Download Chapter 11 solutions and more Study Guides, Projects, Research Accounting in PDF only on Docsity!

CHAPTER 11

CURRENT LIABILITIES AND PAYROLL

QUESTION INFORMATION

Number Objective Description Difficulty Time AACSB AICPA SS GL EO11-1 11-1 Easy 5 min Analytic FN-Measurement EO11-2 11-1 Easy 5 min Analytic FN-Measurement EO11-3 11-2 Easy 5 min Analytic FN-Measurement EO11-4 11-2 Easy 5 min Analytic FN-Measurement EO11-5 11-2 Easy 5 min Analytic FN-Measurement EO11-6 11-2 Easy 5 min Analytic FN-Measurement EO11-7 11-3 Easy 5 min Analytic FN-Measurement EO11-8 11-3 Easy 5 min Analytic FN-Measurement EO11-9 11-3 Easy 5 min Analytic FN-Measurement EO11-10 11-4 Easy 5 min Analytic FN-Measurement EO11-11 11-4 Easy 5 min Analytic FN-Measurement EO11-12 11-5 Easy 5 min Analytic FN-Measurement EO11-13 11-5 Easy 5 min Analytic FN-Measurement EO11-14 11-5 Easy 5 min Analytic FN-Measurement PE11-1A 11-1 Calculate proceeds from notes payable

Easy 5 min Analytic FN-Measurement

PE11-1B 11-1 Calculate proceeds from notes payable

Easy 5 min Analytic FN-Measurement

PE11-2A 11-2 Calculate federal income tax withholding

Easy 5 min Analytic FN-Measurement

PE11-2B 11-2 Calculate federal income tax withholding

Easy 5 min Analytic FN-Measurement

PE11-3A 11-2 Calculate employee net pay

Easy 5 min Analytic FN-Measurement

PE11-3B 11-2 Calculate employee net pay

Easy 5 min Analytic FN-Measurement

PE11-4A 11-3 Journalize period payroll

Easy 5 min Analytic FN-Measurement

PE11-4B 11-3 Journalize period payroll

Easy 5 min Analytic FN-Measurement

PE11-5A 11-3 Journalize period payroll

Easy 5 min Analytic FN-Measurement

PE11-5B 11-3 Journalize period payroll

Easy 5 min Analytic FN-Measurement

PE11-6A 11-4 Journalize vacation pay and pension benefits

Easy 5 min Analytic FN-Measurement

PE11-6B 11-4 Journalize vacation pay and pension benefits

Easy 5 min Analytic FN-Measurement

PE11-7A 11-5 Journalize estimated warranty liability

Easy 10 min Analytic FN-Measurement

PE11-7B 11-5 Journalize estimated warranty liability

Easy 10 min Analytic FN-Measurement

Ex11-1 11-1 Current liabilities Easy 10 min Analytic FN-Measurement Ex11-2 11-1 Entries for discounting notes payable

Easy 15 min Analytic FN-Measurement

Ex11-3 11-1 Evaluate alternative notes

Moderate 15 min Analytic FN-Measurement

Ex11-4 11-1 Entries for notes payable

Easy 10 min Analytic FN-Measurement

Ex11-5 11-1 Entries for discounted notes payable

Easy 10 min Analytic FN-Measurement

Ex11-6 11-1 Fixed asset purchases with note

Moderate 15 min Analytic FN-Measurement

Ex11-7 11-1 Current portion of long- term debt

Easy 10 min Analytic FN-Measurement

Ex11-8 11-2 Calculate payroll Easy 10 min Analytic FN-Measurement Ex11-9 11-2 Calculate payroll Moderate 15 min Analytic FN-Measurement Ex11-10 11-2, 11-3 Summary payroll data Moderate 15 min Analytic FN-Measurement Ex11-11 11-3 Payroll tax entries Easy 10 min Analytic FN-Measurement Ex11-12 11-3 Payroll tax entries Easy 10 min Analytic FN-Measurement Ex11-13 11-3 Payroll tax entries Easy 10 min Analytic FN-Measurement Ex11-14 11-3 Payroll internal control procedures

Easy 10 min Analytic FN-Measurement

Ex11-15 11-3 Internal control procedures

Moderate 15 min Analytic FN-Measurement

Ex11-16 11-3 Payroll procedures Easy 5 min Analytic FN-Measurement Ex11-17 11-4 Accrued vacation pay Easy 5 min Analytic FN-Measurement Ex11-18 11-4 Pension plan entries Easy 10 min Analytic FN-Measurement Ex11-19 11-4 Defined benefit pension plan

Easy 5 min Analytic FN-Measurement

Ex11-20 11-5 Accrued product warranty

Easy 10 min Analytic FN-Measurement

Ex11-21 11-5 Accrued product warranty

Easy 5 min Analytic FN-Measurement

Ex11-22 11-5 Contingent liabilities Moderate 15 min Analytic FN-Measurement Ex11-23 FAI Quick ratio Easy 10 min Analytic FN-Measurement Ex11-24 FAI Quick ratio Easy 10 min Analytic FN-Measurement Pr11-1A 11-1, 11-5 Liability transactions Moderate 45 min Analytic FN-Measurement KA Pr11-2A 11-2, 11-3 Entries for payroll and payroll taxes

Moderate 1 hr Analytic FN-Measurement KA

Pr11-3A 11-2, 11-3 Wage and tax statement data and employer FICA

Difficult 1 1/4 hr Analytic FN-Measurement Exl

Pr11-4A 11-2, 11-3 Payroll register Moderate 1 hr Analytic FN-Measurement Pr11-5A 11-2, 11-3 Payroll register Difficult 1 1/4 hr Analytic FN-Measurement Exl Pr11-6A 11-2, 11-3, 11-

Payroll accounts and year-end entries

Difficult 2 hr Analytic FN-Measurement KA

Pr11-1B 11-1, 11-5 Liability transactions Moderate 45 min Analytic FN-Measurement KA Pr11-2B 11-2, 11-3 Entries for payroll and payroll taxes

Moderate 1 hr Analytic FN-Measurement KA

Pr11-3B 11-2, 11-3 Wage and tax statement data and employer FICA

Difficult 1 1/4 hr Analytic FN-Measurement Exl

Pr11-4B 11-2, 11-3 Payroll register Moderate 1 hr Analytic FN-Measurement Pr11-5B 11-2, 11-3 Payroll register Difficult 1 1/4 hr Analytic FN-Measurement Exl Pr11-6B 11-2 ,11-3, 11-

Payroll accounts and year-end entries

Difficult 2 hr Analytic FN-Measurement KA

Comp Problem 3

11-1, 11-2, 11-3, 11-4,11-

Journal entries, bank reconciliation, adjusting entries, balance sheet

Difficult 3 hr Analytic FN-Measurement KA

SA11-1 11-3 Ethics and professional conduct

Easy 15 min Ethics BB-Industry

EYE OPENERS

- A discounted note payable has no stated interest rate, but provides interest by discounting the note proceeds. The discount, which is the difference between the proceeds and the face of the note, is the interest and is accounted for as such.

- a. Income or withholding taxes, social security, and Medicare b. Employees Federal Income Tax Payable, Social Security Tax Payable, and Medicare Tax Payable.

- There is a ceiling on (c) the social security portion of the FICA tax and (d) the federal unemployment compensation tax.

- The deductions from employee earnings are for amounts owed (liabilities) to others for such items as federal taxes, state and local income taxes, and contributions to pension plans.

- Yes. Unemployment compensation taxes are paid by the employer on the first $7, of annual earnings for each employee. Therefore, hiring two employees, each earning $12,500 per year, would require the payment of twice the unemployment tax than if only one employee, earning $25,000, was hired.

- a

- c

- c

- b

- b

- The use of special payroll checks relieves the treasurer or other executives of the task of signing a large number of regular checks each payday. Another advantage of this system is that reconciling the regular bank statement is simplified. The paid payroll checks are returned by the bank separately from regular checks and are accompanied by a statement of the special bank account. Any balance shown on the bank’s statement will correspond to the sum of the payroll checks outstanding because the amount of each deposit is exactly the same as the total amount of checks drawn.

- a. Input data that remain relatively unchanged from period to period (and therefore do not need to be reintroduced

into the system frequently) are called constants. b. Input data that differ from period to period are called variables.

- a. If employees’ attendance records are kept and their preparation supervised in such a manner as to prevent errors and abuses, then one can be assured that wages paid are based on hours actually worked. The use of “In” and “Out” cards, whereby employees indicate by punching a time clock their time of arrival and departure, is especially useful. Employee identification cards or badges can be very helpful in giving additional assurance. Employee identification cards and badges can also contain bar codes that can be used by electronic scanners to account for employee time and control access to authorized locations. b. The requirement that the addition of names on the payroll be supported by written authorizations from the Personnel Department can help ensure that payroll checks are not being issued to fictitious persons. Endorsements on payroll checks can be compared with other samples of employees’ signatures. Many businesses directly deposit payroll checks to employee bank accounts, thereby eliminating the need for endorsement and check disbursement controls.

- If the vacation payment is probable and can be reasonably estimated, the vacation pay expense should be recorded during the period in which the vacation privilege is earned.

- Employee life expectancies, expected employee retirement dates, employee turnover, employee compensation levels, and investment income on pension contributions are factors that influence the future pension obligation of an employer.

- To match revenues and expenses properly, the liability to cover product warranties should be recorded in the period during which the sale of the product is made.

- When the defective product is repaired, the repair costs would be recorded by debiting

Product Warranty Payable and crediting Cash, Supplies, or another appropriate account.

- Yes. Since the $5,000 is payable within one year, Company A should present it as a current liability at September 30.

PE 11–3A

Total wage payment $ 1,680.

00 Less: Federal income tax withholding 298.

Earnings subject to social security tax ($100,000 – $99,000)

Social security tax rate × 6% Social security tax 60. Medicare tax ($1,680 × 1.5%) 25.

Net pay $ 1,296. 29

2. 4 PE 11–3B

Total wage payment $ 600.

Less: Federal income tax withholding 65.

Earnings subject to social security tax 600. Social security tax rate × 6% Social security tax 36. Medicare tax ($600 × 1.5%) 9.

Net pay $ 489.

2. 5 PE 11–4A

Salaries Expense 21, Social Security Tax Payable 1, Medicare Tax Payable 315 Employees Federal Income Tax Payable 3, Salaries Payable 15,

2. 6 PE 11–4B

Salaries Expense 450, Social Security Tax Payable 25, Medicare Tax payable 6, Employees Federal Income Tax Payable 89, Retirement Savings Deductions Payable 27, Salaries Payable 301,

PE 11–5A

Payroll Tax Expense 1,980. Social Security Tax Payable 1,260. Medicare Tax Payable 315. State Unemployment Tax Payable 353.16* Federal Unemployment Tax Payable 52.32**

*$6,540 × 5.4% **$6,540 × 0.8%

2. 7 PE 11–5B

Payroll Tax Expense 33,178. Social Security Tax Payable 25,650. Medicare Tax Payable 6,750. State Unemployment Tax Payable 677.70* Federal Unemployment Tax Payable 100.40**

*$12,550 × 5.4% **$12,550 × 0.8%

2. 8 PE 11–6A

a. Vacation Pay Expense 17, Vacation Pay Payable 17, Vacation pay accrued for the period.

b. Pension Expense 12, Cash 12, To record pension contribution, 7% × $180,000.

2. 9 PE 11–6B

a. Vacation Pay Expense 52, Vacation Pay Payable 52, Vacation pay accrued for the period.

b. Pension Expense 123, Cash 100, Unfunded Pension Liability 23, To record pension cost and funding.

PE 11–7A

a.

Mar. 31Product Warranty Expense 39, Product Warranty Payable 39, To record warranty expense for March, 4.5% × $870,000.

b. Oct. 4Product Warranty Payable 520 Supplies 420 Wages Payable 100

2. 10 PE 11–7B

a. June 30Product Warranty Expense 24, Product Warranty Payable 24, To record warranty expense for June, 5% × $480,000.

b. Aug. 16Product Warranty Payable 90 Cash 90

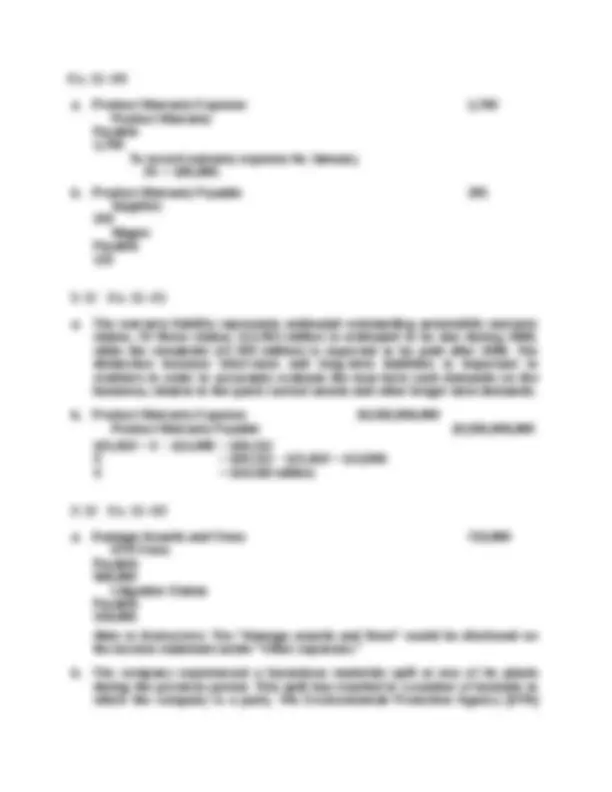

Ex. 11–

a. $120,000 × 6% × 90/360 = $1,800 for each alternative. b. (1) $120,000 simple-interest note: $120,000 proceeds (2) $120,000 discounted note: $120,000 – $1,800 interest = $118, proceeds c. Alternative (1) is more favorable to the borrower. This can be verified by comparing the effective interest rates for each loan as follows: Situation (1): 6% effective interest rate ($1,800 × 360/90) / $120,000 = 6% Situation (2): 6.09% effective interest rate ($1,800 × 360/90) / $118,200 = 6.09% The effective interest rate is higher for the second loan because the creditor lent only $118,200 in return for $1,800 interest over 90 days. In the simple- interest loan, the creditor must lend $120,000 for 90 days to earn the same $1,800 interest.

3. 2 Ex. 11–

a. Accounts Payable 15, Notes Payable 15,

b. Notes Payable 15, Interest Expense 175* Cash 15,

*$15,000 × 7% × 60/360 = $

3. 3 Ex. 11–

a. Accounts Payable 78, Interest Expense 1,600* Notes Payable 80,

*$80,000 × 8% × 90/

b. Notes Payable 80, Cash 80,

Ex. 11–

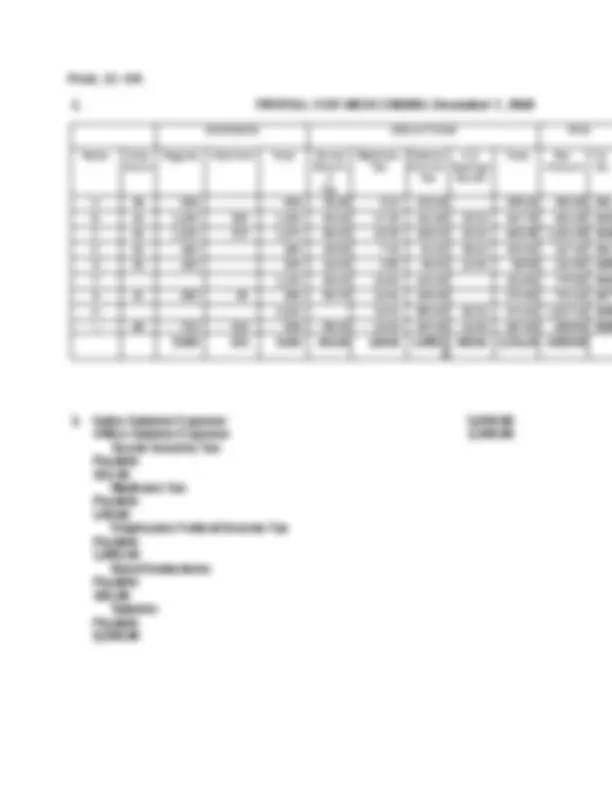

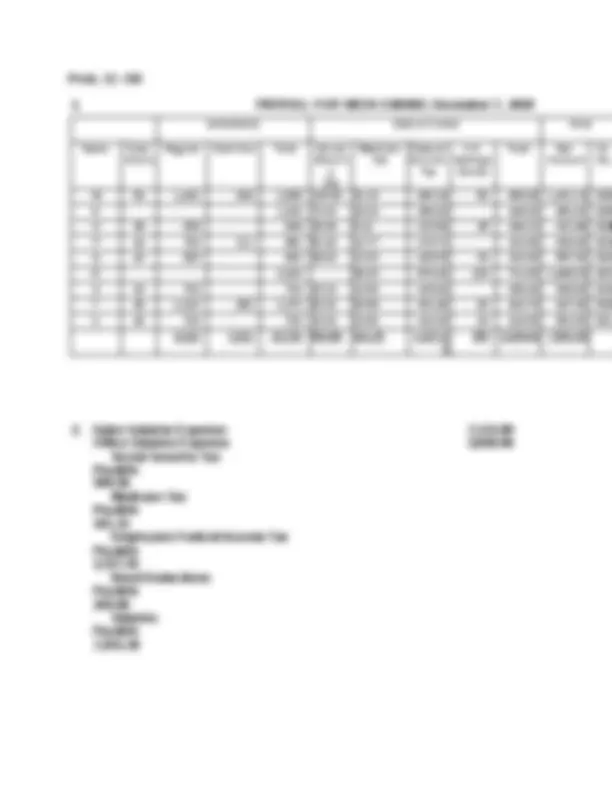

Computer Consultant Programmer^ Administrator Regular earnings $2,400.00 $1,600.00 $

Overtime earnings 480.00 165. 0 Gross pay $2,400.00$2,080.00^ $1,045. Less: Social security tax $ 0.00^1 $ 84.00 2 $ 62.70 3 Medicare tax 36.00 31.20 15. Federal income tax withheld^4 535.39 463.43 137. 0 $ 571.39 $ 578.63 $ 215. 8 Net pay $1,828.61$1,501.37 $ 829. (^1) Gross pay exceeds $100,000, so there is no social security tax withheld. (^2) [($100,000 – $98,600) × 6%] = $84. (^3) $1,045 × 6% = $62. (^4) The federal income tax withheld is determined from applying the calculation procedure associated with Exhibit 3 in the chapter, as follows:

Withholding supporting calculations: Computer Consultant Programmer^ Administrator Gross weekly pay $2,400.00 $2,080.00 $1,

Number of withholding allowances 1 0 3 Multiplied by: Value of one allowance × $63.00 × $63.00 × $63. 0 Amount to be deducted $ 63.00 $ 0.00 $ 189. 0 Amount subject to withholding $2,337.00 $2,080.00^ $

Initial withholding from wage bracket in Exhibit 3 $ 275.55 $ 275.55 $ 78.

Plus: Bracket percentage over bracket excess 259.84 5 187.88 6 59.00 7 Amount

withheld $ 535.39 $^ 463.43^ $^ 137. 0

(^5) 28% × ($2,337 – $1,409)

(^6) 28% × ($2,080 – $1,409) (^7) 25% × ($856 – $620)

Medicare Tax Payable 3, Employees Income Tax Payable 46, Medical Insurance Payable 7, Union Dues Payable 2, Salaries Payable 184,

c. Salaries Payable 184, Cash 184,

d. The amount of social security tax withheld, $15,250, is $350 less than 6.0% of the total earnings of $260,000. This indicates that the cumulative earnings of some employees exceed $100,000. Therefore, it is unlikely that this payroll was paid during the first few weeks of the calendar year.

State Unemployment Tax Payable 1,352*

- Ex. 11– - a. Social security tax (6% × $350,000) $21, - Medicare tax (1.5% × $420,000) 6, - State unemployment (4.3% × $14,000) - Federal unemployment (0.8% × $14,000) - $28, - b. Payroll Tax Expense 28, - Social Security Tax Payable 21, - Medicare Tax Payable 6, - State Unemployment Tax Payable - Federal Unemployment Tax Payable

- 6 Ex. 11–

- a. Salaries Expense 690, - Social Security Tax Payable 32, - Medicare Tax Payable 10, - Employees Federal Income Tax Payable 138, - Salaries Payable 508,

- b. Payroll Tax Expense 44, - Social Security Tax Payable 32, - Medicare Tax Payable 10,

- 5.2% × $26, Federal Unemployment Tax Payable 208*

- **0.8% × $26,