Contemporary Financial

Management

Chapter 3:

Evaluating and Forecasting Financial

Performance

Docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

This chapter from contemporary financial management explores financial statement analysis techniques using financial ratios. Ratios are essential tools for management, credit managers, and investors to assess a company's financial health. However, it's crucial to remember that ratios should be compared to industry peers and analyzed over time. Various types of ratios, including liquidity, asset management, financial leverage, profitability, market-based, and dividend policy ratios. Additionally, it discusses major financial statements and abbreviations used in the chapter.

Typology: Slides

1 / 10

This page cannot be seen from the preview

Don't miss anything!

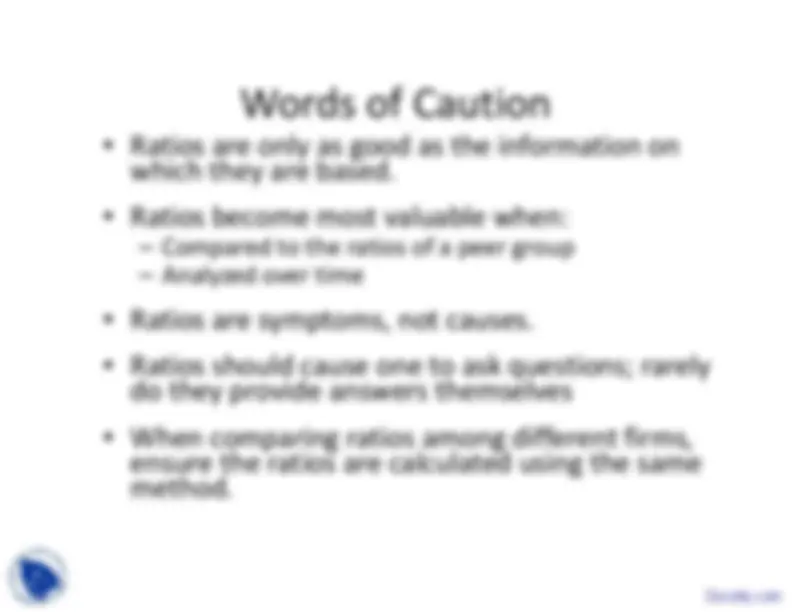

Ratios are only as good as the information onwhich they are based.

Ratios become most valuable when: - Compared to the ratios of a peer group - Analyzed over time - Ratios are symptoms, not causes. - Ratios should cause one to ask questions; rarelydo they provide answers themselves - When comparing ratios among different firms,ensure the ratios are calculated using the samemethod.

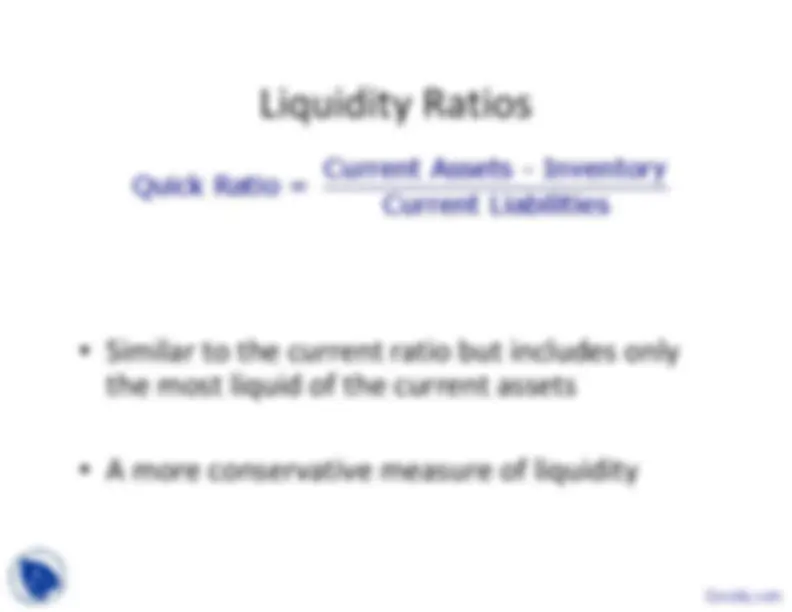

Liquidity

Asset management - Financial leverage - Profitability - Market-based - Dividend policy

EBIT – Earnings Before Interest & Taxes - ROI – Return on Investment - ROE – Return on Equity - P/E Ratio – Price to Earnings Ratio - EAT – Earnings After Tax - r – Return on total capital - k – Cost of capital

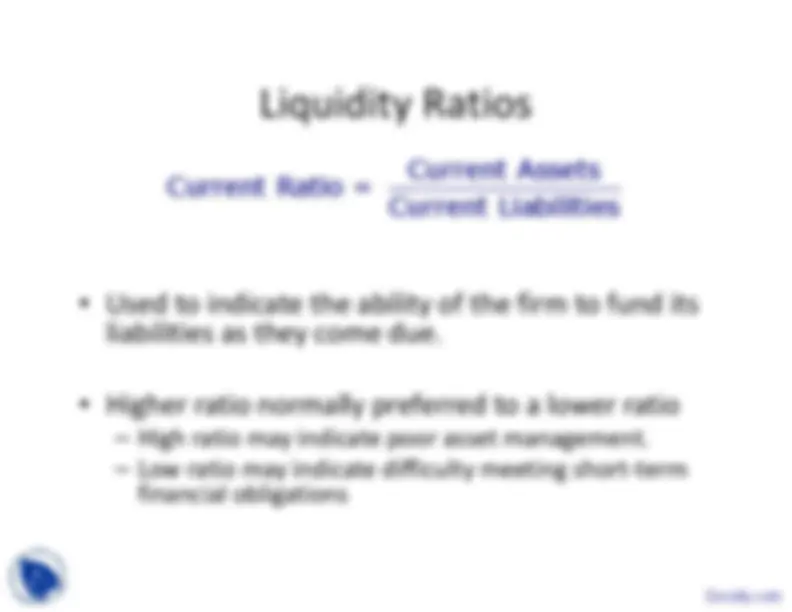

Used to indicate the ability of the firm to fund itsliabilities as they come due.

Higher ratio normally preferred to a lower ratio - High ratio may indicate poor asset management. - Low ratio may indicate difficulty meeting short-termfinancial obligations Current Assets Current Ratio = Current Liabilities

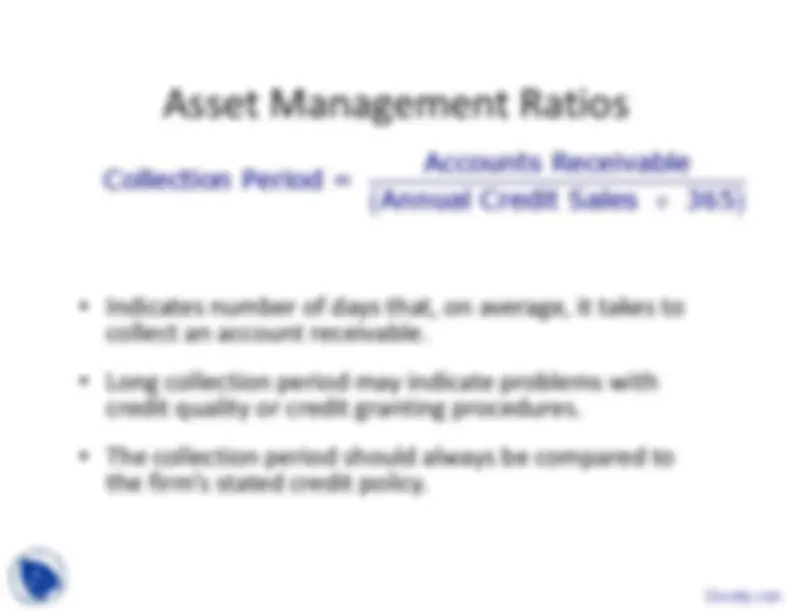

Indicates number of days that, on average, it takes tocollect an account receivable. - Long collection period may indicate problems withcredit quality or credit granting procedures. - The collection period should always be compared tothe firm’s stated credit policy.

÷ Accounts Receivable Collection Period = Annual Credit Sales 365 Docsity.com