650,

Sept. 20 Cash 800, Preferred Stock 500, Paid-In Capital in Excess of Par— Preferred Stock 300,

b. $6,200,000 ($5,400,000 + $800,000)

Ex. 13–

Nov. 10Land 480, Common Stock 120, Paid-In Capital in Excess of Par 360,

Paid-In Capital in Excess of Par—

- Ex. 13–

- Feb. 19Cash 1,500, - Common Stock 1,500,

- 27Organizational Expenses 7, - Common Stock 7,

- Mar. 13Land 80, - Buildings 350, - Equipment 45, - Common Stock 450, - Common Stock 25,

- May 6Cash 230, - Preferred Stock 200, - Preferred Stock 30, Paid-In Capital in Excess of Par—

- Ex. 13–

- July 2Cash Dividends 275, - Cash Dividends Payable 275,

- Sept. 1Cash Dividends Payable 275, Aug. 1No entry required. - Cash 275,

Ex. 13–

a. (1) Stock Dividends 720,000* Stock Dividends Distributable 600, Paid-In Capital in Excess of Par— Common Stock 120,

*[($30,000,000/$100) × $120] × 2%

(2) Stock Dividends Distributable 600, Common Stock 600,

b. (1) $34,500,000 ($30,000,000 + $4,500,000)

(2) $50,600,

(3) $85,100,000 ($34,500,000 + $50,600,000)

c. (1) $35,220,000 ($34,500,000 + $720,000)

(2) $49,880,000 ($50,600,000 – $720,000)

(3) $85,100,000 ($35,220,000 + $49,880,000)

Ex. 13–

a. May 2 Treasury Stock 216, Cash 216,

Aug. 14 Cash 190, Treasury Stock 180, Paid-In Capital from Sale of Treasury Stock 10,

Nov. 7 Cash 35, Paid-In Capital from Sale of Treasury Stock 1, Treasury Stock 36,

b. $9,000 credit

c. Mountain Springs may have purchased the stock to support the market price of the stock, to provide shares for resale to employees, or for reissuance to employees as a bonus according to stock purchase agreements.

Ex. 13–

Ex. 13–

a. Sept. 9 Treasury Stock 1,068, Cash 1,068,

Oct. 31 Cash 966, Treasury Stock 934, Paid-In Capital from Sale of Treasury Stock 31,

Dec. 4 Cash 85, Treasury Stock 80, Paid-In Capital from Sale of Treasury Stock 5,

b. $36,900 ($31,500 + $5,400) credit

c. $53,400 (600 × $89) debit

d. The balance in the treasury stock account is reported as a deduction from the total of the paid-in capital and retained earnings.

Ex. 13–

a. June 12 Treasury Stock 720, Cash 720,

Aug. 10 Cash 450, Treasury Stock 432, Paid-In Capital from Sale of Treasury Stock 18,

Dec. 20 Cash 282, Paid-In Capital from Sale of Treasury Stock 6, Treasury Stock 288,

b. $12,000 credit

c. Stockholders’ Equity section

d. Tacoma Inc. may have purchased the stock to support the market price of the

stock, to provide shares for resale to employees, or for reissuance to employees as a bonus according to stock purchase agreements.